Expedia Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Delve into how political, economic, and technological forces are reshaping Expedia Group's prospects with our concise PESTLE snapshot—designed to inform investors and strategists fast.

Buy the full PESTLE analysis to access a complete, actionable breakdown of risks and opportunities, ready for boardrooms, pitches, or investment models.

Political factors

Geopolitical instability and travel restrictions

Ongoing conflicts in Eastern Europe and the Middle East have rerouted flights and heightened safety concerns, contributing to regional booking drops—e.g., Europe-Middle East bookings fell ~12% YoY in Q3 2025 on major OTAs. Governments’ frequent travel-advisories can trigger sudden corridor-specific revenue declines; Expedia Group reported a 9% revenue sensitivity in international leisure bookings to alerts in 2024. Expedia must rapidly reallocate marketing and inventory toward stable markets to mitigate these shocks.

Short-term rental regulations

Major metros have tightened short-term rental rules to ease housing shortages and density; New York, San Francisco and Barcelona cut available listings by up to 20–30% in 2023–2024, pressuring supply for Vrbo.

Common measures include strict licensing and 30–90 day annual caps, directly reducing Vrbo host revenue and contributing to a reported 6% year-over-year dip in US short-term supply on marketplace platforms in 2024.

Expedia must manage a fragmented legal patchwork across 100+ jurisdictions, investing compliance costs estimated in 2024 at tens of millions annually to keep hosts compliant while stabilizing inventory levels.

International trade and tax policies

Implementation of the OECD/G20 global minimum tax (15%) and proliferation of digital services taxes in 20+ jurisdictions affect Expedia Group’s reported international earnings and effective tax rate; Expedia cited a 2024 tax rate impact in its filings, with non-U.S. taxes contributing to its 2024 effective tax rate of around 18–20% (company disclosure). Shifts in U.S.-EU and U.S.-China trade relations can raise cross-border transaction costs and regulatory friction for Expedia’s payments and supplier contracts. Adapting corporate structure and transfer-pricing policies to evolving tax treaties and BEPS-related rules remains a material compliance and planning challenge for Expedia’s international operations.

Government tourism promotion initiatives

Many governments boosted tourism budgets post-pandemic—EU member states increased funding by an estimated 12% in 2024—enabling public-private campaigns that Expedia co-funds to promote destinations and absorb promotional costs.

Expedia leverages these subsidies to drive platform traffic; co-marketing has lifted partner ADRs by up to 8% and contributed to a 2024 YoY room-night growth of ~6% across its brands.

These alliances help Expedia smooth demand seasonality and allocate inventory globally, supporting revenue diversification and higher take-rates in emerging markets.

- Governments ↑ tourism spend (~12% EU, 2024)

- Co-marketing boosts ADR ≈8% for partners

- Platform room-night growth ~6% YoY (2024)

- Improves demand smoothing and revenue diversification

Visa processing and border security

- US visa waits >200 days (selected consulates, 2023)

- China inbound passenger variance ~30% post-2022 reopening

- Long-haul bookings ≈40% of OTA revenue share (2023)

- Expedia operates policy feeds and real-time customer alerts

Political risk slashes travel demand: Europe -12%, US supply -6%, ADR +8%

Political risks (conflict, regulation, tax, visas) drive demand swings and costs: Q3 2025 Europe-ME bookings -12% YoY; US short-term supply -6% YoY (2024); Expedia 2024 effective tax ~18–20%; co-marketing lifted ADR ~8% and room-nights +6% YoY; US visa waits >200 days (2023); China inbound variance ~30% post-reopening.

| Metric | Value |

|---|---|

| Europe-ME bookings | -12% Q3 2025 |

| US STR supply | -6% 2024 |

| Expedia tax rate | 18–20% 2024 |

| ADR lift (co-marketing) | +8% |

| Room-nights | +6% YoY 2024 |

What is included in the product

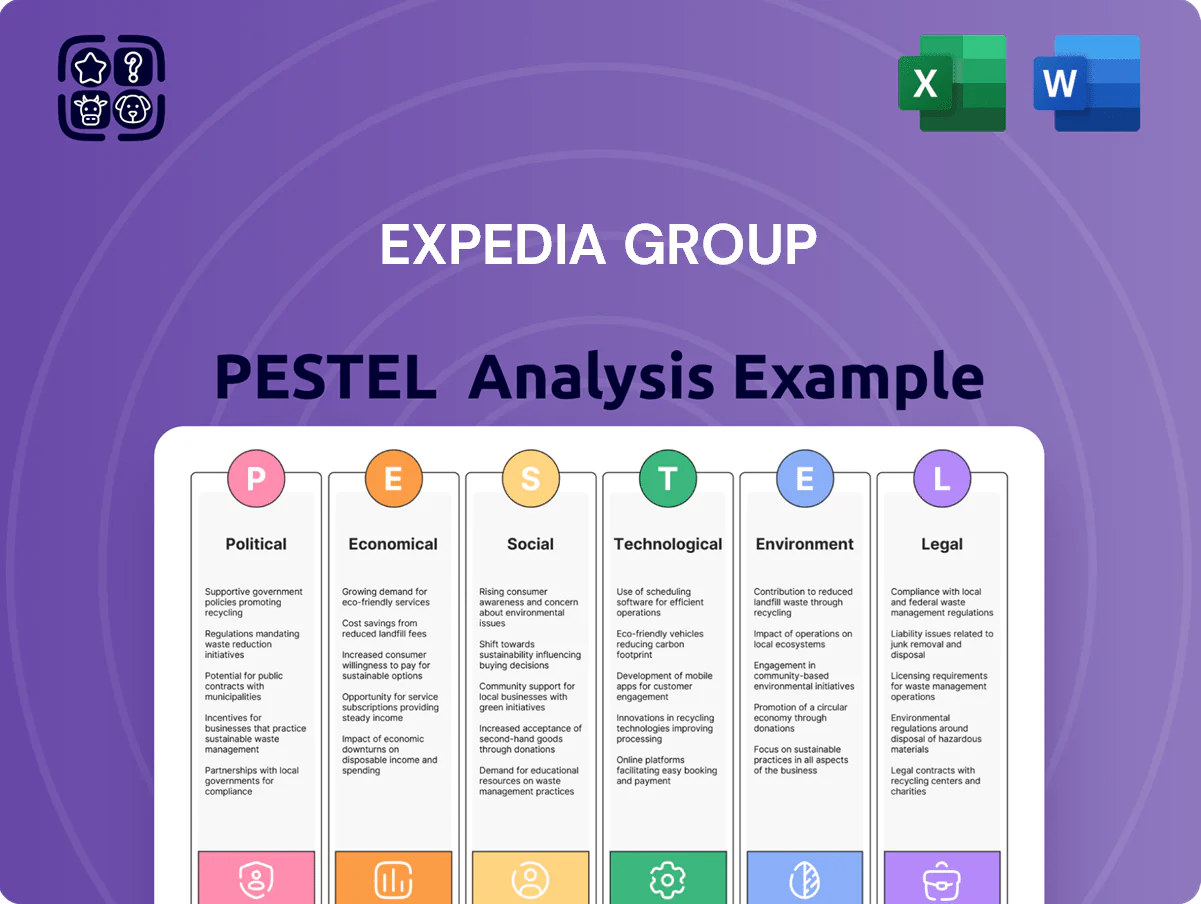

Explores how external macro-environmental factors uniquely affect Expedia Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented Expedia Group PESTLE summary for quick reference in meetings, easily editable for regional or business-line notes and drop-in ready for presentations or strategy packs.

Economic factors

Global inflation and consumer spending

Persistent inflation through 2025 trimmed global real disposable income, with OECD CPI averaging about 4.8% YTD and US core CPI ~3.9%, pushing travelers toward budget options; Expedia’s value brands and One Key loyalty — reported to drive ~20% higher repeat bookings — are central to retaining price-sensitive customers. The group must offset competitive pricing with rising FY25 operating cost pressures, including wage inflation and higher processing fees, to defend margins.

Currency exchange rate volatility

Significant fluctuations in the U.S. dollar—which strengthened ~8% vs. the euro and weakened ~3% vs. the yen in 2024—affect international travelers’ purchasing power and demand on Expedia Group platforms.

As a U.S.-based company with ~70% of gross bookings originating outside North America, Expedia faces material foreign exchange translation risk that can swing reported revenue quarter-to-quarter.

Expedia reported using derivatives and localized pricing, reducing FX sensitivity; by FY2024 management noted hedges and currency-adjusted revenue metrics lowered reported volatility by an estimated mid-single digits percent.

Interest rate impacts on capital

Higher interest rates—U.S. fed funds averaging ~4.9% in 2024 vs ~1.4% 2010–2019—have raised Expedia Group's cost of debt, increasing interest expense (FY2024 interest expense ~$290m) and making acquisitions pricier.

Management emphasizes a strong balance sheet and disciplined capex; Expedia ended 2024 with ~$3.1bn cash and equivalents and reduced net leverage versus prior year to preserve liquidity.

Investors watch free cash flow (2024 FCF roughly $1.2bn) as proof Expedia can sustain operations and strategic investment despite elevated borrowing costs.

Economic growth in emerging markets

Rapid GDP growth in Southeast Asia (2024 GDP growth: Philippines 5.6%, Vietnam 6.0%) and India (2024 GDP growth ~6.8%) and a rising middle class—projected to add ~350 million consumers in Asia by 2030—create strong demand tailwinds for Expedia Group.

Expedia reported increasing investments in localized content and payment integrations across APAC in 2024, aiming to boost GMV in high-growth markets where local payment adoption exceeds 60% in India and Southeast Asia.

Capturing these opportunities requires granular insight into local income distribution, urbanization rates, and shifting discretionary travel spend as per 2024 consumer surveys showing 25–30% higher travel intent among middle-class cohorts.

- High regional GDP growth: India ~6.8% (2024), Vietnam ~6.0%, Philippines ~5.6%

- Asia middle-class expansion: ~350M new consumers by 2030

- Local payment adoption >60% in APAC markets (2024)

- Expedia focusing on localized content/payment integrations to grow GMV

Fuel price fluctuations affecting airfare

Volatility in global energy markets kept jet fuel prices elevated through 2024–2025, with IATA reporting jet fuel averaging about $2.40/gal in 2024 vs $1.80/gal in 2023, pushing airlines to raise fares and fees.

Higher airfares shifted demand to domestic road trips and short-haul flights, boosting Expedia Group’s car rental and local hotel bookings—Q4 2024 car rental bookings rose ~12% YoY.

Expedia leverages data analytics to forecast demand shifts and reallocate marketing spend, increasing promotions for ground travel and regional stays when jet-fuel-driven airfare spikes occur.

- Jet fuel avg $2.40/gal (2024) vs $1.80 (2023)

- Q4 2024 car rentals +12% YoY for Expedia

- Data-driven promo reallocation to ground travel

Expedia: FCF resilience, APAC growth and travel rebound offset rate, FX headwinds

Inflation and higher rates pressured consumer spending and Expedia margins (FY2024 interest expense ~$290m; FCF ~$1.2bn), FX swings altered revenue (USD ±8% vs EUR in 2024) while hedging cut volatility mid-single digits; APAC growth (India 6.8%, Vietnam 6.0%, Philippines 5.6% in 2024) and >60% local payment adoption offer GMV upside; jet fuel ~$2.40/gal (2024) lifted airfare and boosted Q4 2024 car rentals +12% YoY.

| Metric | 2024 / Note |

|---|---|

| Interest expense | ~$290m |

| Free cash flow | ~$1.2bn |

| USD vs EUR | ~+8% |

| India GDP | 6.8% |

| Jet fuel | $2.40/gal |

| Car rentals Q4 YoY | +12% |

What You See Is What You Get

Expedia Group PESTLE Analysis

The preview shown here is the exact Expedia Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Delve into how political, economic, and technological forces are reshaping Expedia Group's prospects with our concise PESTLE snapshot—designed to inform investors and strategists fast.

Buy the full PESTLE analysis to access a complete, actionable breakdown of risks and opportunities, ready for boardrooms, pitches, or investment models.

Political factors

Geopolitical instability and travel restrictions

Ongoing conflicts in Eastern Europe and the Middle East have rerouted flights and heightened safety concerns, contributing to regional booking drops—e.g., Europe-Middle East bookings fell ~12% YoY in Q3 2025 on major OTAs. Governments’ frequent travel-advisories can trigger sudden corridor-specific revenue declines; Expedia Group reported a 9% revenue sensitivity in international leisure bookings to alerts in 2024. Expedia must rapidly reallocate marketing and inventory toward stable markets to mitigate these shocks.

Short-term rental regulations

Major metros have tightened short-term rental rules to ease housing shortages and density; New York, San Francisco and Barcelona cut available listings by up to 20–30% in 2023–2024, pressuring supply for Vrbo.

Common measures include strict licensing and 30–90 day annual caps, directly reducing Vrbo host revenue and contributing to a reported 6% year-over-year dip in US short-term supply on marketplace platforms in 2024.

Expedia must manage a fragmented legal patchwork across 100+ jurisdictions, investing compliance costs estimated in 2024 at tens of millions annually to keep hosts compliant while stabilizing inventory levels.

International trade and tax policies

Implementation of the OECD/G20 global minimum tax (15%) and proliferation of digital services taxes in 20+ jurisdictions affect Expedia Group’s reported international earnings and effective tax rate; Expedia cited a 2024 tax rate impact in its filings, with non-U.S. taxes contributing to its 2024 effective tax rate of around 18–20% (company disclosure). Shifts in U.S.-EU and U.S.-China trade relations can raise cross-border transaction costs and regulatory friction for Expedia’s payments and supplier contracts. Adapting corporate structure and transfer-pricing policies to evolving tax treaties and BEPS-related rules remains a material compliance and planning challenge for Expedia’s international operations.

Government tourism promotion initiatives

Many governments boosted tourism budgets post-pandemic—EU member states increased funding by an estimated 12% in 2024—enabling public-private campaigns that Expedia co-funds to promote destinations and absorb promotional costs.

Expedia leverages these subsidies to drive platform traffic; co-marketing has lifted partner ADRs by up to 8% and contributed to a 2024 YoY room-night growth of ~6% across its brands.

These alliances help Expedia smooth demand seasonality and allocate inventory globally, supporting revenue diversification and higher take-rates in emerging markets.

- Governments ↑ tourism spend (~12% EU, 2024)

- Co-marketing boosts ADR ≈8% for partners

- Platform room-night growth ~6% YoY (2024)

- Improves demand smoothing and revenue diversification

Visa processing and border security

- US visa waits >200 days (selected consulates, 2023)

- China inbound passenger variance ~30% post-2022 reopening

- Long-haul bookings ≈40% of OTA revenue share (2023)

- Expedia operates policy feeds and real-time customer alerts

Political risk slashes travel demand: Europe -12%, US supply -6%, ADR +8%

Political risks (conflict, regulation, tax, visas) drive demand swings and costs: Q3 2025 Europe-ME bookings -12% YoY; US short-term supply -6% YoY (2024); Expedia 2024 effective tax ~18–20%; co-marketing lifted ADR ~8% and room-nights +6% YoY; US visa waits >200 days (2023); China inbound variance ~30% post-reopening.

| Metric | Value |

|---|---|

| Europe-ME bookings | -12% Q3 2025 |

| US STR supply | -6% 2024 |

| Expedia tax rate | 18–20% 2024 |

| ADR lift (co-marketing) | +8% |

| Room-nights | +6% YoY 2024 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Expedia Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented Expedia Group PESTLE summary for quick reference in meetings, easily editable for regional or business-line notes and drop-in ready for presentations or strategy packs.

Economic factors

Global inflation and consumer spending

Persistent inflation through 2025 trimmed global real disposable income, with OECD CPI averaging about 4.8% YTD and US core CPI ~3.9%, pushing travelers toward budget options; Expedia’s value brands and One Key loyalty — reported to drive ~20% higher repeat bookings — are central to retaining price-sensitive customers. The group must offset competitive pricing with rising FY25 operating cost pressures, including wage inflation and higher processing fees, to defend margins.

Currency exchange rate volatility

Significant fluctuations in the U.S. dollar—which strengthened ~8% vs. the euro and weakened ~3% vs. the yen in 2024—affect international travelers’ purchasing power and demand on Expedia Group platforms.

As a U.S.-based company with ~70% of gross bookings originating outside North America, Expedia faces material foreign exchange translation risk that can swing reported revenue quarter-to-quarter.

Expedia reported using derivatives and localized pricing, reducing FX sensitivity; by FY2024 management noted hedges and currency-adjusted revenue metrics lowered reported volatility by an estimated mid-single digits percent.

Interest rate impacts on capital

Higher interest rates—U.S. fed funds averaging ~4.9% in 2024 vs ~1.4% 2010–2019—have raised Expedia Group's cost of debt, increasing interest expense (FY2024 interest expense ~$290m) and making acquisitions pricier.

Management emphasizes a strong balance sheet and disciplined capex; Expedia ended 2024 with ~$3.1bn cash and equivalents and reduced net leverage versus prior year to preserve liquidity.

Investors watch free cash flow (2024 FCF roughly $1.2bn) as proof Expedia can sustain operations and strategic investment despite elevated borrowing costs.

Economic growth in emerging markets

Rapid GDP growth in Southeast Asia (2024 GDP growth: Philippines 5.6%, Vietnam 6.0%) and India (2024 GDP growth ~6.8%) and a rising middle class—projected to add ~350 million consumers in Asia by 2030—create strong demand tailwinds for Expedia Group.

Expedia reported increasing investments in localized content and payment integrations across APAC in 2024, aiming to boost GMV in high-growth markets where local payment adoption exceeds 60% in India and Southeast Asia.

Capturing these opportunities requires granular insight into local income distribution, urbanization rates, and shifting discretionary travel spend as per 2024 consumer surveys showing 25–30% higher travel intent among middle-class cohorts.

- High regional GDP growth: India ~6.8% (2024), Vietnam ~6.0%, Philippines ~5.6%

- Asia middle-class expansion: ~350M new consumers by 2030

- Local payment adoption >60% in APAC markets (2024)

- Expedia focusing on localized content/payment integrations to grow GMV

Fuel price fluctuations affecting airfare

Volatility in global energy markets kept jet fuel prices elevated through 2024–2025, with IATA reporting jet fuel averaging about $2.40/gal in 2024 vs $1.80/gal in 2023, pushing airlines to raise fares and fees.

Higher airfares shifted demand to domestic road trips and short-haul flights, boosting Expedia Group’s car rental and local hotel bookings—Q4 2024 car rental bookings rose ~12% YoY.

Expedia leverages data analytics to forecast demand shifts and reallocate marketing spend, increasing promotions for ground travel and regional stays when jet-fuel-driven airfare spikes occur.

- Jet fuel avg $2.40/gal (2024) vs $1.80 (2023)

- Q4 2024 car rentals +12% YoY for Expedia

- Data-driven promo reallocation to ground travel

Expedia: FCF resilience, APAC growth and travel rebound offset rate, FX headwinds

Inflation and higher rates pressured consumer spending and Expedia margins (FY2024 interest expense ~$290m; FCF ~$1.2bn), FX swings altered revenue (USD ±8% vs EUR in 2024) while hedging cut volatility mid-single digits; APAC growth (India 6.8%, Vietnam 6.0%, Philippines 5.6% in 2024) and >60% local payment adoption offer GMV upside; jet fuel ~$2.40/gal (2024) lifted airfare and boosted Q4 2024 car rentals +12% YoY.

| Metric | 2024 / Note |

|---|---|

| Interest expense | ~$290m |

| Free cash flow | ~$1.2bn |

| USD vs EUR | ~+8% |

| India GDP | 6.8% |

| Jet fuel | $2.40/gal |

| Car rentals Q4 YoY | +12% |

What You See Is What You Get

Expedia Group PESTLE Analysis

The preview shown here is the exact Expedia Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.