Evergy Boston Consulting Group Matrix

Unlock Strategic Clarity

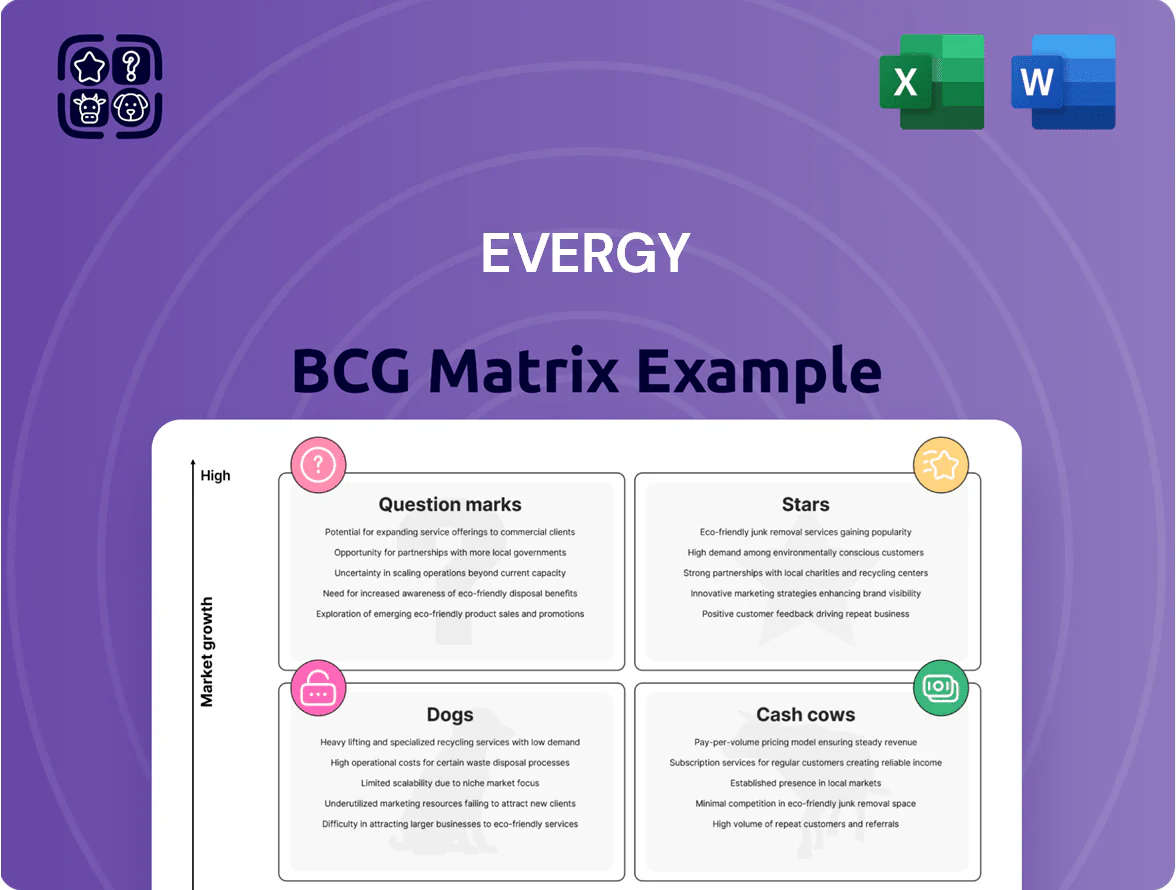

Evergy’s BCG Matrix preview highlights how its core segments—regulated utility operations, renewable investments, and emerging energy services—stack up by market share and growth potential, revealing likely Cash Cows and budding Question Marks. This snapshot suggests where Evergy can harvest stable cash flows versus where it should invest to capture future growth amid grid modernization and decarbonization trends. The full BCG Matrix delivers quadrant-by-quadrant placement, data-backed strategic moves, and actionable recommendations. Purchase the complete report for a ready-to-use Word and Excel package that guides capital allocation and competitive strategy.

Stars

Renewable Energy Portfolio Expansion

Evergy has shifted its generation mix to 42% renewables by 2024, mainly wind and solar, to meet Kansas/Missouri mandates and a 50% carbon reduction target by 2030.

These assets hold roughly 35% regional market share in intermittent renewables and sit in a high-growth segment as fossil generation falls ~18% 2020–2025.

Evergy spent $1.1 billion on renewables and grid upgrades in 2024 and plans ~ $3.2 billion capex through 2026 to keep leadership as the market matures.

Grid Modernization and Digitalization

Evergy is investing roughly $2.3 billion through 2027 in smart grid upgrades—sensors, two-way meters, and grid software—to boost reliability and enable distributed energy flows for renewables and EVs.

Demand for grid modernization is rising: regional outage minutes fell 18% where upgrades completed, while investments respond to increased extreme-weather losses (Midwest insured losses rose 35% 2015–2024) and growing cyber threats.

These heavy capital expenditures compress near-term free cash flow but position Evergy as a tech leader in utilities, supporting higher tariff petitions and potential grid-service revenue streams estimated at $40–60 million annually by 2030.

Electric Vehicle Infrastructure

Evergy, via its Clean Charge Network and public-private deals, leads the regional EV charging market; by 2025 U.S. EV registrations hit ~3.2M (IEA/EDTA data) boosting utility charging demand 40% YoY in many Midwestern corridors.

This high-growth Stars segment could contribute materially to future revenue—Evergy projects network EBITDA margins near 20% by 2026 if adoption keeps rising and utilization exceeds 30%.

Continued capex—estimated $50–75M through 2026—is needed to defend share versus third-party providers like ChargePoint and EVgo entering the region.

Utility-Scale Battery Storage

Utility-Scale Battery Storage: large-scale storage balances intermittent wind and solar and stabilizes the grid at peak demand; industry projections show US utility battery capacity grew 45% in 2024 to ~5.2 GW (SEIA/EIA data).

Evergy leads deployments in the Southwest Power Pool, operating multiple MW-scale projects and holding ~15% market share of announced SPP storage capacity as of Dec 2025; projects are capital intensive and currently cash-consuming.

This high-growth segment is investment-heavy now but is forecasted to deliver steady regulated returns and support decarbonization—storage LCOE fell ~30% since 2020, improving project IRRs and grid value.

- 2024 US utility battery capacity ~5.2 GW (+45% YoY)

- Evergy ~15% share of announced SPP storage (Dec 2025)

- Storage LCOE down ~30% since 2020

- Currently cash-consuming; long-term regulated returns expected

Regional Transmission Projects

Regional Transmission Projects: Expanding high-voltage lines moves wind from rural Kansas to cities; Evergy’s regulated transmission segment earned ~35% of 2024 capex (~$420M of $1.2B) and holds a leading regional share backed by state-approved ratebase recovery, matching rising interconnection requests (MISO filed ~50 GW active in 2024).

These projects are capital intensive but strategic—project IRRs often 6–9% after regulatory allowance, enabling Evergy to defend market dominance as Midwest renewables grow; expected transmission spend in 2025–2027 is $1.8B per regional plans.

- 35% of Evergy 2024 capex: ~$420M

- MISO 2024 interconnection backlog: ~50 GW

- Projected regional transmission spend 2025–2027: ~$1.8B

- Typical regulated IRR: 6–9%

Evergy’s Growth Play: 42% Renewables, Big Storage & $3.2B Capex Through 2026

Evergy’s Stars: renewables, storage, transmission—42% renewables (2024), ~35% regional renewables share, $1.1B renewables/grid spend 2024, $3.2B capex thru 2026; storage ~15% SPP announced share (Dec 2025), US utility battery 5.2 GW (2024); transmission $420M capex (2024), projected $1.8B 2025–27.

| Metric | Value |

|---|---|

| Renewables % (2024) | 42% |

| Regional share | ~35% |

| 2024 renew/grid spend | $1.1B |

| Capex thru 2026 | $3.2B |

| US battery (2024) | 5.2 GW |

| Evergy SPP storage share | ~15% |

| Transm. 2024 capex | $420M |

| Transm. 2025–27 proj | $1.8B |

What is included in the product

Comprehensive BCG Matrix of Evergy: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page BCG Matrix placing Evergy’s units into clear quadrants for fast strategic decisions.

Cash Cows

Regulated Electricity Distribution

Evergy’s regulated electricity distribution serves 1.6 million customers in Kansas and Missouri, generating steady cash flow—Evergy reported $2.1 billion operating cash flow in 2024, largely from core distribution services.

Markets are mature with low volume growth; Evergy holds de facto monopoly shares in many service territories, enabling regulated returns and predictable margins (2024 ROR ~8.5%).

These stable revenues fund a $0.505 annual dividend in 2024 and bankroll renewable investments—Evergy committed $1.2 billion to clean energy projects through 2025.

Wolf Creek Nuclear Station

Wolf Creek Nuclear Station supplies about 1,200 MW of carbon-free baseload power, representing roughly 40–50% of Evergy’s regional generation mix in 2025 and giving the company a dominant market share in steady output.

As a mature plant online since 1985, Wolf Creek needs relatively low growth capex—estimated routine maintenance of ~$40–60 million annually—while generating high daily cash flow that supports Evergy’s operations.

Its predictable output and low fuel-price sensitivity act as a financial pillar, cutting earnings volatility; in 2024 Wolf Creek helped stabilize Evergy’s EBITDA by an estimated $150–200 million versus fossil-only scenarios.

Missouri Service Territory Operations

Evergy Metro and Evergy Missouri West serve ~1.6 million customers across Missouri, holding high regional market share and delivering stable regulated returns; their 2024 combined electric revenue was about $2.8 billion, underpinning predictable cash flow.

Operating under Missouri’s established rate-setting rules, these utilities generate strong free cash flow—Evergy reported $1.1 billion operating cash flow in 2024—that funds multi-year renewable investments such as the 2025-27 $2.5 billion clean-energy program.

Kansas Service Territory Operations

Kansas Service Territory Operations generate stable, high-margin cash flows for Evergy (EVRG; 2025 revenue estimate $4.6B), serving ~1.2M customers with steady residential and agricultural demand growing ~0.6% annually through 2024–25; mature grid means capital spending focuses on maintenance and smart-meter/AMI upgrades rather than expansion.

That stability lets Evergy harvest free cash flow (~$850M LTM free cash flow 2024) to pay down corporate debt (debt/EBITDA ~4.2x 2024) and sustain dividends for long-term shareholders.

- ~1.2M customers in Kansas

- Revenue contribution significant to $4.6B company total (2025 est)

- Customer growth ~0.6% annually (2024–25)

- LTM free cash flow ~ $850M (2024)

- Debt/EBITDA ~4.2x (2024)

Commercial and Industrial Base

Evergy serves a high share of large-scale industrial customers in the Midwest, supplying bulk power to manufacturers and data centers and capturing roughly 28% of regional industrial demand as of 2025.

This mature segment shows low volume growth but delivers substantial, stable revenue—industrial and commercial sales generated about $2.1 billion in 2024, or ~38% of total retail margins.

Long-term contracts and high consumption yield predictable cash flow and liquidity, funding Evergy’s grid upgrades and clean-energy pivots while keeping credit metrics strong (2024 FFO-to-debt ~12%).

- Large-scale customers ~28% of regional industrial demand (2025)

- Industrial/commercial sales ≈ $2.1B (2024)

- Represents ~38% of retail margins

- FFO-to-debt ≈ 12% (2024)

Evergy: Stable cash cows—Wolf Creek nuclear & regulated distribution drive strong FCF

Evergy’s regulated distribution and Wolf Creek nuclear are cash cows: stable revenues (~$4.6B regional revenue est. 2025), LTM free cash flow ~$850M (2024), operating cash flow $2.1B (2024), dividend $0.505 (2024), debt/EBITDA ~4.2x (2024), Wolf Creek ~1,200 MW (~45% generation mix 2025).

| Metric | Value |

|---|---|

| Free cash flow | $850M (2024) |

| Op CF | $2.1B (2024) |

| Dividend | $0.505 (2024) |

| Debt/EBITDA | 4.2x (2024) |

What You See Is What You Get

Evergy BCG Matrix

The file you're previewing on this page is the final Evergy BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report crafted for clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Evergy’s BCG Matrix preview highlights how its core segments—regulated utility operations, renewable investments, and emerging energy services—stack up by market share and growth potential, revealing likely Cash Cows and budding Question Marks. This snapshot suggests where Evergy can harvest stable cash flows versus where it should invest to capture future growth amid grid modernization and decarbonization trends. The full BCG Matrix delivers quadrant-by-quadrant placement, data-backed strategic moves, and actionable recommendations. Purchase the complete report for a ready-to-use Word and Excel package that guides capital allocation and competitive strategy.

Stars

Renewable Energy Portfolio Expansion

Evergy has shifted its generation mix to 42% renewables by 2024, mainly wind and solar, to meet Kansas/Missouri mandates and a 50% carbon reduction target by 2030.

These assets hold roughly 35% regional market share in intermittent renewables and sit in a high-growth segment as fossil generation falls ~18% 2020–2025.

Evergy spent $1.1 billion on renewables and grid upgrades in 2024 and plans ~ $3.2 billion capex through 2026 to keep leadership as the market matures.

Grid Modernization and Digitalization

Evergy is investing roughly $2.3 billion through 2027 in smart grid upgrades—sensors, two-way meters, and grid software—to boost reliability and enable distributed energy flows for renewables and EVs.

Demand for grid modernization is rising: regional outage minutes fell 18% where upgrades completed, while investments respond to increased extreme-weather losses (Midwest insured losses rose 35% 2015–2024) and growing cyber threats.

These heavy capital expenditures compress near-term free cash flow but position Evergy as a tech leader in utilities, supporting higher tariff petitions and potential grid-service revenue streams estimated at $40–60 million annually by 2030.

Electric Vehicle Infrastructure

Evergy, via its Clean Charge Network and public-private deals, leads the regional EV charging market; by 2025 U.S. EV registrations hit ~3.2M (IEA/EDTA data) boosting utility charging demand 40% YoY in many Midwestern corridors.

This high-growth Stars segment could contribute materially to future revenue—Evergy projects network EBITDA margins near 20% by 2026 if adoption keeps rising and utilization exceeds 30%.

Continued capex—estimated $50–75M through 2026—is needed to defend share versus third-party providers like ChargePoint and EVgo entering the region.

Utility-Scale Battery Storage

Utility-Scale Battery Storage: large-scale storage balances intermittent wind and solar and stabilizes the grid at peak demand; industry projections show US utility battery capacity grew 45% in 2024 to ~5.2 GW (SEIA/EIA data).

Evergy leads deployments in the Southwest Power Pool, operating multiple MW-scale projects and holding ~15% market share of announced SPP storage capacity as of Dec 2025; projects are capital intensive and currently cash-consuming.

This high-growth segment is investment-heavy now but is forecasted to deliver steady regulated returns and support decarbonization—storage LCOE fell ~30% since 2020, improving project IRRs and grid value.

- 2024 US utility battery capacity ~5.2 GW (+45% YoY)

- Evergy ~15% share of announced SPP storage (Dec 2025)

- Storage LCOE down ~30% since 2020

- Currently cash-consuming; long-term regulated returns expected

Regional Transmission Projects

Regional Transmission Projects: Expanding high-voltage lines moves wind from rural Kansas to cities; Evergy’s regulated transmission segment earned ~35% of 2024 capex (~$420M of $1.2B) and holds a leading regional share backed by state-approved ratebase recovery, matching rising interconnection requests (MISO filed ~50 GW active in 2024).

These projects are capital intensive but strategic—project IRRs often 6–9% after regulatory allowance, enabling Evergy to defend market dominance as Midwest renewables grow; expected transmission spend in 2025–2027 is $1.8B per regional plans.

- 35% of Evergy 2024 capex: ~$420M

- MISO 2024 interconnection backlog: ~50 GW

- Projected regional transmission spend 2025–2027: ~$1.8B

- Typical regulated IRR: 6–9%

Evergy’s Growth Play: 42% Renewables, Big Storage & $3.2B Capex Through 2026

Evergy’s Stars: renewables, storage, transmission—42% renewables (2024), ~35% regional renewables share, $1.1B renewables/grid spend 2024, $3.2B capex thru 2026; storage ~15% SPP announced share (Dec 2025), US utility battery 5.2 GW (2024); transmission $420M capex (2024), projected $1.8B 2025–27.

| Metric | Value |

|---|---|

| Renewables % (2024) | 42% |

| Regional share | ~35% |

| 2024 renew/grid spend | $1.1B |

| Capex thru 2026 | $3.2B |

| US battery (2024) | 5.2 GW |

| Evergy SPP storage share | ~15% |

| Transm. 2024 capex | $420M |

| Transm. 2025–27 proj | $1.8B |

What is included in the product

Comprehensive BCG Matrix of Evergy: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page BCG Matrix placing Evergy’s units into clear quadrants for fast strategic decisions.

Cash Cows

Regulated Electricity Distribution

Evergy’s regulated electricity distribution serves 1.6 million customers in Kansas and Missouri, generating steady cash flow—Evergy reported $2.1 billion operating cash flow in 2024, largely from core distribution services.

Markets are mature with low volume growth; Evergy holds de facto monopoly shares in many service territories, enabling regulated returns and predictable margins (2024 ROR ~8.5%).

These stable revenues fund a $0.505 annual dividend in 2024 and bankroll renewable investments—Evergy committed $1.2 billion to clean energy projects through 2025.

Wolf Creek Nuclear Station

Wolf Creek Nuclear Station supplies about 1,200 MW of carbon-free baseload power, representing roughly 40–50% of Evergy’s regional generation mix in 2025 and giving the company a dominant market share in steady output.

As a mature plant online since 1985, Wolf Creek needs relatively low growth capex—estimated routine maintenance of ~$40–60 million annually—while generating high daily cash flow that supports Evergy’s operations.

Its predictable output and low fuel-price sensitivity act as a financial pillar, cutting earnings volatility; in 2024 Wolf Creek helped stabilize Evergy’s EBITDA by an estimated $150–200 million versus fossil-only scenarios.

Missouri Service Territory Operations

Evergy Metro and Evergy Missouri West serve ~1.6 million customers across Missouri, holding high regional market share and delivering stable regulated returns; their 2024 combined electric revenue was about $2.8 billion, underpinning predictable cash flow.

Operating under Missouri’s established rate-setting rules, these utilities generate strong free cash flow—Evergy reported $1.1 billion operating cash flow in 2024—that funds multi-year renewable investments such as the 2025-27 $2.5 billion clean-energy program.

Kansas Service Territory Operations

Kansas Service Territory Operations generate stable, high-margin cash flows for Evergy (EVRG; 2025 revenue estimate $4.6B), serving ~1.2M customers with steady residential and agricultural demand growing ~0.6% annually through 2024–25; mature grid means capital spending focuses on maintenance and smart-meter/AMI upgrades rather than expansion.

That stability lets Evergy harvest free cash flow (~$850M LTM free cash flow 2024) to pay down corporate debt (debt/EBITDA ~4.2x 2024) and sustain dividends for long-term shareholders.

- ~1.2M customers in Kansas

- Revenue contribution significant to $4.6B company total (2025 est)

- Customer growth ~0.6% annually (2024–25)

- LTM free cash flow ~ $850M (2024)

- Debt/EBITDA ~4.2x (2024)

Commercial and Industrial Base

Evergy serves a high share of large-scale industrial customers in the Midwest, supplying bulk power to manufacturers and data centers and capturing roughly 28% of regional industrial demand as of 2025.

This mature segment shows low volume growth but delivers substantial, stable revenue—industrial and commercial sales generated about $2.1 billion in 2024, or ~38% of total retail margins.

Long-term contracts and high consumption yield predictable cash flow and liquidity, funding Evergy’s grid upgrades and clean-energy pivots while keeping credit metrics strong (2024 FFO-to-debt ~12%).

- Large-scale customers ~28% of regional industrial demand (2025)

- Industrial/commercial sales ≈ $2.1B (2024)

- Represents ~38% of retail margins

- FFO-to-debt ≈ 12% (2024)

Evergy: Stable cash cows—Wolf Creek nuclear & regulated distribution drive strong FCF

Evergy’s regulated distribution and Wolf Creek nuclear are cash cows: stable revenues (~$4.6B regional revenue est. 2025), LTM free cash flow ~$850M (2024), operating cash flow $2.1B (2024), dividend $0.505 (2024), debt/EBITDA ~4.2x (2024), Wolf Creek ~1,200 MW (~45% generation mix 2025).

| Metric | Value |

|---|---|

| Free cash flow | $850M (2024) |

| Op CF | $2.1B (2024) |

| Dividend | $0.505 (2024) |

| Debt/EBITDA | 4.2x (2024) |

What You See Is What You Get

Evergy BCG Matrix

The file you're previewing on this page is the final Evergy BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report crafted for clarity and professional presentation.