Experian PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how regulatory shifts, data privacy trends, and fintech innovation are reshaping Experian’s competitive landscape with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Buy the full PESTLE analysis to access detailed risk assessments, market implications, and ready-to-use slides that accelerate decision-making.

Political factors

Geopolitical Data Sovereignty

Governments are imposing stricter data residency laws, with over 70 countries enacting or proposing data localization rules by 2025, forcing Experian to store and process citizen data within national borders in key markets such as India and Brazil.

This has compelled Experian to fragment its infrastructure, increasing capex and opex—estimated regional compliance costs rose by ~12% in 2024—while managing diverse regulatory regimes across 35+ jurisdictions.

By late 2025 these political shifts raised operational complexity, requiring localized data-management strategies, on-prem/cloud splits, and partnerships to protect revenue streams in regulated markets where Experian derives a significant portion of its £3.2bn FY2024 revenue.

Government Financial Inclusion Policies

Political initiatives expanding credit access to underserved groups create major upside for Experian in markets like Brazil and India, where 2024 central bank programs aim to increase formal credit penetration by ~10–15% by 2027. Governments are partnering with data providers to use alternative data scoring—Brazil’s open banking rollout reached 60% adoption in 2024—driving demand for Experian’s analytics. These policies boost uptake of Experian’s credit-building tools, aligning with national goals to raise financial inclusion and GDP growth.

International Trade Relations

Ongoing trade tensions and shifting alliances between major economies affect cross-border flow of financial services and data analytics; in 2024 global data localization rules grew 8% year-on-year, increasing compliance costs for Experian’s cross-border services.

National Security and Infrastructure Regulations

As financial data is now classed as critical national infrastructure in multiple jurisdictions, Experian faces intensified government scrutiny and must meet stricter resilience and security protocols, contributing to its FY2024 security-related capex rise of ~12% year-on-year.

Political leaders demand transparency on defenses against state-sponsored cyber threats, prompting Experian to undergo more frequent audits and share risk assessments with regulators after 68% of global breaches in 2023 were attributed to nation-state actors.

- Classified as critical infrastructure → higher oversight

- FY2024 security capex +12% YoY

- More frequent audits and regulatory reporting

- 68% of 2023 breaches linked to nation-state actors

Public Sector Digitization Initiatives

Rising global digitization of government services boosts demand for Experian’s identity-verification and eligibility tools; public-sector projects accounted for an estimated 10–15% of global identity-verification spend in 2024, benefiting Experian’s governmental contracts.

Political mandates to modernize administration drive multi-year deals—Experian reported government-related recurring revenue growth of roughly 12% in 2024—securing roles in social benefit distribution and tax compliance.

These long-term partnerships position Experian as a core digital infrastructure provider to states, reinforcing stable cash flows and increasing switching costs for public agencies.

- Public-sector identity spend ~10–15% (2024)

- Experian government-related recurring revenue growth ~12% (2024)

- Multi-year contracts increase stability and switching costs

Data-residency rules hit 35+ markets—security capex +12%, compliance costs +12%

Governments tightened data residency and critical-infrastructure rules across 35+ jurisdictions, driving FY2024 compliance/security capex +12% and fragmenting Experian’s infrastructure, raising regional compliance costs ~12% in 2024.

Public-sector digitization and credit inclusion programs (open banking 60% adoption in Brazil 2024) expanded government recurring revenue ~12% in 2024, with public identity spend ~10–15%.

| Metric | Value |

|---|---|

| Jurisdictions with strict data rules | 35+ |

| FY2024 security capex YoY | +12% |

| Regional compliance cost rise (2024) | ~12% |

| Brazil open banking adoption (2024) | 60% |

| Govt recurring revenue growth (2024) | ~12% |

| Public identity spend (2024) | 10–15% |

What is included in the product

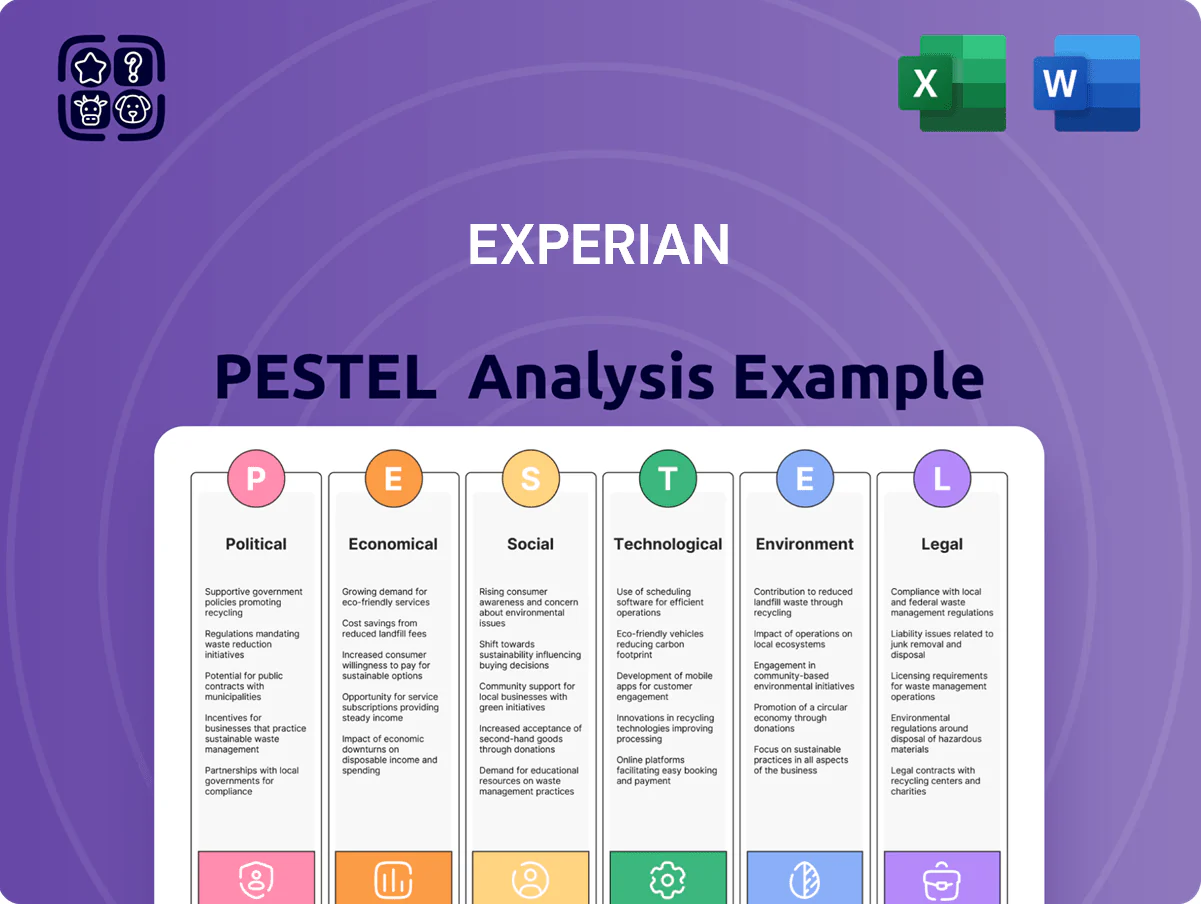

Explores how macro-environmental forces uniquely impact Experian across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

Condenses Experian's PESTLE into a clear, shareable summary that teams can drop into presentations or planning folders for fast alignment on external risks and market positioning.

Economic factors

Global Interest Rate Cycles

Fluctuations in central bank rates directly affect consumer credit demand and mortgage volumes, key revenue drivers for Experian; UK Bank Rate rose to 5.25% in 2023 then eased to 4.5% by Q4 2025, reducing refinance activity but supporting new-credit originations.

As rates stabilized in late 2025, Experian saw demand shift from debt consolidation toward new credit acquisitions, with UK mortgage approvals up 6% YoY and US credit card originations rising 8% in 2025.

Heightened economic volatility pushed lenders to adopt Experian’s dynamic risk tools; usage of its decisioning platforms grew ~20% in 2024–25 as delinquency forecasting and stress-testing became critical.

Emerging Market Expansion

High GDP growth in emerging markets—Sub-Saharan Africa ~3.5% and South Asia ~6.5% projected 2025 IMF—creates fertile ground for Experian to scale credit bureau services; rising middle-class households (projected 1.4 billion additional middle-class people in EMs by 2030, Brookings) increases demand for loans and data analytics. Experian’s targeted investments in LATAM and APAC, which accounted for ~30% of 2024 revenue, offset saturation in North America and UK.

Inflationary Pressure on Operations

Persistent inflation raises Experian’s operating costs, notably specialized labor and tech procurement, with UK CPI averaging 4.0% in 2024 and global cloud costs up ~18% YoY; index-linked contracts let Experian pass much through, but rapid price spikes compressed adjusted operating margin to 17.8% in FY2024, forcing management to balance competitive pricing against maintaining data-processing quality and investing in automation to curb future inflationary pressure.

Consumer Spending and Debt Levels

Higher household debt and shifting consumer spend drive credit demand; US household debt hit $17.7 trillion Q3 2025, raising delinquencies and boosting Experian’s fraud-prevention and debt-recovery services as lenders seek loss mitigation.

When consumer confidence strengthens—US Conference Board index climbed to 110.5 Dec 2025—Experian’s marketing services and credit-prospecting tools gain traction, expanding revenue from targeted acquisition products.

- Rising debt → higher fraud/debt-recovery demand

- Strong confidence → growth in marketing/credit-prospecting

- Q3 2025 US household debt $17.7T; Consumer Confidence 110.5 Dec 2025

Mortgage Market Fluctuations

The housing market remains a critical component of the economic landscape, directly affecting Experian’s Decision Analytics and North America segments as mortgage originations fell about 15% in 2024 versus 2021 peaks, reducing demand for credit decisioning and valuation services.

Declines in property values—U.S. FHFA index rose only 1.2% YoY in 2024 after prior volatility—and tighter lending standards drove higher credit inquiries for loan workouts and increased need for risk scoring.

Experian’s real-time property datasets and automated risk insights, used by over 4,500 banking clients, are essential for clients to adapt to these cyclical shifts and manage credit exposure.

- Mortgage originations -15% vs 2021

- FHFA price growth +1.2% YoY (2024)

- 4,500+ banking clients rely on Experian data

Experian weathers higher rates and debt; decisioning up 20%, EMs ~30% of revenue

Economic shifts—rising rates, inflation, household debt, and varied regional GDP—reshaped Experian: FY2024 adj. op. margin 17.8%, Q3 2025 US household debt $17.7T, UK Bank Rate 5.25% (2023) → 4.5% (Q4 2025); mortgage originations -15% vs 2021; decisioning platform usage +20% (2024–25); emerging markets ~30% of 2024 revenue.

| Metric | Value |

|---|---|

| Adj. op. margin FY2024 | 17.8% |

| US household debt Q3 2025 | $17.7T |

| UK Bank Rate | 5.25% (2023) → 4.5% (Q4 2025) |

| Mortgage originations vs 2021 | -15% |

| Decisioning platform usage 2024–25 | +20% |

| EM revenue share 2024 | ~30% |

Preview the Actual Deliverable

Experian PESTLE Analysis

The preview shown here is the exact Experian PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. What you see is the final, professionally structured file you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how regulatory shifts, data privacy trends, and fintech innovation are reshaping Experian’s competitive landscape with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Buy the full PESTLE analysis to access detailed risk assessments, market implications, and ready-to-use slides that accelerate decision-making.

Political factors

Geopolitical Data Sovereignty

Governments are imposing stricter data residency laws, with over 70 countries enacting or proposing data localization rules by 2025, forcing Experian to store and process citizen data within national borders in key markets such as India and Brazil.

This has compelled Experian to fragment its infrastructure, increasing capex and opex—estimated regional compliance costs rose by ~12% in 2024—while managing diverse regulatory regimes across 35+ jurisdictions.

By late 2025 these political shifts raised operational complexity, requiring localized data-management strategies, on-prem/cloud splits, and partnerships to protect revenue streams in regulated markets where Experian derives a significant portion of its £3.2bn FY2024 revenue.

Government Financial Inclusion Policies

Political initiatives expanding credit access to underserved groups create major upside for Experian in markets like Brazil and India, where 2024 central bank programs aim to increase formal credit penetration by ~10–15% by 2027. Governments are partnering with data providers to use alternative data scoring—Brazil’s open banking rollout reached 60% adoption in 2024—driving demand for Experian’s analytics. These policies boost uptake of Experian’s credit-building tools, aligning with national goals to raise financial inclusion and GDP growth.

International Trade Relations

Ongoing trade tensions and shifting alliances between major economies affect cross-border flow of financial services and data analytics; in 2024 global data localization rules grew 8% year-on-year, increasing compliance costs for Experian’s cross-border services.

National Security and Infrastructure Regulations

As financial data is now classed as critical national infrastructure in multiple jurisdictions, Experian faces intensified government scrutiny and must meet stricter resilience and security protocols, contributing to its FY2024 security-related capex rise of ~12% year-on-year.

Political leaders demand transparency on defenses against state-sponsored cyber threats, prompting Experian to undergo more frequent audits and share risk assessments with regulators after 68% of global breaches in 2023 were attributed to nation-state actors.

- Classified as critical infrastructure → higher oversight

- FY2024 security capex +12% YoY

- More frequent audits and regulatory reporting

- 68% of 2023 breaches linked to nation-state actors

Public Sector Digitization Initiatives

Rising global digitization of government services boosts demand for Experian’s identity-verification and eligibility tools; public-sector projects accounted for an estimated 10–15% of global identity-verification spend in 2024, benefiting Experian’s governmental contracts.

Political mandates to modernize administration drive multi-year deals—Experian reported government-related recurring revenue growth of roughly 12% in 2024—securing roles in social benefit distribution and tax compliance.

These long-term partnerships position Experian as a core digital infrastructure provider to states, reinforcing stable cash flows and increasing switching costs for public agencies.

- Public-sector identity spend ~10–15% (2024)

- Experian government-related recurring revenue growth ~12% (2024)

- Multi-year contracts increase stability and switching costs

Data-residency rules hit 35+ markets—security capex +12%, compliance costs +12%

Governments tightened data residency and critical-infrastructure rules across 35+ jurisdictions, driving FY2024 compliance/security capex +12% and fragmenting Experian’s infrastructure, raising regional compliance costs ~12% in 2024.

Public-sector digitization and credit inclusion programs (open banking 60% adoption in Brazil 2024) expanded government recurring revenue ~12% in 2024, with public identity spend ~10–15%.

| Metric | Value |

|---|---|

| Jurisdictions with strict data rules | 35+ |

| FY2024 security capex YoY | +12% |

| Regional compliance cost rise (2024) | ~12% |

| Brazil open banking adoption (2024) | 60% |

| Govt recurring revenue growth (2024) | ~12% |

| Public identity spend (2024) | 10–15% |

What is included in the product

Explores how macro-environmental forces uniquely impact Experian across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

Condenses Experian's PESTLE into a clear, shareable summary that teams can drop into presentations or planning folders for fast alignment on external risks and market positioning.

Economic factors

Global Interest Rate Cycles

Fluctuations in central bank rates directly affect consumer credit demand and mortgage volumes, key revenue drivers for Experian; UK Bank Rate rose to 5.25% in 2023 then eased to 4.5% by Q4 2025, reducing refinance activity but supporting new-credit originations.

As rates stabilized in late 2025, Experian saw demand shift from debt consolidation toward new credit acquisitions, with UK mortgage approvals up 6% YoY and US credit card originations rising 8% in 2025.

Heightened economic volatility pushed lenders to adopt Experian’s dynamic risk tools; usage of its decisioning platforms grew ~20% in 2024–25 as delinquency forecasting and stress-testing became critical.

Emerging Market Expansion

High GDP growth in emerging markets—Sub-Saharan Africa ~3.5% and South Asia ~6.5% projected 2025 IMF—creates fertile ground for Experian to scale credit bureau services; rising middle-class households (projected 1.4 billion additional middle-class people in EMs by 2030, Brookings) increases demand for loans and data analytics. Experian’s targeted investments in LATAM and APAC, which accounted for ~30% of 2024 revenue, offset saturation in North America and UK.

Inflationary Pressure on Operations

Persistent inflation raises Experian’s operating costs, notably specialized labor and tech procurement, with UK CPI averaging 4.0% in 2024 and global cloud costs up ~18% YoY; index-linked contracts let Experian pass much through, but rapid price spikes compressed adjusted operating margin to 17.8% in FY2024, forcing management to balance competitive pricing against maintaining data-processing quality and investing in automation to curb future inflationary pressure.

Consumer Spending and Debt Levels

Higher household debt and shifting consumer spend drive credit demand; US household debt hit $17.7 trillion Q3 2025, raising delinquencies and boosting Experian’s fraud-prevention and debt-recovery services as lenders seek loss mitigation.

When consumer confidence strengthens—US Conference Board index climbed to 110.5 Dec 2025—Experian’s marketing services and credit-prospecting tools gain traction, expanding revenue from targeted acquisition products.

- Rising debt → higher fraud/debt-recovery demand

- Strong confidence → growth in marketing/credit-prospecting

- Q3 2025 US household debt $17.7T; Consumer Confidence 110.5 Dec 2025

Mortgage Market Fluctuations

The housing market remains a critical component of the economic landscape, directly affecting Experian’s Decision Analytics and North America segments as mortgage originations fell about 15% in 2024 versus 2021 peaks, reducing demand for credit decisioning and valuation services.

Declines in property values—U.S. FHFA index rose only 1.2% YoY in 2024 after prior volatility—and tighter lending standards drove higher credit inquiries for loan workouts and increased need for risk scoring.

Experian’s real-time property datasets and automated risk insights, used by over 4,500 banking clients, are essential for clients to adapt to these cyclical shifts and manage credit exposure.

- Mortgage originations -15% vs 2021

- FHFA price growth +1.2% YoY (2024)

- 4,500+ banking clients rely on Experian data

Experian weathers higher rates and debt; decisioning up 20%, EMs ~30% of revenue

Economic shifts—rising rates, inflation, household debt, and varied regional GDP—reshaped Experian: FY2024 adj. op. margin 17.8%, Q3 2025 US household debt $17.7T, UK Bank Rate 5.25% (2023) → 4.5% (Q4 2025); mortgage originations -15% vs 2021; decisioning platform usage +20% (2024–25); emerging markets ~30% of 2024 revenue.

| Metric | Value |

|---|---|

| Adj. op. margin FY2024 | 17.8% |

| US household debt Q3 2025 | $17.7T |

| UK Bank Rate | 5.25% (2023) → 4.5% (Q4 2025) |

| Mortgage originations vs 2021 | -15% |

| Decisioning platform usage 2024–25 | +20% |

| EM revenue share 2024 | ~30% |

Preview the Actual Deliverable

Experian PESTLE Analysis

The preview shown here is the exact Experian PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. What you see is the final, professionally structured file you’ll own upon checkout.