E.Sun Financial PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological adoption are shaping E.Sun Financial’s strategic trajectory in our concise PESTLE snapshot—designed for investors and strategists who need clear, actionable context. Purchase the full analysis to access detailed risk assessments, regulatory implications, and market opportunities, all delivered in editable formats for immediate use.

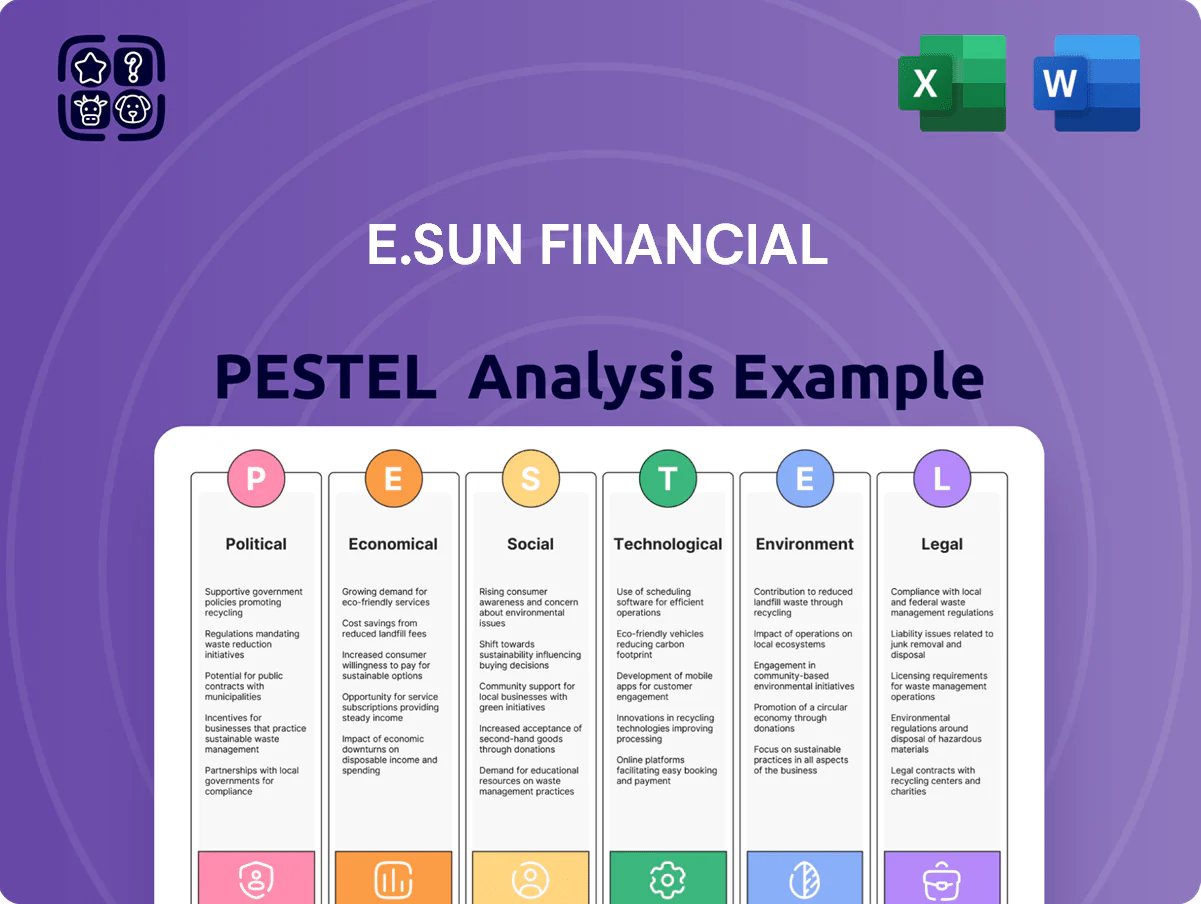

Political factors

Geopolitical stability and cross-strait relations

The ongoing tension between Taiwan and mainland China materially affects investor sentiment and capital flows, with Taiwan's foreign direct investment falling 12% in 2024 Q3 year-on-year and the TAIEX volatility climbing 18% over 2023–24, pressuring regional liquidity. E.Sun Financial must factor regional security into strategic planning—delaying some 2025 overseas branch expansion scenarios—and adjust capital buffer targets after the bank's 2024 CET1 ratio was 12.8%. The bank actively monitors cross-strait developments to hedge FX, credit and operational risks across its domestic and international portfolios.

Financial Supervisory Commission regulatory alignment

The Financial Supervisory Commission sets Taiwan’s regulatory tone, pushing banks toward digitalization; E.Sun reported NT$3.2 trillion in total assets (2025 Q1) and channels digital investments to meet FSC standards on cybersecurity and open banking. E.Sun aligns expansion with the government’s New Southbound Policy, growing Southeast Asia revenue by 18% YoY in 2024, and maintains regulator ties to keep product approval timelines predictable (average 4–6 months).

International trade agreements and participation

Taiwan's push to join CPTPP and other trade blocs boosts exporters—the manufacturing/export sector, ~33% of Taiwan's goods exports in 2024, increases demand for E.Sun's trade finance, letters of credit and commercial loans; 2024 trade finance volumes in Taiwan rose ~6.2% YoY. Changes in trade policy prompt E.Sun to recalibrate credit-risk models, stress-testing exposure to key trading partners and adjusting provisioning ratios accordingly.

Government mandates for sustainable finance

The Taiwanese government embedded a 2050 net-zero target into national policy, pushing banks to expand green lending; Taiwan set a 2025 renewable capacity target of 20 GW and a 2030 non-nuclear renewables share goal of ~20%, creating demand for project financing.

E.Sun acts as a strategic partner in financing favored renewable projects, having committed NT$150 billion to sustainable finance by 2024 and expanding green loan facilities to capture politically driven opportunities.

This policy alignment helped E.Sun secure a leading local sustainable finance position, with green loan growth of ~18% year-on-year in 2023 and a top-3 market share in Taiwan’s green lending segment.

- 2050 net-zero target; 2025 target 20 GW renewables

- E.Sun NT$150 billion sustainable finance commitment (2024)

- Green loan growth ~18% YoY (2023); top-3 market share

ASEAN political climate for expansion

E.Sun's expansion in Cambodia, Vietnam and Thailand hinges on host-nation political stability; Cambodia's IMF-adjusted growth 2024 forecast 5.8% and Vietnam's 2024 GDP +5.4% influence credit demand and branch viability.

Cross-strait and Taiwan–ASEAN diplomatic ties affect licensing speed and regulatory cooperation; recent 2024 MOUs eased entry in Vietnam but Thailand remains cautious.

The bank deploys localized risk controls—local management, currency hedges, and a 2023-24 compliance budget increase of ~12%—to mitigate political volatility.

- Dependence on host stability: GDP growth rates (Cambodia 5.8%, Vietnam 5.4% 2024)

- Diplomatic influence on licensing: 2024 MOUs improved Vietnam entry

- Mitigation: local leadership, hedging, +12% compliance spend 2023-24

Cross‑strait strain trims FDI -12%, boosts TAIEX vol +18%; E.Sun steadies CET1, pivots SEA & green loans

Cross-strait tensions cut FDI -12% (2024 Q3) and raised TAIEX volatility +18% (2023–24), prompting E.Sun to delay some 2025 overseas expansions and hold CET1 at 12.8% (2024). FSC digital/cyber rules drive NT$3.2T asset bank to boost digital spend; Southeast Asia revenue +18% YoY (2024). Taiwan 2050 net-zero spurs green loans (NT$150B commitment, 18% YoY growth). Local political stability: Cambodia GDP 5.8%, Vietnam 5.4% (2024).

| Metric | Value |

|---|---|

| FDI change 2024 Q3 | -12% |

| TAIEX vol change | +18% |

| CET1 (2024) | 12.8% |

| Total assets (2025 Q1) | NT$3.2T |

| SEA revenue YoY (2024) | +18% |

| Sustainable finance commitment | NT$150B |

| Green loan growth (2023) | +18% YoY |

| Cambodia GDP (2024) | 5.8% |

| Vietnam GDP (2024) | 5.4% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect E.Sun Financial, with data-driven subpoints and forward-looking insights tied to regional market and regulatory dynamics to aid executives, consultants, and investors in spotting risks and opportunities.

A concise, visually segmented PESTLE summary for E.Sun Financial that’s easy to drop into presentations or share across teams, enabling quick interpretation of external risks and market positioning while allowing users to add notes tailored to their region or business line.

Economic factors

Interest rate cycles and monetary policy

Fluctuations in rates by the Central Bank of Taiwan and the US Federal Reserve directly affect E.Sun’s net interest margin; Taiwan’s policy rate rose to 1.875% in 2024 while the Fed held at 5.25–5.50% in late 2024, raising funding and lending spread volatility.

As a major provider of TWD and USD loans, E.Sun benefits from rate hikes via wider margins but faces margin compression if cuts occur; USD exposure means Fed moves can alter international funding costs.

Robust asset-liability management—E.Sun reported a 2024 net interest margin around 1.40%—is crucial to hedge duration, rebalance loan-deposit mix, and use swaps to mitigate interest-rate risk.

Inflationary pressures and consumer behavior

Persistent inflation—Taiwan CPI rose 2.6% in 2024—erodes retail purchasing power and raises E.Sun Financial’s operating costs via higher wages and service expenses.

Higher living costs push clients toward inflation-hedged assets; Taiwan household deposits fell 0.8% y/y Sept 2024 while real estate and gold inflows rose.

E.Sun monitors these shifts and adjusted 2024 product mix, expanding inflation-linked notes and diversified wealth solutions for HNW and retail segments.

Semiconductor and technology sector performance

Taiwan's GDP had ~20% exposure to semiconductors and electronics in 2024, leaving E.Sun's corporate loan book sensitive to global tech demand; a 2023–24 downturn saw regional electronics exports fall ~8% YoY, pressuring borrowers.

Supply-chain contractions can raise corporate NPLs—Taiwanese bank NPL ratio in 2024 ticked to ~0.45% from 0.38% in 2022—raising risk for E.Sun’s tech-linked credits.

E.Sun reports a diversified lending mix with <30% corporate exposure to electronics/tech and growing SME, consumer, and green lending to limit concentration risk.

Currency exchange rate volatility

The New Taiwan Dollar's 2024 swing: NT$ appreciated ~1.8% vs USD and depreciated ~2.3% vs JPY year-to-date, directly impacting E.Sun's trade finance margins and overseas asset valuations.

E.Sun offers forward contracts, FX swaps and option-based hedges while actively managing a reported FX VaR of NT$3.2 billion (2024) to limit balance-sheet exposure.

FX volatility drove a ±12% range in the bank's 2024 non-interest income from trading and FX gains.

- NT$ movement vs USD/JPY alters trade finance pricing and overseas valuations

- E.Sun provides forwards, swaps, options; FX VaR ~NT$3.2bn (2024)

- FX volatility caused ~±12% swing in 2024 non-interest income

Global economic growth outlook

- IMF 2025 global GDP forecast 3.0%

- Taiwan mortgages -4% in 2024 vs 2023

- E.SUN CET1 12.8% (2024)

Tight rates, weak tech hit margins—Taiwan banks cushioned by 12.8% CET1

Interest-rate shifts (TW policy 1.875% 2024; Fed 5.25–5.50% late 2024) drive NIM (E.Sun ~1.40% 2024) and funding costs; Taiwan CPI 2.6% 2024 pressures margins and deposits (-0.8% y/y Sept 2024). Tech exposure (~20% GDP; electronics exports -8% 2023–24) raises corporate NPL risk (bank NPL ~0.45% 2024); CET1 12.8% cushions shocks.

| Metric | 2024 |

|---|---|

| Policy rate TW | 1.875% |

| Fed rate | 5.25–5.50% |

| NIM (E.Sun) | ~1.40% |

| CPI Taiwan | 2.6% |

| Deposits change | -0.8% Y/Y |

| Electronics exports | -8% Y/Y |

| Bank NPL | ~0.45% |

| CET1 | 12.8% |

Preview Before You Purchase

E.Sun Financial PESTLE Analysis

The preview shown here is the exact E.Sun Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real file and you’ll be able to download the identical document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological adoption are shaping E.Sun Financial’s strategic trajectory in our concise PESTLE snapshot—designed for investors and strategists who need clear, actionable context. Purchase the full analysis to access detailed risk assessments, regulatory implications, and market opportunities, all delivered in editable formats for immediate use.

Political factors

Geopolitical stability and cross-strait relations

The ongoing tension between Taiwan and mainland China materially affects investor sentiment and capital flows, with Taiwan's foreign direct investment falling 12% in 2024 Q3 year-on-year and the TAIEX volatility climbing 18% over 2023–24, pressuring regional liquidity. E.Sun Financial must factor regional security into strategic planning—delaying some 2025 overseas branch expansion scenarios—and adjust capital buffer targets after the bank's 2024 CET1 ratio was 12.8%. The bank actively monitors cross-strait developments to hedge FX, credit and operational risks across its domestic and international portfolios.

Financial Supervisory Commission regulatory alignment

The Financial Supervisory Commission sets Taiwan’s regulatory tone, pushing banks toward digitalization; E.Sun reported NT$3.2 trillion in total assets (2025 Q1) and channels digital investments to meet FSC standards on cybersecurity and open banking. E.Sun aligns expansion with the government’s New Southbound Policy, growing Southeast Asia revenue by 18% YoY in 2024, and maintains regulator ties to keep product approval timelines predictable (average 4–6 months).

International trade agreements and participation

Taiwan's push to join CPTPP and other trade blocs boosts exporters—the manufacturing/export sector, ~33% of Taiwan's goods exports in 2024, increases demand for E.Sun's trade finance, letters of credit and commercial loans; 2024 trade finance volumes in Taiwan rose ~6.2% YoY. Changes in trade policy prompt E.Sun to recalibrate credit-risk models, stress-testing exposure to key trading partners and adjusting provisioning ratios accordingly.

Government mandates for sustainable finance

The Taiwanese government embedded a 2050 net-zero target into national policy, pushing banks to expand green lending; Taiwan set a 2025 renewable capacity target of 20 GW and a 2030 non-nuclear renewables share goal of ~20%, creating demand for project financing.

E.Sun acts as a strategic partner in financing favored renewable projects, having committed NT$150 billion to sustainable finance by 2024 and expanding green loan facilities to capture politically driven opportunities.

This policy alignment helped E.Sun secure a leading local sustainable finance position, with green loan growth of ~18% year-on-year in 2023 and a top-3 market share in Taiwan’s green lending segment.

- 2050 net-zero target; 2025 target 20 GW renewables

- E.Sun NT$150 billion sustainable finance commitment (2024)

- Green loan growth ~18% YoY (2023); top-3 market share

ASEAN political climate for expansion

E.Sun's expansion in Cambodia, Vietnam and Thailand hinges on host-nation political stability; Cambodia's IMF-adjusted growth 2024 forecast 5.8% and Vietnam's 2024 GDP +5.4% influence credit demand and branch viability.

Cross-strait and Taiwan–ASEAN diplomatic ties affect licensing speed and regulatory cooperation; recent 2024 MOUs eased entry in Vietnam but Thailand remains cautious.

The bank deploys localized risk controls—local management, currency hedges, and a 2023-24 compliance budget increase of ~12%—to mitigate political volatility.

- Dependence on host stability: GDP growth rates (Cambodia 5.8%, Vietnam 5.4% 2024)

- Diplomatic influence on licensing: 2024 MOUs improved Vietnam entry

- Mitigation: local leadership, hedging, +12% compliance spend 2023-24

Cross‑strait strain trims FDI -12%, boosts TAIEX vol +18%; E.Sun steadies CET1, pivots SEA & green loans

Cross-strait tensions cut FDI -12% (2024 Q3) and raised TAIEX volatility +18% (2023–24), prompting E.Sun to delay some 2025 overseas expansions and hold CET1 at 12.8% (2024). FSC digital/cyber rules drive NT$3.2T asset bank to boost digital spend; Southeast Asia revenue +18% YoY (2024). Taiwan 2050 net-zero spurs green loans (NT$150B commitment, 18% YoY growth). Local political stability: Cambodia GDP 5.8%, Vietnam 5.4% (2024).

| Metric | Value |

|---|---|

| FDI change 2024 Q3 | -12% |

| TAIEX vol change | +18% |

| CET1 (2024) | 12.8% |

| Total assets (2025 Q1) | NT$3.2T |

| SEA revenue YoY (2024) | +18% |

| Sustainable finance commitment | NT$150B |

| Green loan growth (2023) | +18% YoY |

| Cambodia GDP (2024) | 5.8% |

| Vietnam GDP (2024) | 5.4% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect E.Sun Financial, with data-driven subpoints and forward-looking insights tied to regional market and regulatory dynamics to aid executives, consultants, and investors in spotting risks and opportunities.

A concise, visually segmented PESTLE summary for E.Sun Financial that’s easy to drop into presentations or share across teams, enabling quick interpretation of external risks and market positioning while allowing users to add notes tailored to their region or business line.

Economic factors

Interest rate cycles and monetary policy

Fluctuations in rates by the Central Bank of Taiwan and the US Federal Reserve directly affect E.Sun’s net interest margin; Taiwan’s policy rate rose to 1.875% in 2024 while the Fed held at 5.25–5.50% in late 2024, raising funding and lending spread volatility.

As a major provider of TWD and USD loans, E.Sun benefits from rate hikes via wider margins but faces margin compression if cuts occur; USD exposure means Fed moves can alter international funding costs.

Robust asset-liability management—E.Sun reported a 2024 net interest margin around 1.40%—is crucial to hedge duration, rebalance loan-deposit mix, and use swaps to mitigate interest-rate risk.

Inflationary pressures and consumer behavior

Persistent inflation—Taiwan CPI rose 2.6% in 2024—erodes retail purchasing power and raises E.Sun Financial’s operating costs via higher wages and service expenses.

Higher living costs push clients toward inflation-hedged assets; Taiwan household deposits fell 0.8% y/y Sept 2024 while real estate and gold inflows rose.

E.Sun monitors these shifts and adjusted 2024 product mix, expanding inflation-linked notes and diversified wealth solutions for HNW and retail segments.

Semiconductor and technology sector performance

Taiwan's GDP had ~20% exposure to semiconductors and electronics in 2024, leaving E.Sun's corporate loan book sensitive to global tech demand; a 2023–24 downturn saw regional electronics exports fall ~8% YoY, pressuring borrowers.

Supply-chain contractions can raise corporate NPLs—Taiwanese bank NPL ratio in 2024 ticked to ~0.45% from 0.38% in 2022—raising risk for E.Sun’s tech-linked credits.

E.Sun reports a diversified lending mix with <30% corporate exposure to electronics/tech and growing SME, consumer, and green lending to limit concentration risk.

Currency exchange rate volatility

The New Taiwan Dollar's 2024 swing: NT$ appreciated ~1.8% vs USD and depreciated ~2.3% vs JPY year-to-date, directly impacting E.Sun's trade finance margins and overseas asset valuations.

E.Sun offers forward contracts, FX swaps and option-based hedges while actively managing a reported FX VaR of NT$3.2 billion (2024) to limit balance-sheet exposure.

FX volatility drove a ±12% range in the bank's 2024 non-interest income from trading and FX gains.

- NT$ movement vs USD/JPY alters trade finance pricing and overseas valuations

- E.Sun provides forwards, swaps, options; FX VaR ~NT$3.2bn (2024)

- FX volatility caused ~±12% swing in 2024 non-interest income

Global economic growth outlook

- IMF 2025 global GDP forecast 3.0%

- Taiwan mortgages -4% in 2024 vs 2023

- E.SUN CET1 12.8% (2024)

Tight rates, weak tech hit margins—Taiwan banks cushioned by 12.8% CET1

Interest-rate shifts (TW policy 1.875% 2024; Fed 5.25–5.50% late 2024) drive NIM (E.Sun ~1.40% 2024) and funding costs; Taiwan CPI 2.6% 2024 pressures margins and deposits (-0.8% y/y Sept 2024). Tech exposure (~20% GDP; electronics exports -8% 2023–24) raises corporate NPL risk (bank NPL ~0.45% 2024); CET1 12.8% cushions shocks.

| Metric | 2024 |

|---|---|

| Policy rate TW | 1.875% |

| Fed rate | 5.25–5.50% |

| NIM (E.Sun) | ~1.40% |

| CPI Taiwan | 2.6% |

| Deposits change | -0.8% Y/Y |

| Electronics exports | -8% Y/Y |

| Bank NPL | ~0.45% |

| CET1 | 12.8% |

Preview Before You Purchase

E.Sun Financial PESTLE Analysis

The preview shown here is the exact E.Sun Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real file and you’ll be able to download the identical document immediately after checkout.