Eurotech PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech disruption are shaping Eurotech’s outlook with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context; purchase the full analysis to access the complete, editable report and make smarter decisions today.

Political factors

Geopolitical Trade Tensions

The ongoing trade friction between major powers in late 2025 has raised semiconductor tariffs and export controls, contributing to a 7–12% increase in component costs for European electronics firms year‑over‑year; Eurotech faces higher procurement expenses and potential market access limits in China and the US.

Shifting tariffs and sanctions force Eurotech to reassess supply routes: diversifying suppliers reduced similar firms' single‑source exposure from 45% to under 25% in 2024, a benchmark Eurotech aims to match to protect margins and delivery reliability.

European Strategic Autonomy

As a European-based firm, Eurotech benefits from EU strategic autonomy drives such as the 2023 EU Chips Act, which includes a 43 billion euro EU funding mobilization target to boost semiconductor capacity and R&D across the bloc.

Strong government incentives and grants—EU and member-state programs pledging tens of billions through 2024–25—favor companies aligned with regional security and supply-chain resilience objectives.

This political momentum accelerates domestic capability building, reducing reliance on non-European providers and expanding market opportunities for Eurotech in secure, funded projects.

Government Digitalization Subsidies

Public investment in digitalizing critical infrastructure—EU Recovery and Resilience Facility committed over €200bn to digital and green projects through 2021–2026—drives IoT uptake, with national programs offering grants and tax credits for edge computing in energy and transport; e.g., Germany’s €7bn grid modernization funding and Italy’s 2024 tax incentives for smart infrastructure boost demand. Eurotech can target public/regulatory tenders to secure multi-year contracts and predictable revenue streams.

National Security Infrastructure Protection

Governments are tightening oversight on hardware and software for essential services to counter cyber warfare and espionage, with EU investment in cybersecurity rising to €10.7 billion in 2024 under the NIS2 and EU Cybersecurity Strategy.

This political environment favors Eurotech, whose ruggedized, secure embedded systems meet military and industrial reliability standards and align with stricter procurement rules.

Vetting processes for vendors in critical sectors prioritize trusted Western suppliers, giving Eurotech a competitive advantage reflected in increased defense and critical-infrastructure contracts across 2024–2025.

- EU cybersecurity budget €10.7B in 2024

- Higher procurement scrutiny benefits established Western vendors

- Eurotech’s rugged secure systems align with NIS2 requirements

Export Control on AI Technologies

The EU and US tightened export controls in 2023–2024, with US BIS rules covering AI semiconductors and HPC; affected markets saw a 12–18% reduction in cross-border hardware shipments, constraining Eurotech’s edge AI platform distribution.

Eurotech must enforce ISO-aligned compliance, allocate ~€2–4m annually to export-control risk management, and may face blocked entry into select APAC and MENA jurisdictions, raising go-to-market costs.

- 2023–24 export-rule-driven shipment drop: 12–18%

Eurotech pivots suppliers, adds €2–4m compliance spend as EU funding boosts secure edge demand

Geopolitical trade tensions and 2023–24 export controls raised component costs 7–12% and cut cross-border hardware shipments 12–18%, pushing Eurotech to diversify suppliers to <25% single-source exposure and spend ~€2–4m/yr on export-compliance; EU funding (Chips Act €43bn target) and cybersecurity budgets (€10.7bn in 2024) create funded demand for Eurotech’s secure edge systems.

| Metric | Value |

|---|---|

| Component cost rise | 7–12% |

| Shipment drop | 12–18% |

| Single-source target | <25% |

| Export compliance spend | €2–4m/yr |

| EU Chips Act funding | €43bn target |

| EU cybersecurity 2024 | €10.7bn |

What is included in the product

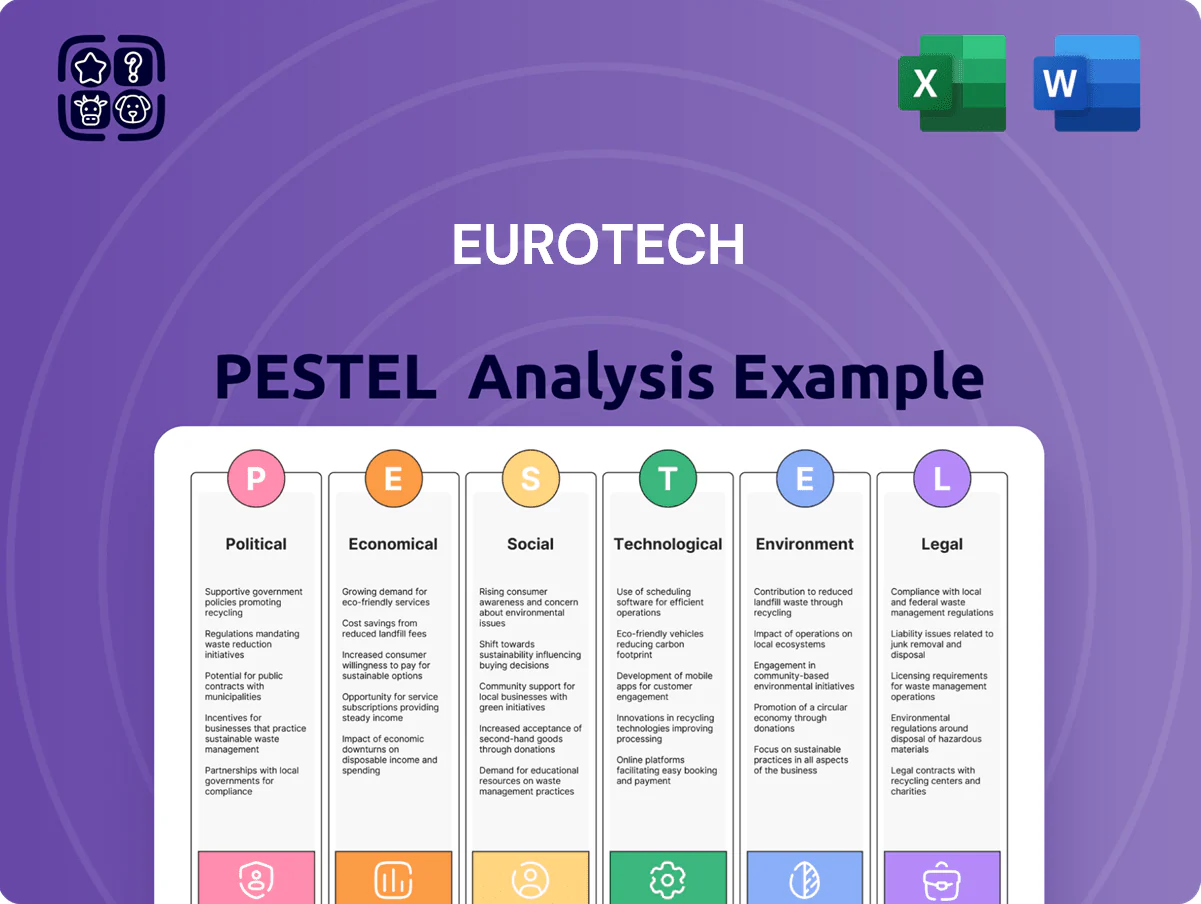

Explores how external macro-environmental factors uniquely affect Eurotech across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and industry-specific examples.

A concise, visually segmented PESTLE summary for Eurotech that distills external risks and opportunities into an easily shareable slide or handout, ideal for quick alignment across teams and decision-making in planning sessions.

Economic factors

Industrial Capital Expenditure Trends

Industrial capex for automation and IoT is tightening as global policy rates averaged ~3.8% in 2025 and US corporate margins slipped to 9.6% H2 2025, prompting firms to delay hardware-heavy projects until ROI exceeds higher financing costs.

Surveys show 42% of manufacturers postponed major automation buys in 2025; Eurotech’s revenue sensitivity to cyclical capex means order flows and backlog realization correlate strongly with these upgrade cycles.

Global Supply Chain Cost Volatility

Fluctuations in prices for specialized materials and energy pushed Eurotech’s component and manufacturing costs up an estimated 6–9% in 2024, while global logistics rates—still ~30% above pre‑pandemic levels per Drewry—keep margins under pressure; although bottlenecks eased versus 2021–22, high‑grade semiconductors remain volatile with spot price swings of 10–20%. Eurotech needs dynamic pricing and tiered contracts to protect EBITDA without losing price‑sensitive industrial clients.

Currency Exchange Rate Fluctuations

Eurotech’s global operations expose it to EUR/USD and other major currency swings; between 2023–2025 the euro moved ~8–10% against the dollar, which can widen margins or erode competitiveness in key markets.

Exchange shifts raise imported component costs—Eurotech reported ~22% of COGS from non-euro suppliers in 2024—pressuring prices unless offset.

Financial hedging (forwards/options) and localized production or invoicing helped peers cut FX impact by up to 60% in 2024 and are critical risk mitigants for Eurotech.

Inflationary Pressures on Raw Materials

Persistent inflation in rare earth metals and high-grade plastics—prices up roughly 18–27% YoY in 2024 for neodymium/praseodymium and specialty polymers—squeezes margins on Eurotech ruggedized equipment, reducing gross margins unless costs are passed on.

Eurotech must choose between pricing power or internal efficiencies; supply-chain optimization and design-for-cost could offset rising input costs bearing on 2024–25 EBIT margins.

Securing long-term fixed-price supply contracts is a critical stabilizer; hedges or multi-year agreements covering 40–60% of key inputs can materially reduce volatility.

- Rare earths +18–27% YoY (2024)

- Specialty plastics significant price inflation

- Hedges/long-term contracts reduce volatility

- Design/cost efficiencies protect EBIT margins

Labor Market Competition for Tech Talent

The surge in demand for edge AI and IoT engineers has pushed global tech hiring costs up; median European senior AI engineer salaries rose ~18% in 2024 to €95k–€120k, tightening margins for Eurotech.

Higher wage bills and recruiting premiums can raise operating expenses by an estimated 5–8% annually, pressuring EBITDA unless offset by productivity gains or price increases.

Eurotech must prioritize retention, upskilling, and employer brand investment—benchmarks show companies reducing churn by 20–30% after targeted retention programs.

- European senior AI engineer median salary 2024: €95k–€120k

- Estimated annual operating expense impact: +5–8%

- Retention programs can cut churn 20–30%

Manufacturing pauses as costs, FX and AI wages surge—hedge 40–60% to cut volatility

Industrial capex slowed as 2025 policy rates averaged ~3.8%, with 42% of manufacturers delaying automation; Eurotech saw 6–9% higher component costs in 2024 and EUR/USD swings of ~8–10% (2023–25). Wage inflation: senior AI salaries €95k–€120k (+18% 2024), adding ~5–8% Opex. Hedging/long-term contracts covering 40–60% of inputs cut FX and input volatility up to 60%.

| Metric | Value |

|---|---|

| Policy rates 2025 | ~3.8% |

| Manufacturers delaying buys | 42% |

| Component cost rise 2024 | 6–9% |

| EUR/USD move 2023–25 | 8–10% |

| Senior AI salary 2024 | €95k–€120k |

| Opex impact | +5–8% |

| Hedge coverage suggested | 40–60% |

Preview Before You Purchase

Eurotech PESTLE Analysis

The preview shown here is the exact Eurotech PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file you’re buying, with no placeholders or teasers, and the layout, content, and structure match the downloadable product. After checkout you’ll instantly get this exact, professionally structured file. What you see is what you’ll be working with.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech disruption are shaping Eurotech’s outlook with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context; purchase the full analysis to access the complete, editable report and make smarter decisions today.

Political factors

Geopolitical Trade Tensions

The ongoing trade friction between major powers in late 2025 has raised semiconductor tariffs and export controls, contributing to a 7–12% increase in component costs for European electronics firms year‑over‑year; Eurotech faces higher procurement expenses and potential market access limits in China and the US.

Shifting tariffs and sanctions force Eurotech to reassess supply routes: diversifying suppliers reduced similar firms' single‑source exposure from 45% to under 25% in 2024, a benchmark Eurotech aims to match to protect margins and delivery reliability.

European Strategic Autonomy

As a European-based firm, Eurotech benefits from EU strategic autonomy drives such as the 2023 EU Chips Act, which includes a 43 billion euro EU funding mobilization target to boost semiconductor capacity and R&D across the bloc.

Strong government incentives and grants—EU and member-state programs pledging tens of billions through 2024–25—favor companies aligned with regional security and supply-chain resilience objectives.

This political momentum accelerates domestic capability building, reducing reliance on non-European providers and expanding market opportunities for Eurotech in secure, funded projects.

Government Digitalization Subsidies

Public investment in digitalizing critical infrastructure—EU Recovery and Resilience Facility committed over €200bn to digital and green projects through 2021–2026—drives IoT uptake, with national programs offering grants and tax credits for edge computing in energy and transport; e.g., Germany’s €7bn grid modernization funding and Italy’s 2024 tax incentives for smart infrastructure boost demand. Eurotech can target public/regulatory tenders to secure multi-year contracts and predictable revenue streams.

National Security Infrastructure Protection

Governments are tightening oversight on hardware and software for essential services to counter cyber warfare and espionage, with EU investment in cybersecurity rising to €10.7 billion in 2024 under the NIS2 and EU Cybersecurity Strategy.

This political environment favors Eurotech, whose ruggedized, secure embedded systems meet military and industrial reliability standards and align with stricter procurement rules.

Vetting processes for vendors in critical sectors prioritize trusted Western suppliers, giving Eurotech a competitive advantage reflected in increased defense and critical-infrastructure contracts across 2024–2025.

- EU cybersecurity budget €10.7B in 2024

- Higher procurement scrutiny benefits established Western vendors

- Eurotech’s rugged secure systems align with NIS2 requirements

Export Control on AI Technologies

The EU and US tightened export controls in 2023–2024, with US BIS rules covering AI semiconductors and HPC; affected markets saw a 12–18% reduction in cross-border hardware shipments, constraining Eurotech’s edge AI platform distribution.

Eurotech must enforce ISO-aligned compliance, allocate ~€2–4m annually to export-control risk management, and may face blocked entry into select APAC and MENA jurisdictions, raising go-to-market costs.

- 2023–24 export-rule-driven shipment drop: 12–18%

Eurotech pivots suppliers, adds €2–4m compliance spend as EU funding boosts secure edge demand

Geopolitical trade tensions and 2023–24 export controls raised component costs 7–12% and cut cross-border hardware shipments 12–18%, pushing Eurotech to diversify suppliers to <25% single-source exposure and spend ~€2–4m/yr on export-compliance; EU funding (Chips Act €43bn target) and cybersecurity budgets (€10.7bn in 2024) create funded demand for Eurotech’s secure edge systems.

| Metric | Value |

|---|---|

| Component cost rise | 7–12% |

| Shipment drop | 12–18% |

| Single-source target | <25% |

| Export compliance spend | €2–4m/yr |

| EU Chips Act funding | €43bn target |

| EU cybersecurity 2024 | €10.7bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Eurotech across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and industry-specific examples.

A concise, visually segmented PESTLE summary for Eurotech that distills external risks and opportunities into an easily shareable slide or handout, ideal for quick alignment across teams and decision-making in planning sessions.

Economic factors

Industrial Capital Expenditure Trends

Industrial capex for automation and IoT is tightening as global policy rates averaged ~3.8% in 2025 and US corporate margins slipped to 9.6% H2 2025, prompting firms to delay hardware-heavy projects until ROI exceeds higher financing costs.

Surveys show 42% of manufacturers postponed major automation buys in 2025; Eurotech’s revenue sensitivity to cyclical capex means order flows and backlog realization correlate strongly with these upgrade cycles.

Global Supply Chain Cost Volatility

Fluctuations in prices for specialized materials and energy pushed Eurotech’s component and manufacturing costs up an estimated 6–9% in 2024, while global logistics rates—still ~30% above pre‑pandemic levels per Drewry—keep margins under pressure; although bottlenecks eased versus 2021–22, high‑grade semiconductors remain volatile with spot price swings of 10–20%. Eurotech needs dynamic pricing and tiered contracts to protect EBITDA without losing price‑sensitive industrial clients.

Currency Exchange Rate Fluctuations

Eurotech’s global operations expose it to EUR/USD and other major currency swings; between 2023–2025 the euro moved ~8–10% against the dollar, which can widen margins or erode competitiveness in key markets.

Exchange shifts raise imported component costs—Eurotech reported ~22% of COGS from non-euro suppliers in 2024—pressuring prices unless offset.

Financial hedging (forwards/options) and localized production or invoicing helped peers cut FX impact by up to 60% in 2024 and are critical risk mitigants for Eurotech.

Inflationary Pressures on Raw Materials

Persistent inflation in rare earth metals and high-grade plastics—prices up roughly 18–27% YoY in 2024 for neodymium/praseodymium and specialty polymers—squeezes margins on Eurotech ruggedized equipment, reducing gross margins unless costs are passed on.

Eurotech must choose between pricing power or internal efficiencies; supply-chain optimization and design-for-cost could offset rising input costs bearing on 2024–25 EBIT margins.

Securing long-term fixed-price supply contracts is a critical stabilizer; hedges or multi-year agreements covering 40–60% of key inputs can materially reduce volatility.

- Rare earths +18–27% YoY (2024)

- Specialty plastics significant price inflation

- Hedges/long-term contracts reduce volatility

- Design/cost efficiencies protect EBIT margins

Labor Market Competition for Tech Talent

The surge in demand for edge AI and IoT engineers has pushed global tech hiring costs up; median European senior AI engineer salaries rose ~18% in 2024 to €95k–€120k, tightening margins for Eurotech.

Higher wage bills and recruiting premiums can raise operating expenses by an estimated 5–8% annually, pressuring EBITDA unless offset by productivity gains or price increases.

Eurotech must prioritize retention, upskilling, and employer brand investment—benchmarks show companies reducing churn by 20–30% after targeted retention programs.

- European senior AI engineer median salary 2024: €95k–€120k

- Estimated annual operating expense impact: +5–8%

- Retention programs can cut churn 20–30%

Manufacturing pauses as costs, FX and AI wages surge—hedge 40–60% to cut volatility

Industrial capex slowed as 2025 policy rates averaged ~3.8%, with 42% of manufacturers delaying automation; Eurotech saw 6–9% higher component costs in 2024 and EUR/USD swings of ~8–10% (2023–25). Wage inflation: senior AI salaries €95k–€120k (+18% 2024), adding ~5–8% Opex. Hedging/long-term contracts covering 40–60% of inputs cut FX and input volatility up to 60%.

| Metric | Value |

|---|---|

| Policy rates 2025 | ~3.8% |

| Manufacturers delaying buys | 42% |

| Component cost rise 2024 | 6–9% |

| EUR/USD move 2023–25 | 8–10% |

| Senior AI salary 2024 | €95k–€120k |

| Opex impact | +5–8% |

| Hedge coverage suggested | 40–60% |

Preview Before You Purchase

Eurotech PESTLE Analysis

The preview shown here is the exact Eurotech PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file you’re buying, with no placeholders or teasers, and the layout, content, and structure match the downloadable product. After checkout you’ll instantly get this exact, professionally structured file. What you see is what you’ll be working with.