Etisalat Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

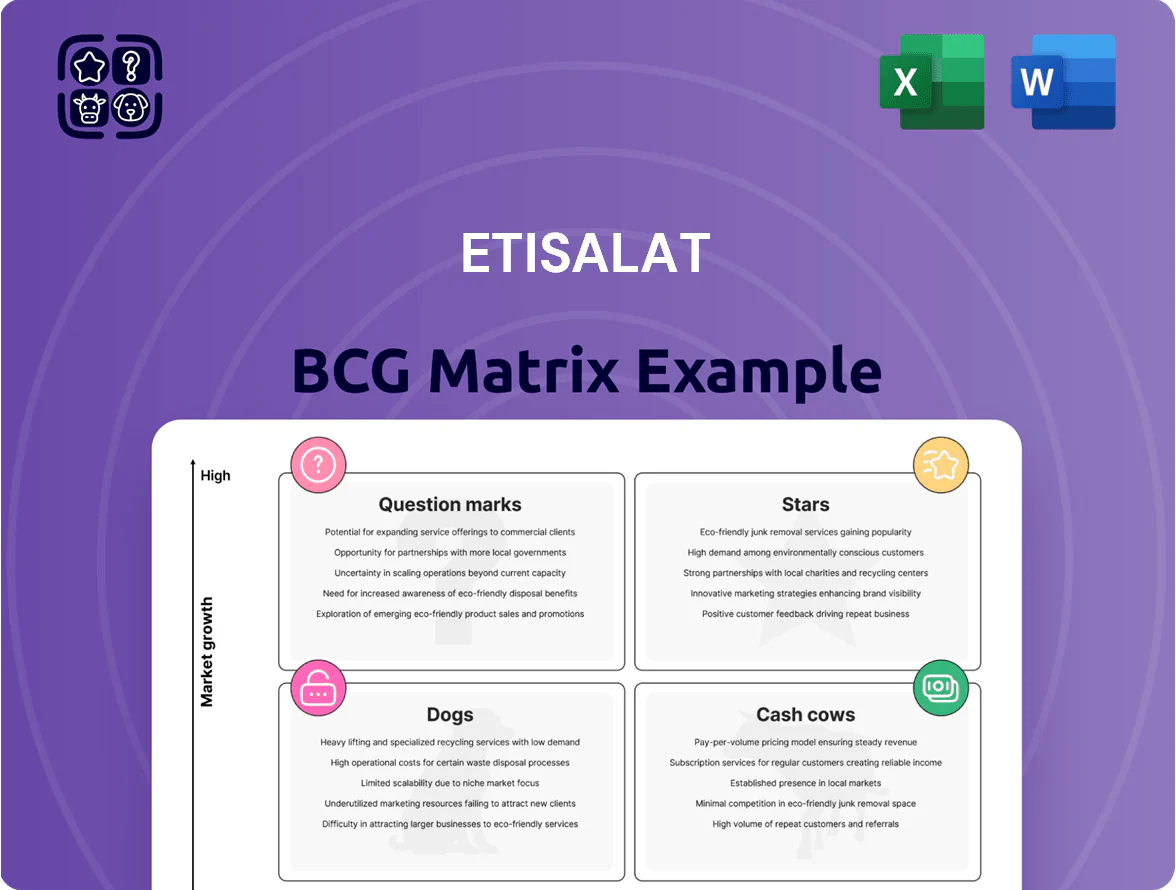

Etisalat’s BCG Matrix preview highlights its mix of high-growth segments—like digital services and business solutions—that act as Stars, alongside mature telecom operations serving as reliable Cash Cows; smaller legacy lines may be classified as Dogs or Question Marks depending on regional performance. This snapshot reveals where cash generation fuels innovation and where divestment or investment shifts could unlock value. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and downloadable Word and Excel files to guide strategic and investment decisions.

Stars

5G Infrastructure and Connectivity

As of Q4 2025 e& (Etisalat Group) holds roughly 60% share of UAE 5G subscribers, cementing a dominant position in a market that grew 22% YoY in 2025 to ~6.1 million 5G lines.

The 5G infrastructure segment demands heavy capex—e& budgeted AED 6.4 billion (~USD 1.7bn) for network upgrades in 2025—driven by ultra‑high‑speed mobile and industrial IoT rollouts.

5G is a primary growth engine: in 2025 e& reported 5G ARPU ~AED 210/month, up 9% YoY, and enterprise IoT revenue grew 31%, supporting the UAE’s push to a fully digital economy.

e& enterprise Digital Solutions

e& enterprise Digital Solutions targets high-growth areas—cloud, cybersecurity, and AI for government—helping e& capture roughly 35% of UAE B2B cloud spend in 2024, with segment revenue ~AED 3.2bn that year.

Rapid national digitization (UAE Digital Economy Strategy 2031) and contracts with three federal agencies drove 22% YoY growth in 2024, but margin pressure persists as annual capex exceeded AED 1.1bn to compete with global hyperscalers.

International Expansion in Emerging Markets

Strategic acquisitions like e&'s 2021 PPF Telecom Group deal, completed for about $4.4 billion effective 2022–2023, put the group into Central and Eastern Europe, boosting 2024 pro forma service revenue by an estimated 12% and adding ~15 million subscribers versus UAE's low single-digit growth.

These emerging markets show annual subscriber growth rates of 3–7% vs UAE ~1%, but integrating PPF assets needs heavy capex—2024–2026 integration capex guided at roughly $2.0–2.5 billion—and higher opex to rebrand and harmonize networks.

Fintech and e& money

e& money, Etisalat Group’s digital finance arm, is a Star in the BCG matrix—growing fast in MENA fintech with a reported 2024 user base exceeding 8 million and year‑on‑year transaction value up ~60% to $9.4 billion.

By leveraging Etisalat’s ~160 million mobile subscribers, e& money is scaling toward a super‑app model (payments, remittances, micro‑lending) but faces fierce competition from regional banks and startups like PayTabs and Tabby.

High market growth (>25% annual fintech expansion in GCC, 2024) supports continued investment; churn and regulatory costs, however, could pressure margins.

- Users: >8M (2024)

- TPV: $9.4B, +60% YoY

- Mobile reach: 160M Etisalat subs

- GCC fintech growth: >25% (2024)

- Competitive risk: banks + fintech startups

AI and Autonomous Technologies

e& (formerly Etisalat Group) leads regional AI and autonomous rollouts—partnering on logistics automation and smart-city ops—backed by a 2025 capex push of ~$1.1B into cloud/AI infrastructure to grab first-mover advantage.

Market signals show rapid demand: regional AI infrastructure spending is forecast to grow ~28% CAGR 2024–2028, and automation can cut logistics costs 15–25% per McKinsey estimates, supporting e&'s strategic bet.

e&'s pilot deployments in 2024 handled thousands of autonomous deliveries and smart-city sensors, signaling scale readiness and high-margin potential versus legacy telco services.

- 2025 capex ~ $1.1B into AI/cloud

- Regional AI infra growth ~28% CAGR (2024–28)

- Logistics cost savings 15–25%

- 2024 pilots: thousands of autonomous ops

e& drives UAE 5G dominance, 8M+ e& money users and $1.1B AI/cloud push

Stars: e& 5G, e& money, and AI/cloud show high growth and strong share—UAE 5G ~60% share, 2025 lines 6.1M (+22%); e& capex AED 6.4bn (2025); e& money >8M users, TPV $9.4B (2024, +60%); AI/cloud capex ~$1.1B (2025), regional AI spend +28% CAGR (2024–28).

| Unit | Metric |

|---|---|

| UAE 5G | 60% share; 6.1M lines (2025) |

| Capex | AED 6.4bn (2025) |

| e& money | >8M users; $9.4B TPV (2024) |

| AI/cloud | $1.1B capex (2025); 28% CAGR |

What is included in the product

Comprehensive BCG review of Etisalat’s units with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page Etisalat BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

UAE Mobile Voice and Data

The UAE mobile voice and data business generates stable free cash flow, accounting for about 45% of Etisalat Group’s UAE EBITDA in 2024 (Etisalat Group FY2024 report), backed by ~78% mobile penetration and a domestic market share near 50% in 2025. With penetration high, year‑over‑year revenue growth has slowed to ~2% in 2024, lowering marketing intensity versus fast‑growing digital units. This steady cash engine funds capex and investments in 5G, cloud, and IoT expansions.

Fixed-line Broadband Services

As the UAE market leader in fixed-line broadband, Etisalat (Emirates Telecommunications Group Company PJSC) holds near-duopoly share with e& (formerly du), controlling about 70–75% of household fixed broadband subscriptions as of 2024.

With fiber rollout largely complete—FTTH coverage ~85% nationwide in 2024—the segment delivers high EBITDA margins near 50% and steady ARPU around AED 200–220, driving strong recurring cash flow.

Those cash flows funded 2024 dividends of AED 6.5 billion and support debt servicing on total net debt ~AED 30 billion, making fixed broadband a core cash cow for Etisalat.

Etisalat Egypt Operations

Etisalat Egypt, now mature with about 32% market share and ~45 million subscribers as of Dec 2025, sits squarely in the Cash Cows quadrant, delivering stable EGP-denominated EBITDA margins near 38% and FY2024 free cash flow around EGP 6.2bn.

Macroeconomic swings (2022–2025 inflation averaging ~26% annually) dent revenue growth, but retention keeps operating cash steady; capex/reinvestment is ~3–4% of revenue, focused on maintenance not new-market expansion.

Carrier and Wholesale Services

e& (Etisalat by e&, Abu Dhabi-listed telco) is a regional hub for international roaming, subsea cable capacity, and wholesale voice, handling ~30% of GCC transit and co-owning 6+ cables; this B2B segment sits in a low-growth global market but yields high EBITDA margins (~35% in 2024) due to scale and long-term contracts.

The business’s extensive fiber and cable footprint creates a durable moat, keeping churn low and capex intensity down; wholesale contributed roughly AED 4.2bn in revenue and >40% operating profit margin in FY 2024, making it a classic cash cow.

- Handles ~30% GCC transit

- Co-owns 6+ subsea cables

- EBITDA ~35% (2024)

- Wholesale revenue ~AED 4.2bn (FY2024)

- Low capex intensity, high margins

Legacy Satellite Communications

Legacy Satellite Communications delivers steady revenue for Etisalat (e&), serving oil, gas, and maritime clients with mature satellite and maritime links; revenue from these services contributed roughly AED 450–500 million in 2024 and showed <1% year-on-year volatility.

Low capex needs and predictable contracts make it a cash cow: EBITDA margins near 40% in 2024 and multi-year contracts underpin cash generation for group operations.

- Stable demand: niche clients in oil, gas, maritime

- Mature tech: low R&D, predictable costs

- 2024 revenue: ~AED 450–500M

- 2024 EBITDA margin: ~40%

- Market volatility: <1% YoY

Etisalat cash cows: UAE mobile, FTTH, Egypt, wholesale & satellite drive steady FCF

Etisalat’s UAE mobile/fixed broadband, Egypt operations, wholesale and satellite are Cash Cows, generating stable free cash flow: UAE mobile ~45% of UAE EBITDA (2024), FTTH coverage ~85% (2024), fixed broadband ARPU AED 200–220, Egypt FCF EGP 6.2bn (FY2024), wholesale revenue AED 4.2bn (FY2024), satellite revenue AED 450–500M (2024).

| Segment | Key 2024–25 metrics |

|---|---|

| UAE mobile | 45% UAE EBITDA; growth ~2% |

| Fixed broadband | FTTH 85%; ARPU AED200–220; EBITDA ~50% |

| Egypt | FCF EGP6.2bn; EBITDA ~38% |

| Wholesale | Revenue AED4.2bn; EBITDA ~35% |

| Satellite | Revenue AED450–500M; EBITDA ~40% |

Preview = Final Product

Etisalat BCG Matrix

The file you're previewing is the exact Etisalat BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Etisalat’s BCG Matrix preview highlights its mix of high-growth segments—like digital services and business solutions—that act as Stars, alongside mature telecom operations serving as reliable Cash Cows; smaller legacy lines may be classified as Dogs or Question Marks depending on regional performance. This snapshot reveals where cash generation fuels innovation and where divestment or investment shifts could unlock value. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and downloadable Word and Excel files to guide strategic and investment decisions.

Stars

5G Infrastructure and Connectivity

As of Q4 2025 e& (Etisalat Group) holds roughly 60% share of UAE 5G subscribers, cementing a dominant position in a market that grew 22% YoY in 2025 to ~6.1 million 5G lines.

The 5G infrastructure segment demands heavy capex—e& budgeted AED 6.4 billion (~USD 1.7bn) for network upgrades in 2025—driven by ultra‑high‑speed mobile and industrial IoT rollouts.

5G is a primary growth engine: in 2025 e& reported 5G ARPU ~AED 210/month, up 9% YoY, and enterprise IoT revenue grew 31%, supporting the UAE’s push to a fully digital economy.

e& enterprise Digital Solutions

e& enterprise Digital Solutions targets high-growth areas—cloud, cybersecurity, and AI for government—helping e& capture roughly 35% of UAE B2B cloud spend in 2024, with segment revenue ~AED 3.2bn that year.

Rapid national digitization (UAE Digital Economy Strategy 2031) and contracts with three federal agencies drove 22% YoY growth in 2024, but margin pressure persists as annual capex exceeded AED 1.1bn to compete with global hyperscalers.

International Expansion in Emerging Markets

Strategic acquisitions like e&'s 2021 PPF Telecom Group deal, completed for about $4.4 billion effective 2022–2023, put the group into Central and Eastern Europe, boosting 2024 pro forma service revenue by an estimated 12% and adding ~15 million subscribers versus UAE's low single-digit growth.

These emerging markets show annual subscriber growth rates of 3–7% vs UAE ~1%, but integrating PPF assets needs heavy capex—2024–2026 integration capex guided at roughly $2.0–2.5 billion—and higher opex to rebrand and harmonize networks.

Fintech and e& money

e& money, Etisalat Group’s digital finance arm, is a Star in the BCG matrix—growing fast in MENA fintech with a reported 2024 user base exceeding 8 million and year‑on‑year transaction value up ~60% to $9.4 billion.

By leveraging Etisalat’s ~160 million mobile subscribers, e& money is scaling toward a super‑app model (payments, remittances, micro‑lending) but faces fierce competition from regional banks and startups like PayTabs and Tabby.

High market growth (>25% annual fintech expansion in GCC, 2024) supports continued investment; churn and regulatory costs, however, could pressure margins.

- Users: >8M (2024)

- TPV: $9.4B, +60% YoY

- Mobile reach: 160M Etisalat subs

- GCC fintech growth: >25% (2024)

- Competitive risk: banks + fintech startups

AI and Autonomous Technologies

e& (formerly Etisalat Group) leads regional AI and autonomous rollouts—partnering on logistics automation and smart-city ops—backed by a 2025 capex push of ~$1.1B into cloud/AI infrastructure to grab first-mover advantage.

Market signals show rapid demand: regional AI infrastructure spending is forecast to grow ~28% CAGR 2024–2028, and automation can cut logistics costs 15–25% per McKinsey estimates, supporting e&'s strategic bet.

e&'s pilot deployments in 2024 handled thousands of autonomous deliveries and smart-city sensors, signaling scale readiness and high-margin potential versus legacy telco services.

- 2025 capex ~ $1.1B into AI/cloud

- Regional AI infra growth ~28% CAGR (2024–28)

- Logistics cost savings 15–25%

- 2024 pilots: thousands of autonomous ops

e& drives UAE 5G dominance, 8M+ e& money users and $1.1B AI/cloud push

Stars: e& 5G, e& money, and AI/cloud show high growth and strong share—UAE 5G ~60% share, 2025 lines 6.1M (+22%); e& capex AED 6.4bn (2025); e& money >8M users, TPV $9.4B (2024, +60%); AI/cloud capex ~$1.1B (2025), regional AI spend +28% CAGR (2024–28).

| Unit | Metric |

|---|---|

| UAE 5G | 60% share; 6.1M lines (2025) |

| Capex | AED 6.4bn (2025) |

| e& money | >8M users; $9.4B TPV (2024) |

| AI/cloud | $1.1B capex (2025); 28% CAGR |

What is included in the product

Comprehensive BCG review of Etisalat’s units with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page Etisalat BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

UAE Mobile Voice and Data

The UAE mobile voice and data business generates stable free cash flow, accounting for about 45% of Etisalat Group’s UAE EBITDA in 2024 (Etisalat Group FY2024 report), backed by ~78% mobile penetration and a domestic market share near 50% in 2025. With penetration high, year‑over‑year revenue growth has slowed to ~2% in 2024, lowering marketing intensity versus fast‑growing digital units. This steady cash engine funds capex and investments in 5G, cloud, and IoT expansions.

Fixed-line Broadband Services

As the UAE market leader in fixed-line broadband, Etisalat (Emirates Telecommunications Group Company PJSC) holds near-duopoly share with e& (formerly du), controlling about 70–75% of household fixed broadband subscriptions as of 2024.

With fiber rollout largely complete—FTTH coverage ~85% nationwide in 2024—the segment delivers high EBITDA margins near 50% and steady ARPU around AED 200–220, driving strong recurring cash flow.

Those cash flows funded 2024 dividends of AED 6.5 billion and support debt servicing on total net debt ~AED 30 billion, making fixed broadband a core cash cow for Etisalat.

Etisalat Egypt Operations

Etisalat Egypt, now mature with about 32% market share and ~45 million subscribers as of Dec 2025, sits squarely in the Cash Cows quadrant, delivering stable EGP-denominated EBITDA margins near 38% and FY2024 free cash flow around EGP 6.2bn.

Macroeconomic swings (2022–2025 inflation averaging ~26% annually) dent revenue growth, but retention keeps operating cash steady; capex/reinvestment is ~3–4% of revenue, focused on maintenance not new-market expansion.

Carrier and Wholesale Services

e& (Etisalat by e&, Abu Dhabi-listed telco) is a regional hub for international roaming, subsea cable capacity, and wholesale voice, handling ~30% of GCC transit and co-owning 6+ cables; this B2B segment sits in a low-growth global market but yields high EBITDA margins (~35% in 2024) due to scale and long-term contracts.

The business’s extensive fiber and cable footprint creates a durable moat, keeping churn low and capex intensity down; wholesale contributed roughly AED 4.2bn in revenue and >40% operating profit margin in FY 2024, making it a classic cash cow.

- Handles ~30% GCC transit

- Co-owns 6+ subsea cables

- EBITDA ~35% (2024)

- Wholesale revenue ~AED 4.2bn (FY2024)

- Low capex intensity, high margins

Legacy Satellite Communications

Legacy Satellite Communications delivers steady revenue for Etisalat (e&), serving oil, gas, and maritime clients with mature satellite and maritime links; revenue from these services contributed roughly AED 450–500 million in 2024 and showed <1% year-on-year volatility.

Low capex needs and predictable contracts make it a cash cow: EBITDA margins near 40% in 2024 and multi-year contracts underpin cash generation for group operations.

- Stable demand: niche clients in oil, gas, maritime

- Mature tech: low R&D, predictable costs

- 2024 revenue: ~AED 450–500M

- 2024 EBITDA margin: ~40%

- Market volatility: <1% YoY

Etisalat cash cows: UAE mobile, FTTH, Egypt, wholesale & satellite drive steady FCF

Etisalat’s UAE mobile/fixed broadband, Egypt operations, wholesale and satellite are Cash Cows, generating stable free cash flow: UAE mobile ~45% of UAE EBITDA (2024), FTTH coverage ~85% (2024), fixed broadband ARPU AED 200–220, Egypt FCF EGP 6.2bn (FY2024), wholesale revenue AED 4.2bn (FY2024), satellite revenue AED 450–500M (2024).

| Segment | Key 2024–25 metrics |

|---|---|

| UAE mobile | 45% UAE EBITDA; growth ~2% |

| Fixed broadband | FTTH 85%; ARPU AED200–220; EBITDA ~50% |

| Egypt | FCF EGP6.2bn; EBITDA ~38% |

| Wholesale | Revenue AED4.2bn; EBITDA ~35% |

| Satellite | Revenue AED450–500M; EBITDA ~40% |

Preview = Final Product

Etisalat BCG Matrix

The file you're previewing is the exact Etisalat BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready document designed for strategic clarity and professional presentation.