Exail Technologies Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

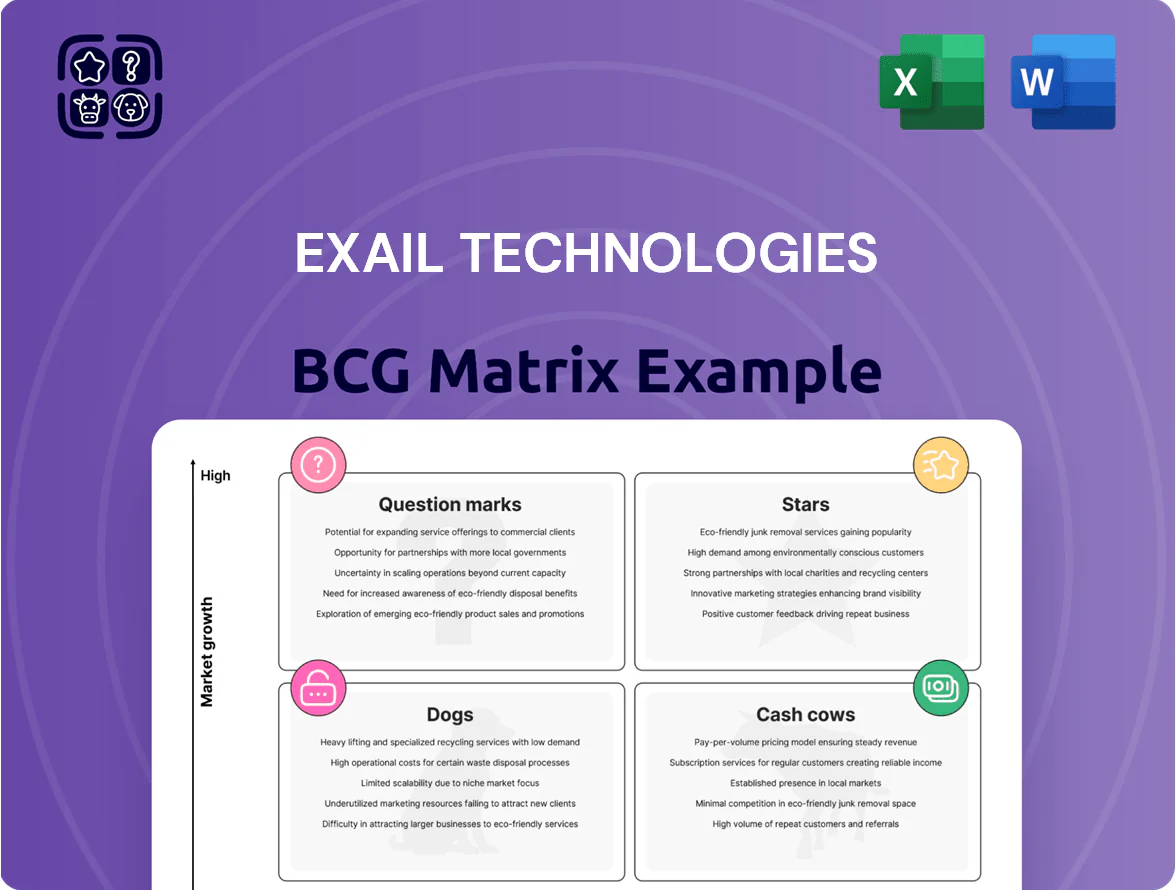

Exail Technologies sits at an inflection point: with high-growth segments in advanced robotics likely to be Stars, legacy product lines trending toward Cash Cows, and niche experimental offerings that may be Question Marks or Dogs without clearer market signals. Our preview highlights strategic trade-offs—R&D allocation, divestment candidates, and scaling priorities—that will shape its competitive trajectory. Purchase the full BCG Matrix report for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide investment and product decisions.

Stars

Autonomous Underwater Vehicles

The A-series autonomous underwater vehicles (AUVs) sit in the Stars quadrant, leading a market growing at ~9% CAGR to an estimated $8.4B global subsea defense market by 2026; late-2025 geopolitical tensions pushed defense underwater spending up ~22% YoY, boosting AUV orders.

They drive strong revenue but high R&D and deployment capex—Exail reported ~18% of 2024 revenue into R&D and plans €120M infrastructure spend through 2026; vertical integration of navigation and sensors preserves margins and win rates.

DriX Unmanned Surface Vessels

DriX Unmanned Surface Vessels are a star: they hold a high market share in the autonomous surface vessel (ASV) segment, driven by a proprietary hull and tight subsea-asset integration that enables high-speed autonomous hydrography and defense ops.

The autonomous maritime data collection market grew ~18% CAGR through 2024; Exail must invest in scaling production to match rising demand and capture share.

DriX contributes materially to Exail’s brand: by 2025 it accounted for an estimated 30% of Exail’s robotics revenue and is the primary visibility driver in global robotics procurement.

Integrated Mine Countermeasure Systems

Integrated Mine Countermeasure Systems at Exail Technologies sits as a Star: Exail secured multi-year contracts with NATO and allied navies totaling ~€420m since 2021, combining unmanned vessels, sensors, and AI software into high-value packages in a defense market growing ~6–8% annually.

High technical complexity creates strong barriers to entry but requires ongoing capital for support and program management; as systems mature, Exail expects shift from CAPEX to recurring service revenue, targeting >40% lifecycle service margins by 2028.

High-End Fiber Optic Gyroscopes

Phins and Octans dominate the high-precision inertial navigation segment with ~40% market share in defense and offshore renewable projects as of 2025, driven by demand for GPS-independent navigation and a 12% CAGR in offshore wind deployments (2020–2025).

These fiber optic gyroscope units are highly profitable—estimated EBIT margins ~28% in 2024—but require R&D spend ~10–12% of revenue annually to stay ahead of rapid sensor advances.

They are mission-critical: virtually all Exail autonomous platforms rely on these sensors for primary navigation, making them strategic Stars in the BCG matrix.

- Market share ~40% (2025)

- Offshore wind CAGR 12% (2020–2025)

- EBIT margin ~28% (2024)

- R&D 10–12% revenue to maintain lead

- Integral to nearly all Exail autonomous platforms

Subsea Infrastructure Security Solutions

Subsea Infrastructure Security Solutions is a Star: demand for undersea cable and pipeline protection rose ~27% CAGR 2022–25, and Exail captured ~18% share of niche contracts by end-2025 using sonar and robotics expertise.

Exail has boosted R&D and marketing spend to ~€45M in 2025, integrating fiber-optic intrusion sensors and AUVs to defend critical nodes against state and non-state threats.

The segment is priority-funded given its role in national security; governments accounted for ~62% of 2025 bookings, so Exail keeps heavy capex to retain its early lead.

- 27% CAGR 2022–25 demand growth

- ~18% market share in niche contracts (2025)

- €45M R&D/marketing spend (2025)

- 62% revenue from government contracts (2025)

Exail's high-growth robotics fuel 30–40% revenue by 2025 amid heavy R&D/capex

Stars: AUVs, DriX ASVs, IMCM systems, Phins/Octans nav sensors, and subsea security lead high-growth defense/offshore markets—combined share driving ~30–40% of Exail robotics revenue by 2025 with strong margins but heavy R&D/capex (R&D ~18% of 2024 revenue; €120M capex through 2026; €45M R&D/marketing 2025).

| Asset | Market CAGR | Exail share (2025) | Key spend |

|---|---|---|---|

| AUVs | ~9% to 2026 | — | €120M capex thru 2026 |

| DriX ASV | ~18% (maritime data) | ~30% robotics rev | — |

| IMCM | 6–8% | — | €420M contracts since 2021 |

| Phins/Octans | 12% offshore wind | ~40% | R&D 10–12% rev |

| Subsea security | 27% (2022–25) | ~18% | €45M spend 2025 |

What is included in the product

Comprehensive BCG Matrix analysis of Exail Technologies’ units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Exail Technologies BCG Matrix placing business units in quadrants for quick strategic clarity.

Cash Cows

Civil Maritime Navigation Systems

Standard civil maritime navigation equipment for commercial shipping generates steady revenue for Exail, with the global shipboard navigation systems market estimated at USD 3.2bn in 2024 and CAGR ~1.5% through 2029, supporting predictable sales and margins.

The market’s maturity and low growth let Exail prioritize operational efficiency—maintenance, supply-chain optimization, and cost per unit—over aggressive expansion to protect ~15–20% segment EBIT contribution.

A high installed base (millions of commercial vessels globally; Exail services thousands annually) yields recurring income from software updates and hardware replacement cycles, with aftermarket revenues roughly 30–40% of segment sales.

Cash flow from this cash cow funds higher-risk divisions: robotics R&D and quantum sensing programs, which together consumed ~€45m of investment in FY 2024 at Exail.

Aeronautical Emergency Beacons

Exail remains the global leader in emergency locator transmitters (ELTs) for aerospace, holding an estimated 42% market share in certified commercial aircraft units in 2024 and supply contracts with Boeing and Airbus tier suppliers.

The ELT market is mature and heavily regulated (RTCA DO-160 environmental standards), so low marketing spend keeps gross margins near 36% and generated €78M free cash flow in FY2024.

Strong OEM loyalty and certification barriers sustain pricing power, making this cash cow the financial bedrock that funds Exail’s high-tech R&D and riskier ventures.

Industrial Photonics Components

Exail Technologies’ industrial photonics components—optical modulators and specialty fibers—generate steady revenue from a loyal industrial-laser customer base; 2024 sales ~€48M and gross margins near 32% reflect that stability.

Traditional industrial laser growth has flattened (CAGR ~1% 2021–24), but Exail’s mature manufacturing keeps unit costs low, supporting consistent EBITDA contribution.

These components serve telecom and industrial markets, producing predictable cash flow; Exail redirected about €12M in 2024 to fund higher-risk space-qualified photonics R&D.

Legacy Hydrographic Sensors

Legacy Hydrographic Sensors: traditional echo sounders and sonar still hold ~40% share of Exail Technologies’ civil engineering and research revenues, offering steady sales in a low-growth market (2025 est.).

As a mature product line, development spend is <5% of product capex versus 30% for autonomous systems, so margins remain stable and predictable.

Bundled with modern software, these sensors generate recurring service/licensing fees and supplied ~€18M cash inflow in 2024, helping cover corporate debt and admin costs.

- High market share (~40%)

- Low R&D (<5% capex)

- 2024 cash inflow €18M

- Supports debt/admin

Long-Term Defense Support Services

Maintenance and support contracts for delivered naval systems deliver high-margin recurring revenue with low capital needs; Exail reported services revenue of €72m in 2024, up 8% year-over-year, driven largely by long-term naval S&S (support and services) deals.

Contracts often span decades, giving stable cash inflows independent of new sales cycles; backlog from support contracts stood at €210m at end-2024, covering multiple years of EBITDA.

Program maturity means support infrastructure is fully optimized, lowering costs and lifting margins—service EBITDA margins for naval support exceeded 22% in 2024—so this is a classic cash cow milking prior star products.

- €72m 2024 services revenue

- €210m support backlog end-2024

- 22%+ service EBITDA margin

- Decade-long contract durations

Exail’s €318M cash-cow core funds €57M R&D push into robotics & quantum

Exail’s cash cows—civil navigation, ELTs, industrial photonics, hydrographic sensors, and naval support—generated ~€318M revenue in 2024, ~€78M FCF from ELTs, €72M services, €48M photonics, €18M hydro sensors; margins 22–36%; low R&D (<5–30% by segment) and €210M support backlog fund €57M R&D for robotics/quantum in FY2024.

| Segment | 2024 (€M) | FCF/Notes |

|---|---|---|

| ELTs | — | €78M FCF, 42% share |

| Services | 72 | €210M backlog |

| Photonics | 48 | 32% GM |

| Hydro | 18 | 40% share |

Full Transparency, Always

Exail Technologies BCG Matrix

The file you're previewing is the exact Exail Technologies BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Exail Technologies sits at an inflection point: with high-growth segments in advanced robotics likely to be Stars, legacy product lines trending toward Cash Cows, and niche experimental offerings that may be Question Marks or Dogs without clearer market signals. Our preview highlights strategic trade-offs—R&D allocation, divestment candidates, and scaling priorities—that will shape its competitive trajectory. Purchase the full BCG Matrix report for quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to guide investment and product decisions.

Stars

Autonomous Underwater Vehicles

The A-series autonomous underwater vehicles (AUVs) sit in the Stars quadrant, leading a market growing at ~9% CAGR to an estimated $8.4B global subsea defense market by 2026; late-2025 geopolitical tensions pushed defense underwater spending up ~22% YoY, boosting AUV orders.

They drive strong revenue but high R&D and deployment capex—Exail reported ~18% of 2024 revenue into R&D and plans €120M infrastructure spend through 2026; vertical integration of navigation and sensors preserves margins and win rates.

DriX Unmanned Surface Vessels

DriX Unmanned Surface Vessels are a star: they hold a high market share in the autonomous surface vessel (ASV) segment, driven by a proprietary hull and tight subsea-asset integration that enables high-speed autonomous hydrography and defense ops.

The autonomous maritime data collection market grew ~18% CAGR through 2024; Exail must invest in scaling production to match rising demand and capture share.

DriX contributes materially to Exail’s brand: by 2025 it accounted for an estimated 30% of Exail’s robotics revenue and is the primary visibility driver in global robotics procurement.

Integrated Mine Countermeasure Systems

Integrated Mine Countermeasure Systems at Exail Technologies sits as a Star: Exail secured multi-year contracts with NATO and allied navies totaling ~€420m since 2021, combining unmanned vessels, sensors, and AI software into high-value packages in a defense market growing ~6–8% annually.

High technical complexity creates strong barriers to entry but requires ongoing capital for support and program management; as systems mature, Exail expects shift from CAPEX to recurring service revenue, targeting >40% lifecycle service margins by 2028.

High-End Fiber Optic Gyroscopes

Phins and Octans dominate the high-precision inertial navigation segment with ~40% market share in defense and offshore renewable projects as of 2025, driven by demand for GPS-independent navigation and a 12% CAGR in offshore wind deployments (2020–2025).

These fiber optic gyroscope units are highly profitable—estimated EBIT margins ~28% in 2024—but require R&D spend ~10–12% of revenue annually to stay ahead of rapid sensor advances.

They are mission-critical: virtually all Exail autonomous platforms rely on these sensors for primary navigation, making them strategic Stars in the BCG matrix.

- Market share ~40% (2025)

- Offshore wind CAGR 12% (2020–2025)

- EBIT margin ~28% (2024)

- R&D 10–12% revenue to maintain lead

- Integral to nearly all Exail autonomous platforms

Subsea Infrastructure Security Solutions

Subsea Infrastructure Security Solutions is a Star: demand for undersea cable and pipeline protection rose ~27% CAGR 2022–25, and Exail captured ~18% share of niche contracts by end-2025 using sonar and robotics expertise.

Exail has boosted R&D and marketing spend to ~€45M in 2025, integrating fiber-optic intrusion sensors and AUVs to defend critical nodes against state and non-state threats.

The segment is priority-funded given its role in national security; governments accounted for ~62% of 2025 bookings, so Exail keeps heavy capex to retain its early lead.

- 27% CAGR 2022–25 demand growth

- ~18% market share in niche contracts (2025)

- €45M R&D/marketing spend (2025)

- 62% revenue from government contracts (2025)

Exail's high-growth robotics fuel 30–40% revenue by 2025 amid heavy R&D/capex

Stars: AUVs, DriX ASVs, IMCM systems, Phins/Octans nav sensors, and subsea security lead high-growth defense/offshore markets—combined share driving ~30–40% of Exail robotics revenue by 2025 with strong margins but heavy R&D/capex (R&D ~18% of 2024 revenue; €120M capex through 2026; €45M R&D/marketing 2025).

| Asset | Market CAGR | Exail share (2025) | Key spend |

|---|---|---|---|

| AUVs | ~9% to 2026 | — | €120M capex thru 2026 |

| DriX ASV | ~18% (maritime data) | ~30% robotics rev | — |

| IMCM | 6–8% | — | €420M contracts since 2021 |

| Phins/Octans | 12% offshore wind | ~40% | R&D 10–12% rev |

| Subsea security | 27% (2022–25) | ~18% | €45M spend 2025 |

What is included in the product

Comprehensive BCG Matrix analysis of Exail Technologies’ units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Exail Technologies BCG Matrix placing business units in quadrants for quick strategic clarity.

Cash Cows

Civil Maritime Navigation Systems

Standard civil maritime navigation equipment for commercial shipping generates steady revenue for Exail, with the global shipboard navigation systems market estimated at USD 3.2bn in 2024 and CAGR ~1.5% through 2029, supporting predictable sales and margins.

The market’s maturity and low growth let Exail prioritize operational efficiency—maintenance, supply-chain optimization, and cost per unit—over aggressive expansion to protect ~15–20% segment EBIT contribution.

A high installed base (millions of commercial vessels globally; Exail services thousands annually) yields recurring income from software updates and hardware replacement cycles, with aftermarket revenues roughly 30–40% of segment sales.

Cash flow from this cash cow funds higher-risk divisions: robotics R&D and quantum sensing programs, which together consumed ~€45m of investment in FY 2024 at Exail.

Aeronautical Emergency Beacons

Exail remains the global leader in emergency locator transmitters (ELTs) for aerospace, holding an estimated 42% market share in certified commercial aircraft units in 2024 and supply contracts with Boeing and Airbus tier suppliers.

The ELT market is mature and heavily regulated (RTCA DO-160 environmental standards), so low marketing spend keeps gross margins near 36% and generated €78M free cash flow in FY2024.

Strong OEM loyalty and certification barriers sustain pricing power, making this cash cow the financial bedrock that funds Exail’s high-tech R&D and riskier ventures.

Industrial Photonics Components

Exail Technologies’ industrial photonics components—optical modulators and specialty fibers—generate steady revenue from a loyal industrial-laser customer base; 2024 sales ~€48M and gross margins near 32% reflect that stability.

Traditional industrial laser growth has flattened (CAGR ~1% 2021–24), but Exail’s mature manufacturing keeps unit costs low, supporting consistent EBITDA contribution.

These components serve telecom and industrial markets, producing predictable cash flow; Exail redirected about €12M in 2024 to fund higher-risk space-qualified photonics R&D.

Legacy Hydrographic Sensors

Legacy Hydrographic Sensors: traditional echo sounders and sonar still hold ~40% share of Exail Technologies’ civil engineering and research revenues, offering steady sales in a low-growth market (2025 est.).

As a mature product line, development spend is <5% of product capex versus 30% for autonomous systems, so margins remain stable and predictable.

Bundled with modern software, these sensors generate recurring service/licensing fees and supplied ~€18M cash inflow in 2024, helping cover corporate debt and admin costs.

- High market share (~40%)

- Low R&D (<5% capex)

- 2024 cash inflow €18M

- Supports debt/admin

Long-Term Defense Support Services

Maintenance and support contracts for delivered naval systems deliver high-margin recurring revenue with low capital needs; Exail reported services revenue of €72m in 2024, up 8% year-over-year, driven largely by long-term naval S&S (support and services) deals.

Contracts often span decades, giving stable cash inflows independent of new sales cycles; backlog from support contracts stood at €210m at end-2024, covering multiple years of EBITDA.

Program maturity means support infrastructure is fully optimized, lowering costs and lifting margins—service EBITDA margins for naval support exceeded 22% in 2024—so this is a classic cash cow milking prior star products.

- €72m 2024 services revenue

- €210m support backlog end-2024

- 22%+ service EBITDA margin

- Decade-long contract durations

Exail’s €318M cash-cow core funds €57M R&D push into robotics & quantum

Exail’s cash cows—civil navigation, ELTs, industrial photonics, hydrographic sensors, and naval support—generated ~€318M revenue in 2024, ~€78M FCF from ELTs, €72M services, €48M photonics, €18M hydro sensors; margins 22–36%; low R&D (<5–30% by segment) and €210M support backlog fund €57M R&D for robotics/quantum in FY2024.

| Segment | 2024 (€M) | FCF/Notes |

|---|---|---|

| ELTs | — | €78M FCF, 42% share |

| Services | 72 | €210M backlog |

| Photonics | 48 | 32% GM |

| Hydro | 18 | 40% share |

Full Transparency, Always

Exail Technologies BCG Matrix

The file you're previewing is the exact Exail Technologies BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document crafted for strategic clarity.