EssilorLuxottica Boston Consulting Group Matrix

See the Bigger Picture

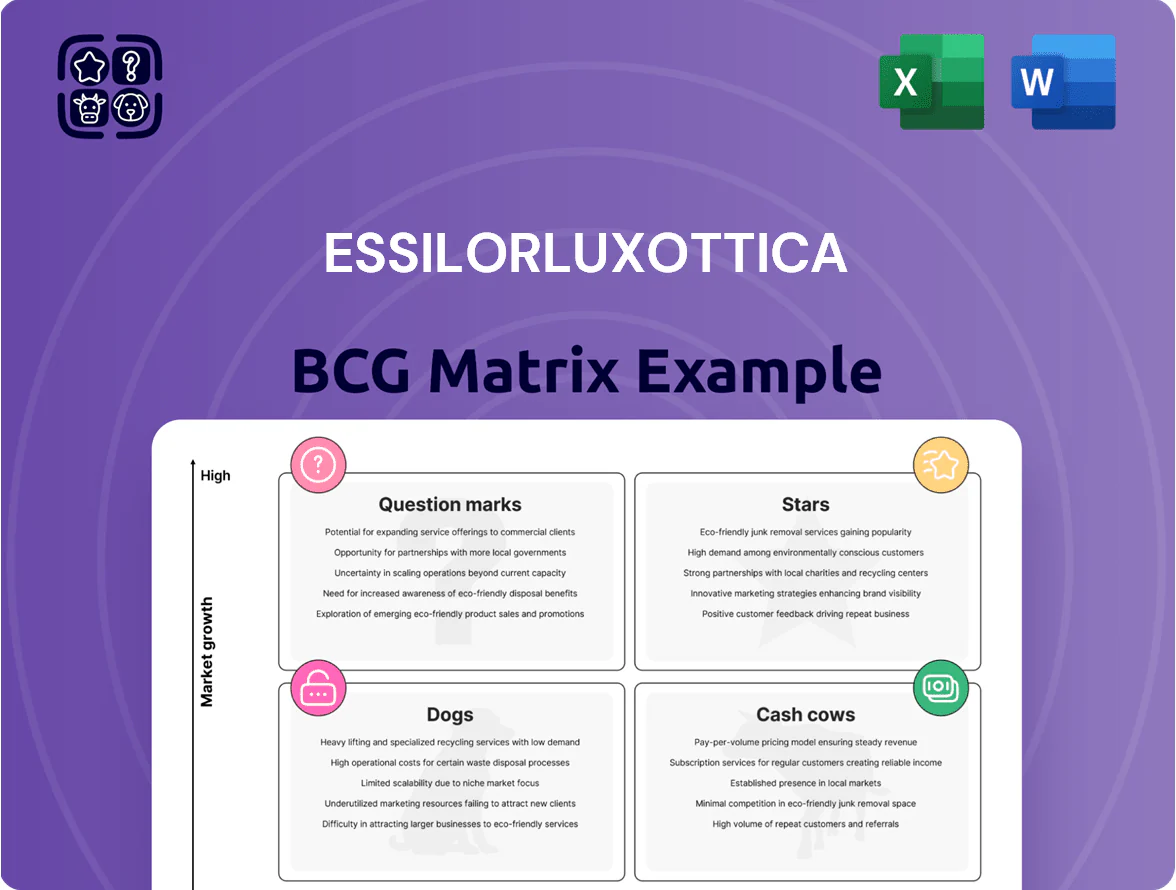

EssilorLuxottica’s BCG Matrix preview highlights how its eyewear brands and lens technologies likely span Stars, Cash Cows, Question Marks, and Dogs amid shifting consumer trends and vertical integration advantages; understanding these placements helps prioritize investment and product strategy. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and competitive moves with confidence.

Stars

Smart Eyewear and Ray-Ban Meta

The Ray-Ban Meta collaboration made smart eyewear a high-growth leader in wearables by late 2025, with estimated 2025 category share ~42% and unit sales ~1.2M devices, driven by Ray-Ban’s cultural reach and Meta’s software stack.

These products command dominant share in the nascent smart-eyewear segment while capturing premium ASPs near €350 and contributing an estimated €420M to EssilorLuxottica 2025 revenues.

To hold leadership against Qualcomm- and Apple-led rivals, continued capex for AI integration and hardware miniaturization—R&D spend uptick ~18% YoY—is required.

Direct-to-Consumer E-commerce Platforms

Direct-to-consumer e-commerce for Ray-Ban, Oakley, and Sunglass Hut drives double-digit growth: online sales rose ~28% YoY in 2024, reaching an estimated €3.1bn of EssilorLuxottica’s revenue mix, capturing ~22% of global eyewear e-commerce (2024 Euromonitor).

These channels yield higher gross margins (mid-60s%) versus wholesale, and are key to a 12–15% CAGR forecast to 2028; heavy capex targets AR virtual try-on and logistics, with €450m committed in 2024–25 to sustain scale.

Stellest Myopia Control Lenses

Stellest myopia-control lenses hold a leading market share in fast-growing myopia management, with EssilorLuxottica reporting >30% share in China and double-digit share in Europe by 2024 as myopia prevalence climbed to ~50% in East Asia among young adults (WHO/2024 estimates).

Luxury License Portfolio Expansion

Luxury License Portfolio Expansion sits in the BCG Matrix as a Star: high market share in a fast-growing ultra-luxury eyewear segment, driven by acquisitions and license renewals like Brunello Cucinelli (renewed 2024) and Swarovski, with segment revenue rising ~18% CAGR 2021–2024 to about €1.1bn in 2024.

By using EssilorLuxottica’s dominant manufacturing and global retail network, the group captures ~30–35% share of branded ultra-luxury eyewear, though brands demand elevated marketing spend—often 12–18% of sales—to keep prestige and win affluent buyers in emerging markets.

- Star: high share, high growth (~18% CAGR)

- Revenue: ~€1.1bn luxury segment (2024)

- Market share: ~30–35% ultra-luxury eyewear

- Promo spend: ~12–18% of sales

Advanced Eye Examination Equipment

Advanced Eye Examination Equipment sits in Stars: instrument division growth ~12% CAGR 2021–25 as global retailers upgrade to digital, AI-driven diagnostics; EssilorLuxottica held ~28% market share in optical instruments in 2024, providing core infrastructure for primary vision care.

Company invested €420M in R&D for medical devices in 2024 to fund AI diagnostics and maintain a technical moat; device sales grew 18% YoY in H1 2025, signaling strong market uptake.

- ~12% CAGR 2021–25

- ~28% market share (2024)

- €420M R&D (2024)

- +18% device sales H1 2025

High-growth eyewear portfolio: €4.03bn revenue, 12–18% CAGRs, €870m capex/R&D

Stars: Ray-Ban Meta smart eyewear, DTC e‑commerce, Stellest lenses, luxury licenses, and advanced instruments show high share and high growth—combined 2024–25 revenue ~€4.03bn, segment CAGRs 12–18%, and targeted capex/R&D ~€870m (2024–25).

| Asset | 2024–25 rev (€M) | Market share | CAGR | Capex/R&D (€M) |

|---|---|---|---|---|

| Smart eyewear | 420 | ~42% | — | — |

| DTC e‑com | 3100 | ~22% | ~28% YoY | 450 |

| Stellest | — | >30% CN | — | — |

| Luxury | 1100 | 30–35% | ~18% | — |

| Instruments | — | ~28% | ~12% | 420 |

What is included in the product

Comprehensive BCG Matrix for EssilorLuxottica: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment recommendations.

One-page BCG Matrix placing EssilorLuxottica units into quadrants for quick strategic decisions and investor briefings.

Cash Cows

Ray-Ban Heritage Collections

Ray-Ban remains the world’s most recognized eyewear brand, holding roughly 20–25% share of the global sunglasses market (estimated $14.6B in 2024), in a mature segment growing ~3–4% CAGR; brand strength converts to predictable, high-margin sales.

Its Heritage collections generate sizable free cash flow—Luxottica reported €4.2B operating cash flow in 2024—requiring low incremental marketing spend to sustain awareness, so cash funds R&D in smart eyewear and funds steady dividends (2024 dividend yield ~1.8%).

Varilux Progressive Lenses

Varilux, the pioneer in progressive lenses, dominates the mature global ophthalmic lens market for the 50+ cohort, holding an estimated 35–40% share of premium progressive sales in 2024 and generating roughly €650–700 million in annual gross margin for EssilorLuxottica’s lens division.

High brand loyalty and premium pricing sustain 20–25% EBITDA margins, producing steady cash inflows used to fund R&D and retail expansion.

With tech mature, management prioritizes manufacturing efficiency—automation and lean lines lifted lens output 8% in 2023—plus small optical improvements to maximize cash extraction.

Oakley Performance Eyewear

Oakley Performance Eyewear dominates the global sports eyewear segment, which McKinsey estimated at about $5.6bn in 2024, with Oakley holding roughly 25% share in premium performance frames and lenses.

Strong patents on Prizm lens tech and ~200 athlete endorsements drive 18–22% gross margins and stable unit sales, per EssilorLuxottica 2024 disclosures.

As a BCG Cash Cow, Oakley generates consistent free cash flow; 2024 segment-level EBIT margin stayed near 16%, needing moderate marketing spend to defend share.

Sunglass Hut Retail Network

Sunglass Hut operates over 3,000 stores globally (2024), holding clear leadership in specialty sun retail within a mature market; its scale drives consistent high-volume sales across proprietary labels and licensed brands, making it a classic Cash Cow in EssilorLuxottica’s BCG matrix.

The network generated an estimated €1.1–1.3 billion in retail sales (2023–2024 range) and delivers strong free cash flow, with capex focusing on store refreshes and digital upgrades rather than rapid geographic expansion.

- 3,000+ stores worldwide (2024)

- Estimated €1.1–1.3B retail sales (2023–24)

- High gross margins on branded sunglasses

- Capex mainly for renovations, not expansion

Crizal Anti-Reflective Coatings

Crizal anti-reflective coatings are a market leader in mature lens coatings, delivering premium durability and clarity; they support EssilorLuxottica’s high market share in prescription lenses, contributing steady gross margins—Crizal generated an estimated €400–€450m in retail revenue for ELC brands in 2024, per sector estimates.

Low annual market growth (~1–2% CAGR) pushes Crizal to prioritize operational excellence and cost control, freeing cash to fund high-growth R&D and premium lens launches across 2025–2026.

- Market position: dominant leader in AR coatings

- Revenue: ~€400–€450m retail est. (2024)

- Growth: coating market ~1–2% CAGR

- Strategy: efficiency to fund R&D and new lens tech

EssilorLuxottica’s Cash Cows: Ray‑Ban, Varilux, Oakley, Sunglass Hut & Crizal

EssilorLuxottica cash cows: Ray-Ban (20–25% sunglasses share; $14.6B market 2024; high margins), Varilux (35–40% premium progressive share; €650–700M gross margin 2024), Oakley (≈25% premium sports share; €5.6B segment 2024; 18–22% gross margins), Sunglass Hut (3,000+ stores; €1.1–1.3B sales 2023–24), Crizal (€400–450M est. 2024; 1–2% CAGR).

| Brand | 2024 metric |

|---|---|

| Ray-Ban | 20–25% share; $14.6B market |

| Varilux | 35–40% premium; €650–700M GM |

| Oakley | ≈25% premium; 18–22% GM |

| Sunglass Hut | 3,000+ stores; €1.1–1.3B sales |

| Crizal | €400–450M; 1–2% CAGR |

Full Transparency, Always

EssilorLuxottica BCG Matrix

The file you're previewing is the final EssilorLuxottica BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

EssilorLuxottica’s BCG Matrix preview highlights how its eyewear brands and lens technologies likely span Stars, Cash Cows, Question Marks, and Dogs amid shifting consumer trends and vertical integration advantages; understanding these placements helps prioritize investment and product strategy. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and competitive moves with confidence.

Stars

Smart Eyewear and Ray-Ban Meta

The Ray-Ban Meta collaboration made smart eyewear a high-growth leader in wearables by late 2025, with estimated 2025 category share ~42% and unit sales ~1.2M devices, driven by Ray-Ban’s cultural reach and Meta’s software stack.

These products command dominant share in the nascent smart-eyewear segment while capturing premium ASPs near €350 and contributing an estimated €420M to EssilorLuxottica 2025 revenues.

To hold leadership against Qualcomm- and Apple-led rivals, continued capex for AI integration and hardware miniaturization—R&D spend uptick ~18% YoY—is required.

Direct-to-Consumer E-commerce Platforms

Direct-to-consumer e-commerce for Ray-Ban, Oakley, and Sunglass Hut drives double-digit growth: online sales rose ~28% YoY in 2024, reaching an estimated €3.1bn of EssilorLuxottica’s revenue mix, capturing ~22% of global eyewear e-commerce (2024 Euromonitor).

These channels yield higher gross margins (mid-60s%) versus wholesale, and are key to a 12–15% CAGR forecast to 2028; heavy capex targets AR virtual try-on and logistics, with €450m committed in 2024–25 to sustain scale.

Stellest Myopia Control Lenses

Stellest myopia-control lenses hold a leading market share in fast-growing myopia management, with EssilorLuxottica reporting >30% share in China and double-digit share in Europe by 2024 as myopia prevalence climbed to ~50% in East Asia among young adults (WHO/2024 estimates).

Luxury License Portfolio Expansion

Luxury License Portfolio Expansion sits in the BCG Matrix as a Star: high market share in a fast-growing ultra-luxury eyewear segment, driven by acquisitions and license renewals like Brunello Cucinelli (renewed 2024) and Swarovski, with segment revenue rising ~18% CAGR 2021–2024 to about €1.1bn in 2024.

By using EssilorLuxottica’s dominant manufacturing and global retail network, the group captures ~30–35% share of branded ultra-luxury eyewear, though brands demand elevated marketing spend—often 12–18% of sales—to keep prestige and win affluent buyers in emerging markets.

- Star: high share, high growth (~18% CAGR)

- Revenue: ~€1.1bn luxury segment (2024)

- Market share: ~30–35% ultra-luxury eyewear

- Promo spend: ~12–18% of sales

Advanced Eye Examination Equipment

Advanced Eye Examination Equipment sits in Stars: instrument division growth ~12% CAGR 2021–25 as global retailers upgrade to digital, AI-driven diagnostics; EssilorLuxottica held ~28% market share in optical instruments in 2024, providing core infrastructure for primary vision care.

Company invested €420M in R&D for medical devices in 2024 to fund AI diagnostics and maintain a technical moat; device sales grew 18% YoY in H1 2025, signaling strong market uptake.

- ~12% CAGR 2021–25

- ~28% market share (2024)

- €420M R&D (2024)

- +18% device sales H1 2025

High-growth eyewear portfolio: €4.03bn revenue, 12–18% CAGRs, €870m capex/R&D

Stars: Ray-Ban Meta smart eyewear, DTC e‑commerce, Stellest lenses, luxury licenses, and advanced instruments show high share and high growth—combined 2024–25 revenue ~€4.03bn, segment CAGRs 12–18%, and targeted capex/R&D ~€870m (2024–25).

| Asset | 2024–25 rev (€M) | Market share | CAGR | Capex/R&D (€M) |

|---|---|---|---|---|

| Smart eyewear | 420 | ~42% | — | — |

| DTC e‑com | 3100 | ~22% | ~28% YoY | 450 |

| Stellest | — | >30% CN | — | — |

| Luxury | 1100 | 30–35% | ~18% | — |

| Instruments | — | ~28% | ~12% | 420 |

What is included in the product

Comprehensive BCG Matrix for EssilorLuxottica: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment recommendations.

One-page BCG Matrix placing EssilorLuxottica units into quadrants for quick strategic decisions and investor briefings.

Cash Cows

Ray-Ban Heritage Collections

Ray-Ban remains the world’s most recognized eyewear brand, holding roughly 20–25% share of the global sunglasses market (estimated $14.6B in 2024), in a mature segment growing ~3–4% CAGR; brand strength converts to predictable, high-margin sales.

Its Heritage collections generate sizable free cash flow—Luxottica reported €4.2B operating cash flow in 2024—requiring low incremental marketing spend to sustain awareness, so cash funds R&D in smart eyewear and funds steady dividends (2024 dividend yield ~1.8%).

Varilux Progressive Lenses

Varilux, the pioneer in progressive lenses, dominates the mature global ophthalmic lens market for the 50+ cohort, holding an estimated 35–40% share of premium progressive sales in 2024 and generating roughly €650–700 million in annual gross margin for EssilorLuxottica’s lens division.

High brand loyalty and premium pricing sustain 20–25% EBITDA margins, producing steady cash inflows used to fund R&D and retail expansion.

With tech mature, management prioritizes manufacturing efficiency—automation and lean lines lifted lens output 8% in 2023—plus small optical improvements to maximize cash extraction.

Oakley Performance Eyewear

Oakley Performance Eyewear dominates the global sports eyewear segment, which McKinsey estimated at about $5.6bn in 2024, with Oakley holding roughly 25% share in premium performance frames and lenses.

Strong patents on Prizm lens tech and ~200 athlete endorsements drive 18–22% gross margins and stable unit sales, per EssilorLuxottica 2024 disclosures.

As a BCG Cash Cow, Oakley generates consistent free cash flow; 2024 segment-level EBIT margin stayed near 16%, needing moderate marketing spend to defend share.

Sunglass Hut Retail Network

Sunglass Hut operates over 3,000 stores globally (2024), holding clear leadership in specialty sun retail within a mature market; its scale drives consistent high-volume sales across proprietary labels and licensed brands, making it a classic Cash Cow in EssilorLuxottica’s BCG matrix.

The network generated an estimated €1.1–1.3 billion in retail sales (2023–2024 range) and delivers strong free cash flow, with capex focusing on store refreshes and digital upgrades rather than rapid geographic expansion.

- 3,000+ stores worldwide (2024)

- Estimated €1.1–1.3B retail sales (2023–24)

- High gross margins on branded sunglasses

- Capex mainly for renovations, not expansion

Crizal Anti-Reflective Coatings

Crizal anti-reflective coatings are a market leader in mature lens coatings, delivering premium durability and clarity; they support EssilorLuxottica’s high market share in prescription lenses, contributing steady gross margins—Crizal generated an estimated €400–€450m in retail revenue for ELC brands in 2024, per sector estimates.

Low annual market growth (~1–2% CAGR) pushes Crizal to prioritize operational excellence and cost control, freeing cash to fund high-growth R&D and premium lens launches across 2025–2026.

- Market position: dominant leader in AR coatings

- Revenue: ~€400–€450m retail est. (2024)

- Growth: coating market ~1–2% CAGR

- Strategy: efficiency to fund R&D and new lens tech

EssilorLuxottica’s Cash Cows: Ray‑Ban, Varilux, Oakley, Sunglass Hut & Crizal

EssilorLuxottica cash cows: Ray-Ban (20–25% sunglasses share; $14.6B market 2024; high margins), Varilux (35–40% premium progressive share; €650–700M gross margin 2024), Oakley (≈25% premium sports share; €5.6B segment 2024; 18–22% gross margins), Sunglass Hut (3,000+ stores; €1.1–1.3B sales 2023–24), Crizal (€400–450M est. 2024; 1–2% CAGR).

| Brand | 2024 metric |

|---|---|

| Ray-Ban | 20–25% share; $14.6B market |

| Varilux | 35–40% premium; €650–700M GM |

| Oakley | ≈25% premium; 18–22% GM |

| Sunglass Hut | 3,000+ stores; €1.1–1.3B sales |

| Crizal | €400–450M; 1–2% CAGR |

Full Transparency, Always

EssilorLuxottica BCG Matrix

The file you're previewing is the final EssilorLuxottica BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.