Evolent Health Boston Consulting Group Matrix

Actionable Strategy Starts Here

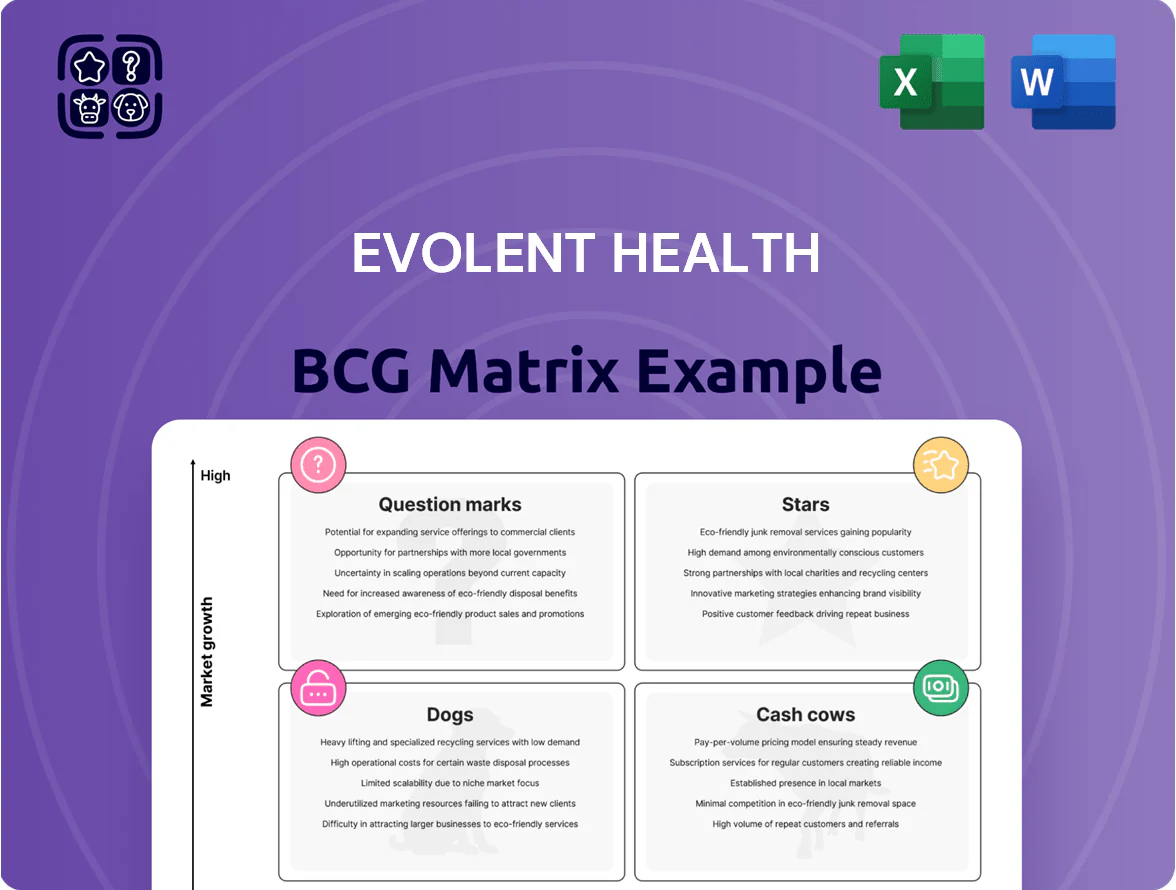

Evolent Health’s BCG Matrix preview highlights how its care-delivery and technology offerings stack up amid shifting payer-provider dynamics, signaling which services are scaling fast, which generate steady cash, and where investments may lag. This snapshot teases quadrant placements and key strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant evidence, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report for data-driven clarity on where to invest, divest, or accelerate growth.

Stars

Specialty Care Management Oncology and Cardiology

By end-2025 Evolent Health's Specialty Care Management (Oncology and Cardiology) sits as a star in the BCG matrix, growing ~18–22% CAGR and generating roughly $420M of segment revenue in 2024 with projected $510M in 2025, driven by outsourced high-cost chronic care management.

The integrated clinical platform and ongoing $60M+ annual R&D on clinical pathways and provider-engagement tools preserve ~35–40% market share in value-based contracts, making these services key drivers of performance-based revenue and enterprise valuation.

Performance-Based Value-Based Care Contracts

Evolent has moved over 60% of its portfolio into performance-based value contracts, sharing savings with payers and providers and driving revenue growth as the industry shifts to total cost-of-care accountability.

These contracts are in a high-growth phase: value-based arrangements grew ~28% year-over-year in 2024, but require heavy upfront clinical investment and data integration—Evolent reported $120M in care transformation spend in 2024.

They are the primary engine for future profitability, contributing ~45% of adjusted EBITDA guidance for 2025, and Evolent’s leading market share in this niche lets it influence industry outcome standards.

Evolent Care Partners ACO Expansion

The Evolent Care Partners unit is a Star, managing ACOs for independent physician practices and capturing a large share of the physician-led ACO market, which grew ~12–15% CAGR 2020–2024; Evolent reported ECP revenues of $182M in FY2024, up ~22% year-over-year.

Advanced AI Clinical Decision Support Tools

Advanced AI Clinical Decision Support Tools drive high growth for Evolent Health by delivering real-time, evidence-based recommendations at point of care, cutting unnecessary medical spend by an estimated 12–18% per case in pilot programs through 2024.

Evolent holds a leading market share in AI-driven specialty authorizations—about 42% vs ~18% for manual-review incumbents—and reported $95M in related ARR in FY2024, positioning the tech to become a cash-generating asset as adoption scales.

- Reduces unnecessary spend 12–18%

- Market share ~42% in AI authorizations (2024)

- $95M ARR from AI tools (FY2024)

- Path to high-margin cash flow as tech matures

Integrated Behavioral Health Services

Integrated Behavioral Health Services is a Stars business for Evolent Health after integrating specialty assets; behavioral management grew ~30% YoY in 2024 and sits atop a market where integrated physical–mental care demand rose after 2023 federal mandates and 2024 employer requirements.

Evolent’s unified platform ties specialty medical and behavioral care, giving it a strong competitive position, creating high entry barriers, and requiring ongoing capital to expand provider network and tech—Evolent spent $120M on network and platform scaling in 2024.

- ~30% YoY growth 2024

- $120M capex for network/platform 2024

- Federal mandates since 2023 expanded market

- High barrier: unified specialty+behavioral platform

Evolent’s Specialty & AI Power Surge: $420M→$510M, 18–22% CAGR, 45% EBITDA

By end-2025 Evolent’s Specialty Care Management and Evolent Care Partners rank as Stars: ~18–22% CAGR, $420M revenue 2024 → $510M projected 2025; AI tools $95M ARR (FY2024) with ~42% market share in authorizations; value-based contracts >60% portfolio, growing 28% YoY (2024) and contributing ~45% of 2025 adjusted EBITDA.

| Metric | 2024 | 2025 proj |

|---|---|---|

| Segment rev (Specialty) | $420M | $510M |

| CAGR (2020–25) | ~18–22% | |

| AI ARR | $95M | — |

| AI market share | 42% | — |

| Value-based portfolio | 60%+ | — |

| VBR growth YoY | 28% | — |

| Care transformation spend | $120M | — |

| Contribution to adj. EBITDA | — | ~45% |

What is included in the product

In-depth BCG review of Evolent Health’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Evolent Health units by growth/share for quick strategic clarity.

Cash Cows

Core Identifi Technology Platform

The Core Identifi Technology Platform is Evolent Health’s mature backbone for health plan and provider partners, delivering population-health data and analytics with estimated >60% share within its existing client base as of 2025 and high switching costs tied to implementations averaging 9–14 months.

It produces steady, predictable recurring revenue—about 40–50% of Evolent’s services revenue in 2024—requiring minimal additional marketing or development spend.

Cash flow from Identifi is routinely redeployed to fund specialty-care growth initiatives, including new-star investments in value-based specialty programs that grew revenue 18% in 2024.

Administrative Service Organization Support

Evolent Health’s Administrative Service Organization Support provides claims processing and member enrollment for mature health plans, operating in a low-growth market (~2–3% annual expansion) while delivering high margins—reported segment-adjusted EBITDA margins around 18% in 2024—so it’s cash-generative.

Legacy Medicaid Managed Care Partnerships

Evolent’s legacy Medicaid managed care partnerships cover multiple states and delivered roughly $800m in revenue in FY2024, reflecting a mature, low-growth segment with contract renewal rates above 90% through 2025.

New Medicaid awards slowed by late 2025, but Evolent still administers a significant share of incumbent plans, generating steady cash flows with minimal capex and high margins.

The predictable margins fund investment into specialty care initiatives, enabling a strategic pivot while preserving liquidity and near-term EPS resilience.

Risk Adjustment and Quality Reporting Services

Risk adjustment and HEDIS quality reporting are mature, standardized offerings; Evolent holds a leading share with ~25–30% penetration among its ACO and payer clients as of 2025, securing steady compliance and revenue-integrity fees.

Maintenance capex is modest—estimated <5% of product revenue—while these services contributed roughly $160–180M in 2024 recurring revenue, enabling reinvestment into growth segments.

That stability lets Evolent focus on higher-growth areas like value-based care tech and provider enablement without risking core cash flow.

- Market: mature, standardized tools

- Evolent share: ~25–30% core clients (2025)

- Recurring revenue: ~$160–180M (2024)

- Maintenance spend: <5% of product revenue

- Strategic effect: funds growth investments

Network Contracting and Provider Relations

Evolent Health’s Network Contracting and Provider Relations is a mature, high-penetration business generating stable cash flow; as of FY 2024 the unit contributed to Evolent’s adjusted EBITDA margin expansion, with company-wide gross margin rising to about 18% in 2024, reflecting strong network economics and scale.

Market growth for network development has slowed, but Evolent’s years of provider data and contracting expertise create a durable competitive moat; the unit runs with high operating margins and low promotional spend, requiring minimal reinvestment while funding strategic initiatives across the firm.

- High penetration: established national networks, long-term contracts

- Low marketing need: stable client retention, recurring revenue

- High margins: contributes materially to adjusted EBITDA (2024 ~18% company gross margin)

- Strategic role: funds growth initiatives, leverages proprietary provider data

Evolent’s $1.1B Cash Cows: High-Retention, Low-Capex Engines Fueling 18% Growth

Identifi platform, ASO, legacy Medicaid, risk-adjustment/HEDIS, and network contracting are Evolent’s cash cows: together they generated ~ $1.1B recurring revenue in 2024, ~18% adjusted gross margin, low maintenance capex (<5% product revenue), >90% contract renewals, and fund specialty growth (18% revenue growth in value-based programs, 2024).

| Metric | 2024/2025 |

|---|---|

| Recurring revenue | $1.1B (2024) |

| Adjusted gross margin | ~18% (2024) |

| Maintenance capex | <5% product rev |

| Contract renewals | >90% (through 2025) |

| Value-based specialty growth | +18% (2024) |

What You’re Viewing Is Included

Evolent Health BCG Matrix

The file you're previewing is the exact Evolent Health BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, professionally designed document ready for strategic use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Evolent Health’s BCG Matrix preview highlights how its care-delivery and technology offerings stack up amid shifting payer-provider dynamics, signaling which services are scaling fast, which generate steady cash, and where investments may lag. This snapshot teases quadrant placements and key strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant evidence, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report for data-driven clarity on where to invest, divest, or accelerate growth.

Stars

Specialty Care Management Oncology and Cardiology

By end-2025 Evolent Health's Specialty Care Management (Oncology and Cardiology) sits as a star in the BCG matrix, growing ~18–22% CAGR and generating roughly $420M of segment revenue in 2024 with projected $510M in 2025, driven by outsourced high-cost chronic care management.

The integrated clinical platform and ongoing $60M+ annual R&D on clinical pathways and provider-engagement tools preserve ~35–40% market share in value-based contracts, making these services key drivers of performance-based revenue and enterprise valuation.

Performance-Based Value-Based Care Contracts

Evolent has moved over 60% of its portfolio into performance-based value contracts, sharing savings with payers and providers and driving revenue growth as the industry shifts to total cost-of-care accountability.

These contracts are in a high-growth phase: value-based arrangements grew ~28% year-over-year in 2024, but require heavy upfront clinical investment and data integration—Evolent reported $120M in care transformation spend in 2024.

They are the primary engine for future profitability, contributing ~45% of adjusted EBITDA guidance for 2025, and Evolent’s leading market share in this niche lets it influence industry outcome standards.

Evolent Care Partners ACO Expansion

The Evolent Care Partners unit is a Star, managing ACOs for independent physician practices and capturing a large share of the physician-led ACO market, which grew ~12–15% CAGR 2020–2024; Evolent reported ECP revenues of $182M in FY2024, up ~22% year-over-year.

Advanced AI Clinical Decision Support Tools

Advanced AI Clinical Decision Support Tools drive high growth for Evolent Health by delivering real-time, evidence-based recommendations at point of care, cutting unnecessary medical spend by an estimated 12–18% per case in pilot programs through 2024.

Evolent holds a leading market share in AI-driven specialty authorizations—about 42% vs ~18% for manual-review incumbents—and reported $95M in related ARR in FY2024, positioning the tech to become a cash-generating asset as adoption scales.

- Reduces unnecessary spend 12–18%

- Market share ~42% in AI authorizations (2024)

- $95M ARR from AI tools (FY2024)

- Path to high-margin cash flow as tech matures

Integrated Behavioral Health Services

Integrated Behavioral Health Services is a Stars business for Evolent Health after integrating specialty assets; behavioral management grew ~30% YoY in 2024 and sits atop a market where integrated physical–mental care demand rose after 2023 federal mandates and 2024 employer requirements.

Evolent’s unified platform ties specialty medical and behavioral care, giving it a strong competitive position, creating high entry barriers, and requiring ongoing capital to expand provider network and tech—Evolent spent $120M on network and platform scaling in 2024.

- ~30% YoY growth 2024

- $120M capex for network/platform 2024

- Federal mandates since 2023 expanded market

- High barrier: unified specialty+behavioral platform

Evolent’s Specialty & AI Power Surge: $420M→$510M, 18–22% CAGR, 45% EBITDA

By end-2025 Evolent’s Specialty Care Management and Evolent Care Partners rank as Stars: ~18–22% CAGR, $420M revenue 2024 → $510M projected 2025; AI tools $95M ARR (FY2024) with ~42% market share in authorizations; value-based contracts >60% portfolio, growing 28% YoY (2024) and contributing ~45% of 2025 adjusted EBITDA.

| Metric | 2024 | 2025 proj |

|---|---|---|

| Segment rev (Specialty) | $420M | $510M |

| CAGR (2020–25) | ~18–22% | |

| AI ARR | $95M | — |

| AI market share | 42% | — |

| Value-based portfolio | 60%+ | — |

| VBR growth YoY | 28% | — |

| Care transformation spend | $120M | — |

| Contribution to adj. EBITDA | — | ~45% |

What is included in the product

In-depth BCG review of Evolent Health’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Evolent Health units by growth/share for quick strategic clarity.

Cash Cows

Core Identifi Technology Platform

The Core Identifi Technology Platform is Evolent Health’s mature backbone for health plan and provider partners, delivering population-health data and analytics with estimated >60% share within its existing client base as of 2025 and high switching costs tied to implementations averaging 9–14 months.

It produces steady, predictable recurring revenue—about 40–50% of Evolent’s services revenue in 2024—requiring minimal additional marketing or development spend.

Cash flow from Identifi is routinely redeployed to fund specialty-care growth initiatives, including new-star investments in value-based specialty programs that grew revenue 18% in 2024.

Administrative Service Organization Support

Evolent Health’s Administrative Service Organization Support provides claims processing and member enrollment for mature health plans, operating in a low-growth market (~2–3% annual expansion) while delivering high margins—reported segment-adjusted EBITDA margins around 18% in 2024—so it’s cash-generative.

Legacy Medicaid Managed Care Partnerships

Evolent’s legacy Medicaid managed care partnerships cover multiple states and delivered roughly $800m in revenue in FY2024, reflecting a mature, low-growth segment with contract renewal rates above 90% through 2025.

New Medicaid awards slowed by late 2025, but Evolent still administers a significant share of incumbent plans, generating steady cash flows with minimal capex and high margins.

The predictable margins fund investment into specialty care initiatives, enabling a strategic pivot while preserving liquidity and near-term EPS resilience.

Risk Adjustment and Quality Reporting Services

Risk adjustment and HEDIS quality reporting are mature, standardized offerings; Evolent holds a leading share with ~25–30% penetration among its ACO and payer clients as of 2025, securing steady compliance and revenue-integrity fees.

Maintenance capex is modest—estimated <5% of product revenue—while these services contributed roughly $160–180M in 2024 recurring revenue, enabling reinvestment into growth segments.

That stability lets Evolent focus on higher-growth areas like value-based care tech and provider enablement without risking core cash flow.

- Market: mature, standardized tools

- Evolent share: ~25–30% core clients (2025)

- Recurring revenue: ~$160–180M (2024)

- Maintenance spend: <5% of product revenue

- Strategic effect: funds growth investments

Network Contracting and Provider Relations

Evolent Health’s Network Contracting and Provider Relations is a mature, high-penetration business generating stable cash flow; as of FY 2024 the unit contributed to Evolent’s adjusted EBITDA margin expansion, with company-wide gross margin rising to about 18% in 2024, reflecting strong network economics and scale.

Market growth for network development has slowed, but Evolent’s years of provider data and contracting expertise create a durable competitive moat; the unit runs with high operating margins and low promotional spend, requiring minimal reinvestment while funding strategic initiatives across the firm.

- High penetration: established national networks, long-term contracts

- Low marketing need: stable client retention, recurring revenue

- High margins: contributes materially to adjusted EBITDA (2024 ~18% company gross margin)

- Strategic role: funds growth initiatives, leverages proprietary provider data

Evolent’s $1.1B Cash Cows: High-Retention, Low-Capex Engines Fueling 18% Growth

Identifi platform, ASO, legacy Medicaid, risk-adjustment/HEDIS, and network contracting are Evolent’s cash cows: together they generated ~ $1.1B recurring revenue in 2024, ~18% adjusted gross margin, low maintenance capex (<5% product revenue), >90% contract renewals, and fund specialty growth (18% revenue growth in value-based programs, 2024).

| Metric | 2024/2025 |

|---|---|

| Recurring revenue | $1.1B (2024) |

| Adjusted gross margin | ~18% (2024) |

| Maintenance capex | <5% product rev |

| Contract renewals | >90% (through 2025) |

| Value-based specialty growth | +18% (2024) |

What You’re Viewing Is Included

Evolent Health BCG Matrix

The file you're previewing is the exact Evolent Health BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, professionally designed document ready for strategic use.