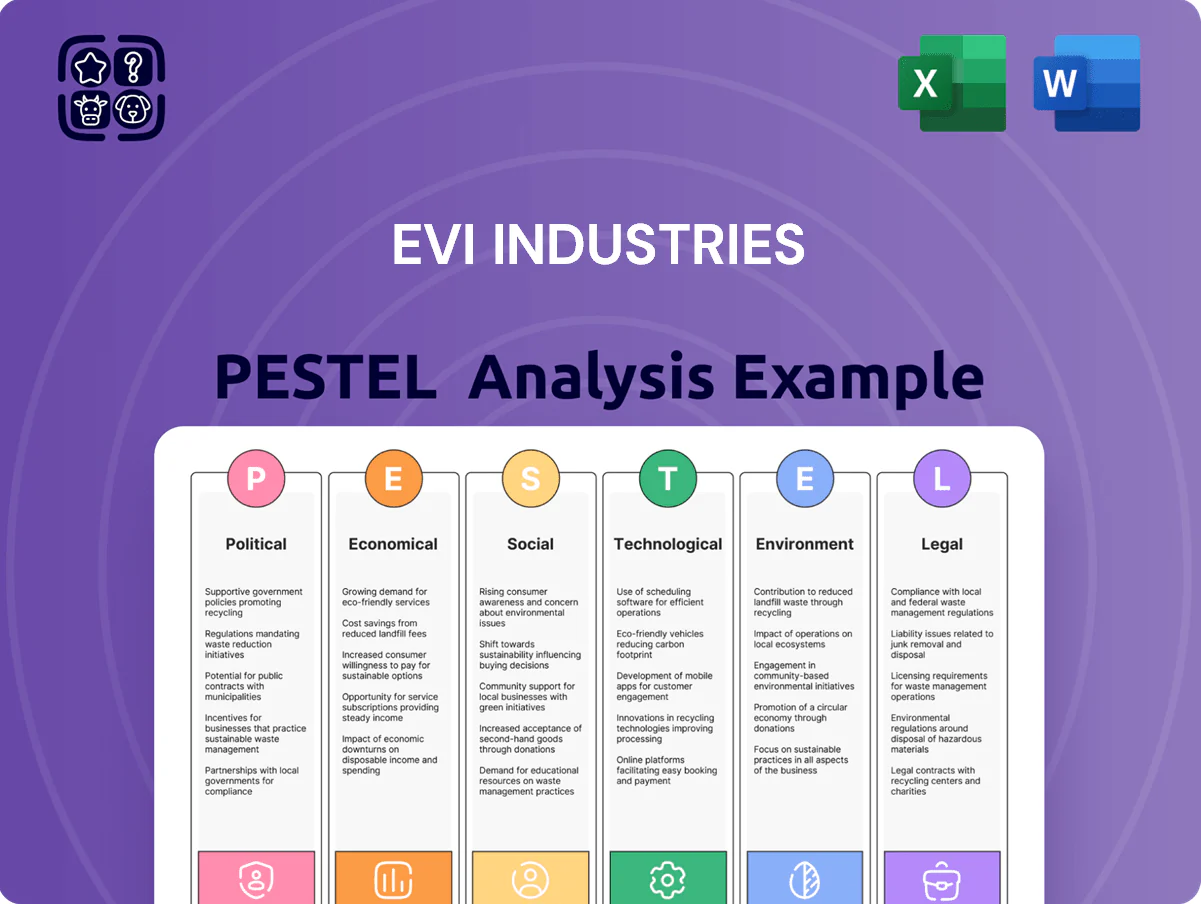

EVI Industries PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic foresight with our PESTLE Analysis of EVI Industries—spot regulatory, economic, and technological forces shaping its trajectory and turn insights into actionable strategy. Ideal for investors and planners, this concise, expert report saves you time and sharpens decision-making. Purchase the full version now for the complete, editable breakdown and immediate download.

Political factors

Trade Policy and Tariffs

Changes in international trade agreements or new tariffs on imported commercial laundry machinery could raise EVI Industries' procurement costs by an estimated 5–12%, given its 60% reliance on overseas suppliers; recent U.S. tariffs added 7%–10% on industrial equipment in 2024. Protectionist measures risk margin compression—EVI reported a 14.8% gross margin in FY2024—forcing price increases or cost pass-through. Monitoring North American trade relations, where 48% of 2024 revenue originated, is critical to keep hardware pricing competitive.

Government Infrastructure Spending

Federal and state funding for VA hospitals, correctional facilities and government housing—federal health construction outlays rose to $12.5B in FY2024 and state capital spending reached $125B in 2024—increases demand for EVI’s large-scale laundry systems through long-term procurement contracts tied to modernization projects.

Expanded public-sector capital budgets supported a 6–8% CAGR in institutional equipment spending from 2021–2024, providing steady multi-year revenue opportunities for EVI, while austerity or sequestration risks could defer upgrades and compress order pipelines.

Tax Incentives for Capital Investment

Political moves like the 2025 US bonus depreciation reinstatement and 30% tax credits for energy-efficient equipment boost EVI Industries’ sales by lowering after-tax cost; firms replacing laundry fleets saw capex upticks of 18% in 2024–2025 within commercial services. Immediate expensing increases ROI payback periods by 30–40%, accelerating replacement cycles and enlarging addressable market for EVI’s machines, critical for sector turnover rates.

Labor Relations and Union Influence

Political shifts expanding collective bargaining and recent 2024 US state laws tightening union rules affect EVI’s workforce and clients across hospitality and industrial sectors; national union membership rose to 10.1% in 2023, up from 9.8% in 2022, raising wage negotiation pressure.

Higher unionization and rising minimum wages (US median wage growth ~4.5% in 2024) can lift EVI service labor costs and marginally compress EBITDA margins for service lines.

Textile rental strikes and supply-chain labor disputes—e.g., 2023 industry shutdowns reducing client output by up to 6% in quarters—can cut EVI volume handled and revenue predictability.

- Union membership 10.1% (2023)

- Wage growth ~4.5% (2024)

- Industry disruptions can reduce client volume ~6%

Geopolitical Stability and Supply Chains

Ongoing geopolitical tensions, including 2024 trade restrictions and 2025 Red Sea shipping disruptions, risk interrupting manufacture and transit of specialized laundry equipment parts, raising lead times by up to 30% in some corridors.

EVI must manage supply-chain fragility from international conflicts and regional instability, where single-supplier outages have driven component price spikes of 12–18% in 2024.

Maintaining a diversified supplier base across at least three regions is a political necessity to limit part shortages and delivery delays affecting service revenue and uptime.

- 2024 shipping delays up to 30%

- Component price spikes 12–18% in 2024

- Target: suppliers in ≥3 regions

Tariffs, wages and supply shocks threaten EVI margins despite a public-capex-led demand boost

Political risks like tariffs (7%–10% added in 2024) and trade disruptions (lead times +30%) could raise EVI’s COGS by 5–12%, pressuring a FY2024 gross margin of 14.8% and requiring price or supply adjustments.

Increased public-sector capex (federal health construction $12.5B, state capital $125B in 2024) and tax incentives (2025 bonus depreciation, 30% EE credits) boosted institutional orders, lifting capex replacements ~18% in 2024–25.

Rising unionization (10.1% in 2023) and wage growth (~4.5% in 2024) increase service labor costs, compressing EBITDA on service lines; supplier diversification (≥3 regions) is recommended to limit component spikes (12–18% in 2024).

| Metric | Value |

|---|---|

| Tariffs added (2024) | 7%–10% |

| COGS risk | +5–12% |

| Gross margin FY2024 | 14.8% |

| Federal health construction (2024) | $12.5B |

| State capital spending (2024) | $125B |

| Capex uptick (2024–25) | ~18% |

| Union membership (2023) | 10.1% |

| Wage growth (2024) | ~4.5% |

| Component price spikes (2024) | 12–18% |

| Lead time increases | up to 30% |

| Supplier diversification | ≥3 regions |

What is included in the product

Explores how external macro-environmental factors uniquely affect EVI Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify threats and opportunities for executives and investors.

Condenses EVI Industries' full PESTLE into a clear, shareable snapshot that teams can drop into presentations or planning docs to quickly align on external risks and strategic implications.

Economic factors

Interest Rate Volatility

Fluctuations in interest rates raise financing costs for EVI customers who rely on loans or leases for industrial equipment; U.S. prime rates rose from 3.25% in 2021 to 8.50% by Dec 2023, dampening equipment purchases in 2024 with CapEx intentions down ~12% in hospitality and ~9% in healthcare year-over-year. Higher rates also increase EVI’s weighted average cost of capital, making acquisitions pricier under tighter central bank policy.

Inflationary Pressure on Service Costs

Rising inflation—US CPI up 3.4% year-on-year in 2025 and global fuel prices averaging 14% higher than 2023—raises costs for raw materials, spare parts, and diesel for EVI’s mobile service fleet, increasing per-job operating expense. EVI can pass some increases via variable billing, but fixed-price maintenance contracts face margin compression when input costs spike rapidly. Between Jan 2024–Dec 2025, supplier lead-time inflation added an estimated 6–9% to parts procurement costs, forcing tighter cost controls. Balancing competitive pricing with rising overheads remains a material economic risk to profitability.

Hospitality and Tourism Performance

The global travel and tourism sector contributed 9.8% of world GDP in 2023 and saw a 37% rebound in international arrivals vs 2022, driving higher hotel occupancy and boosting demand for EVI Industries’ commercial laundry installations and maintenance in 2024; RevPAR growth averaged 8–12% in key markets, increasing linen turnover and service cycles. During 2023–24 expansion EVI reported higher equipment orders, while industry downturns like a 2024 regional slowdown that cut arrivals by 15% led to delayed capex and reduced service frequency.

Labor Market Tightness

Labor market tightness in North America, with US unemployment around 3.7% (2024) and technician vacancy rates in advanced manufacturing/services estimated 5–7%, pressures EVI Industries to raise technician wages—reported median pay rises of 4–6% in 2024—making service scaling costlier and necessitating larger recruitment/retention spend.

- Skilled technician shortage drives 4–6% wage inflation (2024)

- Technician vacancy rates ~5–7% increase hiring difficulty

- Low unemployment (3.7% US, 2024) raises retention costs

- Higher HR/recruitment spend needed to sustain service scale

Consolidation Trends in the Industry

Economic cycles drive EVI’s M&A tempo; during 2024 PE-backed deal value in US distribution rose 18% y/y to $42bn, supporting EVI’s buy-and-build acquisitions of regional distributors to scale its national reach.

Low interest rates and abundant capital in 2023–24 enabled smaller add-ons, while 2025 tightening could curb leverage; recession windows offer distressed targets at lower multiples but with reduced credit availability.

- Strong 2024 deal market: +18% y/y, $42bn

- Favorable 2023–24 capital = easier add-ons

- Downturns = cheaper targets but tighter credit

Higher rates, rising costs and travel rebound reshape linen & equipment demand

Interest-rate rise to 8.50% (Dec 2023) raised borrowing costs and CapEx intentions fell ~10% across key clients in 2024; US CPI ~3.4% (2025) and +14% fuel vs 2023 increased operating costs; travel rebound (international arrivals +37% vs 2022) boosted linen demand and equipment orders in 2024; US unemployment ~3.7% (2024) drove technician wage inflation 4–6%.

| Metric | Value |

|---|---|

| US prime rate (Dec 2023) | 8.50% |

| US CPI (2025) | 3.4% |

| Fuel vs 2023 | +14% |

| Intl arrivals rebound (vs 2022) | +37% |

| US unemployment (2024) | 3.7% |

| Technician wage inflation (2024) | 4–6% |

Preview the Actual Deliverable

EVI Industries PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of EVI Industries covering political, economic, social, technological, legal, and environmental factors to inform strategy and investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic foresight with our PESTLE Analysis of EVI Industries—spot regulatory, economic, and technological forces shaping its trajectory and turn insights into actionable strategy. Ideal for investors and planners, this concise, expert report saves you time and sharpens decision-making. Purchase the full version now for the complete, editable breakdown and immediate download.

Political factors

Trade Policy and Tariffs

Changes in international trade agreements or new tariffs on imported commercial laundry machinery could raise EVI Industries' procurement costs by an estimated 5–12%, given its 60% reliance on overseas suppliers; recent U.S. tariffs added 7%–10% on industrial equipment in 2024. Protectionist measures risk margin compression—EVI reported a 14.8% gross margin in FY2024—forcing price increases or cost pass-through. Monitoring North American trade relations, where 48% of 2024 revenue originated, is critical to keep hardware pricing competitive.

Government Infrastructure Spending

Federal and state funding for VA hospitals, correctional facilities and government housing—federal health construction outlays rose to $12.5B in FY2024 and state capital spending reached $125B in 2024—increases demand for EVI’s large-scale laundry systems through long-term procurement contracts tied to modernization projects.

Expanded public-sector capital budgets supported a 6–8% CAGR in institutional equipment spending from 2021–2024, providing steady multi-year revenue opportunities for EVI, while austerity or sequestration risks could defer upgrades and compress order pipelines.

Tax Incentives for Capital Investment

Political moves like the 2025 US bonus depreciation reinstatement and 30% tax credits for energy-efficient equipment boost EVI Industries’ sales by lowering after-tax cost; firms replacing laundry fleets saw capex upticks of 18% in 2024–2025 within commercial services. Immediate expensing increases ROI payback periods by 30–40%, accelerating replacement cycles and enlarging addressable market for EVI’s machines, critical for sector turnover rates.

Labor Relations and Union Influence

Political shifts expanding collective bargaining and recent 2024 US state laws tightening union rules affect EVI’s workforce and clients across hospitality and industrial sectors; national union membership rose to 10.1% in 2023, up from 9.8% in 2022, raising wage negotiation pressure.

Higher unionization and rising minimum wages (US median wage growth ~4.5% in 2024) can lift EVI service labor costs and marginally compress EBITDA margins for service lines.

Textile rental strikes and supply-chain labor disputes—e.g., 2023 industry shutdowns reducing client output by up to 6% in quarters—can cut EVI volume handled and revenue predictability.

- Union membership 10.1% (2023)

- Wage growth ~4.5% (2024)

- Industry disruptions can reduce client volume ~6%

Geopolitical Stability and Supply Chains

Ongoing geopolitical tensions, including 2024 trade restrictions and 2025 Red Sea shipping disruptions, risk interrupting manufacture and transit of specialized laundry equipment parts, raising lead times by up to 30% in some corridors.

EVI must manage supply-chain fragility from international conflicts and regional instability, where single-supplier outages have driven component price spikes of 12–18% in 2024.

Maintaining a diversified supplier base across at least three regions is a political necessity to limit part shortages and delivery delays affecting service revenue and uptime.

- 2024 shipping delays up to 30%

- Component price spikes 12–18% in 2024

- Target: suppliers in ≥3 regions

Tariffs, wages and supply shocks threaten EVI margins despite a public-capex-led demand boost

Political risks like tariffs (7%–10% added in 2024) and trade disruptions (lead times +30%) could raise EVI’s COGS by 5–12%, pressuring a FY2024 gross margin of 14.8% and requiring price or supply adjustments.

Increased public-sector capex (federal health construction $12.5B, state capital $125B in 2024) and tax incentives (2025 bonus depreciation, 30% EE credits) boosted institutional orders, lifting capex replacements ~18% in 2024–25.

Rising unionization (10.1% in 2023) and wage growth (~4.5% in 2024) increase service labor costs, compressing EBITDA on service lines; supplier diversification (≥3 regions) is recommended to limit component spikes (12–18% in 2024).

| Metric | Value |

|---|---|

| Tariffs added (2024) | 7%–10% |

| COGS risk | +5–12% |

| Gross margin FY2024 | 14.8% |

| Federal health construction (2024) | $12.5B |

| State capital spending (2024) | $125B |

| Capex uptick (2024–25) | ~18% |

| Union membership (2023) | 10.1% |

| Wage growth (2024) | ~4.5% |

| Component price spikes (2024) | 12–18% |

| Lead time increases | up to 30% |

| Supplier diversification | ≥3 regions |

What is included in the product

Explores how external macro-environmental factors uniquely affect EVI Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify threats and opportunities for executives and investors.

Condenses EVI Industries' full PESTLE into a clear, shareable snapshot that teams can drop into presentations or planning docs to quickly align on external risks and strategic implications.

Economic factors

Interest Rate Volatility

Fluctuations in interest rates raise financing costs for EVI customers who rely on loans or leases for industrial equipment; U.S. prime rates rose from 3.25% in 2021 to 8.50% by Dec 2023, dampening equipment purchases in 2024 with CapEx intentions down ~12% in hospitality and ~9% in healthcare year-over-year. Higher rates also increase EVI’s weighted average cost of capital, making acquisitions pricier under tighter central bank policy.

Inflationary Pressure on Service Costs

Rising inflation—US CPI up 3.4% year-on-year in 2025 and global fuel prices averaging 14% higher than 2023—raises costs for raw materials, spare parts, and diesel for EVI’s mobile service fleet, increasing per-job operating expense. EVI can pass some increases via variable billing, but fixed-price maintenance contracts face margin compression when input costs spike rapidly. Between Jan 2024–Dec 2025, supplier lead-time inflation added an estimated 6–9% to parts procurement costs, forcing tighter cost controls. Balancing competitive pricing with rising overheads remains a material economic risk to profitability.

Hospitality and Tourism Performance

The global travel and tourism sector contributed 9.8% of world GDP in 2023 and saw a 37% rebound in international arrivals vs 2022, driving higher hotel occupancy and boosting demand for EVI Industries’ commercial laundry installations and maintenance in 2024; RevPAR growth averaged 8–12% in key markets, increasing linen turnover and service cycles. During 2023–24 expansion EVI reported higher equipment orders, while industry downturns like a 2024 regional slowdown that cut arrivals by 15% led to delayed capex and reduced service frequency.

Labor Market Tightness

Labor market tightness in North America, with US unemployment around 3.7% (2024) and technician vacancy rates in advanced manufacturing/services estimated 5–7%, pressures EVI Industries to raise technician wages—reported median pay rises of 4–6% in 2024—making service scaling costlier and necessitating larger recruitment/retention spend.

- Skilled technician shortage drives 4–6% wage inflation (2024)

- Technician vacancy rates ~5–7% increase hiring difficulty

- Low unemployment (3.7% US, 2024) raises retention costs

- Higher HR/recruitment spend needed to sustain service scale

Consolidation Trends in the Industry

Economic cycles drive EVI’s M&A tempo; during 2024 PE-backed deal value in US distribution rose 18% y/y to $42bn, supporting EVI’s buy-and-build acquisitions of regional distributors to scale its national reach.

Low interest rates and abundant capital in 2023–24 enabled smaller add-ons, while 2025 tightening could curb leverage; recession windows offer distressed targets at lower multiples but with reduced credit availability.

- Strong 2024 deal market: +18% y/y, $42bn

- Favorable 2023–24 capital = easier add-ons

- Downturns = cheaper targets but tighter credit

Higher rates, rising costs and travel rebound reshape linen & equipment demand

Interest-rate rise to 8.50% (Dec 2023) raised borrowing costs and CapEx intentions fell ~10% across key clients in 2024; US CPI ~3.4% (2025) and +14% fuel vs 2023 increased operating costs; travel rebound (international arrivals +37% vs 2022) boosted linen demand and equipment orders in 2024; US unemployment ~3.7% (2024) drove technician wage inflation 4–6%.

| Metric | Value |

|---|---|

| US prime rate (Dec 2023) | 8.50% |

| US CPI (2025) | 3.4% |

| Fuel vs 2023 | +14% |

| Intl arrivals rebound (vs 2022) | +37% |

| US unemployment (2024) | 3.7% |

| Technician wage inflation (2024) | 4–6% |

Preview the Actual Deliverable

EVI Industries PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of EVI Industries covering political, economic, social, technological, legal, and environmental factors to inform strategy and investment decisions.