Expedia Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

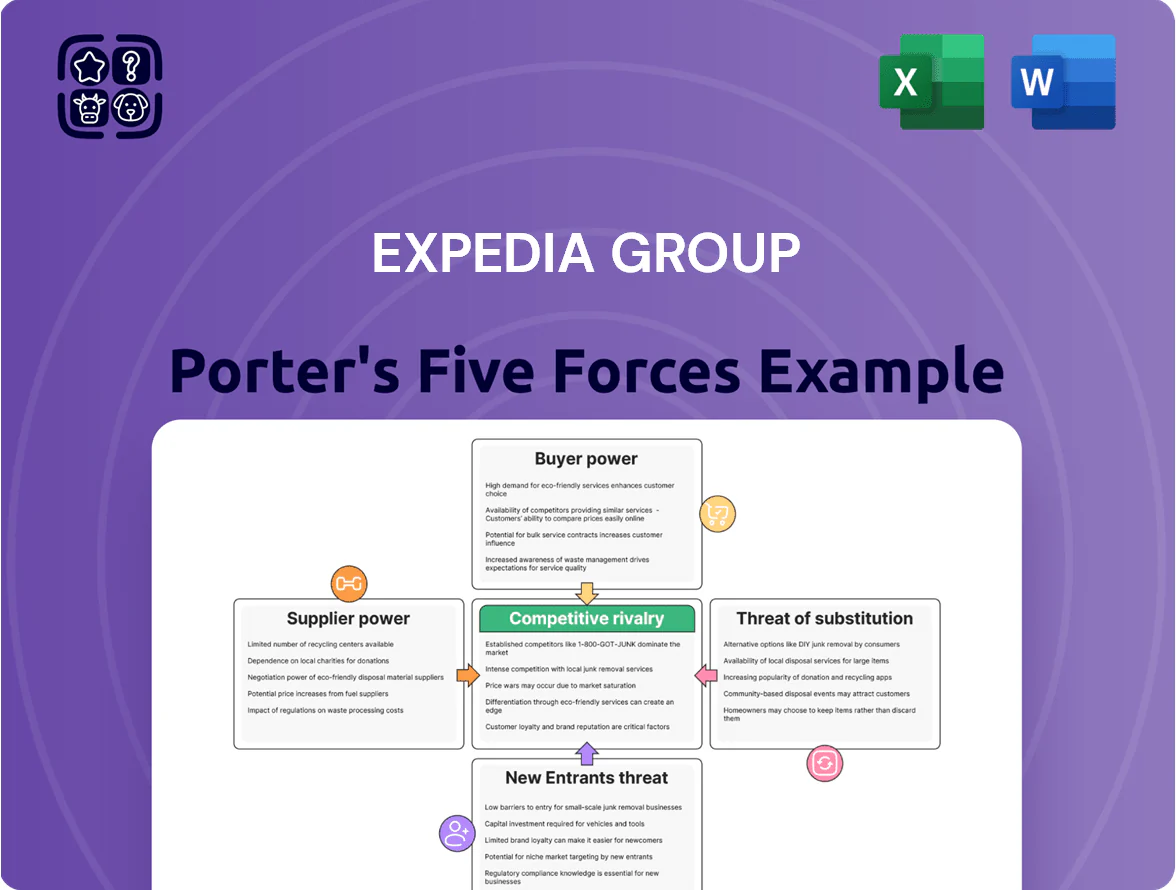

Expedia Group faces intense platform rivalry, significant buyer power, and complex supplier dynamics that shape pricing and margin pressure across travel distribution; network effects and tech scale are critical defensive assets. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Expedia Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Airline Carriers

The airline market is concentrated: the top 10 global carriers held about 40% of revenue passenger km in 2024, giving them leverage over platforms like Expedia Group. Major airlines can set commission fees or limit API access, pushing customers to direct channels and squeezing OTA margins—Expedia reported air revenues fell 6% in FY2024 vs FY2019 mix pressures. Expedia must keep tight airline ties to offer complete flight choice and avoid user churn.

Fragmentation of Independent Hotel Properties

The accommodation sector stayed highly fragmented in 2024, with over 70% of global rooms outside major chains, which lowers bargaining power of individual boutique or independent hotels.

These smaller suppliers depend on Expedia Group’s global reach—Expedia reported 90+ million room nights booked in 2024—so independents trade higher commissions for distribution and demand management.

As a result, Expedia can often secure commission rates above market averages from independents; industry reports in 2024 show OTAs charged independents 15–25% vs 10–15% for major chains.

Direct Booking Strategies and Loyalty Programs

Major hotel chains and car rental firms pushed direct-booking: Marriott, Hilton, and Enterprise reported 8–12% higher direct web bookings in 2024 after rolling out exclusive member rates and points, reclaiming customers from Expedia Group.

Suppliers aim to cut commissions—hotel group margins rose ~1.5 percentage points in 2024 after loyalty-driven direct bookings—reducing Expedia’s bargaining power.

Expedia must prove value via better UX and bundles; in 2024 Expedia’s advertising and marketing spend was $3.1B, signaling investment to retain distribution and counter supplier defection.

Technological Control and Dynamic Pricing

Suppliers now use advanced revenue management systems to adjust inventory and prices in real time across channels, letting hotels pull listings from Expedia or hike rates within minutes when direct demand rises.

This technical agility boosted supplier margins: a 2024 STR report found 45% of branded hotels used dynamic pricing engines, and Expedia disclosed in Q4 2024 that direct-booking rates grew 6%, pressuring OTA commission leverage.

- Real-time inventory control reduces Expedia’s share of customer bookings

- 45% of branded hotels using dynamic pricing (STR, 2024)

- Expedia saw 6% direct-booking rate growth in Q4 2024

- Suppliers can delist quickly, raising price bargaining power

Dependence on Global Distribution Systems

Expedia depends on third-party Global Distribution Systems (GDS) for real-time booking data from thousands of hotels and airlines; in 2024 Expedia processed millions of GDS-driven bookings, linking directly to supplier inventories.

GDSs add a cost layer and can bottleneck flows—if GDS fees rise 5–15% or if a provider changes APIs, Expedia’s gross margin and time-to-market for supplier inventory suffer.

Shifts in GDS tech or pricing can raise operating costs and reduce connectivity; Expedia hedges by direct integrations with large chains but still relies heavily on Amadeus, Sabre, and Travelport for breadth.

- Millions of bookings rely on GDS in 2024

- Fee increases of 5–15% hit margins

- Direct integrations mitigate but don’t remove risk

- Key vendors: Amadeus, Sabre, Travelport

Supplier Power Shifts: Airlines Concentrated, Hotels Fragmented—Pressure on Expedia Margins

Suppliers mix: airlines concentrated (top 10 = ~40% RPK, 2024) and exert high leverage; hotels fragmented (70% rooms outside chains), so independents accept higher OTA commissions (15–25% vs 10–15% for chains). GDSs (Amadeus, Sabre, Travelport) and dynamic-pricing adoption (45% branded hotels, STR 2024) give suppliers real-time control, raising delisting risk and pressuring Expedia margins; Expedia spent $3.1B on marketing in 2024 to defend distribution.

| Metric | 2024 |

|---|---|

| Top-10 airlines RPK share | ~40% |

| Rooms outside major chains | ~70% |

| Indie hotel OTA commission | 15–25% |

| Branded hotels using dynamic pricing | 45% |

| Expedia marketing spend | $3.1B |

What is included in the product

Concise Porter's Five Forces assessment of Expedia Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and disruptive threats shaping its pricing power and strategic resilience.

A concise Porter's Five Forces one-sheet for Expedia Group—quickly highlights competitive pressures and relieves strategic decision pain by surfacing threats from OTAs, suppliers, substitutes, entrants, and buyer bargaining power.

Customers Bargaining Power

Low Switching Costs for Travelers

Low switching costs mean consumers can move from Expedia Group to Booking Holdings or direct suppliers for almost no fee; 2024 data show metasearch referrals lifted Booking.com's share, and OTA churn rose as price-comparison browsers increased 12% year-over-year.

High Price Transparency and Comparison Tools

The rise of metasearch engines and price-comparison browser extensions lets customers scan dozens of OTAs in seconds; Skyscanner and Google Flights reported 2024 search growth of ~12% YoY, increasing cross-platform price checks and pushing Expedia Group to match lowest fares. This transparency compresses Expedia’s margin: online travel agency gross margins fell ~150 basis points industry-wide in 2023–24, so buyers can demand the best market value each booking.

Influence of User-Generated Content and Reviews

Modern travelers lean on reviews and social proof, giving them collective power over Expedia Group’s reputation; 93% of travelers in a 2024 Phocuswright survey said reviews influence bookings, so negative sentiment can cut conversion rates sharply.

Consolidated Loyalty Programs and Rewards

Expedia launched One Key in 2023 to unite Expedia, Hotels.com, and Vrbo rewards, boosting repeat bookings by offering shared points and member-only pricing; by Q4 2024 loyalty members drove ~38% of gross bookings, helping reduce CAC per booking.

Shared rewards raise switching costs and increase lifetime value, but major rivals—Booking Holdings and Airbnb—operate comparable programs, so customers still pick the most lucrative ecosystem based on price and benefit.

- One Key launched 2023

- Loyalty ~38% of gross bookings (Q4 2024)

- Rewards earn/spend across three brands

- Rivals offer similar programs

Mobile-First Booking Behavior

Mobile-first booking lets customers book instantly; in 2024 mobile accounted for ~58% of Expedia Group gross bookings, so users can shift to rivals with one tap if performance lags.

Expedia must sustain sub-second load times and top-tier UX across iOS/Android; App Store 4.5+ ratings and crash rates below 1% correlate with higher retention and revenue.

- 58% mobile gross bookings (2024)

- Target: <1s load, crash rate <1%

- High app ratings drive repeat purchases

Rising metasearch & mobile power squeeze OTAs—loyalty helps but rivals neutralize gains

Customers hold moderate-to-high bargaining power: low switching costs and metasearch transparency (Google Flights/Skyscanner +12% searches YoY, 2024) compress OTA margins (~150 bps drop 2023–24) while reviews drive conversion (93% influence, Phocuswright 2024); loyalty (One Key launched 2023) raised repeat share to ~38% of gross bookings (Q4 2024) but rivals match rewards, and mobile (58% bookings, 2024) enables instant switching.

| Metric | Value |

|---|---|

| Metasearch search growth (2024) | ~12% YoY |

| OTA margin compression | ~150 bps (2023–24) |

| Review influence | 93% (Phocuswright 2024) |

| One Key loyalty share | ~38% gross bookings (Q4 2024) |

| Mobile share | ~58% gross bookings (2024) |

Preview the Actual Deliverable

Expedia Group Porter's Five Forces Analysis

This preview shows the exact Expedia Group Porter's Five Forces analysis you'll receive upon purchase—complete, professionally formatted, and ready for immediate download with no placeholders.

The document displayed here is the full, final version of the analysis, so once you buy you'll have instant access to this same file for use in strategy, valuation, or competitive assessment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Expedia Group faces intense platform rivalry, significant buyer power, and complex supplier dynamics that shape pricing and margin pressure across travel distribution; network effects and tech scale are critical defensive assets. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Expedia Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Airline Carriers

The airline market is concentrated: the top 10 global carriers held about 40% of revenue passenger km in 2024, giving them leverage over platforms like Expedia Group. Major airlines can set commission fees or limit API access, pushing customers to direct channels and squeezing OTA margins—Expedia reported air revenues fell 6% in FY2024 vs FY2019 mix pressures. Expedia must keep tight airline ties to offer complete flight choice and avoid user churn.

Fragmentation of Independent Hotel Properties

The accommodation sector stayed highly fragmented in 2024, with over 70% of global rooms outside major chains, which lowers bargaining power of individual boutique or independent hotels.

These smaller suppliers depend on Expedia Group’s global reach—Expedia reported 90+ million room nights booked in 2024—so independents trade higher commissions for distribution and demand management.

As a result, Expedia can often secure commission rates above market averages from independents; industry reports in 2024 show OTAs charged independents 15–25% vs 10–15% for major chains.

Direct Booking Strategies and Loyalty Programs

Major hotel chains and car rental firms pushed direct-booking: Marriott, Hilton, and Enterprise reported 8–12% higher direct web bookings in 2024 after rolling out exclusive member rates and points, reclaiming customers from Expedia Group.

Suppliers aim to cut commissions—hotel group margins rose ~1.5 percentage points in 2024 after loyalty-driven direct bookings—reducing Expedia’s bargaining power.

Expedia must prove value via better UX and bundles; in 2024 Expedia’s advertising and marketing spend was $3.1B, signaling investment to retain distribution and counter supplier defection.

Technological Control and Dynamic Pricing

Suppliers now use advanced revenue management systems to adjust inventory and prices in real time across channels, letting hotels pull listings from Expedia or hike rates within minutes when direct demand rises.

This technical agility boosted supplier margins: a 2024 STR report found 45% of branded hotels used dynamic pricing engines, and Expedia disclosed in Q4 2024 that direct-booking rates grew 6%, pressuring OTA commission leverage.

- Real-time inventory control reduces Expedia’s share of customer bookings

- 45% of branded hotels using dynamic pricing (STR, 2024)

- Expedia saw 6% direct-booking rate growth in Q4 2024

- Suppliers can delist quickly, raising price bargaining power

Dependence on Global Distribution Systems

Expedia depends on third-party Global Distribution Systems (GDS) for real-time booking data from thousands of hotels and airlines; in 2024 Expedia processed millions of GDS-driven bookings, linking directly to supplier inventories.

GDSs add a cost layer and can bottleneck flows—if GDS fees rise 5–15% or if a provider changes APIs, Expedia’s gross margin and time-to-market for supplier inventory suffer.

Shifts in GDS tech or pricing can raise operating costs and reduce connectivity; Expedia hedges by direct integrations with large chains but still relies heavily on Amadeus, Sabre, and Travelport for breadth.

- Millions of bookings rely on GDS in 2024

- Fee increases of 5–15% hit margins

- Direct integrations mitigate but don’t remove risk

- Key vendors: Amadeus, Sabre, Travelport

Supplier Power Shifts: Airlines Concentrated, Hotels Fragmented—Pressure on Expedia Margins

Suppliers mix: airlines concentrated (top 10 = ~40% RPK, 2024) and exert high leverage; hotels fragmented (70% rooms outside chains), so independents accept higher OTA commissions (15–25% vs 10–15% for chains). GDSs (Amadeus, Sabre, Travelport) and dynamic-pricing adoption (45% branded hotels, STR 2024) give suppliers real-time control, raising delisting risk and pressuring Expedia margins; Expedia spent $3.1B on marketing in 2024 to defend distribution.

| Metric | 2024 |

|---|---|

| Top-10 airlines RPK share | ~40% |

| Rooms outside major chains | ~70% |

| Indie hotel OTA commission | 15–25% |

| Branded hotels using dynamic pricing | 45% |

| Expedia marketing spend | $3.1B |

What is included in the product

Concise Porter's Five Forces assessment of Expedia Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitutes, and disruptive threats shaping its pricing power and strategic resilience.

A concise Porter's Five Forces one-sheet for Expedia Group—quickly highlights competitive pressures and relieves strategic decision pain by surfacing threats from OTAs, suppliers, substitutes, entrants, and buyer bargaining power.

Customers Bargaining Power

Low Switching Costs for Travelers

Low switching costs mean consumers can move from Expedia Group to Booking Holdings or direct suppliers for almost no fee; 2024 data show metasearch referrals lifted Booking.com's share, and OTA churn rose as price-comparison browsers increased 12% year-over-year.

High Price Transparency and Comparison Tools

The rise of metasearch engines and price-comparison browser extensions lets customers scan dozens of OTAs in seconds; Skyscanner and Google Flights reported 2024 search growth of ~12% YoY, increasing cross-platform price checks and pushing Expedia Group to match lowest fares. This transparency compresses Expedia’s margin: online travel agency gross margins fell ~150 basis points industry-wide in 2023–24, so buyers can demand the best market value each booking.

Influence of User-Generated Content and Reviews

Modern travelers lean on reviews and social proof, giving them collective power over Expedia Group’s reputation; 93% of travelers in a 2024 Phocuswright survey said reviews influence bookings, so negative sentiment can cut conversion rates sharply.

Consolidated Loyalty Programs and Rewards

Expedia launched One Key in 2023 to unite Expedia, Hotels.com, and Vrbo rewards, boosting repeat bookings by offering shared points and member-only pricing; by Q4 2024 loyalty members drove ~38% of gross bookings, helping reduce CAC per booking.

Shared rewards raise switching costs and increase lifetime value, but major rivals—Booking Holdings and Airbnb—operate comparable programs, so customers still pick the most lucrative ecosystem based on price and benefit.

- One Key launched 2023

- Loyalty ~38% of gross bookings (Q4 2024)

- Rewards earn/spend across three brands

- Rivals offer similar programs

Mobile-First Booking Behavior

Mobile-first booking lets customers book instantly; in 2024 mobile accounted for ~58% of Expedia Group gross bookings, so users can shift to rivals with one tap if performance lags.

Expedia must sustain sub-second load times and top-tier UX across iOS/Android; App Store 4.5+ ratings and crash rates below 1% correlate with higher retention and revenue.

- 58% mobile gross bookings (2024)

- Target: <1s load, crash rate <1%

- High app ratings drive repeat purchases

Rising metasearch & mobile power squeeze OTAs—loyalty helps but rivals neutralize gains

Customers hold moderate-to-high bargaining power: low switching costs and metasearch transparency (Google Flights/Skyscanner +12% searches YoY, 2024) compress OTA margins (~150 bps drop 2023–24) while reviews drive conversion (93% influence, Phocuswright 2024); loyalty (One Key launched 2023) raised repeat share to ~38% of gross bookings (Q4 2024) but rivals match rewards, and mobile (58% bookings, 2024) enables instant switching.

| Metric | Value |

|---|---|

| Metasearch search growth (2024) | ~12% YoY |

| OTA margin compression | ~150 bps (2023–24) |

| Review influence | 93% (Phocuswright 2024) |

| One Key loyalty share | ~38% gross bookings (Q4 2024) |

| Mobile share | ~58% gross bookings (2024) |

Preview the Actual Deliverable

Expedia Group Porter's Five Forces Analysis

This preview shows the exact Expedia Group Porter's Five Forces analysis you'll receive upon purchase—complete, professionally formatted, and ready for immediate download with no placeholders.

The document displayed here is the full, final version of the analysis, so once you buy you'll have instant access to this same file for use in strategy, valuation, or competitive assessment.