Euronav NV PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

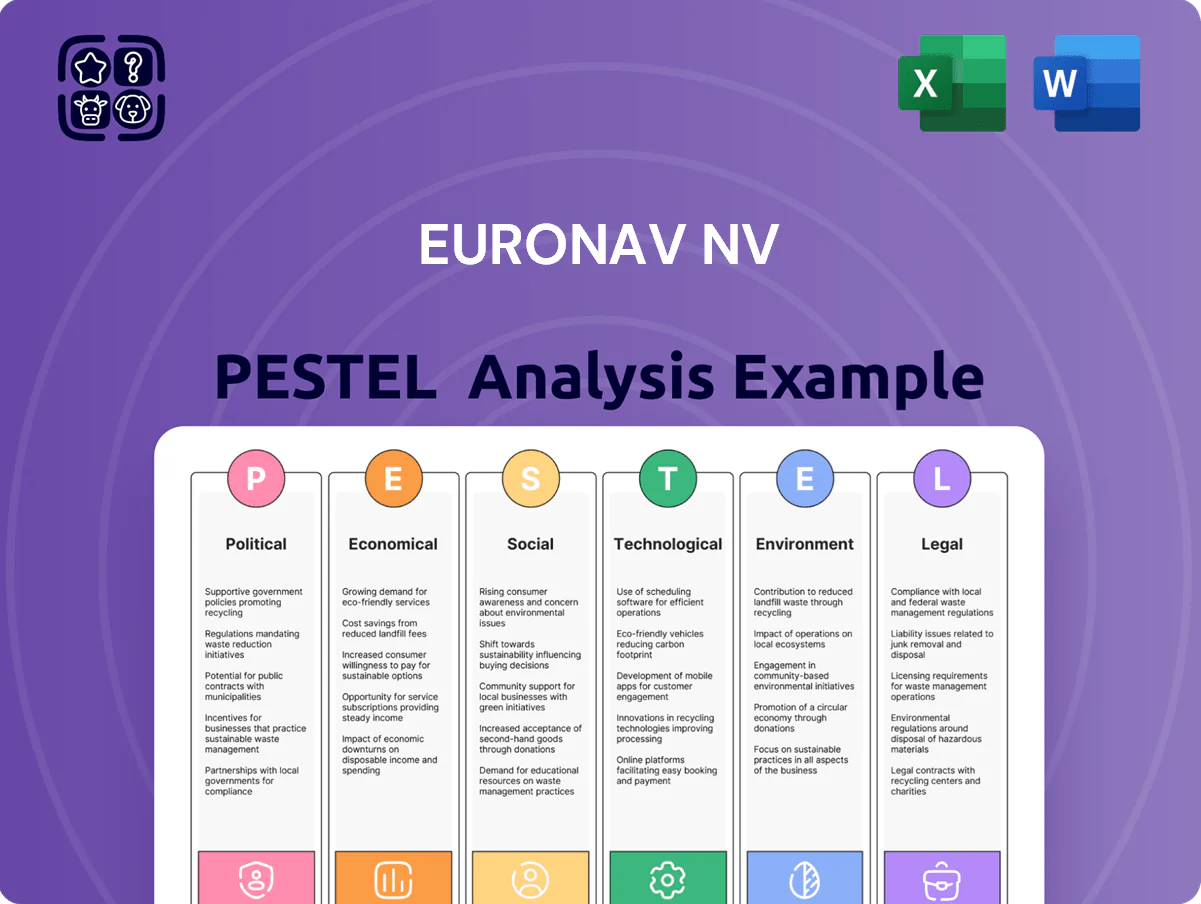

Gain strategic clarity with our PESTLE Analysis of Euronav NV—condensed, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its tanker operations; buy the full report for the complete, actionable breakdown and ready-to-use slides to inform investment or strategic decisions.

Political factors

Geopolitical tensions and trade route security

Ongoing conflicts in the Middle East and Eastern Europe as of late 2025 have led Euronav to reroute ~18-25% of VLCC voyages around the Cape of Good Hope, raising average voyage distances by ~40% and boosting ton-mile demand materially.

Rerouting increased bunker and voyage costs, contributing to a 15-22% uplift in operational expenditures per voyage in 2024–2025 and elevating insurance premiums and incident risks.

Instability at chokepoints like the Suez Canal drives freight rate volatility—spot rates for crude tankers spiked intermittently by 30–60% in 2024–2025—and forces stricter safety and contingency protocols across Euronav fleets.

Energy security and strategic reserves

Governments prioritizing energy sovereignty have driven 2024 SPR drawdowns and 2025 replenishments—IEA reports SPR releases of ~180 Mbbl in 2024 and planned buys of ~150 Mbbl in 2025—causing volatile transatlantic and Asia–Europe crude flows that directly affect Euronav NV VLCC utilization and freight rates.

Sanctions and international trade policy

Enforcement of strict sanctions on major oil producers forces Euronav to sustain robust compliance systems; in 2024 the company reported zero sanctions breaches and increased KYC/AML spend by an estimated 8% to safeguard access to western charters.

Shifts in trade policy between OECD and emerging markets altered crude flows—UNCTAD noted seaborne oil trade rose ~2.5% in 2024—impacting global tanker utilization and Euronav's Suezmax and VLCC deployment rates.

Managing diplomatic complexity is critical for retaining contracts with oil majors: Euronav's 2024 time-charter equivalent (TCE) volatility highlighted the premium placed on politically resilient carriers.

Influence of CMB.TECH integration

The 2023 takeover by CMB shifted Euronav toward Belgian industrial priorities and green hydrogen projects, aligning company strategy with EU decarbonisation goals and making it eligible for Belgian/EU green funding streams; CMB ownership increased access to regional ports and hydrogen corridors critical for low-carbon bunkering.

This political backing improves prospects for securing subsidies for fleet renewal—EU Fit for 55 and Innovation Fund allocations; Euronav could target grants covering up to 30–40% of retrofit/newbuild costs based on recent EU schemes.

- Stronger Belgian/EU political alignment

- Improved access to hydrogen corridors and ports

- Higher eligibility for EU/Belgian subsidies (potentially 30–40% of costs)

OPEC plus production quotas

Decisions by OPEC+ on production quotas directly determine crude volumes and thus cargo availability for Euronav's VLCCs and Suezmaxes; in 2025 OPEC+ cuts of 1.2 mb/d announced in late 2024 tightened exports, reducing seaborne flows and lifting freight rates.

Euronav's commercial teams must reposition ~70-vessel fleet in response to these shifts—political cohesion or fragmentation of OPEC+ remains a principal driver of global export volumes in 2025.

- OPEC+ cuts ~1.2 mb/d (late 2024) reduced seaborne exports

- Freight rates rose as ton-miles tightened in early 2025

- Euronav fleet repositioning key to capture redirected cargoes

Suez reroutes, OPEC+ cuts fuel tanker costs, rates and green funding shakeup

Political instability and chokepoint disruptions (Suez reroutes) raised VLCC voyage distances ~40%, boosting ton-mile demand and lifting 2024–25 voyage OPEX 15–22%; spot crude tanker rates spiked 30–60% intermittently. EU/Belgian backing after CMB takeover improved access to hydrogen corridors and increased eligibility for green funding (potentially covering 30–40% of retrofit/newbuild costs). OPEC+ cuts (~1.2 mb/d late 2024) tightened seaborne flows, increasing TCE volatility and forcing fleet repositioning.

| Metric | Value (2024–25) |

|---|---|

| VLCC reroute distance ↑ | ~40% |

| OPEX per voyage ↑ | 15–22% |

| Spot rate spikes | 30–60% |

| OPEC+ cuts | ~1.2 mb/d |

| EU grant potential | 30–40% of costs |

What is included in the product

Explores how external macro-environmental factors uniquely affect Euronav NV across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented Euronav NV PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Volatility in freight rates

The VLCC and Suezmax spot markets remain highly sensitive to global oil supply/demand shifts; VLCC spot rates averaged around 32,000 USD/day in 2024 with spikes above 80,000 USD/day during tight periods, amplifying revenue swings for Euronav NV.

Economic cycles in China and India drive tanker demand—China crude imports rose ~4% in 2024 and India remained the world’s top crude importer—directly affecting Euronav’s daily earnings volatility.

While elevated rates in 2024 improved profitability, the sector’s inherent volatility and multiyear lows (below 10,000 USD/day in downturns) necessitate Euronav’s robust balance sheet and liquidity to absorb shocks.

Global inflation and interest rate environment

Persistent global inflation—headline CPI averaging ~5.8% in 2024 across major economies—raises Euronav’s operating costs via higher prices for spare parts, maintenance and crew wages, adding pressure to operating margins. Higher policy rates (Fed ~5.25–5.50% in 2024; ECB ~4.00%) increase borrowing costs, pushing all-in yields on new ship finance well above historical lows and raising capital costs for newbuilding projects. Euronav must therefore balance fleet renewal and investment in eco-friendly tankers with more expensive financing, impacting payback periods and fleet expansion timing.

Fuel price fluctuations and bunker costs

As a major consumer of marine fuels, Euronav faces high exposure to Very Low Sulphur Fuel Oil (VLSFO) prices; VLSFO averaged about $520/ton in 2024, pushing bunker costs to roughly 20–30% of voyage expenses for VLCCs.

Refining sector shifts and a 2024 global crude oil average of ~$86/barrel directly influence voyage costs and tightened net margins, with bunker cost volatility contributing to earnings variability quarter-to-quarter.

Adoption of dual-fuel and alternative fuels like LNG and biofuels—Euronav reported retrofits and partnerships targeting 10–15% fleet dual-fuel capability by 2025—acts as a hedge against traditional fuel price swings and regulatory fuel-cost risk.

Shift in global oil demand centers

- Asia Pacific crude imports +1.2 mbd (2019–2024)

- VLCC tonne-mile demand +6% YoY (2024)

- India refining +1.2 mbd capacity by 2025

- India GDP ~6.5% and ASEAN ~4.6% in 2024

Currency exchange rate risks

Euronav earns most revenue in USD while certain operating costs and dividend payouts are Euro-linked; with EUR/USD moving about 1.05–1.12 in 2024–2025, a 5% USD depreciation vs EUR could cut reported EUR earnings similarly, affecting EPS and dividend cover.

The company uses active treasury hedging—for example forward contracts and FX swaps—to stabilize cash flows and protect shareholder returns amid FX volatility and lower freight rate predictability.

- Revenue base: predominantly USD; costs/dividends: partially EUR

- EUR/USD range 2024–2025: ~1.05–1.12; 5% USD move materially affects EUR results

- Mitigation: forwards, swaps, active treasury management to stabilize cash flows

Euronav rides volatile tanker markets: VLCC $32k avg, spikes $80k+, rising costs

Economic volatility drives Euronav: VLCC spot avg ~$32k/day (2024) with spikes >$80k; VLSFO ~$520/ton; Brent ~$86/bbl (2024); Asia import +1.2 mbd (2019–24) raising tonne-miles +6% YoY; China/India demand and higher policy rates (Fed ~5.25–5.50%, ECB ~4.0%) raise financing and operating costs; EUR/USD ~1.05–1.12—FX hedging used to protect USD revenue.

| Metric | 2024 |

|---|---|

| VLCC spot (avg) | $32,000/day |

| VLSFO | $520/ton |

| Brent | $86/bbl |

| Asia crude growth | +1.2 mbd |

Same Document Delivered

Euronav NV PESTLE Analysis

The preview shown here is the exact Euronav NV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and layout visible here are the final file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of Euronav NV—condensed, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its tanker operations; buy the full report for the complete, actionable breakdown and ready-to-use slides to inform investment or strategic decisions.

Political factors

Geopolitical tensions and trade route security

Ongoing conflicts in the Middle East and Eastern Europe as of late 2025 have led Euronav to reroute ~18-25% of VLCC voyages around the Cape of Good Hope, raising average voyage distances by ~40% and boosting ton-mile demand materially.

Rerouting increased bunker and voyage costs, contributing to a 15-22% uplift in operational expenditures per voyage in 2024–2025 and elevating insurance premiums and incident risks.

Instability at chokepoints like the Suez Canal drives freight rate volatility—spot rates for crude tankers spiked intermittently by 30–60% in 2024–2025—and forces stricter safety and contingency protocols across Euronav fleets.

Energy security and strategic reserves

Governments prioritizing energy sovereignty have driven 2024 SPR drawdowns and 2025 replenishments—IEA reports SPR releases of ~180 Mbbl in 2024 and planned buys of ~150 Mbbl in 2025—causing volatile transatlantic and Asia–Europe crude flows that directly affect Euronav NV VLCC utilization and freight rates.

Sanctions and international trade policy

Enforcement of strict sanctions on major oil producers forces Euronav to sustain robust compliance systems; in 2024 the company reported zero sanctions breaches and increased KYC/AML spend by an estimated 8% to safeguard access to western charters.

Shifts in trade policy between OECD and emerging markets altered crude flows—UNCTAD noted seaborne oil trade rose ~2.5% in 2024—impacting global tanker utilization and Euronav's Suezmax and VLCC deployment rates.

Managing diplomatic complexity is critical for retaining contracts with oil majors: Euronav's 2024 time-charter equivalent (TCE) volatility highlighted the premium placed on politically resilient carriers.

Influence of CMB.TECH integration

The 2023 takeover by CMB shifted Euronav toward Belgian industrial priorities and green hydrogen projects, aligning company strategy with EU decarbonisation goals and making it eligible for Belgian/EU green funding streams; CMB ownership increased access to regional ports and hydrogen corridors critical for low-carbon bunkering.

This political backing improves prospects for securing subsidies for fleet renewal—EU Fit for 55 and Innovation Fund allocations; Euronav could target grants covering up to 30–40% of retrofit/newbuild costs based on recent EU schemes.

- Stronger Belgian/EU political alignment

- Improved access to hydrogen corridors and ports

- Higher eligibility for EU/Belgian subsidies (potentially 30–40% of costs)

OPEC plus production quotas

Decisions by OPEC+ on production quotas directly determine crude volumes and thus cargo availability for Euronav's VLCCs and Suezmaxes; in 2025 OPEC+ cuts of 1.2 mb/d announced in late 2024 tightened exports, reducing seaborne flows and lifting freight rates.

Euronav's commercial teams must reposition ~70-vessel fleet in response to these shifts—political cohesion or fragmentation of OPEC+ remains a principal driver of global export volumes in 2025.

- OPEC+ cuts ~1.2 mb/d (late 2024) reduced seaborne exports

- Freight rates rose as ton-miles tightened in early 2025

- Euronav fleet repositioning key to capture redirected cargoes

Suez reroutes, OPEC+ cuts fuel tanker costs, rates and green funding shakeup

Political instability and chokepoint disruptions (Suez reroutes) raised VLCC voyage distances ~40%, boosting ton-mile demand and lifting 2024–25 voyage OPEX 15–22%; spot crude tanker rates spiked 30–60% intermittently. EU/Belgian backing after CMB takeover improved access to hydrogen corridors and increased eligibility for green funding (potentially covering 30–40% of retrofit/newbuild costs). OPEC+ cuts (~1.2 mb/d late 2024) tightened seaborne flows, increasing TCE volatility and forcing fleet repositioning.

| Metric | Value (2024–25) |

|---|---|

| VLCC reroute distance ↑ | ~40% |

| OPEX per voyage ↑ | 15–22% |

| Spot rate spikes | 30–60% |

| OPEC+ cuts | ~1.2 mb/d |

| EU grant potential | 30–40% of costs |

What is included in the product

Explores how external macro-environmental factors uniquely affect Euronav NV across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented Euronav NV PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Volatility in freight rates

The VLCC and Suezmax spot markets remain highly sensitive to global oil supply/demand shifts; VLCC spot rates averaged around 32,000 USD/day in 2024 with spikes above 80,000 USD/day during tight periods, amplifying revenue swings for Euronav NV.

Economic cycles in China and India drive tanker demand—China crude imports rose ~4% in 2024 and India remained the world’s top crude importer—directly affecting Euronav’s daily earnings volatility.

While elevated rates in 2024 improved profitability, the sector’s inherent volatility and multiyear lows (below 10,000 USD/day in downturns) necessitate Euronav’s robust balance sheet and liquidity to absorb shocks.

Global inflation and interest rate environment

Persistent global inflation—headline CPI averaging ~5.8% in 2024 across major economies—raises Euronav’s operating costs via higher prices for spare parts, maintenance and crew wages, adding pressure to operating margins. Higher policy rates (Fed ~5.25–5.50% in 2024; ECB ~4.00%) increase borrowing costs, pushing all-in yields on new ship finance well above historical lows and raising capital costs for newbuilding projects. Euronav must therefore balance fleet renewal and investment in eco-friendly tankers with more expensive financing, impacting payback periods and fleet expansion timing.

Fuel price fluctuations and bunker costs

As a major consumer of marine fuels, Euronav faces high exposure to Very Low Sulphur Fuel Oil (VLSFO) prices; VLSFO averaged about $520/ton in 2024, pushing bunker costs to roughly 20–30% of voyage expenses for VLCCs.

Refining sector shifts and a 2024 global crude oil average of ~$86/barrel directly influence voyage costs and tightened net margins, with bunker cost volatility contributing to earnings variability quarter-to-quarter.

Adoption of dual-fuel and alternative fuels like LNG and biofuels—Euronav reported retrofits and partnerships targeting 10–15% fleet dual-fuel capability by 2025—acts as a hedge against traditional fuel price swings and regulatory fuel-cost risk.

Shift in global oil demand centers

- Asia Pacific crude imports +1.2 mbd (2019–2024)

- VLCC tonne-mile demand +6% YoY (2024)

- India refining +1.2 mbd capacity by 2025

- India GDP ~6.5% and ASEAN ~4.6% in 2024

Currency exchange rate risks

Euronav earns most revenue in USD while certain operating costs and dividend payouts are Euro-linked; with EUR/USD moving about 1.05–1.12 in 2024–2025, a 5% USD depreciation vs EUR could cut reported EUR earnings similarly, affecting EPS and dividend cover.

The company uses active treasury hedging—for example forward contracts and FX swaps—to stabilize cash flows and protect shareholder returns amid FX volatility and lower freight rate predictability.

- Revenue base: predominantly USD; costs/dividends: partially EUR

- EUR/USD range 2024–2025: ~1.05–1.12; 5% USD move materially affects EUR results

- Mitigation: forwards, swaps, active treasury management to stabilize cash flows

Euronav rides volatile tanker markets: VLCC $32k avg, spikes $80k+, rising costs

Economic volatility drives Euronav: VLCC spot avg ~$32k/day (2024) with spikes >$80k; VLSFO ~$520/ton; Brent ~$86/bbl (2024); Asia import +1.2 mbd (2019–24) raising tonne-miles +6% YoY; China/India demand and higher policy rates (Fed ~5.25–5.50%, ECB ~4.0%) raise financing and operating costs; EUR/USD ~1.05–1.12—FX hedging used to protect USD revenue.

| Metric | 2024 |

|---|---|

| VLCC spot (avg) | $32,000/day |

| VLSFO | $520/ton |

| Brent | $86/bbl |

| Asia crude growth | +1.2 mbd |

Same Document Delivered

Euronav NV PESTLE Analysis

The preview shown here is the exact Euronav NV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and layout visible here are the final file you’ll be able to download immediately after payment.