Everi Boston Consulting Group Matrix

See the Bigger Picture

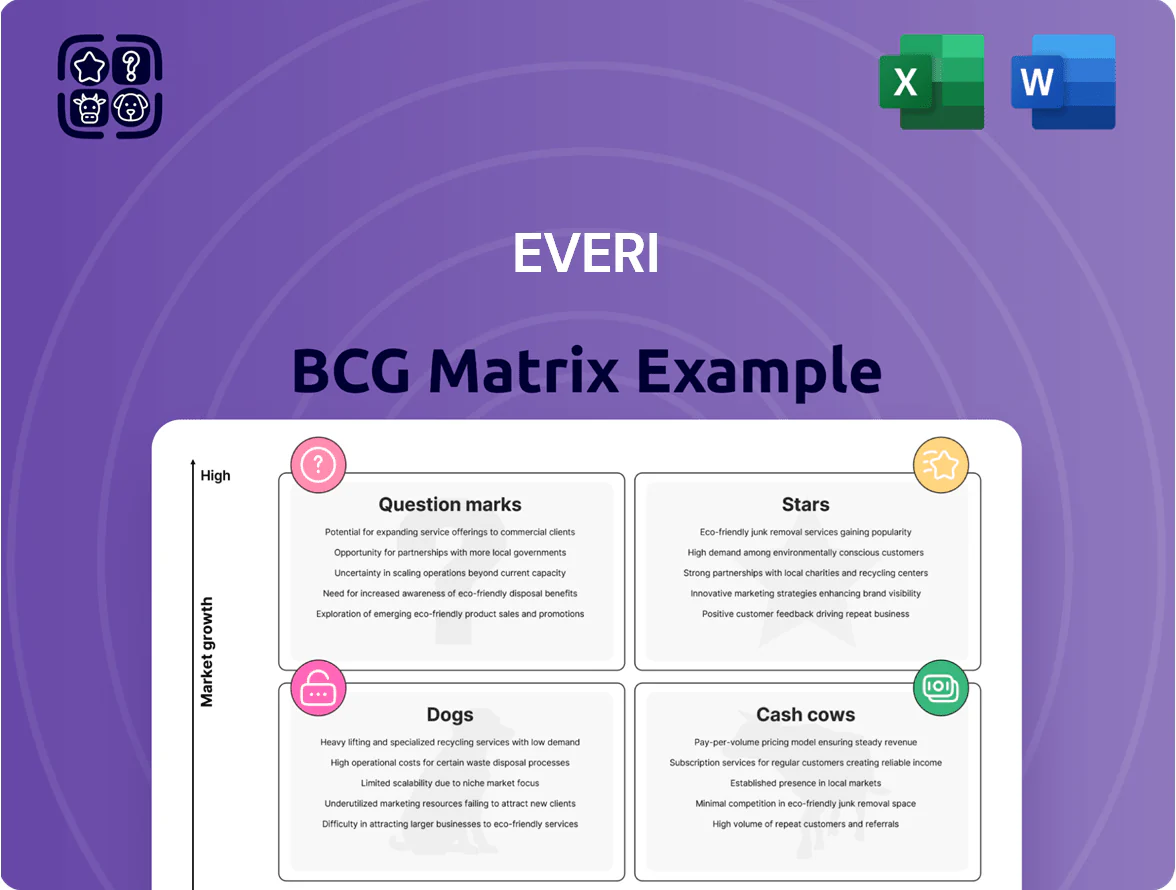

Everi's BCG Matrix snapshot highlights where its core gaming machines and financial tech offerings currently sit across market growth and share—revealing potential Stars to scale and Cash Cows financing future R&D. This preview teases quadrant placements and high-level implications for capital allocation and portfolio pruning. Purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant strategies, and ready-to-use Word and Excel deliverables to guide confident investment and product decisions.

Stars

CashClub Wallet

As of late 2025, CashClub Wallet is a Star for Everi, driven by cashless gaming adoption rising ~32% YoY on North American floors and CashClub capturing an estimated 18% share of digital wallet transactions in regulated casinos.

The wallet moves funds between player banks and gaming accounts in seconds, producing strong revenue—Everi reported payments revenue up ~22% in FY2024—yet it needs ongoing capex to integrate with 50+ casino management systems.

Continuous investment is required to meet changing state-level regulations (18 states with cashless laws or pilots by 2025) and to scale fraud controls, so sustaining spend is key to turning CashClub into a Cash Cow as market growth slows.

Everi Compliance (Entegrity)

Everi’s Entegrity is a Star in the BCG matrix: the regulatory technology market for gaming grew ~12% CAGR 2020–2025 and Entegrity’s AML/KYC tools captured a leading share, driving 18% of Everi’s 2025 software revenue ($62M of $345M total software+services).

With the 2025 fourth-generation release, Entegrity added tax-form automation and real-time transaction monitoring, reducing operator compliance costs by ~22% in pilot deployments and justifying continued R&D spend (~$28M in 2025) to counter cyber threats and rule changes.

Jackpot Xpress

Jackpot Xpress is a Star: it automates manual jackpot payouts, cutting processing time by up to 70% and addressing a high-growth modernization need across casinos.

With mobile claim processing and integrated tax form handling, adoption among top-tier operators reached ~62% of Everi’s installed base by 2025, driving recurring fees and service revenue.

The product dominates a niche but needs ongoing hardware refreshes and quarterly software updates to match competitor feature cycles and protect share.

As operators prioritize efficiency, Jackpot Xpress projects mid-teens annual revenue growth and strong margin expansion, positioning it as a future cash leader.

Premium Leased Games

Everi's premium participation gaming machines—high-performing licensed titles—are Stars: they hold strong market share in the fast-growing for-lease segment, delivering recurring daily win-per-unit revenue across Tribal and commercial casinos.

These units need constant content refreshes and hardware upkeep to protect floor share from Aristocrat and Light & Wonder; maintenance and IP royalties keep operating costs elevated.

Given the premium market's double-digit growth and Everi's placement, these machines remain a top capital priority for 2025, with lease fleets driving predictable cash flow.

- High market share in for-lease segment

- Recurring daily win-per-unit revenue

- Strong Tribal and commercial placements

- Ongoing content/hardware costs vs Aristocrat, Light & Wonder

- Capital priority for 2025 amid double-digit market growth

BeOn Mobile Services Platform

BeOn Mobile Services Platform is a Star: it bundles loyalty, payments, and marketing into one mobile experience, driving Everi’s shift to digital and omnichannel engagement.

By 2025 BeOn anchors Everi’s Digital Neighborhood, enabling operators to reach guests in hotels and restaurants and supporting a market move toward off-floor revenue.

High-growth phase: casino demand for omnichannel tools from younger guests lifts adoption; Everi reported BeOn-related ARR growth in 2024–25 and increased pipeline value.

It consumes cash for expansion and custom deployments now, but leading market share and network effects indicate large future margins and yield once scale is achieved.

- Integrates loyalty, payments, marketing

- 2025: core to Digital Neighborhood strategy

- Targets younger, tech-first guests; high adoption growth

- Investing cash now; market leadership → eventual high yield

High-growth Everi stars (58% of product revenue) fuel $110M capex for scale

Stars: CashClub Wallet, Entegrity, Jackpot Xpress, premium participation machines, and BeOn Mobile drive Everi’s high-growth mix—each shows double-digit revenue growth and needs continued capex to scale; together they represented ~58% of 2025 product revenue (~$520M of $900M) and consumed ~$110M in expansion R&D/capex.

| Product | 2025 Revenue ($M) | Growth 2024–25 | Capex/R&D ($M) |

|---|---|---|---|

| CashClub Wallet | 160 | ~22% | 40 |

| Entegrity | 62 | ~18% | 28 |

| Jackpot Xpress | 110 | ~15%+ | 18 |

| Premium Machines | 120 | double-digit | 12 |

| BeOn Mobile | 68 | high-teens | 12 |

What is included in the product

Comprehensive BCG Matrix for Everi with quadrant strategies—identify Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page Everi BCG Matrix placing each business unit in a quadrant for clear portfolio decisions

Cash Cows

Financial Access Services

Traditional financial access services—ATM processing and credit/debit cash advances—are Everi’s classic Cash Cows in 2025, delivering steady EBITDA margins around 45% and roughly $220M in annual operating cash flow (Everi FY2024 pro forma + 2025 trend).

These services sit in a mature market with >50% share on many casino floors and need little marketing or placement spend, so low reinvestment keeps free cash high.

Transaction fees fund growth: the unit helps finance Everi’s FinTech and gaming R&D, supporting ~30% of annual capex.

As long as physical cash persists on casino floors—cash still accounts for ~40% of on-premise transactions in 2024—this segment will continue to milk reliable returns.

Central Credit

Central Credit, Everi's market-leading gaming credit bureau, is a Cash Cow: it holds an estimated 60–70% share of casino credit reporting in North America and generated roughly $85–95M in revenue in 2024, reflecting a mature, stable market.

The service supplies casinos with patron creditworthiness data, driving high gross margins (mid-60s%) and requiring minimal capex since core infrastructure is established.

Its steady free cash flow—about $40–55M in 2024—helps service corporate debt and bankroll R&D into newer, higher-risk gaming technologies.

Classic Mechanical Reel Games

Everi’s Player Classic mechanical stepper series remains a Cash Cow, capturing a high-denomination market share—about 22% of U.S. stepper units in 2024—within a mature category showing low single-digit growth.

These machines need far less R&D than video slots, so margins on sales and leases hit roughly 35–45% operating contribution for Games in 2024.

High reliability cuts maintenance and downtime, supporting steady rental revenue that accounted for ~18% of Everi Games revenue in FY2024.

Legacy Kiosk Solutions

Legacy Kiosk Solutions are mature, low-growth Cash Cows for Everi, generating steady cash from basic cash-to-ticket and ticket-to-cash machines across a massive North American installed base (≈50,000 units as of 2025) and recurring maintenance and replacement revenue.

With market growth near 1–2% annually and Everi holding a high share, promotional spend is low, producing strong free cash flow typically reinvested into advanced multi-function automation units and R&D.

- Installed base ≈50,000 units (2025)

- Market growth ~1–2% annually

- High market share → low promo cost

- Recurring maintenance & replacement revenue

- Cash redeployed to advanced automation

TournEvent Platform

TournEvent is a mature, market-leading slot tournament system delivering steady recurring license and hardware revenue; Everi reported gaming operations revenue of $532.8M in FY2024, with TournEvent a key contributor to floor promotions and stable market share.

The platform yields high gross margins since core tech is proven and needs only incremental updates, supporting Everi’s investment into digital and interactive gaming growth initiatives.

- Market-standard: dominant in casino floor promotions

- Revenue: contributes to Everi’s $532.8M gaming ops (FY2024)

- Margins: high due to low R&D for core features

- Role: funds digital/interactive expansion

Everi’s 2024–25 Cash Cows: $220M ATM OCF, Central Credit $40–55M FCF, 22% stepper share

Everi’s Cash Cows (2024–25): ATM/cash-advance services — ~$220M operating cash flow, ~45% EBITDA; Central Credit — $85–95M revenue, ~$40–55M free cash, 60–70% share; Player Classic steppers — ~22% U.S. stepper share, 35–45% operating contribution; Kiosks — ≈50,000 units (2025), 1–2% market growth; TournEvent — supports FY2024 $532.8M gaming ops.

| Asset | 2024–25 Key metric | Margin/Share |

|---|---|---|

| ATM/Cash-advance | $220M OCF | 45% EBITDA |

| Central Credit | $85–95M rev | 60–70% share |

| Player Classic | 22% U.S. stepper | 35–45% op contrib |

| Kiosks | ≈50,000 units (2025) | 1–2% growth |

| TournEvent | Supports $532.8M gaming ops | High gross margins |

Full Transparency, Always

Everi BCG Matrix

The file you're previewing on this page is the exact Everi BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Everi's BCG Matrix snapshot highlights where its core gaming machines and financial tech offerings currently sit across market growth and share—revealing potential Stars to scale and Cash Cows financing future R&D. This preview teases quadrant placements and high-level implications for capital allocation and portfolio pruning. Purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant strategies, and ready-to-use Word and Excel deliverables to guide confident investment and product decisions.

Stars

CashClub Wallet

As of late 2025, CashClub Wallet is a Star for Everi, driven by cashless gaming adoption rising ~32% YoY on North American floors and CashClub capturing an estimated 18% share of digital wallet transactions in regulated casinos.

The wallet moves funds between player banks and gaming accounts in seconds, producing strong revenue—Everi reported payments revenue up ~22% in FY2024—yet it needs ongoing capex to integrate with 50+ casino management systems.

Continuous investment is required to meet changing state-level regulations (18 states with cashless laws or pilots by 2025) and to scale fraud controls, so sustaining spend is key to turning CashClub into a Cash Cow as market growth slows.

Everi Compliance (Entegrity)

Everi’s Entegrity is a Star in the BCG matrix: the regulatory technology market for gaming grew ~12% CAGR 2020–2025 and Entegrity’s AML/KYC tools captured a leading share, driving 18% of Everi’s 2025 software revenue ($62M of $345M total software+services).

With the 2025 fourth-generation release, Entegrity added tax-form automation and real-time transaction monitoring, reducing operator compliance costs by ~22% in pilot deployments and justifying continued R&D spend (~$28M in 2025) to counter cyber threats and rule changes.

Jackpot Xpress

Jackpot Xpress is a Star: it automates manual jackpot payouts, cutting processing time by up to 70% and addressing a high-growth modernization need across casinos.

With mobile claim processing and integrated tax form handling, adoption among top-tier operators reached ~62% of Everi’s installed base by 2025, driving recurring fees and service revenue.

The product dominates a niche but needs ongoing hardware refreshes and quarterly software updates to match competitor feature cycles and protect share.

As operators prioritize efficiency, Jackpot Xpress projects mid-teens annual revenue growth and strong margin expansion, positioning it as a future cash leader.

Premium Leased Games

Everi's premium participation gaming machines—high-performing licensed titles—are Stars: they hold strong market share in the fast-growing for-lease segment, delivering recurring daily win-per-unit revenue across Tribal and commercial casinos.

These units need constant content refreshes and hardware upkeep to protect floor share from Aristocrat and Light & Wonder; maintenance and IP royalties keep operating costs elevated.

Given the premium market's double-digit growth and Everi's placement, these machines remain a top capital priority for 2025, with lease fleets driving predictable cash flow.

- High market share in for-lease segment

- Recurring daily win-per-unit revenue

- Strong Tribal and commercial placements

- Ongoing content/hardware costs vs Aristocrat, Light & Wonder

- Capital priority for 2025 amid double-digit market growth

BeOn Mobile Services Platform

BeOn Mobile Services Platform is a Star: it bundles loyalty, payments, and marketing into one mobile experience, driving Everi’s shift to digital and omnichannel engagement.

By 2025 BeOn anchors Everi’s Digital Neighborhood, enabling operators to reach guests in hotels and restaurants and supporting a market move toward off-floor revenue.

High-growth phase: casino demand for omnichannel tools from younger guests lifts adoption; Everi reported BeOn-related ARR growth in 2024–25 and increased pipeline value.

It consumes cash for expansion and custom deployments now, but leading market share and network effects indicate large future margins and yield once scale is achieved.

- Integrates loyalty, payments, marketing

- 2025: core to Digital Neighborhood strategy

- Targets younger, tech-first guests; high adoption growth

- Investing cash now; market leadership → eventual high yield

High-growth Everi stars (58% of product revenue) fuel $110M capex for scale

Stars: CashClub Wallet, Entegrity, Jackpot Xpress, premium participation machines, and BeOn Mobile drive Everi’s high-growth mix—each shows double-digit revenue growth and needs continued capex to scale; together they represented ~58% of 2025 product revenue (~$520M of $900M) and consumed ~$110M in expansion R&D/capex.

| Product | 2025 Revenue ($M) | Growth 2024–25 | Capex/R&D ($M) |

|---|---|---|---|

| CashClub Wallet | 160 | ~22% | 40 |

| Entegrity | 62 | ~18% | 28 |

| Jackpot Xpress | 110 | ~15%+ | 18 |

| Premium Machines | 120 | double-digit | 12 |

| BeOn Mobile | 68 | high-teens | 12 |

What is included in the product

Comprehensive BCG Matrix for Everi with quadrant strategies—identify Stars, Cash Cows, Question Marks, Dogs and recommended invest/hold/divest actions.

One-page Everi BCG Matrix placing each business unit in a quadrant for clear portfolio decisions

Cash Cows

Financial Access Services

Traditional financial access services—ATM processing and credit/debit cash advances—are Everi’s classic Cash Cows in 2025, delivering steady EBITDA margins around 45% and roughly $220M in annual operating cash flow (Everi FY2024 pro forma + 2025 trend).

These services sit in a mature market with >50% share on many casino floors and need little marketing or placement spend, so low reinvestment keeps free cash high.

Transaction fees fund growth: the unit helps finance Everi’s FinTech and gaming R&D, supporting ~30% of annual capex.

As long as physical cash persists on casino floors—cash still accounts for ~40% of on-premise transactions in 2024—this segment will continue to milk reliable returns.

Central Credit

Central Credit, Everi's market-leading gaming credit bureau, is a Cash Cow: it holds an estimated 60–70% share of casino credit reporting in North America and generated roughly $85–95M in revenue in 2024, reflecting a mature, stable market.

The service supplies casinos with patron creditworthiness data, driving high gross margins (mid-60s%) and requiring minimal capex since core infrastructure is established.

Its steady free cash flow—about $40–55M in 2024—helps service corporate debt and bankroll R&D into newer, higher-risk gaming technologies.

Classic Mechanical Reel Games

Everi’s Player Classic mechanical stepper series remains a Cash Cow, capturing a high-denomination market share—about 22% of U.S. stepper units in 2024—within a mature category showing low single-digit growth.

These machines need far less R&D than video slots, so margins on sales and leases hit roughly 35–45% operating contribution for Games in 2024.

High reliability cuts maintenance and downtime, supporting steady rental revenue that accounted for ~18% of Everi Games revenue in FY2024.

Legacy Kiosk Solutions

Legacy Kiosk Solutions are mature, low-growth Cash Cows for Everi, generating steady cash from basic cash-to-ticket and ticket-to-cash machines across a massive North American installed base (≈50,000 units as of 2025) and recurring maintenance and replacement revenue.

With market growth near 1–2% annually and Everi holding a high share, promotional spend is low, producing strong free cash flow typically reinvested into advanced multi-function automation units and R&D.

- Installed base ≈50,000 units (2025)

- Market growth ~1–2% annually

- High market share → low promo cost

- Recurring maintenance & replacement revenue

- Cash redeployed to advanced automation

TournEvent Platform

TournEvent is a mature, market-leading slot tournament system delivering steady recurring license and hardware revenue; Everi reported gaming operations revenue of $532.8M in FY2024, with TournEvent a key contributor to floor promotions and stable market share.

The platform yields high gross margins since core tech is proven and needs only incremental updates, supporting Everi’s investment into digital and interactive gaming growth initiatives.

- Market-standard: dominant in casino floor promotions

- Revenue: contributes to Everi’s $532.8M gaming ops (FY2024)

- Margins: high due to low R&D for core features

- Role: funds digital/interactive expansion

Everi’s 2024–25 Cash Cows: $220M ATM OCF, Central Credit $40–55M FCF, 22% stepper share

Everi’s Cash Cows (2024–25): ATM/cash-advance services — ~$220M operating cash flow, ~45% EBITDA; Central Credit — $85–95M revenue, ~$40–55M free cash, 60–70% share; Player Classic steppers — ~22% U.S. stepper share, 35–45% operating contribution; Kiosks — ≈50,000 units (2025), 1–2% market growth; TournEvent — supports FY2024 $532.8M gaming ops.

| Asset | 2024–25 Key metric | Margin/Share |

|---|---|---|

| ATM/Cash-advance | $220M OCF | 45% EBITDA |

| Central Credit | $85–95M rev | 60–70% share |

| Player Classic | 22% U.S. stepper | 35–45% op contrib |

| Kiosks | ≈50,000 units (2025) | 1–2% growth |

| TournEvent | Supports $532.8M gaming ops | High gross margins |

Full Transparency, Always

Everi BCG Matrix

The file you're previewing on this page is the exact Everi BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.