Experian Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

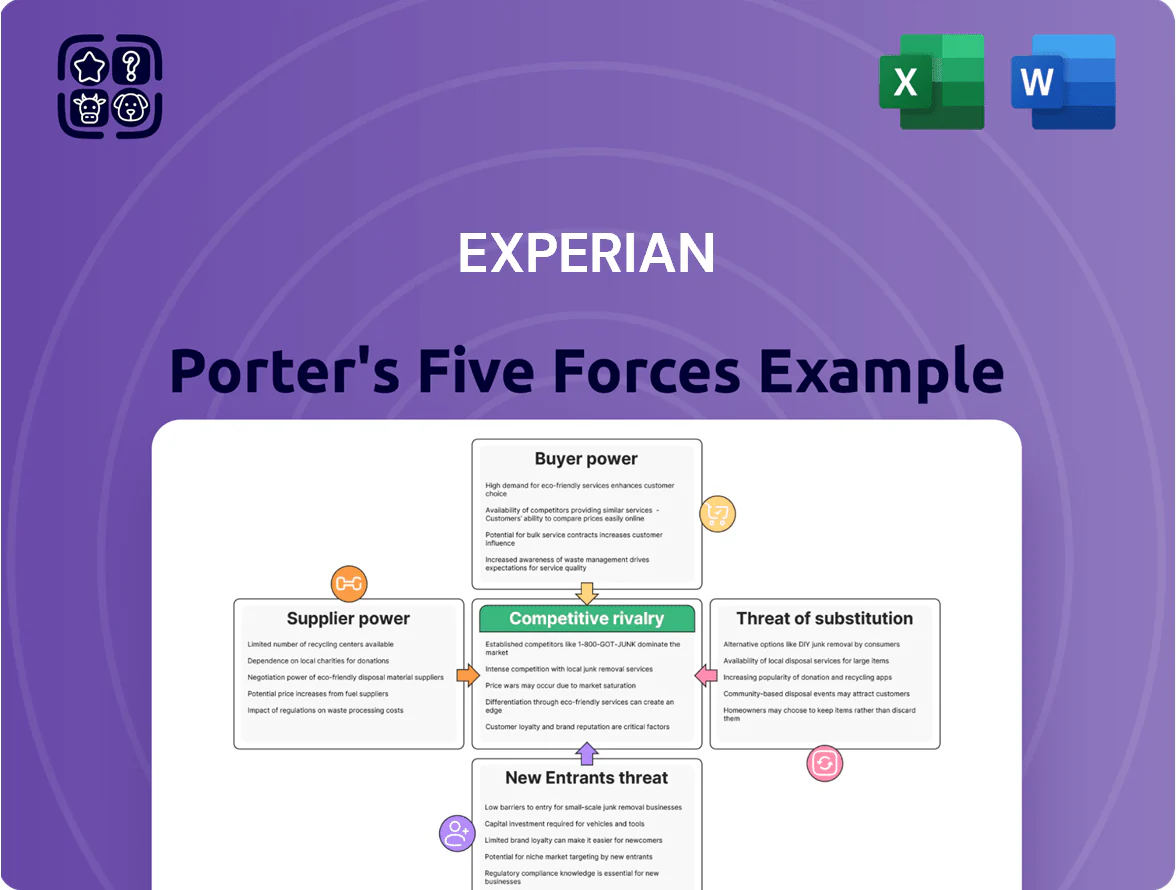

Experian operates in a data-rich, regulation-heavy market where high switching costs and strong buyer expectations limit new entrants but amplify rivalry among incumbents; supplier power is moderate due to diverse data sources while substitutes (free/alternative data) present a growing threat.

This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Experian’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data Providers and Financial Institutions

Banks, utilities, and retail lenders supply the raw credit files that power Experian’s core products; in 2024 US consumer credit data from banks represented roughly 65% of bureau inputs. These providers depend on Experian for risk models and receivables, yet they keep leverage as data owners and can demand pricing or restrict feeds. A loss or cutback in agreements would quickly degrade report accuracy and could hit revenue—Experian reported 2024 global revenue of $6.3B, so even a mid-single-digit data disruption matters.

Cloud Infrastructure and Technology Partners

As Experian shifts more operations to cloud providers like Amazon Web Services and Microsoft Azure, its reliance grows—AWS and Azure held ~65% of global cloud IaaS/PaaS market in 2024, boosting their bargaining power. The specialized infrastructure and estimated multi-million-dollar costs to migrate or reverse a move raise switching barriers. Experian must negotiate volume discounts, commit to multi-year contracts, and use multi-cloud strategies to control costs and preserve uptime.

Regulatory and Governmental Bodies

Government agencies supply essential public-record data—tax liens, bankruptcy filings—that Experian (EXPN: publicly traded) cannot source elsewhere; in 2024 public-record-derived revenue represented about 18% of U.S. consumer-data services, per industry filings.

These agencies set access rules and fees, giving them near-absolute bargaining power; a 2023 DOJ/state initiative raising court-record fees by 12–25% would raise Experian’s data costs directly.

Policy shifts—like increased privacy controls or open-data mandates—can force Experian to alter products quickly; in 2022-24 regulatory changes cut similar vendors’ public-record inventories by ~8% annually, reducing related product revenue and upsell potential.

Specialized Human Capital

The demand for data scientists, cybersecurity experts, and AI developers gives suppliers of specialized human capital strong leverage over Experian, raising hiring costs and turnover risk; US median data scientist pay was about $122,000 in 2024 and cybersecurity roles saw 15% wage growth year-over-year. Experian must pay top-tier total compensation and invest in retention to protect analytics and data repositories.

- High wages: median $122,000 (data scientists, 2024)

- Cybersecurity pay up 15% YoY (2024)

- Must invest in retention: salaries, benefits, training

- Talent shortages raise operational and security risk

Third Party Data Aggregators

Experian supplements its databases with niche third-party aggregators for marketing and fraud prevention; in 2024 roughly 8–12% of revenue-linked datasets came from partners, raising supplier leverage when datasets are unique.

If a supplier holds non-replicable data, they can demand higher fees or exclusivity, so Experian keeps a diverse partner mix to limit single-supplier risk and price pressure.

Here’s the quick math: replacing a unique feed can cost $5–20m in one-time integration and 6–18 months of lost data quality if internal builds are required.

- 8–12% revenue-linked partner data (2024)

- $5–20m estimated replacement cost per unique feed

- 6–18 months integration/time-to-quality risk

- Diverse partner mix reduces single-supplier leverage

Supplier power spikes: banks, cloud & data feeds lock in costs and time to replace

Suppliers hold strong leverage: banks provided ~65% of US credit inputs (2024), cloud vendors (AWS/Azure ~65% IaaS/PaaS share, 2024) raise switching costs, public-record feeds drove ~18% of US consumer-data revenue (2024), and niche partners supplied 8–12% of revenue-linked datasets (2024); replacing unique feeds costs $5–20m and 6–18 months.

| Supplier | 2024 metric |

|---|---|

| Banks | 65% credit inputs |

| Cloud | AWS/Azure ~65% market |

| Public records | 18% revenue |

| Partners | 8–12% datasets |

What is included in the product

Tailored Porter's Five Forces analysis for Experian that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats—delivering data-backed strategic insights for investor reports, business planning, or internal strategy.

One-sheet Experian Porter's Five Forces summary—clarifies competitive pressures quickly and fits straight into decks for fast, data-driven decisions.

Customers Bargaining Power

Tier One Financial Institutions

Small and Medium Enterprises

Smaller business clients have lower bargaining power versus large corporates because they account for a smaller share of Experian’s revenues; in 2024 SMEs likely represented under 20% of global B2B data revenue for major credit bureaus. Still, digital marketplaces let SMEs compare offers quickly, raising price sensitivity. Experian must sell standardized, cost-efficient SME packages—for example, sub-$50/month tiers—to stay competitive while protecting margins through automation and scale.

Individual Consumers

Individual consumers gained influence as 56% of US adults checked their credit in 2024 and free tools rose—so while they lack direct bargaining power, collective behavior forces Experian to add features like Experian Boost (launched 2019; over 17 million users by 2024) to keep engagement.

Retail and E-commerce Merchants

Merchants using Experian for fraud prevention and identity verification have moderate bargaining power because they demand low-friction transactions; 68% of US e-commerce chargebacks in 2024 were linked to identity issues, raising merchant sensitivity to accuracy.

These customers prioritize speed and accuracy and will switch to fintechs—many offer sub-100ms decisioning—if Experian lags, forcing Experian to invest in real-time processing and AI models.

- Moderate power: merchants value accuracy over price

- 68% of 2024 US e-commerce chargebacks tied to identity

- Fintech rivals offer <100ms decisioning

- Drives Experian spend on real-time AI and infra

Marketing and Lead Generation Firms

Clients in marketing use Experian data for targeted ads and customer acquisition; US digital ad spend reached 240 billion in 2024, so ROI sensitivity is high.

Buyers can reallocate budgets to Meta, Google, or data-driven agencies; churn risk rises if Experian’s match rates and lift aren’t clearly better than platform targeting.

To retain clients, Experian must prove superior data accuracy and higher conversion lift—e.g., a 10–20% incremental conversion claim backed by A/B tests.

- Marketing clients demand measurable ROI; $240B US digital ad market (2024)

- High switching risk to Meta/Google or specialty agencies

- Retention needs: demonstrable match rates, 10–20% conversion lift

High‑value banks, price‑sensitive SMEs, real‑time fraud needs, and ad ROI pressure

| Customer | Share/Stat | Key demand |

|---|---|---|

| Top banks | 35–45% B2B; >$50m deals | Discounts, bespoke integration |

| SMEs | <20% B2B | Low‑cost tiers |

| Merchants | 68% chargebacks (2024) | Real‑time, accuracy |

| Marketing clients | $240B US digital ads (2024) | 10–20% conversion lift |

Preview Before You Purchase

Experian Porter's Five Forces Analysis

This preview shows the exact Experian Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the fully formatted, professionally written document ready for download and use the moment you buy. The file covers threat of new entrants, bargaining power of suppliers and buyers, competitive rivalry, and threat of substitutes with actionable insights. What you see is precisely what you’ll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Experian operates in a data-rich, regulation-heavy market where high switching costs and strong buyer expectations limit new entrants but amplify rivalry among incumbents; supplier power is moderate due to diverse data sources while substitutes (free/alternative data) present a growing threat.

This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Experian’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data Providers and Financial Institutions

Banks, utilities, and retail lenders supply the raw credit files that power Experian’s core products; in 2024 US consumer credit data from banks represented roughly 65% of bureau inputs. These providers depend on Experian for risk models and receivables, yet they keep leverage as data owners and can demand pricing or restrict feeds. A loss or cutback in agreements would quickly degrade report accuracy and could hit revenue—Experian reported 2024 global revenue of $6.3B, so even a mid-single-digit data disruption matters.

Cloud Infrastructure and Technology Partners

As Experian shifts more operations to cloud providers like Amazon Web Services and Microsoft Azure, its reliance grows—AWS and Azure held ~65% of global cloud IaaS/PaaS market in 2024, boosting their bargaining power. The specialized infrastructure and estimated multi-million-dollar costs to migrate or reverse a move raise switching barriers. Experian must negotiate volume discounts, commit to multi-year contracts, and use multi-cloud strategies to control costs and preserve uptime.

Regulatory and Governmental Bodies

Government agencies supply essential public-record data—tax liens, bankruptcy filings—that Experian (EXPN: publicly traded) cannot source elsewhere; in 2024 public-record-derived revenue represented about 18% of U.S. consumer-data services, per industry filings.

These agencies set access rules and fees, giving them near-absolute bargaining power; a 2023 DOJ/state initiative raising court-record fees by 12–25% would raise Experian’s data costs directly.

Policy shifts—like increased privacy controls or open-data mandates—can force Experian to alter products quickly; in 2022-24 regulatory changes cut similar vendors’ public-record inventories by ~8% annually, reducing related product revenue and upsell potential.

Specialized Human Capital

The demand for data scientists, cybersecurity experts, and AI developers gives suppliers of specialized human capital strong leverage over Experian, raising hiring costs and turnover risk; US median data scientist pay was about $122,000 in 2024 and cybersecurity roles saw 15% wage growth year-over-year. Experian must pay top-tier total compensation and invest in retention to protect analytics and data repositories.

- High wages: median $122,000 (data scientists, 2024)

- Cybersecurity pay up 15% YoY (2024)

- Must invest in retention: salaries, benefits, training

- Talent shortages raise operational and security risk

Third Party Data Aggregators

Experian supplements its databases with niche third-party aggregators for marketing and fraud prevention; in 2024 roughly 8–12% of revenue-linked datasets came from partners, raising supplier leverage when datasets are unique.

If a supplier holds non-replicable data, they can demand higher fees or exclusivity, so Experian keeps a diverse partner mix to limit single-supplier risk and price pressure.

Here’s the quick math: replacing a unique feed can cost $5–20m in one-time integration and 6–18 months of lost data quality if internal builds are required.

- 8–12% revenue-linked partner data (2024)

- $5–20m estimated replacement cost per unique feed

- 6–18 months integration/time-to-quality risk

- Diverse partner mix reduces single-supplier leverage

Supplier power spikes: banks, cloud & data feeds lock in costs and time to replace

Suppliers hold strong leverage: banks provided ~65% of US credit inputs (2024), cloud vendors (AWS/Azure ~65% IaaS/PaaS share, 2024) raise switching costs, public-record feeds drove ~18% of US consumer-data revenue (2024), and niche partners supplied 8–12% of revenue-linked datasets (2024); replacing unique feeds costs $5–20m and 6–18 months.

| Supplier | 2024 metric |

|---|---|

| Banks | 65% credit inputs |

| Cloud | AWS/Azure ~65% market |

| Public records | 18% revenue |

| Partners | 8–12% datasets |

What is included in the product

Tailored Porter's Five Forces analysis for Experian that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats—delivering data-backed strategic insights for investor reports, business planning, or internal strategy.

One-sheet Experian Porter's Five Forces summary—clarifies competitive pressures quickly and fits straight into decks for fast, data-driven decisions.

Customers Bargaining Power

Tier One Financial Institutions

Small and Medium Enterprises

Smaller business clients have lower bargaining power versus large corporates because they account for a smaller share of Experian’s revenues; in 2024 SMEs likely represented under 20% of global B2B data revenue for major credit bureaus. Still, digital marketplaces let SMEs compare offers quickly, raising price sensitivity. Experian must sell standardized, cost-efficient SME packages—for example, sub-$50/month tiers—to stay competitive while protecting margins through automation and scale.

Individual Consumers

Individual consumers gained influence as 56% of US adults checked their credit in 2024 and free tools rose—so while they lack direct bargaining power, collective behavior forces Experian to add features like Experian Boost (launched 2019; over 17 million users by 2024) to keep engagement.

Retail and E-commerce Merchants

Merchants using Experian for fraud prevention and identity verification have moderate bargaining power because they demand low-friction transactions; 68% of US e-commerce chargebacks in 2024 were linked to identity issues, raising merchant sensitivity to accuracy.

These customers prioritize speed and accuracy and will switch to fintechs—many offer sub-100ms decisioning—if Experian lags, forcing Experian to invest in real-time processing and AI models.

- Moderate power: merchants value accuracy over price

- 68% of 2024 US e-commerce chargebacks tied to identity

- Fintech rivals offer <100ms decisioning

- Drives Experian spend on real-time AI and infra

Marketing and Lead Generation Firms

Clients in marketing use Experian data for targeted ads and customer acquisition; US digital ad spend reached 240 billion in 2024, so ROI sensitivity is high.

Buyers can reallocate budgets to Meta, Google, or data-driven agencies; churn risk rises if Experian’s match rates and lift aren’t clearly better than platform targeting.

To retain clients, Experian must prove superior data accuracy and higher conversion lift—e.g., a 10–20% incremental conversion claim backed by A/B tests.

- Marketing clients demand measurable ROI; $240B US digital ad market (2024)

- High switching risk to Meta/Google or specialty agencies

- Retention needs: demonstrable match rates, 10–20% conversion lift

High‑value banks, price‑sensitive SMEs, real‑time fraud needs, and ad ROI pressure

| Customer | Share/Stat | Key demand |

|---|---|---|

| Top banks | 35–45% B2B; >$50m deals | Discounts, bespoke integration |

| SMEs | <20% B2B | Low‑cost tiers |

| Merchants | 68% chargebacks (2024) | Real‑time, accuracy |

| Marketing clients | $240B US digital ads (2024) | 10–20% conversion lift |

Preview Before You Purchase

Experian Porter's Five Forces Analysis

This preview shows the exact Experian Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the fully formatted, professionally written document ready for download and use the moment you buy. The file covers threat of new entrants, bargaining power of suppliers and buyers, competitive rivalry, and threat of substitutes with actionable insights. What you see is precisely what you’ll get.