Expro PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, regulatory pressures, and technological advances are reshaping Expro’s prospects in our concise PESTLE snapshot—perfect for investors and strategists seeking a quick edge. Purchase the full PESTLE for a complete, actionable breakdown that highlights risks, opportunities, and strategic implications you can use immediately.

Political factors

Geopolitical instability in energy regions

Ongoing conflicts and diplomatic tensions in key oil-producing regions like the Middle East and Eastern Europe continue to disrupt supply chains and operational safety as of late 2025, with IEA reporting a 2.3% drop in regional crude exports year‑on‑year and insurers raising premiums by ~18% for operations in high‑risk zones.

Expro must navigate shifting alliances and potential sanctions that constrained services to Russia in 2024–25, forcing reallocation of ~12% of its subsea and well intervention capacity to alternative markets.

Political volatility often necessitates rapid relocation of assets and personnel to more stable jurisdictions, increasing logistics and standby costs by an estimated $8–12 million annually for mid‑sized service providers.

Energy security and independence policies

Resource nationalism and local content requirements

Governments in emerging markets are tightening local content laws, with Angola and Nigeria increasing local hiring and procurement mandates to 60-70% by 2025, forcing Expro to partner with domestic firms and source local talent to retain contracts.

Expro must balance its global safety and technical standards with national mandates—noncompliance risks license suspension, as seen in 2023 when Brazil fined foreign contractors over local content breaches totaling over $250m.

Failure to adapt could restrict market access and cost Expro significant revenue: in 2024 regional contract losses for oilfield service firms reached an estimated $1.8bn due to resource nationalism enforcement.

Global trade tariffs and protectionism

The 2025 trade environment features heightened tariffs and non-tariff barriers that disrupt movement of specialized oilfield equipment and technology, with US-China tariffs still adding up to 10–25% on relevant components and average EU safeguard duties rising 5% year-on-year.

These duty changes have pushed Expro’s capital expenditure per major well tool program up an estimated 8–12% and extended lead times by 6–10 weeks, increasing project financing needs.

Strategic planning must model tariff volatility, hedging import costs and reallocating supply chains to protect international margins and maintain competitive tender pricing.

- Tariff impact: +8–12% capex; lead times +6–10 weeks

Impact of international climate agreements

Political commitments under COP26/27 accelerate decommissioning and tighten rules on carbon-heavy extraction, with 130+ countries submitting net-zero targets by 2025 pressuring faster asset retirements and stricter permits.

Governments’ net-zero pledges drive demand for well integrity and leak-detection services; methane-focused regulations (e.g., EU methane Pledge cutting emissions 30% by 2030) favor Expro’s monitoring offerings.

Regulatory shifts force Expro to pivot toward decarbonization-aligned services, impacting CAPEX allocation as operators redirect an estimated 5–10% of project spend to emissions control technologies.

- COP commitments increase decommissioning and permit strictness

- Net-zero targets boost demand for leak detection and integrity services

- Estimated 5–10% reallocation of project CAPEX to emissions controls

Geopolitics, sanctions surge costs and reshuffle supplies as rigs, subsidies and local content rise

Geopolitical conflicts and sanctions in 2024–25 cut regional crude exports ~2.3% and forced reallocation of ~12% of Expro’s subsea capacity, raising insurance and logistics costs; Western energy security programs (+12% regional rig activity mid‑2025) and $40–60bn subsidies sustain demand for flow management; local content rules (60–70% in Angola/Nigeria) and tariffs (+8–12% capex, lead times +6–10 weeks) increase compliance and supply‑chain costs.

| Metric | Value |

|---|---|

| Regional crude export change (IEA) | -2.3% (2024–25) |

| Reallocated subsea capacity | ~12% |

| Rig activity (mid‑2025) | +12% YoY |

| Subsidies to local production | $40–60bn (2024–25) |

| Local content mandates (Angola/Nigeria) | 60–70% (2025) |

| Tariff impact on capex | +8–12% |

| Lead time increases | +6–10 weeks |

What is included in the product

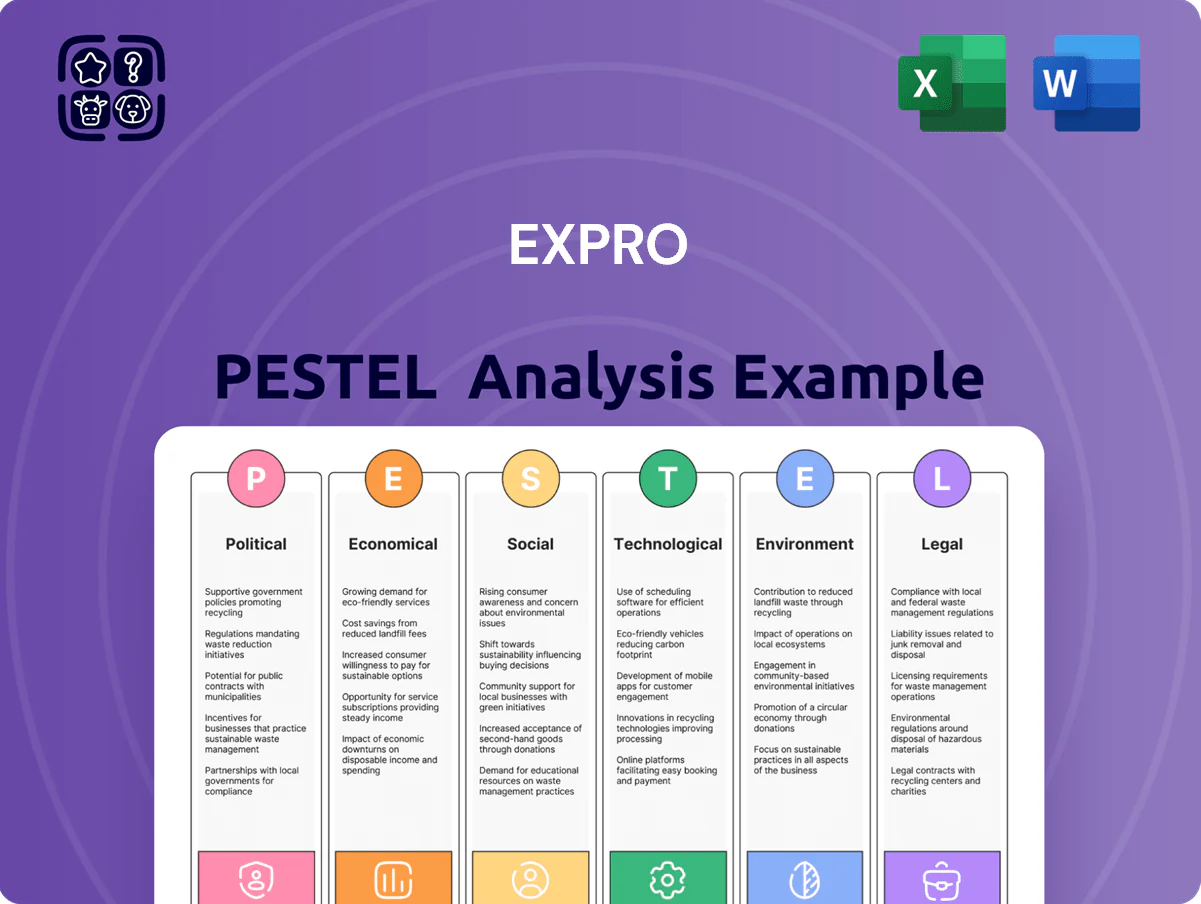

Explores how macro-environmental factors uniquely affect Expro across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and localized market/regulatory context to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Expro's PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and easy drop-in to presentations or planning sessions.

Economic factors

Fluctuations in global crude oil prices

Expro’s revenue is highly sensitive to Brent and WTI prices, which dictate E&P capex; Brent averaged about $86/bbl in 2024 and rose toward $95–$110/bbl in late 2025 amid OPEC+ cuts, boosting client drilling budgets.

Price volatility from OPEC+ decisions and demand shifts reduced new well forecasts by ~5–8% in 2024–25, directly affecting project volume for Expro.

High prices increase demand for Expro’s optimization and completion services, while sub-$70 Brent periods shift clients to lower-cost well intervention and maintenance work.

Inflationary pressure on operational costs

Persistent inflation through 2025 raised input costs for energy service providers—global manufacturing input prices rose ~12% in 2024 and CPI averaged 5.8%—forcing Expro to absorb higher prices for raw materials, specialized labor and logistics.

To protect margins, Expro is pursuing contract price escalations and internal efficiency drives; recent H2 2024 contracts included average 4–7% escalation clauses in new service agreements.

Manufacturing high-spec subsea well access systems is especially exposed: prices for nickel and titanium alloys spiked 18–25% in 2024, increasing BOM costs and pressuring gross margins.

Interest rate environment and capital access

As of late 2025 global policy rates remain elevated versus pre-2022 norms, with the US Fed funds target near 5.25–5.50% and ECB rates around 3.75–4.00%, raising corporate borrowing costs and pushing average global loan spreads for energy projects higher by ~150–200bps versus 2021, which can postpone offshore CAPEX and curb demand for Expro’s long-cycle well construction services.

Global economic growth and energy demand

The pace of industrial recovery in India and Southeast Asia—IMF 2025 growth forecasts of 6.5% for India and 4.6% for ASEAN-5—supports rising hydrocarbon demand, benefiting Expro where deepwater exploration expands to meet local energy needs.

Expro’s regional growth is cyclical; project deferrals during slowdowns can hit exploration/appraisal revenues—E&P capex in Asia-Pacific fell 12% in 2024, signaling risk to near-term orderbooks.

- India GDP 2025 est 6.5%

- ASEAN-5 2025 est 4.6%

- Asia-Pacific E&P capex down 12% in 2024

- Deepwater projects drive Expro exposure

Currency exchange rate volatility

As a multinational, Expro faces material foreign exchange risk: the US dollar strengthened ~8% vs major Latin American currencies and ~6% vs several West African currencies in 2024, which can compress reported international earnings when converted to USD.

Maintaining hedging programs—forward contracts, FX swaps—and pricing/subcontracting in stable currencies (USD, EUR) are essential; in 2024 many energy firms hedged ~40–60% of near-term exposure.

- USD moves of 5–10% in 2024 materially shift reported revenue

Energy services squeezed: Brent rebound vs inflation, alloy costs and FX hit margins

Expro’s revenue and margins closely track Brent/WTI—Brent avg $86/bbl in 2024, ~$95–110 in late‑2025—driving capex and service mix; 2024–25 volatility cut new well forecasts ~5–8% and Asia‑Pacific E&P capex fell 12% in 2024. Inflation (CPI ~5.8% in 2024) and alloy cost spikes (+18–25%) pressured BOM; H2‑24 contracts added 4–7% escalation. FX: USD strengthened ~8% vs LATAM in 2024; global rates elevated (Fed ~5.25–5.50%, ECB ~3.75–4.00%).

| Metric | 2024/late‑2025 |

|---|---|

| Brent | $86 avg (2024); $95–110 (late‑2025) |

| New well forecasts | -5–8% |

| Asia‑Pacific E&P capex | -12% (2024) |

| CPI / input inflation | 5.8% / manufacturing inputs +12% (2024) |

| Alloy costs | +18–25% (2024) |

| Contract escalations | 4–7% (H2‑24) |

| USD moves | +8% vs LATAM (2024) |

| Policy rates | Fed 5.25–5.50%, ECB 3.75–4.00% (late‑2025) |

Full Version Awaits

Expro PESTLE Analysis

The preview shown here is the exact Expro PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now are exactly what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, regulatory pressures, and technological advances are reshaping Expro’s prospects in our concise PESTLE snapshot—perfect for investors and strategists seeking a quick edge. Purchase the full PESTLE for a complete, actionable breakdown that highlights risks, opportunities, and strategic implications you can use immediately.

Political factors

Geopolitical instability in energy regions

Ongoing conflicts and diplomatic tensions in key oil-producing regions like the Middle East and Eastern Europe continue to disrupt supply chains and operational safety as of late 2025, with IEA reporting a 2.3% drop in regional crude exports year‑on‑year and insurers raising premiums by ~18% for operations in high‑risk zones.

Expro must navigate shifting alliances and potential sanctions that constrained services to Russia in 2024–25, forcing reallocation of ~12% of its subsea and well intervention capacity to alternative markets.

Political volatility often necessitates rapid relocation of assets and personnel to more stable jurisdictions, increasing logistics and standby costs by an estimated $8–12 million annually for mid‑sized service providers.

Energy security and independence policies

Resource nationalism and local content requirements

Governments in emerging markets are tightening local content laws, with Angola and Nigeria increasing local hiring and procurement mandates to 60-70% by 2025, forcing Expro to partner with domestic firms and source local talent to retain contracts.

Expro must balance its global safety and technical standards with national mandates—noncompliance risks license suspension, as seen in 2023 when Brazil fined foreign contractors over local content breaches totaling over $250m.

Failure to adapt could restrict market access and cost Expro significant revenue: in 2024 regional contract losses for oilfield service firms reached an estimated $1.8bn due to resource nationalism enforcement.

Global trade tariffs and protectionism

The 2025 trade environment features heightened tariffs and non-tariff barriers that disrupt movement of specialized oilfield equipment and technology, with US-China tariffs still adding up to 10–25% on relevant components and average EU safeguard duties rising 5% year-on-year.

These duty changes have pushed Expro’s capital expenditure per major well tool program up an estimated 8–12% and extended lead times by 6–10 weeks, increasing project financing needs.

Strategic planning must model tariff volatility, hedging import costs and reallocating supply chains to protect international margins and maintain competitive tender pricing.

- Tariff impact: +8–12% capex; lead times +6–10 weeks

Impact of international climate agreements

Political commitments under COP26/27 accelerate decommissioning and tighten rules on carbon-heavy extraction, with 130+ countries submitting net-zero targets by 2025 pressuring faster asset retirements and stricter permits.

Governments’ net-zero pledges drive demand for well integrity and leak-detection services; methane-focused regulations (e.g., EU methane Pledge cutting emissions 30% by 2030) favor Expro’s monitoring offerings.

Regulatory shifts force Expro to pivot toward decarbonization-aligned services, impacting CAPEX allocation as operators redirect an estimated 5–10% of project spend to emissions control technologies.

- COP commitments increase decommissioning and permit strictness

- Net-zero targets boost demand for leak detection and integrity services

- Estimated 5–10% reallocation of project CAPEX to emissions controls

Geopolitics, sanctions surge costs and reshuffle supplies as rigs, subsidies and local content rise

Geopolitical conflicts and sanctions in 2024–25 cut regional crude exports ~2.3% and forced reallocation of ~12% of Expro’s subsea capacity, raising insurance and logistics costs; Western energy security programs (+12% regional rig activity mid‑2025) and $40–60bn subsidies sustain demand for flow management; local content rules (60–70% in Angola/Nigeria) and tariffs (+8–12% capex, lead times +6–10 weeks) increase compliance and supply‑chain costs.

| Metric | Value |

|---|---|

| Regional crude export change (IEA) | -2.3% (2024–25) |

| Reallocated subsea capacity | ~12% |

| Rig activity (mid‑2025) | +12% YoY |

| Subsidies to local production | $40–60bn (2024–25) |

| Local content mandates (Angola/Nigeria) | 60–70% (2025) |

| Tariff impact on capex | +8–12% |

| Lead time increases | +6–10 weeks |

What is included in the product

Explores how macro-environmental factors uniquely affect Expro across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and localized market/regulatory context to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Expro's PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation and easy drop-in to presentations or planning sessions.

Economic factors

Fluctuations in global crude oil prices

Expro’s revenue is highly sensitive to Brent and WTI prices, which dictate E&P capex; Brent averaged about $86/bbl in 2024 and rose toward $95–$110/bbl in late 2025 amid OPEC+ cuts, boosting client drilling budgets.

Price volatility from OPEC+ decisions and demand shifts reduced new well forecasts by ~5–8% in 2024–25, directly affecting project volume for Expro.

High prices increase demand for Expro’s optimization and completion services, while sub-$70 Brent periods shift clients to lower-cost well intervention and maintenance work.

Inflationary pressure on operational costs

Persistent inflation through 2025 raised input costs for energy service providers—global manufacturing input prices rose ~12% in 2024 and CPI averaged 5.8%—forcing Expro to absorb higher prices for raw materials, specialized labor and logistics.

To protect margins, Expro is pursuing contract price escalations and internal efficiency drives; recent H2 2024 contracts included average 4–7% escalation clauses in new service agreements.

Manufacturing high-spec subsea well access systems is especially exposed: prices for nickel and titanium alloys spiked 18–25% in 2024, increasing BOM costs and pressuring gross margins.

Interest rate environment and capital access

As of late 2025 global policy rates remain elevated versus pre-2022 norms, with the US Fed funds target near 5.25–5.50% and ECB rates around 3.75–4.00%, raising corporate borrowing costs and pushing average global loan spreads for energy projects higher by ~150–200bps versus 2021, which can postpone offshore CAPEX and curb demand for Expro’s long-cycle well construction services.

Global economic growth and energy demand

The pace of industrial recovery in India and Southeast Asia—IMF 2025 growth forecasts of 6.5% for India and 4.6% for ASEAN-5—supports rising hydrocarbon demand, benefiting Expro where deepwater exploration expands to meet local energy needs.

Expro’s regional growth is cyclical; project deferrals during slowdowns can hit exploration/appraisal revenues—E&P capex in Asia-Pacific fell 12% in 2024, signaling risk to near-term orderbooks.

- India GDP 2025 est 6.5%

- ASEAN-5 2025 est 4.6%

- Asia-Pacific E&P capex down 12% in 2024

- Deepwater projects drive Expro exposure

Currency exchange rate volatility

As a multinational, Expro faces material foreign exchange risk: the US dollar strengthened ~8% vs major Latin American currencies and ~6% vs several West African currencies in 2024, which can compress reported international earnings when converted to USD.

Maintaining hedging programs—forward contracts, FX swaps—and pricing/subcontracting in stable currencies (USD, EUR) are essential; in 2024 many energy firms hedged ~40–60% of near-term exposure.

- USD moves of 5–10% in 2024 materially shift reported revenue

Energy services squeezed: Brent rebound vs inflation, alloy costs and FX hit margins

Expro’s revenue and margins closely track Brent/WTI—Brent avg $86/bbl in 2024, ~$95–110 in late‑2025—driving capex and service mix; 2024–25 volatility cut new well forecasts ~5–8% and Asia‑Pacific E&P capex fell 12% in 2024. Inflation (CPI ~5.8% in 2024) and alloy cost spikes (+18–25%) pressured BOM; H2‑24 contracts added 4–7% escalation. FX: USD strengthened ~8% vs LATAM in 2024; global rates elevated (Fed ~5.25–5.50%, ECB ~3.75–4.00%).

| Metric | 2024/late‑2025 |

|---|---|

| Brent | $86 avg (2024); $95–110 (late‑2025) |

| New well forecasts | -5–8% |

| Asia‑Pacific E&P capex | -12% (2024) |

| CPI / input inflation | 5.8% / manufacturing inputs +12% (2024) |

| Alloy costs | +18–25% (2024) |

| Contract escalations | 4–7% (H2‑24) |

| USD moves | +8% vs LATAM (2024) |

| Policy rates | Fed 5.25–5.50%, ECB 3.75–4.00% (late‑2025) |

Full Version Awaits

Expro PESTLE Analysis

The preview shown here is the exact Expro PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible now are exactly what you’ll download immediately after payment.