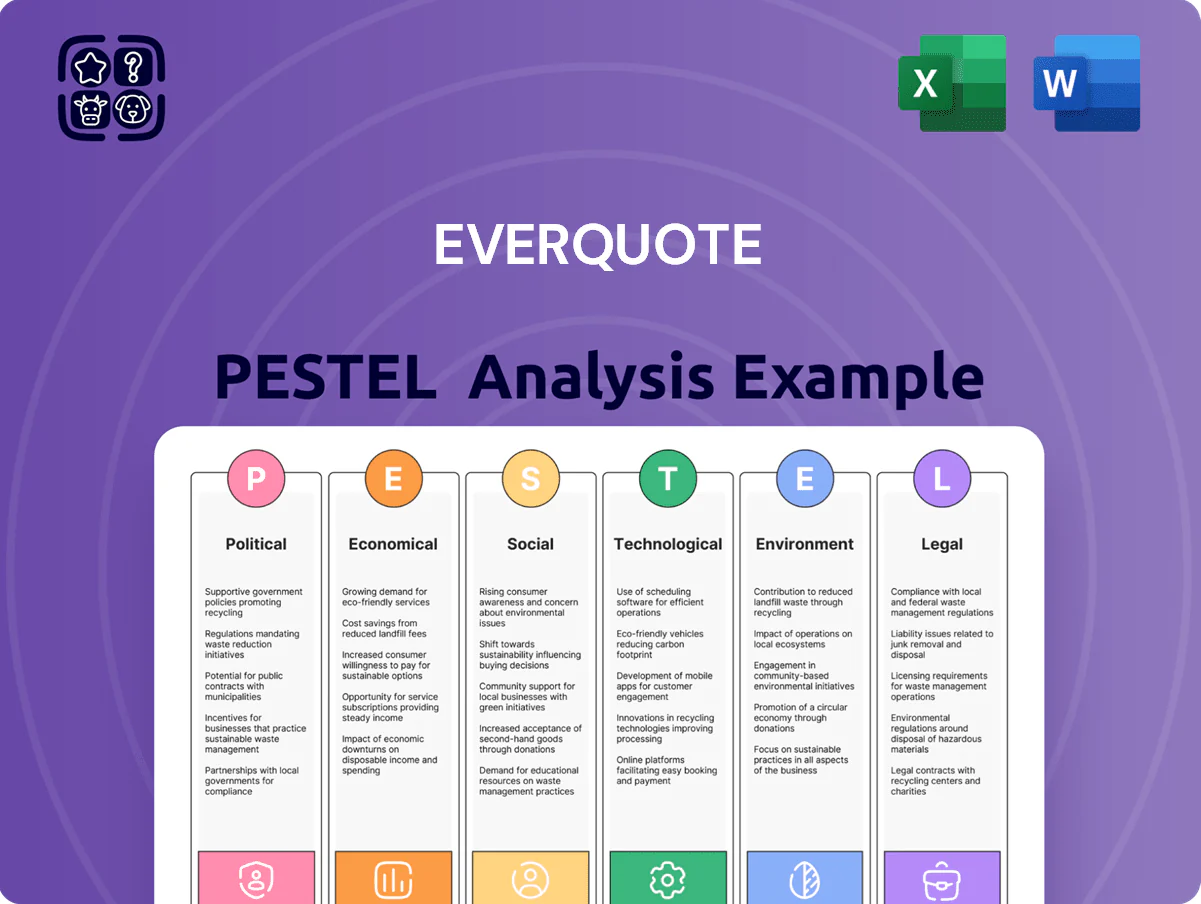

EverQuote PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and rapid tech innovation are reshaping EverQuote’s growth trajectory in our concise PESTLE snapshot—designed for investors and strategists who need swift, actionable insight; purchase the full PESTLE to access the detailed risks, opportunities, and strategic recommendations that will inform smarter decisions.

Political factors

State Insurance Department Oversight

State insurance departments set licensing and operational rules for intermediaries like EverQuote, with 50 distinct regimes requiring ongoing compliance; as of 2025 EverQuote reports operations spanning all 50 states, driving material administrative overhead. Shifts in state leadership affect rate approval timelines—for example slower approvals in 2023–24 correlated with a 4–6% variation in carrier pricing on marketplaces—pressuring margin and go-to-market speed.

Federal Data Privacy Legislation

The push for a unified federal data privacy law remained central through late 2025, with Congress reporting over 20 competing bills and a White House framework proposing national baseline standards; this could replace 50+ state rules and simplify compliance for EverQuote.

However, a federal law may impose stricter consent, data minimization, and breach-notice standards that could raise EverQuote’s compliance costs—estimated industry-wide at $1–3 billion annually—and constrain use of lead-level attributes in matching algorithms.

Political control of Congress and the presidency materially alters passage odds: analysts placed bipartisan compromise at ~40% in late 2025, making regulatory risk a key variable for EverQuote’s data-driven revenue models that reported $432 million in 2024 revenue.

Government Healthcare Policy

Ongoing political debates over the Affordable Care Act and public options materially affect the private insurance market; changes could alter EverQuote’s addressable health-insurance leads, with the U.S. uninsured rate at 8.6% in 2024 and ACA marketplace enrollment at ~14.4 million for 2024 influencing demand. Legislative shifts in subsidies or enrollment windows (e.g., 2024 subsidy changes) can quickly sway consumer searches and insurer participation, impacting EverQuote’s revenue per lead and conversion rates.

Trade Tariffs on Auto Parts

Political decisions raising tariffs on imported auto parts increase repair costs; US auto parts tariffs rose in 2018–2022 episodes, adding 5–10% to component costs and contributing to 2023 average repair-bill inflation of about 7% year-over-year.

Higher repair costs push insurers to raise premiums—US private auto premiums climbed ~6% in 2023—driving price-sensitive consumers toward EverQuote’s comparison platform, where lead volume grew ~12% in 2023.

However, extreme premium spikes can reduce purchase intent and lower lead conversion; regulatory shocks in 2020–2024 showed conversion declines of 8–15% during acute market stress.

- Tariff-driven repair inflation: +5–10% component cost, ~7% repair-bill inflation (2023)

- Insurer premium response: ~6% private auto premium rise (2023)

- EverQuote impact: ~12% lead volume growth (2023)

- Conversion risk: −8–15% during severe premium shocks (2020–2024)

Subsidized Insurance Programs

Government-backed programs like FAIR plans and state-backed wind pools, which covered roughly 1.2 million homeowners in high-risk U.S. markets in 2024, reduce premiums and alter price competition for private insurers, shrinking EverQuote’s addressable market in those ZIP codes.

As political pressure grows to expand subsidies after 2023–2025 catastrophe losses (insured U.S. catastrophe losses averaged about $75B annually 2021–2024), EverQuote must integrate public options into its marketplace and quoting logic to remain relevant.

Shifts in legislative appetite to subsidize risk—evident in 2024 state budget allocations increasing FAIR plan funding by up to 15% in some states—can rapidly reallocate policyholders between public and private carriers, affecting EverQuote referral volumes and commissions.

- FAIR plans/state pools: ~1.2M policies (2024)

- Insured catastrophe losses: ~$75B annual avg (2021–2024)

- 2024 state FAIR funding increases: up to +15% in select states

Regulatory shifts, privacy costs, and market forces reshape insurance lead economics

State-level insurance regimes (50 states) raise compliance costs; EverQuote reported operations in all 50 states and $432M revenue (2024). Federal privacy law uncertainty (20+ bills late 2025) could centralize rules but raise compliance costs (industry $1–3B). Health policy shifts (ACA enrollment ~14.4M, uninsured 8.6% in 2024) and catastrophe subsidies (~$75B avg insured losses 2021–2024) alter lead pools.

| Metric | Value |

|---|---|

| EverQuote 2024 Revenue | $432M |

| ACA 2024 Enrollment | ~14.4M |

| U.S. Uninsured Rate 2024 | 8.6% |

| Insured Catastrophe Losses (avg 2021–24) | $75B |

| Estimated industry privacy compliance cost | $1–3B |

What is included in the product

Explores how external macro-environmental factors uniquely affect EverQuote across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities.

Condenses EverQuote's PESTLE insights into a ready-to-use summary, ideal for dropping into presentations or sharing across teams to streamline external risk and market positioning discussions.

Economic factors

Interest Rate Fluctuations

As of late 2025, US 10-year Treasury yields near 4.5% boosted insurer investment income, with life/auto carriers reporting ~10–15% higher investment yields vs 2022, supporting larger marketing budgets and increased demand for EverQuote leads.

Inflationary Pressure on Claims

Persistent inflation in labor and parts has pushed US auto claim severity up ~18% from 2019–2023; homeowners claim severity rose ~22% over the same period, prompting carriers to file average private-passenger auto rate increases of ~12% in 2023–2024, driving traffic to EverQuote as consumers shop. If inflation outpaces real wage growth—median US wages rose ~6% 2019–2023 while CPI rose ~20%—policyholders may reduce limits, lowering lead lifetime value for EverQuote.

Consumer Spending Power

Disposable income levels directly affect demand for higher-value insurance and riders; US real median household income rose 5.6% to $74,580 in 2023 but remained 1.1% below 2019, influencing purchase of add-ons and comprehensive policies.

During recessions consumers shift to basic liability, reducing EverQuote’s higher-margin leads; 2023 US personal savings rate averaged 3.7%, constraining discretionary insurance spend.

EverQuote’s revenue correlates with middle-class asset maintenance—median net worth for middle-income households was about $121,700 in 2023, impacting propensity to insure vehicles and homes.

Vehicle Market Volatility

- Inventory: new-vehicle inventory ~1.5M (2024)

- Sales: US light-vehicle sales ~14.9M (2024)

- Financing: avg new-car APR ~8.5% (2025)

Advertising Spend Trends

Economic expansion raises digital ad CPCs; US search ad prices rose ~18% in 2024 year‑over‑year, pressuring EverQuote’s lead costs and compressing margins on pay‑per‑click acquisition.

Higher competition for high‑intent insurance keywords during growth periods increases customer acquisition cost (CAC), requiring tighter marketing ROAS targets.

EverQuote must align its spend with insurers’ fluctuating ad budgets—insurer digital ad spend moved +/-10% across 2023–2024—impacting available lead pricing and volume.

- 2024 US search ad price +18% YoY

- Insurer digital budgets varied ~±10% (2023–2024)

- Higher CPCs raise EverQuote CAC, squeezing margins

Rising rates and claims squeeze margins as tight auto market and higher CPCs boost costs

Macro rates and higher investment yields (US 10Y ~4.5% in late‑2025) boosted insurer marketing budgets and EverQuote lead demand, while sustained inflation raised claim severity (~18% auto, ~22% homeowners 2019–2023) and prompted ~12% premium rate filings in 2023–24, increasing shopping activity.

Real median household income up 5.6% to $74,580 in 2023 but still below 2019, plus a 3.7% savings rate in 2023, constrain add‑on purchases and LTV.

Auto market tightness—new‑vehicle inventory ~1.5M (2024), US light‑vehicle sales ~14.9M (2024), avg new‑car APR ~8.5% (2025)—increases used prices and depresses originations; higher search CPCs (+18% in 2024) raise CAC, squeezing margins.

| Metric | Value |

|---|---|

| US 10Y yield | ~4.5% (late‑2025) |

| Auto claim severity | +18% (2019–2023) |

| Homeowners severity | +22% (2019–2023) |

| Median HH income | $74,580 (2023) |

| New‑vehicle inventory | ~1.5M (2024) |

| Light‑vehicle sales | 14.9M (2024) |

| Avg new‑car APR | ~8.5% (2025) |

| Search ad price | +18% YoY (2024) |

Same Document Delivered

EverQuote PESTLE Analysis

The preview shown here is the exact EverQuote PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly the final file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and rapid tech innovation are reshaping EverQuote’s growth trajectory in our concise PESTLE snapshot—designed for investors and strategists who need swift, actionable insight; purchase the full PESTLE to access the detailed risks, opportunities, and strategic recommendations that will inform smarter decisions.

Political factors

State Insurance Department Oversight

State insurance departments set licensing and operational rules for intermediaries like EverQuote, with 50 distinct regimes requiring ongoing compliance; as of 2025 EverQuote reports operations spanning all 50 states, driving material administrative overhead. Shifts in state leadership affect rate approval timelines—for example slower approvals in 2023–24 correlated with a 4–6% variation in carrier pricing on marketplaces—pressuring margin and go-to-market speed.

Federal Data Privacy Legislation

The push for a unified federal data privacy law remained central through late 2025, with Congress reporting over 20 competing bills and a White House framework proposing national baseline standards; this could replace 50+ state rules and simplify compliance for EverQuote.

However, a federal law may impose stricter consent, data minimization, and breach-notice standards that could raise EverQuote’s compliance costs—estimated industry-wide at $1–3 billion annually—and constrain use of lead-level attributes in matching algorithms.

Political control of Congress and the presidency materially alters passage odds: analysts placed bipartisan compromise at ~40% in late 2025, making regulatory risk a key variable for EverQuote’s data-driven revenue models that reported $432 million in 2024 revenue.

Government Healthcare Policy

Ongoing political debates over the Affordable Care Act and public options materially affect the private insurance market; changes could alter EverQuote’s addressable health-insurance leads, with the U.S. uninsured rate at 8.6% in 2024 and ACA marketplace enrollment at ~14.4 million for 2024 influencing demand. Legislative shifts in subsidies or enrollment windows (e.g., 2024 subsidy changes) can quickly sway consumer searches and insurer participation, impacting EverQuote’s revenue per lead and conversion rates.

Trade Tariffs on Auto Parts

Political decisions raising tariffs on imported auto parts increase repair costs; US auto parts tariffs rose in 2018–2022 episodes, adding 5–10% to component costs and contributing to 2023 average repair-bill inflation of about 7% year-over-year.

Higher repair costs push insurers to raise premiums—US private auto premiums climbed ~6% in 2023—driving price-sensitive consumers toward EverQuote’s comparison platform, where lead volume grew ~12% in 2023.

However, extreme premium spikes can reduce purchase intent and lower lead conversion; regulatory shocks in 2020–2024 showed conversion declines of 8–15% during acute market stress.

- Tariff-driven repair inflation: +5–10% component cost, ~7% repair-bill inflation (2023)

- Insurer premium response: ~6% private auto premium rise (2023)

- EverQuote impact: ~12% lead volume growth (2023)

- Conversion risk: −8–15% during severe premium shocks (2020–2024)

Subsidized Insurance Programs

Government-backed programs like FAIR plans and state-backed wind pools, which covered roughly 1.2 million homeowners in high-risk U.S. markets in 2024, reduce premiums and alter price competition for private insurers, shrinking EverQuote’s addressable market in those ZIP codes.

As political pressure grows to expand subsidies after 2023–2025 catastrophe losses (insured U.S. catastrophe losses averaged about $75B annually 2021–2024), EverQuote must integrate public options into its marketplace and quoting logic to remain relevant.

Shifts in legislative appetite to subsidize risk—evident in 2024 state budget allocations increasing FAIR plan funding by up to 15% in some states—can rapidly reallocate policyholders between public and private carriers, affecting EverQuote referral volumes and commissions.

- FAIR plans/state pools: ~1.2M policies (2024)

- Insured catastrophe losses: ~$75B annual avg (2021–2024)

- 2024 state FAIR funding increases: up to +15% in select states

Regulatory shifts, privacy costs, and market forces reshape insurance lead economics

State-level insurance regimes (50 states) raise compliance costs; EverQuote reported operations in all 50 states and $432M revenue (2024). Federal privacy law uncertainty (20+ bills late 2025) could centralize rules but raise compliance costs (industry $1–3B). Health policy shifts (ACA enrollment ~14.4M, uninsured 8.6% in 2024) and catastrophe subsidies (~$75B avg insured losses 2021–2024) alter lead pools.

| Metric | Value |

|---|---|

| EverQuote 2024 Revenue | $432M |

| ACA 2024 Enrollment | ~14.4M |

| U.S. Uninsured Rate 2024 | 8.6% |

| Insured Catastrophe Losses (avg 2021–24) | $75B |

| Estimated industry privacy compliance cost | $1–3B |

What is included in the product

Explores how external macro-environmental factors uniquely affect EverQuote across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities.

Condenses EverQuote's PESTLE insights into a ready-to-use summary, ideal for dropping into presentations or sharing across teams to streamline external risk and market positioning discussions.

Economic factors

Interest Rate Fluctuations

As of late 2025, US 10-year Treasury yields near 4.5% boosted insurer investment income, with life/auto carriers reporting ~10–15% higher investment yields vs 2022, supporting larger marketing budgets and increased demand for EverQuote leads.

Inflationary Pressure on Claims

Persistent inflation in labor and parts has pushed US auto claim severity up ~18% from 2019–2023; homeowners claim severity rose ~22% over the same period, prompting carriers to file average private-passenger auto rate increases of ~12% in 2023–2024, driving traffic to EverQuote as consumers shop. If inflation outpaces real wage growth—median US wages rose ~6% 2019–2023 while CPI rose ~20%—policyholders may reduce limits, lowering lead lifetime value for EverQuote.

Consumer Spending Power

Disposable income levels directly affect demand for higher-value insurance and riders; US real median household income rose 5.6% to $74,580 in 2023 but remained 1.1% below 2019, influencing purchase of add-ons and comprehensive policies.

During recessions consumers shift to basic liability, reducing EverQuote’s higher-margin leads; 2023 US personal savings rate averaged 3.7%, constraining discretionary insurance spend.

EverQuote’s revenue correlates with middle-class asset maintenance—median net worth for middle-income households was about $121,700 in 2023, impacting propensity to insure vehicles and homes.

Vehicle Market Volatility

- Inventory: new-vehicle inventory ~1.5M (2024)

- Sales: US light-vehicle sales ~14.9M (2024)

- Financing: avg new-car APR ~8.5% (2025)

Advertising Spend Trends

Economic expansion raises digital ad CPCs; US search ad prices rose ~18% in 2024 year‑over‑year, pressuring EverQuote’s lead costs and compressing margins on pay‑per‑click acquisition.

Higher competition for high‑intent insurance keywords during growth periods increases customer acquisition cost (CAC), requiring tighter marketing ROAS targets.

EverQuote must align its spend with insurers’ fluctuating ad budgets—insurer digital ad spend moved +/-10% across 2023–2024—impacting available lead pricing and volume.

- 2024 US search ad price +18% YoY

- Insurer digital budgets varied ~±10% (2023–2024)

- Higher CPCs raise EverQuote CAC, squeezing margins

Rising rates and claims squeeze margins as tight auto market and higher CPCs boost costs

Macro rates and higher investment yields (US 10Y ~4.5% in late‑2025) boosted insurer marketing budgets and EverQuote lead demand, while sustained inflation raised claim severity (~18% auto, ~22% homeowners 2019–2023) and prompted ~12% premium rate filings in 2023–24, increasing shopping activity.

Real median household income up 5.6% to $74,580 in 2023 but still below 2019, plus a 3.7% savings rate in 2023, constrain add‑on purchases and LTV.

Auto market tightness—new‑vehicle inventory ~1.5M (2024), US light‑vehicle sales ~14.9M (2024), avg new‑car APR ~8.5% (2025)—increases used prices and depresses originations; higher search CPCs (+18% in 2024) raise CAC, squeezing margins.

| Metric | Value |

|---|---|

| US 10Y yield | ~4.5% (late‑2025) |

| Auto claim severity | +18% (2019–2023) |

| Homeowners severity | +22% (2019–2023) |

| Median HH income | $74,580 (2023) |

| New‑vehicle inventory | ~1.5M (2024) |

| Light‑vehicle sales | 14.9M (2024) |

| Avg new‑car APR | ~8.5% (2025) |

| Search ad price | +18% YoY (2024) |

Same Document Delivered

EverQuote PESTLE Analysis

The preview shown here is the exact EverQuote PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly the final file you’ll be able to download immediately after payment.