Esker SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Esker’s strengths in AI-driven document automation and strong recurring revenue are balanced by integration challenges and competitive pressure; our full SWOT unpacks these dynamics, quantifies risks, and identifies concrete growth levers to inform investment or strategic moves—purchase the complete, editable report (Word + Excel) for actionable insights and expert commentary.

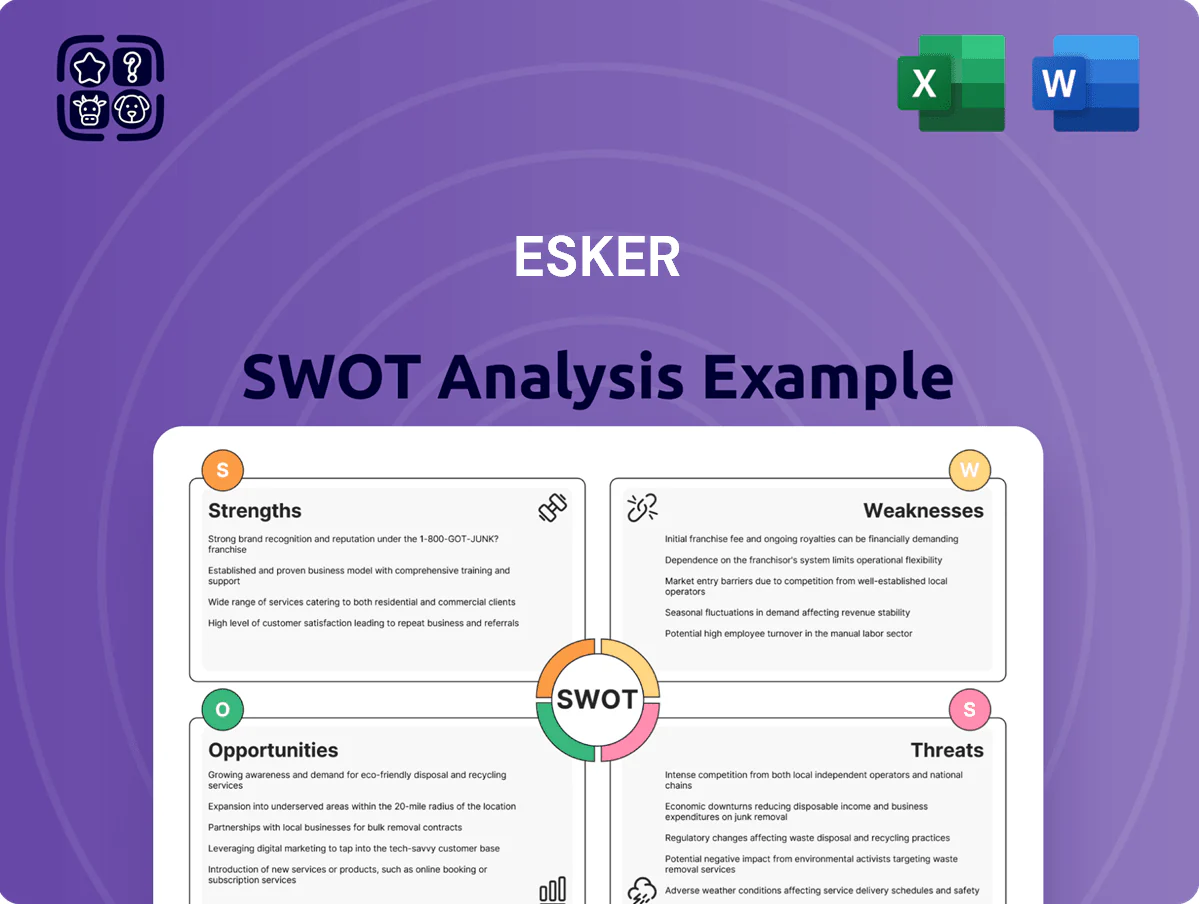

Strengths

High Recurring SaaS Revenue

Esker reports roughly 85% recurring revenue from cloud subscriptions as of FY2024 (year ending Dec 31, 2024), giving predictable cash flow that funds R&D and platform upgrades; recurring ARR rose ~18% YoY to about €120m in 2024.

Integrated AI Capabilities

Esker has embedded AI/ML into its Genesys platform to automate document workflows, cutting manual touchpoints in order-to-cash and procure-to-pay; clients report invoice processing time down by up to 60% and straight-through processing rates rising to ~85% (Esker FY2024 reporting).

Global Market Presence

Esker operates across North America, Europe and Asia-Pacific, serving over 8,000 customers in 50+ countries and generating €181.5m revenue in 2023, which underpins its global footprint. This presence lets Esker standardize document automation across multiple regulatory and linguistic environments for multinational clients. Geographic diversification also spreads risk—roughly 38% of 2023 revenue came from the Americas, 52% from Europe, 10% from APAC—helping hedge local downturns.

Comprehensive O2C and P2P Suite

Esker provides a unified cloud platform that manages the full lifecycle of accounts payable (AP) and accounts receivable (AR), delivering end-to-end visibility into cash flow and working capital; as of FY2024 Esker processed over €6.5 billion in document value annually, underscoring scale.

This single source of truth simplifies month-end close, reduces DSO (days sales outstanding) by up to 20% in customer cases, and positions Esker as a key partner for CFOs seeking automation and cash optimization.

- Unified AP+AR cloud platform

- €6.5B+ documents processed in FY2024

- Up to 20% DSO reduction in reported cases

- Improves cash flow visibility and working capital

Strong Financial Resilience

- 2024 adjusted operating margin ~18.5%

- Net cash €58M at FY 2024

- Private equity injections Q4 2024, Q1 2025

- Funds R&D and tactical acquisitions

Esker: 85% recurring ARR €120m, AI-driven 85% STP, €181.5m revenue, €58m net cash

Esker’s 85% recurring cloud revenue (ARR ~€120m, +18% YoY FY2024) funds R&D; embedded AI/ML boosts STP to ~85% and cuts invoice time ~60% (FY2024). Global footprint: 8,000+ customers, €181.5m revenue 2023, €6.5B+ documents processed FY2024; adjusted op. margin ~18.5% and net cash €58m at FY2024.

| Metric | Value |

|---|---|

| Recurring revenue | ~85% |

| ARR FY2024 | €120m |

| Revenue 2023 | €181.5m |

| Docs processed FY2024 | €6.5B+ |

| Adj. op. margin 2024 | ~18.5% |

| Net cash FY2024 | €58m |

What is included in the product

Provides a clear SWOT framework analyzing Esker’s strategic business environment by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping future growth.

Offers a focused SWOT snapshot of Esker to quickly identify strengths, weaknesses, opportunities, and threats for rapid strategic alignment and decision-making.

Weaknesses

Dependency on Transaction Volumes

High Competition from ERP Vendors

Esker faces strong competition from ERP giants like SAP and Oracle, which in 2024 rolled out expanded native automation—SAP reported a 12% rise in cloud ERP automation adoption—pushing customers toward single-vendor stacks. Esker’s best-of-breed features typically outperform ERP modules on accuracy and throughput, but surveys show 38% of firms prioritize vendor consolidation over feature depth. Esker must keep proving measurable ROI versus standard ERP capabilities.

Complex Implementation Cycles

Implementing Esker’s automation suite in large or legacy-heavy firms often stretches beyond 9–12 months, per vendor case studies, delaying ROI and tying up IT resources.

Such prolonged integrations can raise initial deployment costs by an estimated 15–25%, based on comparable SaaS finance-automation projects in 2024.

Streamlining onboarding—reducing touchpoints and standardizing connectors—remains key to cutting time-to-value and protecting customer satisfaction.

Geographic Revenue Concentration

Despite global operations, Esker reported about 72% of 2024 revenue from Europe and North America (Esker annual report 2024), leaving it vulnerable to EU/US regulatory shifts and regional recessions.

Concentration risks include GDPR-like compliance costs and a 2023–24 FX-adjusted revenue dip of 4% in Europe; expanding in APAC and LATAM—where cloud SaaS spend grew ~18% in 2024—would rebalance exposure.

- 72% revenue from Europe/North America (2024)

- 4% regional revenue dip 2023–24 (FX-adjusted)

- APAC/LATAM cloud spend +18% (2024)

Limited Brand Awareness in Small Business

- High ARPU (~€100k) limits SMB fit

- 2024 revenue €162.6M shows modest SMB share

- SMBs = ~90% of global firms, largely untapped

- Competitors gain share with tiered/entry offers

High revenue volatility, regional concentration & costly long implementations threaten growth

| Metric | Value |

|---|---|

| Consumption-linked ARR | 46% (FY2024) |

| 2024 revenue | €162.6M |

| Regional concentration | 72% Europe/North America (2024) |

| Avg deal size | ~€100k ARR |

| Implementation time | 9–12 months |

| Implementation cost uplift | 15–25% |

Same Document Delivered

Esker SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real excerpt included in your download. Buy now to unlock the complete, editable version with full detail and structured insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Esker’s strengths in AI-driven document automation and strong recurring revenue are balanced by integration challenges and competitive pressure; our full SWOT unpacks these dynamics, quantifies risks, and identifies concrete growth levers to inform investment or strategic moves—purchase the complete, editable report (Word + Excel) for actionable insights and expert commentary.

Strengths

High Recurring SaaS Revenue

Esker reports roughly 85% recurring revenue from cloud subscriptions as of FY2024 (year ending Dec 31, 2024), giving predictable cash flow that funds R&D and platform upgrades; recurring ARR rose ~18% YoY to about €120m in 2024.

Integrated AI Capabilities

Esker has embedded AI/ML into its Genesys platform to automate document workflows, cutting manual touchpoints in order-to-cash and procure-to-pay; clients report invoice processing time down by up to 60% and straight-through processing rates rising to ~85% (Esker FY2024 reporting).

Global Market Presence

Esker operates across North America, Europe and Asia-Pacific, serving over 8,000 customers in 50+ countries and generating €181.5m revenue in 2023, which underpins its global footprint. This presence lets Esker standardize document automation across multiple regulatory and linguistic environments for multinational clients. Geographic diversification also spreads risk—roughly 38% of 2023 revenue came from the Americas, 52% from Europe, 10% from APAC—helping hedge local downturns.

Comprehensive O2C and P2P Suite

Esker provides a unified cloud platform that manages the full lifecycle of accounts payable (AP) and accounts receivable (AR), delivering end-to-end visibility into cash flow and working capital; as of FY2024 Esker processed over €6.5 billion in document value annually, underscoring scale.

This single source of truth simplifies month-end close, reduces DSO (days sales outstanding) by up to 20% in customer cases, and positions Esker as a key partner for CFOs seeking automation and cash optimization.

- Unified AP+AR cloud platform

- €6.5B+ documents processed in FY2024

- Up to 20% DSO reduction in reported cases

- Improves cash flow visibility and working capital

Strong Financial Resilience

- 2024 adjusted operating margin ~18.5%

- Net cash €58M at FY 2024

- Private equity injections Q4 2024, Q1 2025

- Funds R&D and tactical acquisitions

Esker: 85% recurring ARR €120m, AI-driven 85% STP, €181.5m revenue, €58m net cash

Esker’s 85% recurring cloud revenue (ARR ~€120m, +18% YoY FY2024) funds R&D; embedded AI/ML boosts STP to ~85% and cuts invoice time ~60% (FY2024). Global footprint: 8,000+ customers, €181.5m revenue 2023, €6.5B+ documents processed FY2024; adjusted op. margin ~18.5% and net cash €58m at FY2024.

| Metric | Value |

|---|---|

| Recurring revenue | ~85% |

| ARR FY2024 | €120m |

| Revenue 2023 | €181.5m |

| Docs processed FY2024 | €6.5B+ |

| Adj. op. margin 2024 | ~18.5% |

| Net cash FY2024 | €58m |

What is included in the product

Provides a clear SWOT framework analyzing Esker’s strategic business environment by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping future growth.

Offers a focused SWOT snapshot of Esker to quickly identify strengths, weaknesses, opportunities, and threats for rapid strategic alignment and decision-making.

Weaknesses

Dependency on Transaction Volumes

High Competition from ERP Vendors

Esker faces strong competition from ERP giants like SAP and Oracle, which in 2024 rolled out expanded native automation—SAP reported a 12% rise in cloud ERP automation adoption—pushing customers toward single-vendor stacks. Esker’s best-of-breed features typically outperform ERP modules on accuracy and throughput, but surveys show 38% of firms prioritize vendor consolidation over feature depth. Esker must keep proving measurable ROI versus standard ERP capabilities.

Complex Implementation Cycles

Implementing Esker’s automation suite in large or legacy-heavy firms often stretches beyond 9–12 months, per vendor case studies, delaying ROI and tying up IT resources.

Such prolonged integrations can raise initial deployment costs by an estimated 15–25%, based on comparable SaaS finance-automation projects in 2024.

Streamlining onboarding—reducing touchpoints and standardizing connectors—remains key to cutting time-to-value and protecting customer satisfaction.

Geographic Revenue Concentration

Despite global operations, Esker reported about 72% of 2024 revenue from Europe and North America (Esker annual report 2024), leaving it vulnerable to EU/US regulatory shifts and regional recessions.

Concentration risks include GDPR-like compliance costs and a 2023–24 FX-adjusted revenue dip of 4% in Europe; expanding in APAC and LATAM—where cloud SaaS spend grew ~18% in 2024—would rebalance exposure.

- 72% revenue from Europe/North America (2024)

- 4% regional revenue dip 2023–24 (FX-adjusted)

- APAC/LATAM cloud spend +18% (2024)

Limited Brand Awareness in Small Business

- High ARPU (~€100k) limits SMB fit

- 2024 revenue €162.6M shows modest SMB share

- SMBs = ~90% of global firms, largely untapped

- Competitors gain share with tiered/entry offers

High revenue volatility, regional concentration & costly long implementations threaten growth

| Metric | Value |

|---|---|

| Consumption-linked ARR | 46% (FY2024) |

| 2024 revenue | €162.6M |

| Regional concentration | 72% Europe/North America (2024) |

| Avg deal size | ~€100k ARR |

| Implementation time | 9–12 months |

| Implementation cost uplift | 15–25% |

Same Document Delivered

Esker SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real excerpt included in your download. Buy now to unlock the complete, editable version with full detail and structured insights.