Evergy Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Evergy faces moderate supplier power, regulated pricing constraints, and rising competitive pressure from renewables and distributed generation—while customer bargaining remains muted due to utility monopolies; this snapshot highlights key tensions shaping margins and growth prospects. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Evergy for smarter investment and strategy decisions.

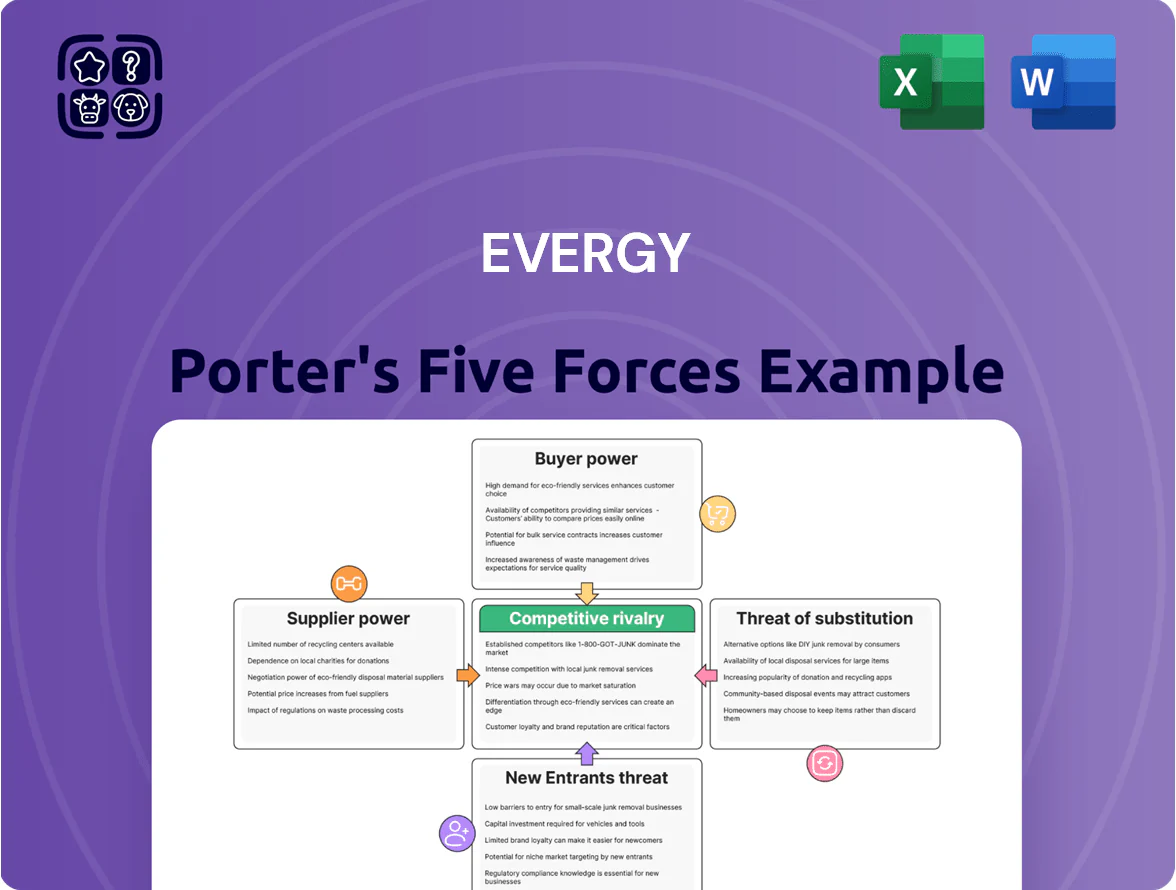

Suppliers Bargaining Power

Concentration of Fuel and Energy Raw Materials

Evergy depends on a small set of suppliers for coal, natural gas, and uranium; in 2024 roughly 60% of its thermal fuel spend tied to three major vendors, giving suppliers moderate pricing leverage.

Supply shocks—2022–23 gas price spikes raised fuel costs by ~18% for US utilities—and geopolitical shifts can push Evergy to seek cost recovery via Kansas and Missouri regulatory rate cases.

Renewable Energy Infrastructure Providers

As Evergy expands wind and solar, it now sources turbines, PV panels, and batteries from a handful of global makers, raising supplier bargaining power; top turbine makers control ~60% of global capacity and top PV producers >50% as of 2025.

High demand and limited suppliers for high-efficiency components pushed lead times to 9–15 months in 2025, risking higher capex for Evergy if bottlenecks persist.

Specialized Technical Labor and Union Influence

Evergy relies on specialized, often unionized crews for grid upkeep, nuclear safety, and renewables—roles that raised labor costs industry-wide: US utility average annual wage for electrical engineers was $108,000 in 2024 (BLS).

Unions negotiate wages/benefits that flow into Evergy’s O&M; Evergy reported 2024 labor and benefits expense rising 6% year-over-year, pressuring margins.

Midwest shortages of skilled technicians (vacancy rates ~4–6% in 2024) boost supplier leverage and recruitment costs.

Capital Market and Financing Dependency

Evergy needs large capital for grid upgrades and clean-energy projects; at year-end 2024 its long-term debt was about $14.2 billion and 2024 capex guidance was $1.3–1.6 billion, so lenders’ terms matter materially.

Debt markets and big banks set pricing based on Fed-driven rates and Evergy’s BBB-/stable S&P rating (Dec 2024); a 100 bp rise in borrowing costs raises annual interest expense by roughly $142 million on current debt.

- 2024 long-term debt ~$14.2B

- 2024 capex guidance $1.3–1.6B

- S&P rating BBB-/stable (Dec 2024)

- +100 bp ≈ $142M annual interest

Technological and Software Service Providers

The shift to a smart grid forces Evergy to integrate closely with software providers for grid management, cybersecurity, and billing, with utilities spending an estimated 5–8% of capex on IT and OT modernization in 2024.

Many vendors supply proprietary platforms, raising switching costs and lock-in risks that can exceed $50m for grid-scale replacements.

As digital transformation drives operations, these suppliers gain outsized influence on Evergy’s long-term strategy and vendor roadmap decisions.

- 5–8% of capex on IT/OT (2024)

- $50m+ potential switching cost

- Proprietary platforms = high lock-in

Supplier Concentration Raises Costs & Lead-Time Risks Amid High Debt and Rising Wages

Suppliers exert moderate-to-high power: 2024 fuel spend concentrated (~60%) with three vendors; top turbine/PV makers control ~60%/>50% global share (2025); lead times 9–15 months (2025); 2024 labor costs up 6% with US EE avg wage $108k; long-term debt ~$14.2B, capex $1.3–1.6B, S&P BBB-/stable (Dec 2024).

| Metric | Value |

|---|---|

| Fuel concentration | ~60% |

| Turbine/PV share | ~60% / >50% |

| Lead times (2025) | 9–15 mo |

| Long-term debt (2024) | $14.2B |

What is included in the product

Tailored exclusively for Evergy, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic defenses.

Clear, one-sheet Porter's Five Forces for Evergy—rapidly assess competitive pressures, regulatory impact, and supplier/customer bargaining to inform strategic and investment decisions.

Customers Bargaining Power

Regulatory Oversight as a Buyer Proxy

Individual residential customers have negligible direct bargaining power, so the Kansas Corporation Commission and Missouri Public Service Commission act as buyer proxies; they set and approve rates, limiting Evergy’s allowed return on equity (ROE)—recent orders set ROE bands around 9.5–10.5% in 2024—thereby capping profit margins and requiring detailed cost justification for any rate increase; regulatory scrutiny reduces revenue volatility and enforces consumer protections.

Industrial and Large Commercial Customer Leverage

Large industrial and commercial customers represent about 40% of Evergy’s retail load in 2024 and wield outsized bargaining power, often securing bespoke rate structures tied to demand profiles.

These firms can threaten relocation—Midwest manufacturing shifts cut costs by up to 15%—pressuring Evergy to match lower tariffs or offer economic development credits.

Some clients pursue self-generation or PPAs; Evergy reported competitive rate concessions averaging 6% in 2023 to retain large accounts.

Adoption of Distributed Energy Resources

Rooftop solar costs fell about 47% per kW from 2015–2024 and US residential battery deployments grew ~35% YoY in 2023, letting Kansas–Missouri customers cut grid use and raising Evergy’s customer bargaining power.

These distributed energy resources (DERs) offer a credible alternative to Evergy’s service, pressuring rates and contract terms.

Evergy must bundle DER integration, virtual net metering, and storage services; otherwise utility revenue and load forecasts—already down ~2–3% in some US territories—face further erosion.

Energy Efficiency and Demand Response Programs

Customers' uptake of energy efficiency and demand response cuts Evergy's load: US household electricity use per customer fell ~1.1% annually 2019–2023, and utility peak demand programs reduced system peaks by ~2–4% in 2023, lowering kWh sales and revenue growth pressure.

Smart thermostats and efficient appliances shift consumption; Evergy faces margin squeeze as customers use less and control costs, forcing new rate designs and non‑commodity services to recoup fixed costs.

- Customer efficiency trimmed sales growth ~1–2% in 2023

- Peak reductions 2–4% via demand response (2023)

- Smart device penetration rising ~15–20% YoY

Public Sentiment and Political Pressure

As an essential-service provider, Evergy is vulnerable to public opinion on rates and emissions; Missouri and Kansas regulatory cases in 2024 saw consumer rate disputes affecting a combined $200m+ in proposed revenue adjustments.

Organized advocacy—e.g., Sierra Club campaigns and local ratepayer coalitions—pushed legislative measures in 2023–2025 that influenced renewable procurement timelines and net-metering credits.

This social and political pressure functions as indirect bargaining power, steering Evergy’s capital allocation toward affordability and its 2030 emissions targets.

- Public disputes tied to $200m+ revenue impacts (2024)

- Advocacy altered renewable procurement/net-metering rules (2023–2025)

- Pressure shifts capital spending toward affordability and 2030 emissions goals

Regulated ROE capped ~10% as large customers and DERs squeeze margins

Regulated retail customers have low direct bargaining power; Kansas and Missouri commissions capped ROE ~9.5–10.5% (2024), limiting margins. Large industrials (~40% load in 2024) secure bespoke rates/credits and can threaten relocation; Evergy gave ~6% concessions in 2023. DERs and efficiency cut load (~1–3% sales impact), pressuring rate design and noncommodity services.

| Metric | Value |

|---|---|

| Large-customer load | ~40% (2024) |

| ROE band | 9.5–10.5% (2024) |

| Concessions | ~6% (2023) |

| Sales impact | ~1–3% |

What You See Is What You Get

Evergy Porter's Five Forces Analysis

This preview shows the exact Evergy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready for use.

The document displayed here is the same professionally written file available for instant download once you complete your payment, containing the complete analysis and actionable insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Evergy faces moderate supplier power, regulated pricing constraints, and rising competitive pressure from renewables and distributed generation—while customer bargaining remains muted due to utility monopolies; this snapshot highlights key tensions shaping margins and growth prospects. This preview is just the beginning. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Evergy for smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentration of Fuel and Energy Raw Materials

Evergy depends on a small set of suppliers for coal, natural gas, and uranium; in 2024 roughly 60% of its thermal fuel spend tied to three major vendors, giving suppliers moderate pricing leverage.

Supply shocks—2022–23 gas price spikes raised fuel costs by ~18% for US utilities—and geopolitical shifts can push Evergy to seek cost recovery via Kansas and Missouri regulatory rate cases.

Renewable Energy Infrastructure Providers

As Evergy expands wind and solar, it now sources turbines, PV panels, and batteries from a handful of global makers, raising supplier bargaining power; top turbine makers control ~60% of global capacity and top PV producers >50% as of 2025.

High demand and limited suppliers for high-efficiency components pushed lead times to 9–15 months in 2025, risking higher capex for Evergy if bottlenecks persist.

Specialized Technical Labor and Union Influence

Evergy relies on specialized, often unionized crews for grid upkeep, nuclear safety, and renewables—roles that raised labor costs industry-wide: US utility average annual wage for electrical engineers was $108,000 in 2024 (BLS).

Unions negotiate wages/benefits that flow into Evergy’s O&M; Evergy reported 2024 labor and benefits expense rising 6% year-over-year, pressuring margins.

Midwest shortages of skilled technicians (vacancy rates ~4–6% in 2024) boost supplier leverage and recruitment costs.

Capital Market and Financing Dependency

Evergy needs large capital for grid upgrades and clean-energy projects; at year-end 2024 its long-term debt was about $14.2 billion and 2024 capex guidance was $1.3–1.6 billion, so lenders’ terms matter materially.

Debt markets and big banks set pricing based on Fed-driven rates and Evergy’s BBB-/stable S&P rating (Dec 2024); a 100 bp rise in borrowing costs raises annual interest expense by roughly $142 million on current debt.

- 2024 long-term debt ~$14.2B

- 2024 capex guidance $1.3–1.6B

- S&P rating BBB-/stable (Dec 2024)

- +100 bp ≈ $142M annual interest

Technological and Software Service Providers

The shift to a smart grid forces Evergy to integrate closely with software providers for grid management, cybersecurity, and billing, with utilities spending an estimated 5–8% of capex on IT and OT modernization in 2024.

Many vendors supply proprietary platforms, raising switching costs and lock-in risks that can exceed $50m for grid-scale replacements.

As digital transformation drives operations, these suppliers gain outsized influence on Evergy’s long-term strategy and vendor roadmap decisions.

- 5–8% of capex on IT/OT (2024)

- $50m+ potential switching cost

- Proprietary platforms = high lock-in

Supplier Concentration Raises Costs & Lead-Time Risks Amid High Debt and Rising Wages

Suppliers exert moderate-to-high power: 2024 fuel spend concentrated (~60%) with three vendors; top turbine/PV makers control ~60%/>50% global share (2025); lead times 9–15 months (2025); 2024 labor costs up 6% with US EE avg wage $108k; long-term debt ~$14.2B, capex $1.3–1.6B, S&P BBB-/stable (Dec 2024).

| Metric | Value |

|---|---|

| Fuel concentration | ~60% |

| Turbine/PV share | ~60% / >50% |

| Lead times (2025) | 9–15 mo |

| Long-term debt (2024) | $14.2B |

What is included in the product

Tailored exclusively for Evergy, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic defenses.

Clear, one-sheet Porter's Five Forces for Evergy—rapidly assess competitive pressures, regulatory impact, and supplier/customer bargaining to inform strategic and investment decisions.

Customers Bargaining Power

Regulatory Oversight as a Buyer Proxy

Individual residential customers have negligible direct bargaining power, so the Kansas Corporation Commission and Missouri Public Service Commission act as buyer proxies; they set and approve rates, limiting Evergy’s allowed return on equity (ROE)—recent orders set ROE bands around 9.5–10.5% in 2024—thereby capping profit margins and requiring detailed cost justification for any rate increase; regulatory scrutiny reduces revenue volatility and enforces consumer protections.

Industrial and Large Commercial Customer Leverage

Large industrial and commercial customers represent about 40% of Evergy’s retail load in 2024 and wield outsized bargaining power, often securing bespoke rate structures tied to demand profiles.

These firms can threaten relocation—Midwest manufacturing shifts cut costs by up to 15%—pressuring Evergy to match lower tariffs or offer economic development credits.

Some clients pursue self-generation or PPAs; Evergy reported competitive rate concessions averaging 6% in 2023 to retain large accounts.

Adoption of Distributed Energy Resources

Rooftop solar costs fell about 47% per kW from 2015–2024 and US residential battery deployments grew ~35% YoY in 2023, letting Kansas–Missouri customers cut grid use and raising Evergy’s customer bargaining power.

These distributed energy resources (DERs) offer a credible alternative to Evergy’s service, pressuring rates and contract terms.

Evergy must bundle DER integration, virtual net metering, and storage services; otherwise utility revenue and load forecasts—already down ~2–3% in some US territories—face further erosion.

Energy Efficiency and Demand Response Programs

Customers' uptake of energy efficiency and demand response cuts Evergy's load: US household electricity use per customer fell ~1.1% annually 2019–2023, and utility peak demand programs reduced system peaks by ~2–4% in 2023, lowering kWh sales and revenue growth pressure.

Smart thermostats and efficient appliances shift consumption; Evergy faces margin squeeze as customers use less and control costs, forcing new rate designs and non‑commodity services to recoup fixed costs.

- Customer efficiency trimmed sales growth ~1–2% in 2023

- Peak reductions 2–4% via demand response (2023)

- Smart device penetration rising ~15–20% YoY

Public Sentiment and Political Pressure

As an essential-service provider, Evergy is vulnerable to public opinion on rates and emissions; Missouri and Kansas regulatory cases in 2024 saw consumer rate disputes affecting a combined $200m+ in proposed revenue adjustments.

Organized advocacy—e.g., Sierra Club campaigns and local ratepayer coalitions—pushed legislative measures in 2023–2025 that influenced renewable procurement timelines and net-metering credits.

This social and political pressure functions as indirect bargaining power, steering Evergy’s capital allocation toward affordability and its 2030 emissions targets.

- Public disputes tied to $200m+ revenue impacts (2024)

- Advocacy altered renewable procurement/net-metering rules (2023–2025)

- Pressure shifts capital spending toward affordability and 2030 emissions goals

Regulated ROE capped ~10% as large customers and DERs squeeze margins

Regulated retail customers have low direct bargaining power; Kansas and Missouri commissions capped ROE ~9.5–10.5% (2024), limiting margins. Large industrials (~40% load in 2024) secure bespoke rates/credits and can threaten relocation; Evergy gave ~6% concessions in 2023. DERs and efficiency cut load (~1–3% sales impact), pressuring rate design and noncommodity services.

| Metric | Value |

|---|---|

| Large-customer load | ~40% (2024) |

| ROE band | 9.5–10.5% (2024) |

| Concessions | ~6% (2023) |

| Sales impact | ~1–3% |

What You See Is What You Get

Evergy Porter's Five Forces Analysis

This preview shows the exact Evergy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready for use.

The document displayed here is the same professionally written file available for instant download once you complete your payment, containing the complete analysis and actionable insights.