Etihad Airways Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

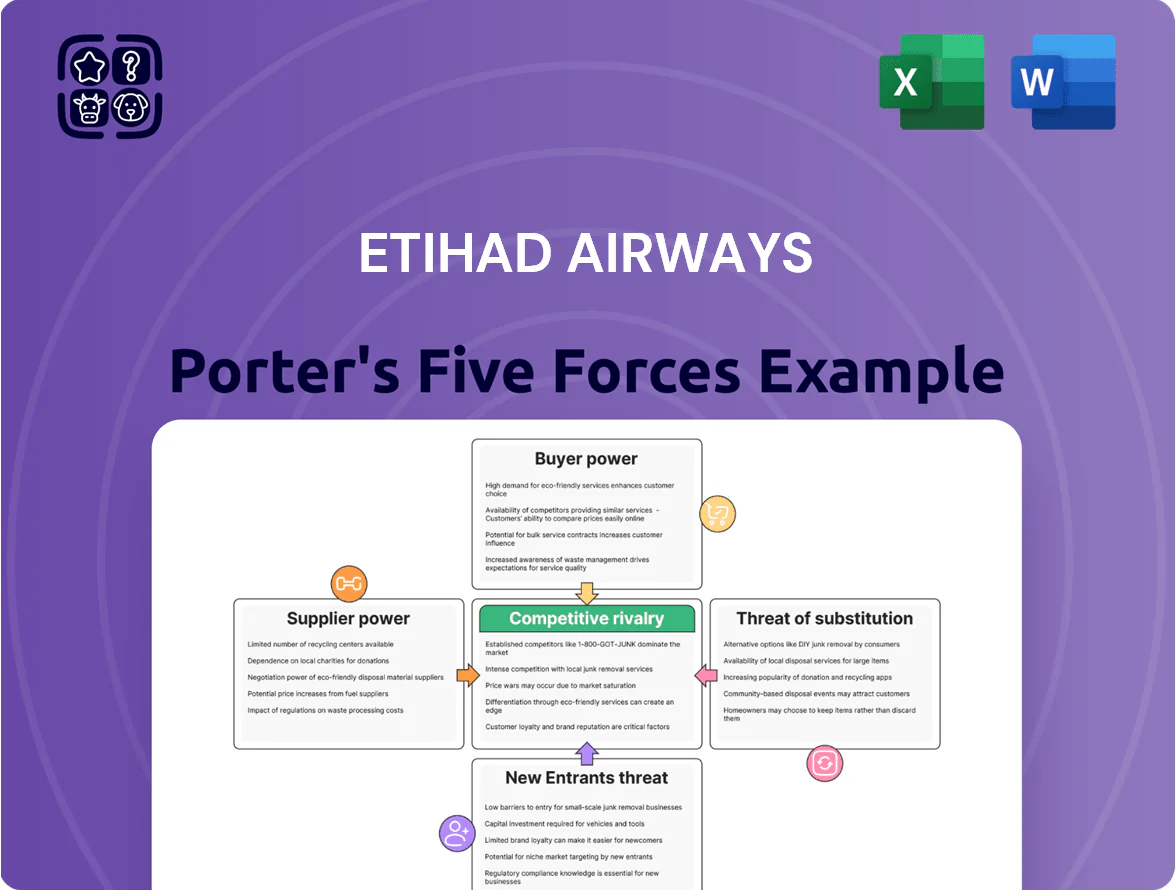

Etihad Airways faces moderate supplier power, intense rivalry among Gulf and global carriers, and rising substitute threats from high-speed rail on short-haul routes; regulatory barriers and capital intensity keep new entrants limited but existing competitors aggressive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Etihad Airways’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Aircraft Manufacturing Duopoly

Etihad depends mainly on Boeing and Airbus for its wide-body fleet, with over 85% of long-haul frames sourced from them as of 2025, creating high supplier dependency.

Few viable alternatives for long-haul jets give Boeing and Airbus leverage on price and delivery; in 2024 OEM order backlogs totaled ~8,200 aircraft, stretching lead times.

The technical complexity and stringent safety certifications (EASA, FAA) raise switching costs and strengthen supplier bargaining power.

Volatility in Aviation Fuel Costs

Fuel is one of Etihad Airways’ largest costs—about 20–25% of operating expenses in 2024—so global crude swings and refinery pricing give suppliers strong leverage.

Hedging cut volatility short-term (Etihad used jet fuel hedges covering ~30% of consumption in 2023–24), but geopolitical shocks like 2022–23 OPEC+ moves still spike costs.

Suppliers of sustainable aviation fuel (SAF) are few; global SAF production was ~0.1% of jet fuel demand in 2024, so tightening regulations by late 2025 will increase supplier pricing power.

Specialized Engine Maintenance and Parts

Etihad relies on GE Aerospace and Rolls‑Royce engines that typically come with long‑term, exclusive service agreements; OEMs captured about 60–70% of global narrowbody MRO revenue in 2024, concentrating spare‑parts control and technical expertise. This supplier dominance raises high switching costs for Etihad—replacing engine fleets would need billions in capital and retraining and risk grounding aircraft during multi‑year retrofit programs.

Labor Union and Skilled Talent Availability

The post-2024 recovery left certified pilots and specialized technicians scarce; IATA estimated a global pilot shortfall of about 34,000 by end-2024, raising supplier leverage for Etihad.

Abu Dhabi’s tax-free pay helps recruitment, but global competition—especially from Gulf carriers offering sign-on bonuses (often USD 20k–60k)—forces Etihad to match pay and benefits to keep ops steady.

- Global pilot gap ~34,000 (IATA, 2024)

- Sign-on bonuses typically USD 20k–60k

- Etihad must match pay/benefits to avoid disruptions

Airport Infrastructure and Slot Constraints

Etihad depends on airport infrastructure and ATC; limited slots at major hubs boost airport operators’ bargaining power, raising landing fees and schedule limits—IATA reported global slot-constrained airports caused 12% flight delays in 2024.

As primary tenant at Zayed International Airport, Etihad’s growth is tied to Abu Dhabi’s CAPEX plan: AED 24 billion (USD 6.5 billion) announced for airport expansion through 2028, shaping fleet and route timing.

- Slot scarcity raises unit costs and schedule risk

- Airport fees up to 15–25% of short-haul CASM in constrained hubs

- Zayed expansion AED 24B guides Etihad capacity planning

Supplier Dominance: Boeing/Airbus, OEM Backlogs, Fuel & Pilot Crunch Shape Aviation

Suppliers hold high bargaining power: Boeing/Airbus supply >85% long‑haul fleet (2025), OEM backlogs ~8,200 aircraft (2024), jet fuel = 20–25% opex (2024), SAF ~0.1% of jet fuel demand (2024), pilot shortfall ~34,000 (IATA 2024), engine OEMs control 60–70% MRO revenue (2024).

| Metric | Value |

|---|---|

| Long‑haul fleet reliance | >85% (2025) |

| OEM backlog | ~8,200 aircraft (2024) |

| Jet fuel share of opex | 20–25% (2024) |

| SAF share | ~0.1% global demand (2024) |

| Pilot shortfall | ~34,000 (IATA, 2024) |

| Engine OEM MRO share | 60–70% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Etihad Airways, uncovering competitive pressures, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect profitability and market position.

A concise Porter's Five Forces snapshot for Etihad—clear visuals and scores to speed strategic choices and investor briefs.

Customers Bargaining Power

High Price Sensitivity in Economy Class

The majority of leisure flyers use price-comparison sites; 72% of global leisure passengers searched fares online in 2024, so Etihad struggles to keep economy loyalty and must match rivals’ fares.

Etihad faces direct pressure from full-service peers and low-cost carriers—economy yields fell 4.1% industry-wide in 2024—forcing competitive pricing and promo fares.

Even small price moves matter: a 5% fare cut can lift load factor by ~3–5%, quickly shifting volume to rivals.

Low Switching Costs for Travelers

Individual passengers face negligible costs switching airlines on common international routes, and global online travel agencies account for over 40% of bookings in 2024, increasing brand churn.

Etihad Guest loyalty membership reached ~7.2 million in 2024, but weak switching barriers mean loyalty alone is insufficient to lock customers in.

That forces Etihad to keep investing in cabin service and IFC/IFE—Etihad reported a $120–150 million annual spend on product and entertainment improvements in 2023–24—to defend yield and load factor.

Influence of Corporate Travel Contracts

Large corporate clients and government entities push Etihad for volume-based discounts—corporate travel can account for 20–30% of premium-cabin revenue on Gulf carriers—so buyers secure lower yields via negotiated rates.

They also demand tailored services and flexible booking terms; contracts often include seat blocks, rollover clauses, and net fares that cut average fare per premium passenger by 10–25%.

To lock steady load factors in premium cabins (Etihad’s premium load factor target ~70% in 2024), Etihad must bid aggressively for these high-value deals, trading margin for occupancy.

Transparency via Digital Platforms

The ubiquity of social media and travel sites (Tripadvisor, Skytrax) lets customers publicly critique Etihad’s service, directly affecting bookings; 72% of travelers in 2024 said online reviews influenced their airline choice.

Real-time tracking apps and flight-status tools expose delays, seat comfort, and amenity issues instantly, increasing service accountability and complaint volumes.

Etihad must sustain high standards—customer satisfaction dips can hit revenue: a 1% drop in NPS often correlates with ~0.5% lower ancillary revenue within 12 months.

- 72% of travelers rely on reviews (2024)

- Real-time delay alerts raise complaint rates

- 1% NPS drop ≈ 0.5% ancillary revenue loss

Cargo Client Consolidation

- Top buyers: ~45% global tonnage

- Revenue exposure: 40–55%

- Switch trigger: small price/reliability gaps

- Must offer: advanced tracking, SLAs, pharma handling

Customers dictate fares: OTAs, corporate cuts & cargo reshape Etihad’s revenue mix

Customers hold strong bargaining power: 72% used online fare search in 2024, OTAs drove >40% bookings, a 5% fare cut lifts load by ~3–5%, Etihad Guest reached ~7.2M members (2024) but low switching costs persist, corporate deals cut premium fares 10–25%, cargo forwarders drive 40–55% revenue; Etihad spent $120–150M on product/IFE (2023–24) to defend yield.

| Metric | 2024 value |

|---|---|

| Online fare search | 72% |

| OTA bookings | >40% |

| Etihad Guest | 7.2M |

| Corp fare cuts | 10–25% |

| Product spend | $120–150M |

| Cargo revenue | 40–55% |

Full Version Awaits

Etihad Airways Porter's Five Forces Analysis

This preview shows the exact Etihad Airways Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll get—ready for download and use the moment you buy.

You're viewing the actual final file; upon payment you’ll gain instant access to this same deliverable, fully researched and ready for your needs.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Etihad Airways faces moderate supplier power, intense rivalry among Gulf and global carriers, and rising substitute threats from high-speed rail on short-haul routes; regulatory barriers and capital intensity keep new entrants limited but existing competitors aggressive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Etihad Airways’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Aircraft Manufacturing Duopoly

Etihad depends mainly on Boeing and Airbus for its wide-body fleet, with over 85% of long-haul frames sourced from them as of 2025, creating high supplier dependency.

Few viable alternatives for long-haul jets give Boeing and Airbus leverage on price and delivery; in 2024 OEM order backlogs totaled ~8,200 aircraft, stretching lead times.

The technical complexity and stringent safety certifications (EASA, FAA) raise switching costs and strengthen supplier bargaining power.

Volatility in Aviation Fuel Costs

Fuel is one of Etihad Airways’ largest costs—about 20–25% of operating expenses in 2024—so global crude swings and refinery pricing give suppliers strong leverage.

Hedging cut volatility short-term (Etihad used jet fuel hedges covering ~30% of consumption in 2023–24), but geopolitical shocks like 2022–23 OPEC+ moves still spike costs.

Suppliers of sustainable aviation fuel (SAF) are few; global SAF production was ~0.1% of jet fuel demand in 2024, so tightening regulations by late 2025 will increase supplier pricing power.

Specialized Engine Maintenance and Parts

Etihad relies on GE Aerospace and Rolls‑Royce engines that typically come with long‑term, exclusive service agreements; OEMs captured about 60–70% of global narrowbody MRO revenue in 2024, concentrating spare‑parts control and technical expertise. This supplier dominance raises high switching costs for Etihad—replacing engine fleets would need billions in capital and retraining and risk grounding aircraft during multi‑year retrofit programs.

Labor Union and Skilled Talent Availability

The post-2024 recovery left certified pilots and specialized technicians scarce; IATA estimated a global pilot shortfall of about 34,000 by end-2024, raising supplier leverage for Etihad.

Abu Dhabi’s tax-free pay helps recruitment, but global competition—especially from Gulf carriers offering sign-on bonuses (often USD 20k–60k)—forces Etihad to match pay and benefits to keep ops steady.

- Global pilot gap ~34,000 (IATA, 2024)

- Sign-on bonuses typically USD 20k–60k

- Etihad must match pay/benefits to avoid disruptions

Airport Infrastructure and Slot Constraints

Etihad depends on airport infrastructure and ATC; limited slots at major hubs boost airport operators’ bargaining power, raising landing fees and schedule limits—IATA reported global slot-constrained airports caused 12% flight delays in 2024.

As primary tenant at Zayed International Airport, Etihad’s growth is tied to Abu Dhabi’s CAPEX plan: AED 24 billion (USD 6.5 billion) announced for airport expansion through 2028, shaping fleet and route timing.

- Slot scarcity raises unit costs and schedule risk

- Airport fees up to 15–25% of short-haul CASM in constrained hubs

- Zayed expansion AED 24B guides Etihad capacity planning

Supplier Dominance: Boeing/Airbus, OEM Backlogs, Fuel & Pilot Crunch Shape Aviation

Suppliers hold high bargaining power: Boeing/Airbus supply >85% long‑haul fleet (2025), OEM backlogs ~8,200 aircraft (2024), jet fuel = 20–25% opex (2024), SAF ~0.1% of jet fuel demand (2024), pilot shortfall ~34,000 (IATA 2024), engine OEMs control 60–70% MRO revenue (2024).

| Metric | Value |

|---|---|

| Long‑haul fleet reliance | >85% (2025) |

| OEM backlog | ~8,200 aircraft (2024) |

| Jet fuel share of opex | 20–25% (2024) |

| SAF share | ~0.1% global demand (2024) |

| Pilot shortfall | ~34,000 (IATA, 2024) |

| Engine OEM MRO share | 60–70% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Etihad Airways, uncovering competitive pressures, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect profitability and market position.

A concise Porter's Five Forces snapshot for Etihad—clear visuals and scores to speed strategic choices and investor briefs.

Customers Bargaining Power

High Price Sensitivity in Economy Class

The majority of leisure flyers use price-comparison sites; 72% of global leisure passengers searched fares online in 2024, so Etihad struggles to keep economy loyalty and must match rivals’ fares.

Etihad faces direct pressure from full-service peers and low-cost carriers—economy yields fell 4.1% industry-wide in 2024—forcing competitive pricing and promo fares.

Even small price moves matter: a 5% fare cut can lift load factor by ~3–5%, quickly shifting volume to rivals.

Low Switching Costs for Travelers

Individual passengers face negligible costs switching airlines on common international routes, and global online travel agencies account for over 40% of bookings in 2024, increasing brand churn.

Etihad Guest loyalty membership reached ~7.2 million in 2024, but weak switching barriers mean loyalty alone is insufficient to lock customers in.

That forces Etihad to keep investing in cabin service and IFC/IFE—Etihad reported a $120–150 million annual spend on product and entertainment improvements in 2023–24—to defend yield and load factor.

Influence of Corporate Travel Contracts

Large corporate clients and government entities push Etihad for volume-based discounts—corporate travel can account for 20–30% of premium-cabin revenue on Gulf carriers—so buyers secure lower yields via negotiated rates.

They also demand tailored services and flexible booking terms; contracts often include seat blocks, rollover clauses, and net fares that cut average fare per premium passenger by 10–25%.

To lock steady load factors in premium cabins (Etihad’s premium load factor target ~70% in 2024), Etihad must bid aggressively for these high-value deals, trading margin for occupancy.

Transparency via Digital Platforms

The ubiquity of social media and travel sites (Tripadvisor, Skytrax) lets customers publicly critique Etihad’s service, directly affecting bookings; 72% of travelers in 2024 said online reviews influenced their airline choice.

Real-time tracking apps and flight-status tools expose delays, seat comfort, and amenity issues instantly, increasing service accountability and complaint volumes.

Etihad must sustain high standards—customer satisfaction dips can hit revenue: a 1% drop in NPS often correlates with ~0.5% lower ancillary revenue within 12 months.

- 72% of travelers rely on reviews (2024)

- Real-time delay alerts raise complaint rates

- 1% NPS drop ≈ 0.5% ancillary revenue loss

Cargo Client Consolidation

- Top buyers: ~45% global tonnage

- Revenue exposure: 40–55%

- Switch trigger: small price/reliability gaps

- Must offer: advanced tracking, SLAs, pharma handling

Customers dictate fares: OTAs, corporate cuts & cargo reshape Etihad’s revenue mix

Customers hold strong bargaining power: 72% used online fare search in 2024, OTAs drove >40% bookings, a 5% fare cut lifts load by ~3–5%, Etihad Guest reached ~7.2M members (2024) but low switching costs persist, corporate deals cut premium fares 10–25%, cargo forwarders drive 40–55% revenue; Etihad spent $120–150M on product/IFE (2023–24) to defend yield.

| Metric | 2024 value |

|---|---|

| Online fare search | 72% |

| OTA bookings | >40% |

| Etihad Guest | 7.2M |

| Corp fare cuts | 10–25% |

| Product spend | $120–150M |

| Cargo revenue | 40–55% |

Full Version Awaits

Etihad Airways Porter's Five Forces Analysis

This preview shows the exact Etihad Airways Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll get—ready for download and use the moment you buy.

You're viewing the actual final file; upon payment you’ll gain instant access to this same deliverable, fully researched and ready for your needs.