Everi Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Everi operates in a competitive, regulated payments-and-gaming tech niche where buyer sophistication and regulatory pressure shape margins, while supplier leverage and substitute digital payment options pose clear threats.

This snapshot highlights key tensions—scale-driven advantages vs. nimble fintech entrants—and flags areas where strategic moves can alter industry dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of Everi’s market position, competitive intensity, and external threats—all in one powerful analysis.

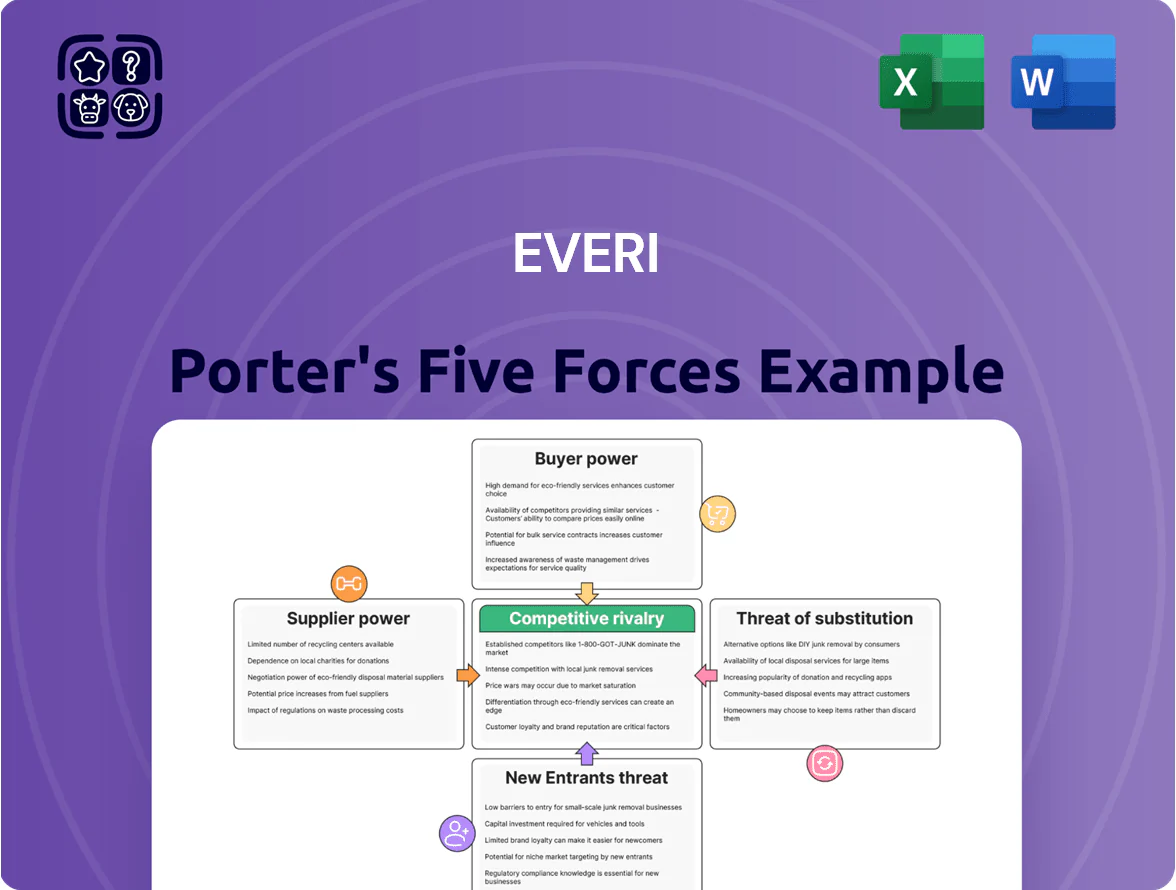

Suppliers Bargaining Power

Specialized Component Manufacturers

The production of Everi gaming cabinets relies on specialized electronic components and high-quality displays from a small set of global suppliers, giving suppliers moderate bargaining power.

Semiconductor shortages in 2021–22 raised component costs ~15–25% industrywide and occasional logistics delays; Everi reported hardware revenue 2024: $182.3M, so supply disruptions can notably hit order fulfillment.

Everi uses multiple sourcing and regional partners, but casino-grade specs limit substitute options, keeping supplier leverage moderate rather than low.

Financial Network Infrastructure

Everi’s FinTech segment depends on global networks like Visa and Mastercard, which set interchange and processing fees—Visa and Mastercard together processed $13.4 trillion in payments in 2024—forcing Everi to accept standardized pricing and rates. These networks also impose technical and security standards (EMV, PCI DSS) that raise compliance and integration costs for Everi. Given Visa/Mastercard scale and limited alternatives, Everi has minimal bargaining power, so supplier pressure is high.

Software Development Talent

The tight labor market for software engineers and game designers raises supplier power for Everi; US tech job openings were 9.1M in 2024 and average software engineer salary rose ~6% to $140K in 2024, forcing higher pay and benefits.

Regulatory Compliance Agencies

Regulatory compliance agencies act as gatekeepers to legal operating capacity, forcing Everi Holdings Inc to spend heavily on compliance and third-party audits across US and Canadian jurisdictions.

Everi reported compliance-related SG&A rising 6% in 2024, and licensing fee hikes or tightened standards can raise operating costs without adding product value; a single-state license renewal can cost $0.5–2.0M upfront.

What this hides: sudden regulatory changes can delay deployments and compress margins, increasing volatility in quarterly EBITDA.

- Regulatory bodies = supplier-like gatekeepers

- Everi compliance costs up 6% in 2024

- Single-state license: $0.5–2.0M

- Policy shifts can delay revenue, compress EBITDA

Third-Party Content Creators

Everi partners with external studios and IP holders to build branded slots and games that attract fans of franchises; these titles drove ~12% of Everi’s gaming revenue in FY2024 (ended Dec 31, 2024), per company filings.

Popular IP owners can demand royalties of 10–25% of net gaming revenues, squeezing margins on those titles and raising break-even install costs.

Licensing deals boost player acquisition but increase supplier bargaining power, forcing Everi to balance portfolio mix toward in‑house content.

- ~12% of gaming revenue from branded IP (FY2024)

- Typical royalty range 10–25% of net gaming revenue

- Higher royalties raise break-even installs and cut margins

Suppliers wield strong leverage: hardware, branded IP & FinTech fees pressure Everi

Suppliers hold moderate-to-high bargaining power: specialized hardware vendors and branded-IP licensors limit substitutes, FinTech networks (Visa/Mastercard) exert high leverage, and tight labor markets and regulators raise costs; Everi’s 2024 hardware rev $182.3M, branded-IP ~12% of gaming rev, compliance SG&A +6% (2024).

| Factor | 2024 data |

|---|---|

| Hardware rev | $182.3M |

| Branded IP | ~12% gaming rev |

| Compliance SG&A | +6% |

| Visa/Mastercard | $13.4T processed (2024) |

What is included in the product

Tailored Five Forces analysis for Everi that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging disruptors, with strategic commentary and industry context to inform investor decks and internal strategy.

Everi Porter's Five Forces: a one-sheet, customizable summary that visualizes competitive pressure with an instant spider chart—ready to copy into decks, tweak for scenarios, and integrate into broader reports without macros or coding.

Customers Bargaining Power

Concentration of Major Casino Operators

The casino market is heavily concentrated: the top 10 U.S. operators controlled about 55% of casino revenue in 2024, giving them strong purchasing power and big volume needs.

These multi-property buyers push for volume discounts and bespoke FinTech integrations—Everi earned ~45% of 2024 revenue from its largest 20 customers, which boosts buyer leverage in pricing and contract terms.

High Switching Costs for FinTech

Once a casino integrates Everi’s financial access and compliance tools, switching costs are high: Everi reported 2024 recurring revenue of $611 million, with core transaction services tightly linked to back-office and loyalty systems, making migration complex and costly for operators.

Performance-Based Leasing Models

Many casino operators prefer participation models, paying a percentage of daily win (commonly 10–20%) instead of buying machines, shifting revenue risk to Everi and reducing operators capital outlay.

This gives operators leverage to demand top-performing titles; Everi needs hit rates above ~5–7% daily win uplift to keep floor share, or operators will request removal.

If a game underperforms, operators can replace it within weeks, forcing Everi to release new content frequently—Everi launched 24 new cabinet titles in 2024 to respond.

Demand for Omnichannel Solutions

As operators expand into online gaming and sports betting, buyers demand vendors delivering seamless cross-platform experiences; in 2024 global iGaming gross gaming revenue rose ~8% to $70B, pushing operators to pick partners with unified stacks.

Buyers can choose vendors offering broad digital and physical payments—Everi reported 2024 cashless terminal installs up ~15%, but faces rivals with end-to-end wallets and sportsbook integrations.

Everi must align its product roadmap to retain share versus versatile competitors; missing omnichannel features risks losing contracts worth millions in ARR.

- Operators favor unified omnichannel vendors

- 2024 iGaming GGR ≈ $70B (up ~8%)

- Everi cashless installs +15% in 2024

- Omnichannel gaps risk multi‑million ARR losses

Price Sensitivity in Regional Markets

- 40% of U.S. outlets are tribal/regional

- 62% prioritize price (2024 survey)

- Typical cabinet price: $18k–$35k

- Premium features can boost LTV 10–18%

Operator Concentration Fuels Price Pressure; Everi Leans on Recurring Revenue & Fast Titles

Buyers (top 10 operators ~55% revenue) wield strong leverage—Everi got ~45% of 2024 revenue from its top 20 clients, raising price/contract pressure; high switching costs (2024 recurring revenue $611M) help Everi, but operators demand omnichannel, fast-performing titles (24 new cabinet titles in 2024) and favor participation models (10–20% of daily win), forcing frequent content and bundled pricing updates.

| Metric | 2024 |

|---|---|

| Top-10 operator share | ≈55% |

| Revenue from top 20 | ≈45% |

| Recurring revenue | $611M |

| New cabinet titles | 24 |

Same Document Delivered

Everi Porter's Five Forces Analysis

This preview shows the exact Everi Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No mockups or samples: the document on display is the final deliverable and will be available for instant download once you complete your payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Everi operates in a competitive, regulated payments-and-gaming tech niche where buyer sophistication and regulatory pressure shape margins, while supplier leverage and substitute digital payment options pose clear threats.

This snapshot highlights key tensions—scale-driven advantages vs. nimble fintech entrants—and flags areas where strategic moves can alter industry dynamics.

Ready to move beyond the basics? Get a full strategic breakdown of Everi’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Specialized Component Manufacturers

The production of Everi gaming cabinets relies on specialized electronic components and high-quality displays from a small set of global suppliers, giving suppliers moderate bargaining power.

Semiconductor shortages in 2021–22 raised component costs ~15–25% industrywide and occasional logistics delays; Everi reported hardware revenue 2024: $182.3M, so supply disruptions can notably hit order fulfillment.

Everi uses multiple sourcing and regional partners, but casino-grade specs limit substitute options, keeping supplier leverage moderate rather than low.

Financial Network Infrastructure

Everi’s FinTech segment depends on global networks like Visa and Mastercard, which set interchange and processing fees—Visa and Mastercard together processed $13.4 trillion in payments in 2024—forcing Everi to accept standardized pricing and rates. These networks also impose technical and security standards (EMV, PCI DSS) that raise compliance and integration costs for Everi. Given Visa/Mastercard scale and limited alternatives, Everi has minimal bargaining power, so supplier pressure is high.

Software Development Talent

The tight labor market for software engineers and game designers raises supplier power for Everi; US tech job openings were 9.1M in 2024 and average software engineer salary rose ~6% to $140K in 2024, forcing higher pay and benefits.

Regulatory Compliance Agencies

Regulatory compliance agencies act as gatekeepers to legal operating capacity, forcing Everi Holdings Inc to spend heavily on compliance and third-party audits across US and Canadian jurisdictions.

Everi reported compliance-related SG&A rising 6% in 2024, and licensing fee hikes or tightened standards can raise operating costs without adding product value; a single-state license renewal can cost $0.5–2.0M upfront.

What this hides: sudden regulatory changes can delay deployments and compress margins, increasing volatility in quarterly EBITDA.

- Regulatory bodies = supplier-like gatekeepers

- Everi compliance costs up 6% in 2024

- Single-state license: $0.5–2.0M

- Policy shifts can delay revenue, compress EBITDA

Third-Party Content Creators

Everi partners with external studios and IP holders to build branded slots and games that attract fans of franchises; these titles drove ~12% of Everi’s gaming revenue in FY2024 (ended Dec 31, 2024), per company filings.

Popular IP owners can demand royalties of 10–25% of net gaming revenues, squeezing margins on those titles and raising break-even install costs.

Licensing deals boost player acquisition but increase supplier bargaining power, forcing Everi to balance portfolio mix toward in‑house content.

- ~12% of gaming revenue from branded IP (FY2024)

- Typical royalty range 10–25% of net gaming revenue

- Higher royalties raise break-even installs and cut margins

Suppliers wield strong leverage: hardware, branded IP & FinTech fees pressure Everi

Suppliers hold moderate-to-high bargaining power: specialized hardware vendors and branded-IP licensors limit substitutes, FinTech networks (Visa/Mastercard) exert high leverage, and tight labor markets and regulators raise costs; Everi’s 2024 hardware rev $182.3M, branded-IP ~12% of gaming rev, compliance SG&A +6% (2024).

| Factor | 2024 data |

|---|---|

| Hardware rev | $182.3M |

| Branded IP | ~12% gaming rev |

| Compliance SG&A | +6% |

| Visa/Mastercard | $13.4T processed (2024) |

What is included in the product

Tailored Five Forces analysis for Everi that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging disruptors, with strategic commentary and industry context to inform investor decks and internal strategy.

Everi Porter's Five Forces: a one-sheet, customizable summary that visualizes competitive pressure with an instant spider chart—ready to copy into decks, tweak for scenarios, and integrate into broader reports without macros or coding.

Customers Bargaining Power

Concentration of Major Casino Operators

The casino market is heavily concentrated: the top 10 U.S. operators controlled about 55% of casino revenue in 2024, giving them strong purchasing power and big volume needs.

These multi-property buyers push for volume discounts and bespoke FinTech integrations—Everi earned ~45% of 2024 revenue from its largest 20 customers, which boosts buyer leverage in pricing and contract terms.

High Switching Costs for FinTech

Once a casino integrates Everi’s financial access and compliance tools, switching costs are high: Everi reported 2024 recurring revenue of $611 million, with core transaction services tightly linked to back-office and loyalty systems, making migration complex and costly for operators.

Performance-Based Leasing Models

Many casino operators prefer participation models, paying a percentage of daily win (commonly 10–20%) instead of buying machines, shifting revenue risk to Everi and reducing operators capital outlay.

This gives operators leverage to demand top-performing titles; Everi needs hit rates above ~5–7% daily win uplift to keep floor share, or operators will request removal.

If a game underperforms, operators can replace it within weeks, forcing Everi to release new content frequently—Everi launched 24 new cabinet titles in 2024 to respond.

Demand for Omnichannel Solutions

As operators expand into online gaming and sports betting, buyers demand vendors delivering seamless cross-platform experiences; in 2024 global iGaming gross gaming revenue rose ~8% to $70B, pushing operators to pick partners with unified stacks.

Buyers can choose vendors offering broad digital and physical payments—Everi reported 2024 cashless terminal installs up ~15%, but faces rivals with end-to-end wallets and sportsbook integrations.

Everi must align its product roadmap to retain share versus versatile competitors; missing omnichannel features risks losing contracts worth millions in ARR.

- Operators favor unified omnichannel vendors

- 2024 iGaming GGR ≈ $70B (up ~8%)

- Everi cashless installs +15% in 2024

- Omnichannel gaps risk multi‑million ARR losses

Price Sensitivity in Regional Markets

- 40% of U.S. outlets are tribal/regional

- 62% prioritize price (2024 survey)

- Typical cabinet price: $18k–$35k

- Premium features can boost LTV 10–18%

Operator Concentration Fuels Price Pressure; Everi Leans on Recurring Revenue & Fast Titles

Buyers (top 10 operators ~55% revenue) wield strong leverage—Everi got ~45% of 2024 revenue from its top 20 clients, raising price/contract pressure; high switching costs (2024 recurring revenue $611M) help Everi, but operators demand omnichannel, fast-performing titles (24 new cabinet titles in 2024) and favor participation models (10–20% of daily win), forcing frequent content and bundled pricing updates.

| Metric | 2024 |

|---|---|

| Top-10 operator share | ≈55% |

| Revenue from top 20 | ≈45% |

| Recurring revenue | $611M |

| New cabinet titles | 24 |

Same Document Delivered

Everi Porter's Five Forces Analysis

This preview shows the exact Everi Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No mockups or samples: the document on display is the final deliverable and will be available for instant download once you complete your payment.