EXp World Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

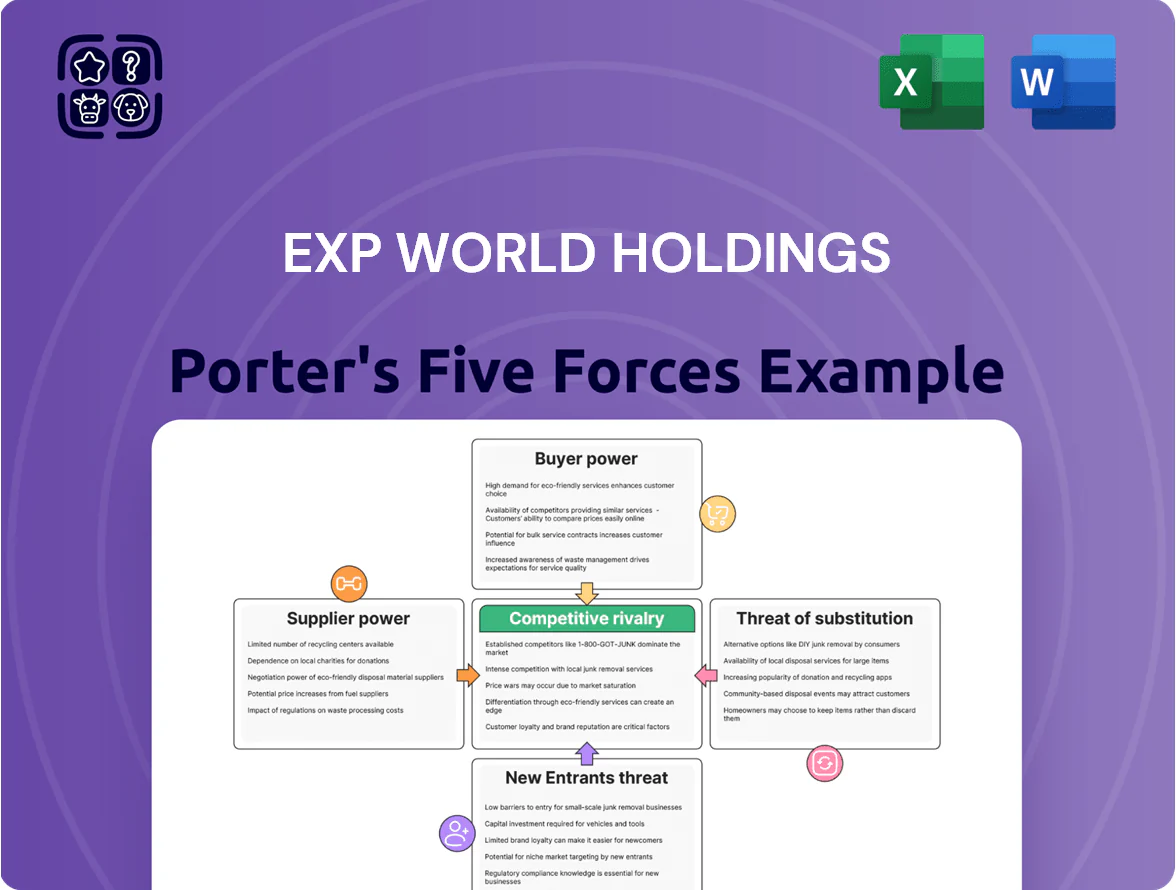

EXp World Holdings operates in a rapidly evolving virtual services and proptech ecosystem where network effects and scale drive competitive advantage, but low switching costs and emerging substitutes keep margins under pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EXp World Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Agent Labor and Talent Retention

Real estate agents are eXp Realty’s primary labor and revenue source; as of Q3 2025 eXp reported ~86,000 agents worldwide, who generate over 90% of sales volume.

Top 5% of agents—responsible for ~45% of production—hold outsized leverage and can jump to rival cloud or hybrid brokers offering higher splits.

To retain talent eXp must tweak revenue-share and equity plans; in 2024-25 the company issued ~$200M in agent-focused equity incentives to limit attrition.

Cloud Infrastructure and Technology Vendors

The company depends on third-party cloud providers to run its Virbela-based virtual campus, while Virbela supplies the app layer; major cloud firms (AWS, Microsoft Azure, Google Cloud) control roughly 60–70% of global cloud IaaS as of 2025, giving them moderate leverage over pricing and SLAs that can squeeze eXp World Holdings’ gross margins—cloud spend variability moved similar SaaS peers’ margins by 100–300 basis points in 2024.

Access to Proprietary Real Estate Data

Multiple Listing Services (MLS) and data aggregators control property feeds that drive agent productivity; in 2024 over 600 US MLSs handled 90% of residential listings, so access is essential. eXp World Holdings, despite 87,000 agents in 2025, depends on localized MLS feeds and regional vendors to power its transaction platform. A 10–25% hike in MLS or aggregator fees—or tighter regional MLS rules—would raise eXp’s per-transaction overhead and compress gross margins. In 2024 some large MLS fee changes increased broker costs by mid-single digits, showing direct P&L sensitivity.

Lead Generation and Marketing Platforms

Third-party lead platforms like Zillow and Google remain essential for eXp agents; Zillow had ~217 million monthly visits in 2024 and Google Search drove ~60% of real-estate lead queries in 2023, giving them leverage to raise ad CPCs and shift algorithm rankings.

Higher platform fees compress agent margins and, since eXp’s revenue growth depends on recruiting and retaining productive agents, these gatekeepers exert continuous pricing pressure on the firm.

- Zillow ~217M monthly visits (2024)

- Google ~60% of real-estate search share (2023)

- Rising CPCs reduce agent profitability and eXp revenue growth

Regulatory and Licensing Compliance Bodies

Regulatory and licensing agencies function as mandatory suppliers, setting the legal framework for eXp World Holdings’ brokerage operations; in 2025 eXp reports operations in 22 countries, so regulatory reach is broad.

Shifts in licensing rules or higher compliance fees—often rising 5–15% annually in key markets—raise operating costs and compress margin per agent.

Global expansion increases the number of distinct regulatory suppliers, complicating efforts to standardize cost-to-serve and raising one-off setup costs (often $50k–$200k per new market).

- Mandatory suppliers: state and international regulators

- Compliance fee inflation: ~5–15% in major markets

- eXp presence: 22 countries (2025)

- New-market setup: $50k–$200k typical

Concentrated suppliers (agents, cloud, platforms) drive pricing, traffic & compliance risk

Suppliers (agents, cloud providers, MLS/data platforms, lead sites, regulators) exert moderate-to-high bargaining power: top 5% of agents drive ~45% production; cloud vendors control ~60–70% IaaS (2025); Zillow ~217M monthly visits (2024); Google ~60% search share (2023); eXp in 22 countries (2025).

| Supplier | Key metric | Impact |

|---|---|---|

| Top agents | Top 5% → ~45% production | High attrition risk |

| Cloud IaaS | 60–70% market share (2025) | Pricing/SLA pressure |

| Zillow | 217M monthly visits (2024) | Lead cost control |

| ~60% search share (2023) | Traffic dependency | |

| Regulators | 22 countries (2025) | Compliance costs |

What is included in the product

Tailored exclusively for eXp World Holdings, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its pricing, profitability, and market position.

One-sheet Porter's Five Forces summary tailored for EXp World Holdings—quickly spot where competitive pressures threaten growth and where strategic moves can relieve pain.

Customers Bargaining Power

Home Buyer and Seller Price Sensitivity

End consumers grew more price-sensitive after 2024–2025 broker commission settlements; 2025 surveys show 62% of US buyers now shop agents by fee, up from 41% in 2022 (NAR internal consumer study, 2025).

That shift lets buyers and sellers push commissions down, cutting gross commission income for eXp agents—eXp reported a 7% decline in average agent GCI per agent in FY2025 vs FY2024 (eXp World Holdings 2025 10-K).

eXp must prove clear ROI—faster listings, digital marketing, lower transaction costs—to defend fees in a market where 68% of sellers cite fee as top switching factor (2025 Redfin consumer pulse).

Agent Mobility and Platform Switching

In the eXp ecosystem agents are internal customers who pay for platform and brand access; in 2024 eXp reported 86,000 agents, highlighting scale but also exposure to churn.

Switching costs between cloud brokerages remain low—teams can migrate digitally with minimal disruption—so agent mobility is high.

High mobility forces eXp to invest in service and tech; eXp spent $160M on technology and support in 2024 to retain agents.

Demand for Virtual and Remote Services

Corporate clients and educational institutions using Virbela demand immersive, low-latency experiences and seamless collaboration; 2024 surveys show 62% of enterprises rate custom integrations and security as top purchase drivers, giving B2B buyers strong leverage. These customers can insist on bespoke features and SOC 2/ISO 27001 controls, often choosing specialized enterprise platforms instead of eXp. If Virbela’s environment lags corporate innovation or uptime (target 99.9%), clients can switch to other metaverse or video-conferencing vendors rapidly.

Institutional Investor Influence

Large institutional investors and REITs negotiate bulk discounts and bespoke liquidation fees; in 2024 institutional trades accounted for about 22% of US commercial transaction volume, giving them leverage to push down margins for consistent deal flow.

As eXp World Holdings expands commercial and luxury arms—revenue from commercial listings rose ~18% year-over-year in 2024—these buyers’ negotiating power grows, pressuring commission rates and service fees.

Here’s the quick math: a 1% commission concession on a $200M portfolio cuts revenue by $2M; that scales with repeat institutional volume.

- 2024: institutions ≈22% of US commercial volume

- eXp commercial revenue +18% YoY (2024)

- 1% fee cut on $200M = $2M revenue loss

Access to Transparent Market Information

The rise of proptech gives buyers and sellers near-instant access to listings, transaction history, and price comps, eroding brokers’ information edge and boosting customer bargaining power.

Consumers now demand real-time feeds and analytics; eXp World Holdings (eXp World Holdings, Inc., NASDAQ: EXPI) must keep investing in consumer-facing tech—its $230M 2024 R&D and platform spend shows this pressure.

Fee-Focused Buyers Shift Power — eXp GCI Down 7% as Tech Spend Ramps

Buyers and agents gained price leverage after 2024–25 commission settlements; 2025 surveys: 62% shop agents by fee, 68% of sellers cite fee as top switching factor, and eXp saw 7% drop in GCI/agent FY2025 vs FY2024 (NAR; Redfin; eXp 2025 10-K). Low switching costs, 86k agents (2024), $160M tech spend (2024), and rising proptech (7–9% CAGR 2021–25) push eXp to invest to retain clients.

| Metric | Value |

|---|---|

| Agents (2024) | 86,000 |

| GCI change (FY2025 vs FY2024) | -7% |

| Buyers shop by fee (2025) | 62% |

| Sellers cite fee (2025) | 68% |

| eXp tech/support spend (2024) | $160M |

| eXp R&D/platform spend (2024) | $230M |

| Proptech CAGR (2021–25) | 7–9% |

Same Document Delivered

EXp World Holdings Porter's Five Forces Analysis

This preview shows the exact EXp World Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed is the final, fully formatted file ready for download and use the moment you buy.

No samples or excerpts: what you see here is precisely the deliverable you’ll get—instant access, professionally prepared.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

EXp World Holdings operates in a rapidly evolving virtual services and proptech ecosystem where network effects and scale drive competitive advantage, but low switching costs and emerging substitutes keep margins under pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EXp World Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Agent Labor and Talent Retention

Real estate agents are eXp Realty’s primary labor and revenue source; as of Q3 2025 eXp reported ~86,000 agents worldwide, who generate over 90% of sales volume.

Top 5% of agents—responsible for ~45% of production—hold outsized leverage and can jump to rival cloud or hybrid brokers offering higher splits.

To retain talent eXp must tweak revenue-share and equity plans; in 2024-25 the company issued ~$200M in agent-focused equity incentives to limit attrition.

Cloud Infrastructure and Technology Vendors

The company depends on third-party cloud providers to run its Virbela-based virtual campus, while Virbela supplies the app layer; major cloud firms (AWS, Microsoft Azure, Google Cloud) control roughly 60–70% of global cloud IaaS as of 2025, giving them moderate leverage over pricing and SLAs that can squeeze eXp World Holdings’ gross margins—cloud spend variability moved similar SaaS peers’ margins by 100–300 basis points in 2024.

Access to Proprietary Real Estate Data

Multiple Listing Services (MLS) and data aggregators control property feeds that drive agent productivity; in 2024 over 600 US MLSs handled 90% of residential listings, so access is essential. eXp World Holdings, despite 87,000 agents in 2025, depends on localized MLS feeds and regional vendors to power its transaction platform. A 10–25% hike in MLS or aggregator fees—or tighter regional MLS rules—would raise eXp’s per-transaction overhead and compress gross margins. In 2024 some large MLS fee changes increased broker costs by mid-single digits, showing direct P&L sensitivity.

Lead Generation and Marketing Platforms

Third-party lead platforms like Zillow and Google remain essential for eXp agents; Zillow had ~217 million monthly visits in 2024 and Google Search drove ~60% of real-estate lead queries in 2023, giving them leverage to raise ad CPCs and shift algorithm rankings.

Higher platform fees compress agent margins and, since eXp’s revenue growth depends on recruiting and retaining productive agents, these gatekeepers exert continuous pricing pressure on the firm.

- Zillow ~217M monthly visits (2024)

- Google ~60% of real-estate search share (2023)

- Rising CPCs reduce agent profitability and eXp revenue growth

Regulatory and Licensing Compliance Bodies

Regulatory and licensing agencies function as mandatory suppliers, setting the legal framework for eXp World Holdings’ brokerage operations; in 2025 eXp reports operations in 22 countries, so regulatory reach is broad.

Shifts in licensing rules or higher compliance fees—often rising 5–15% annually in key markets—raise operating costs and compress margin per agent.

Global expansion increases the number of distinct regulatory suppliers, complicating efforts to standardize cost-to-serve and raising one-off setup costs (often $50k–$200k per new market).

- Mandatory suppliers: state and international regulators

- Compliance fee inflation: ~5–15% in major markets

- eXp presence: 22 countries (2025)

- New-market setup: $50k–$200k typical

Concentrated suppliers (agents, cloud, platforms) drive pricing, traffic & compliance risk

Suppliers (agents, cloud providers, MLS/data platforms, lead sites, regulators) exert moderate-to-high bargaining power: top 5% of agents drive ~45% production; cloud vendors control ~60–70% IaaS (2025); Zillow ~217M monthly visits (2024); Google ~60% search share (2023); eXp in 22 countries (2025).

| Supplier | Key metric | Impact |

|---|---|---|

| Top agents | Top 5% → ~45% production | High attrition risk |

| Cloud IaaS | 60–70% market share (2025) | Pricing/SLA pressure |

| Zillow | 217M monthly visits (2024) | Lead cost control |

| ~60% search share (2023) | Traffic dependency | |

| Regulators | 22 countries (2025) | Compliance costs |

What is included in the product

Tailored exclusively for eXp World Holdings, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its pricing, profitability, and market position.

One-sheet Porter's Five Forces summary tailored for EXp World Holdings—quickly spot where competitive pressures threaten growth and where strategic moves can relieve pain.

Customers Bargaining Power

Home Buyer and Seller Price Sensitivity

End consumers grew more price-sensitive after 2024–2025 broker commission settlements; 2025 surveys show 62% of US buyers now shop agents by fee, up from 41% in 2022 (NAR internal consumer study, 2025).

That shift lets buyers and sellers push commissions down, cutting gross commission income for eXp agents—eXp reported a 7% decline in average agent GCI per agent in FY2025 vs FY2024 (eXp World Holdings 2025 10-K).

eXp must prove clear ROI—faster listings, digital marketing, lower transaction costs—to defend fees in a market where 68% of sellers cite fee as top switching factor (2025 Redfin consumer pulse).

Agent Mobility and Platform Switching

In the eXp ecosystem agents are internal customers who pay for platform and brand access; in 2024 eXp reported 86,000 agents, highlighting scale but also exposure to churn.

Switching costs between cloud brokerages remain low—teams can migrate digitally with minimal disruption—so agent mobility is high.

High mobility forces eXp to invest in service and tech; eXp spent $160M on technology and support in 2024 to retain agents.

Demand for Virtual and Remote Services

Corporate clients and educational institutions using Virbela demand immersive, low-latency experiences and seamless collaboration; 2024 surveys show 62% of enterprises rate custom integrations and security as top purchase drivers, giving B2B buyers strong leverage. These customers can insist on bespoke features and SOC 2/ISO 27001 controls, often choosing specialized enterprise platforms instead of eXp. If Virbela’s environment lags corporate innovation or uptime (target 99.9%), clients can switch to other metaverse or video-conferencing vendors rapidly.

Institutional Investor Influence

Large institutional investors and REITs negotiate bulk discounts and bespoke liquidation fees; in 2024 institutional trades accounted for about 22% of US commercial transaction volume, giving them leverage to push down margins for consistent deal flow.

As eXp World Holdings expands commercial and luxury arms—revenue from commercial listings rose ~18% year-over-year in 2024—these buyers’ negotiating power grows, pressuring commission rates and service fees.

Here’s the quick math: a 1% commission concession on a $200M portfolio cuts revenue by $2M; that scales with repeat institutional volume.

- 2024: institutions ≈22% of US commercial volume

- eXp commercial revenue +18% YoY (2024)

- 1% fee cut on $200M = $2M revenue loss

Access to Transparent Market Information

The rise of proptech gives buyers and sellers near-instant access to listings, transaction history, and price comps, eroding brokers’ information edge and boosting customer bargaining power.

Consumers now demand real-time feeds and analytics; eXp World Holdings (eXp World Holdings, Inc., NASDAQ: EXPI) must keep investing in consumer-facing tech—its $230M 2024 R&D and platform spend shows this pressure.

Fee-Focused Buyers Shift Power — eXp GCI Down 7% as Tech Spend Ramps

Buyers and agents gained price leverage after 2024–25 commission settlements; 2025 surveys: 62% shop agents by fee, 68% of sellers cite fee as top switching factor, and eXp saw 7% drop in GCI/agent FY2025 vs FY2024 (NAR; Redfin; eXp 2025 10-K). Low switching costs, 86k agents (2024), $160M tech spend (2024), and rising proptech (7–9% CAGR 2021–25) push eXp to invest to retain clients.

| Metric | Value |

|---|---|

| Agents (2024) | 86,000 |

| GCI change (FY2025 vs FY2024) | -7% |

| Buyers shop by fee (2025) | 62% |

| Sellers cite fee (2025) | 68% |

| eXp tech/support spend (2024) | $160M |

| eXp R&D/platform spend (2024) | $230M |

| Proptech CAGR (2021–25) | 7–9% |

Same Document Delivered

EXp World Holdings Porter's Five Forces Analysis

This preview shows the exact EXp World Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed is the final, fully formatted file ready for download and use the moment you buy.

No samples or excerpts: what you see here is precisely the deliverable you’ll get—instant access, professionally prepared.