The Estée Lauder Companies Porter's Five Forces Analysis

Don't Miss the Bigger Picture

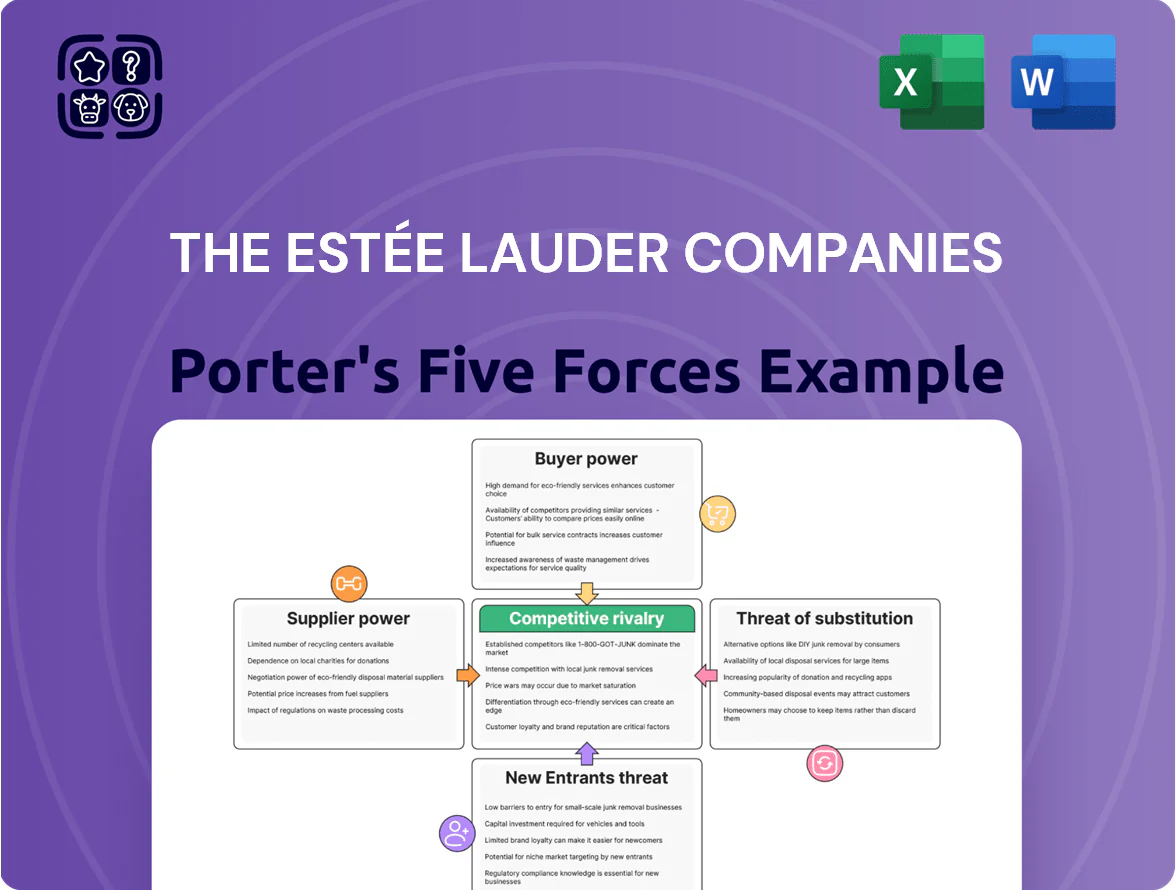

Estée Lauder operates in a high-stakes beauty market where brand power and innovation blunt supplier leverage but intense rivalry and digital-savvy challengers heighten competitive pressure.

Buyers wield growing influence via omnichannel access and premium expectations, while substitutes and regulatory shifts create strategic risks that require nimble differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore The Estée Lauder Companies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Sourcing and Raw Material Diversity

Estée Lauder sources ingredients and packaging from a global supplier base of thousands, lowering dependence on any single vendor and cutting procurement risk.

Multiple vendors for chemicals, fragrances, and containers keep a competitive bidding environment; in 2024 the company reported supply‑chain spend of $6.4B, enabling price negotiation leverage.

This supplier diversification limits supplier pricing power, so suppliers cannot easily raise prices without losing business or volume to competitors.

High Volume Purchasing Power

As one of the largest prestige beauty conglomerates, Estée Lauder Companies (ELC) achieved net sales of $16.2 billion in fiscal 2024, giving it strong economies of scale; this volume makes ELC a critical buyer for raw-material and packaging suppliers.

Massive order sizes and multi-year contracts let ELC negotiate lower unit costs; suppliers commonly offer 5–15% preferential pricing and priority lead times to retain ELC’s stable, high-value business.

Low Switching Costs for Standard Inputs

For many basic ingredients—emollients, pigments, ethanol—switching costs are low, letting The Estée Lauder Companies shift to alternate vendors quickly; in 2024 Estée Lauder reported ~9% COGS inflation but maintained gross margin at 72% by sourcing flexibility.

Specialized Ingredients and Intellectual Property

Bargaining power rises modestly for suppliers of proprietary actives; rare botanical extracts and patented compounds often come from few certified vendors, raising supplier concentration risk.

Estée Lauder spent about 10% of 2024 R&D and procurement on specialty ingredients, so it forms multi-year contracts and joint-development deals to secure exclusivity and pricing stability.

- Few certified suppliers = higher leverage

- 10% of 2024 R&D/procurement tied to specialty actives

- Use multi-year contracts and JVs for supply security

Threat of Backward Integration

Estée Lauder has the cash and technical capacity to internalize more raw-material production if supplier prices rise; year-end 2024 cash and equivalents were about $3.2 billion, supporting CAPEX for backward integration.

This credible threat lowers supplier bargaining power in prestige beauty, since suppliers risk losing volume to in‑house sourcing and long-term contracts worth billions across brands like MAC and La Mer.

Ongoing investment in R&D and owned manufacturing (over $400 million R&D spend in FY2024) keeps ELC defensive against price spikes and supply shocks.

- Cash ≈ $3.2B (YE 2024)

- R&D ≈ $400M (FY2024)

- Brands: MAC, La Mer, Clinique

Estée Lauder’s $6.4B spend and $3.2B cash boost supplier power and integration

Strong supplier diversification and $6.4B supply‑chain spend in 2024 give Estée Lauder high buying power; YE cash ~$3.2B and FY2024 R&D ~$400M support backward integration, while specialty actives (≈10% of R&D/procurement) raise supplier leverage for rare ingredients.

| Metric | 2024 |

|---|---|

| Supply‑chain spend | $6.4B |

| Net sales | $16.2B |

| YE cash | $3.2B |

| R&D | $400M |

| Specialty actives | ≈10% |

What is included in the product

Tailored exclusively for The Estée Lauder Companies, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, supplier power, and market entry risks, highlighting disruptive substitutes and strategic defenses that shape the company's pricing and profitability.

A concise Porter's Five Forces one-sheet for Estée Lauder—instantly shows competitive pressures, supplier/buyer leverage, and threat levels to streamline strategic decisions.

Customers Bargaining Power

Retailer Consolidation and Influence

Low Switching Costs for End Consumers

Individual consumers face almost zero financial cost switching from Estée Lauder to rivals like L'Oréal or Shiseido, driving high churn risk; NielsenIQ 2024 data shows 28% of prestige buyers tried a new premium brand in the past year. Brand loyalty helps—Estée Lauder reports ~60% repeat purchase rate in key markets in 2023—but abundant high-quality alternatives forces heavy spend on R&D and emotional marketing: Estée Lauder spent $1.1B on advertising and $420M on product development in FY2024 to defend share.

Information Transparency and Social Influence

By 2025, social media reach and influencer reviews give buyers instant product and ingredient intel; 72% of US beauty shoppers consult influencers before purchase per McKinsey 2024, so preferences flip fast with viral trends.

This transparency raises buyer power for Estée Lauder: a single viral complaint can cut sales in a category by double digits within weeks, making reputation and consistent product performance critical.

Growth of Direct to Consumer Channels

Estée Lauder’s push into direct-to-consumer (DTC) channels—its e-commerce and ~600 freestanding stores as of FY2024—cuts third-party retailer leverage by raising company-controlled sales to about 35% of net sales in 2024, up from ~28% in 2019.

Direct sales boost gross margins (DTC often 5–10 percentage points higher), let EL capture first-party customer data for personalization, and act as a buffer vs. department store pricing and return demands.

- ~35% net sales via DTC in 2024

- ~600 freestanding stores worldwide

- DTC margin uplift ~5–10 p.p.

- First-party data improves targeting and loyalty

Price Sensitivity in the Prestige Segment

Prestige beauty often resists recessions, but 2023–2024 data show 28% of US consumers traded down to masstige (middle-market prestige) when premium benefits were unclear; in 2024 Estée Lauder Co. saw global net sales grow 6% to $18.5B but US prestige volume softness signaled price pushback.

High inflation and 2024 CPI at ~3.4% mean buyers may swap to masstige if value falls; Estée Lauder must prove superiority via R&D, new product launches, and elevated in-store/digital experiences to defend margins and justify premium pricing.

- 28% of consumers traded down (2023–24 survey)

- Estée Lauder 2024 net sales ~$18.5B, +6%

- 2024 US CPI ~3.4% increases price sensitivity

- Actions: innovate, elevate CX, defend premium margin

Estée Lauder Battles Buyer Power: DTC Gains Offset Rising Trade, Ad & R&D Costs

Buyers have strong leverage: retail consolidation (Sephora+Ulta ≈28% US prestige sales, 2024) and low switching costs force Estée Lauder into higher trade spend (trade up ~120 bps in 2024) and heavy marketing/product R&D (advertising $1.1B, R&D $420M FY2024). DTC growth to ~35% of net sales in 2024 and ~600 stores helps regain margin (DTC +5–10 p.p.) and first‑party data, but viral social trends (72% consult influencers, McKinsey 2024) keep buyer power high.

| Metric | 2024 |

|---|---|

| Net sales | $18.5B |

| DTC share | ~35% |

| Retailer share (Sephora+Ulta) | ~28% US |

| Ad spend | $1.1B |

| R&D | $420M |

Same Document Delivered

The Estée Lauder Companies Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for The Estée Lauder Companies you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Estée Lauder operates in a high-stakes beauty market where brand power and innovation blunt supplier leverage but intense rivalry and digital-savvy challengers heighten competitive pressure.

Buyers wield growing influence via omnichannel access and premium expectations, while substitutes and regulatory shifts create strategic risks that require nimble differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore The Estée Lauder Companies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Sourcing and Raw Material Diversity

Estée Lauder sources ingredients and packaging from a global supplier base of thousands, lowering dependence on any single vendor and cutting procurement risk.

Multiple vendors for chemicals, fragrances, and containers keep a competitive bidding environment; in 2024 the company reported supply‑chain spend of $6.4B, enabling price negotiation leverage.

This supplier diversification limits supplier pricing power, so suppliers cannot easily raise prices without losing business or volume to competitors.

High Volume Purchasing Power

As one of the largest prestige beauty conglomerates, Estée Lauder Companies (ELC) achieved net sales of $16.2 billion in fiscal 2024, giving it strong economies of scale; this volume makes ELC a critical buyer for raw-material and packaging suppliers.

Massive order sizes and multi-year contracts let ELC negotiate lower unit costs; suppliers commonly offer 5–15% preferential pricing and priority lead times to retain ELC’s stable, high-value business.

Low Switching Costs for Standard Inputs

For many basic ingredients—emollients, pigments, ethanol—switching costs are low, letting The Estée Lauder Companies shift to alternate vendors quickly; in 2024 Estée Lauder reported ~9% COGS inflation but maintained gross margin at 72% by sourcing flexibility.

Specialized Ingredients and Intellectual Property

Bargaining power rises modestly for suppliers of proprietary actives; rare botanical extracts and patented compounds often come from few certified vendors, raising supplier concentration risk.

Estée Lauder spent about 10% of 2024 R&D and procurement on specialty ingredients, so it forms multi-year contracts and joint-development deals to secure exclusivity and pricing stability.

- Few certified suppliers = higher leverage

- 10% of 2024 R&D/procurement tied to specialty actives

- Use multi-year contracts and JVs for supply security

Threat of Backward Integration

Estée Lauder has the cash and technical capacity to internalize more raw-material production if supplier prices rise; year-end 2024 cash and equivalents were about $3.2 billion, supporting CAPEX for backward integration.

This credible threat lowers supplier bargaining power in prestige beauty, since suppliers risk losing volume to in‑house sourcing and long-term contracts worth billions across brands like MAC and La Mer.

Ongoing investment in R&D and owned manufacturing (over $400 million R&D spend in FY2024) keeps ELC defensive against price spikes and supply shocks.

- Cash ≈ $3.2B (YE 2024)

- R&D ≈ $400M (FY2024)

- Brands: MAC, La Mer, Clinique

Estée Lauder’s $6.4B spend and $3.2B cash boost supplier power and integration

Strong supplier diversification and $6.4B supply‑chain spend in 2024 give Estée Lauder high buying power; YE cash ~$3.2B and FY2024 R&D ~$400M support backward integration, while specialty actives (≈10% of R&D/procurement) raise supplier leverage for rare ingredients.

| Metric | 2024 |

|---|---|

| Supply‑chain spend | $6.4B |

| Net sales | $16.2B |

| YE cash | $3.2B |

| R&D | $400M |

| Specialty actives | ≈10% |

What is included in the product

Tailored exclusively for The Estée Lauder Companies, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, supplier power, and market entry risks, highlighting disruptive substitutes and strategic defenses that shape the company's pricing and profitability.

A concise Porter's Five Forces one-sheet for Estée Lauder—instantly shows competitive pressures, supplier/buyer leverage, and threat levels to streamline strategic decisions.

Customers Bargaining Power

Retailer Consolidation and Influence

Low Switching Costs for End Consumers

Individual consumers face almost zero financial cost switching from Estée Lauder to rivals like L'Oréal or Shiseido, driving high churn risk; NielsenIQ 2024 data shows 28% of prestige buyers tried a new premium brand in the past year. Brand loyalty helps—Estée Lauder reports ~60% repeat purchase rate in key markets in 2023—but abundant high-quality alternatives forces heavy spend on R&D and emotional marketing: Estée Lauder spent $1.1B on advertising and $420M on product development in FY2024 to defend share.

Information Transparency and Social Influence

By 2025, social media reach and influencer reviews give buyers instant product and ingredient intel; 72% of US beauty shoppers consult influencers before purchase per McKinsey 2024, so preferences flip fast with viral trends.

This transparency raises buyer power for Estée Lauder: a single viral complaint can cut sales in a category by double digits within weeks, making reputation and consistent product performance critical.

Growth of Direct to Consumer Channels

Estée Lauder’s push into direct-to-consumer (DTC) channels—its e-commerce and ~600 freestanding stores as of FY2024—cuts third-party retailer leverage by raising company-controlled sales to about 35% of net sales in 2024, up from ~28% in 2019.

Direct sales boost gross margins (DTC often 5–10 percentage points higher), let EL capture first-party customer data for personalization, and act as a buffer vs. department store pricing and return demands.

- ~35% net sales via DTC in 2024

- ~600 freestanding stores worldwide

- DTC margin uplift ~5–10 p.p.

- First-party data improves targeting and loyalty

Price Sensitivity in the Prestige Segment

Prestige beauty often resists recessions, but 2023–2024 data show 28% of US consumers traded down to masstige (middle-market prestige) when premium benefits were unclear; in 2024 Estée Lauder Co. saw global net sales grow 6% to $18.5B but US prestige volume softness signaled price pushback.

High inflation and 2024 CPI at ~3.4% mean buyers may swap to masstige if value falls; Estée Lauder must prove superiority via R&D, new product launches, and elevated in-store/digital experiences to defend margins and justify premium pricing.

- 28% of consumers traded down (2023–24 survey)

- Estée Lauder 2024 net sales ~$18.5B, +6%

- 2024 US CPI ~3.4% increases price sensitivity

- Actions: innovate, elevate CX, defend premium margin

Estée Lauder Battles Buyer Power: DTC Gains Offset Rising Trade, Ad & R&D Costs

Buyers have strong leverage: retail consolidation (Sephora+Ulta ≈28% US prestige sales, 2024) and low switching costs force Estée Lauder into higher trade spend (trade up ~120 bps in 2024) and heavy marketing/product R&D (advertising $1.1B, R&D $420M FY2024). DTC growth to ~35% of net sales in 2024 and ~600 stores helps regain margin (DTC +5–10 p.p.) and first‑party data, but viral social trends (72% consult influencers, McKinsey 2024) keep buyer power high.

| Metric | 2024 |

|---|---|

| Net sales | $18.5B |

| DTC share | ~35% |

| Retailer share (Sephora+Ulta) | ~28% US |

| Ad spend | $1.1B |

| R&D | $420M |

Same Document Delivered

The Estée Lauder Companies Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for The Estée Lauder Companies you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase.