Extra Space Storage Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

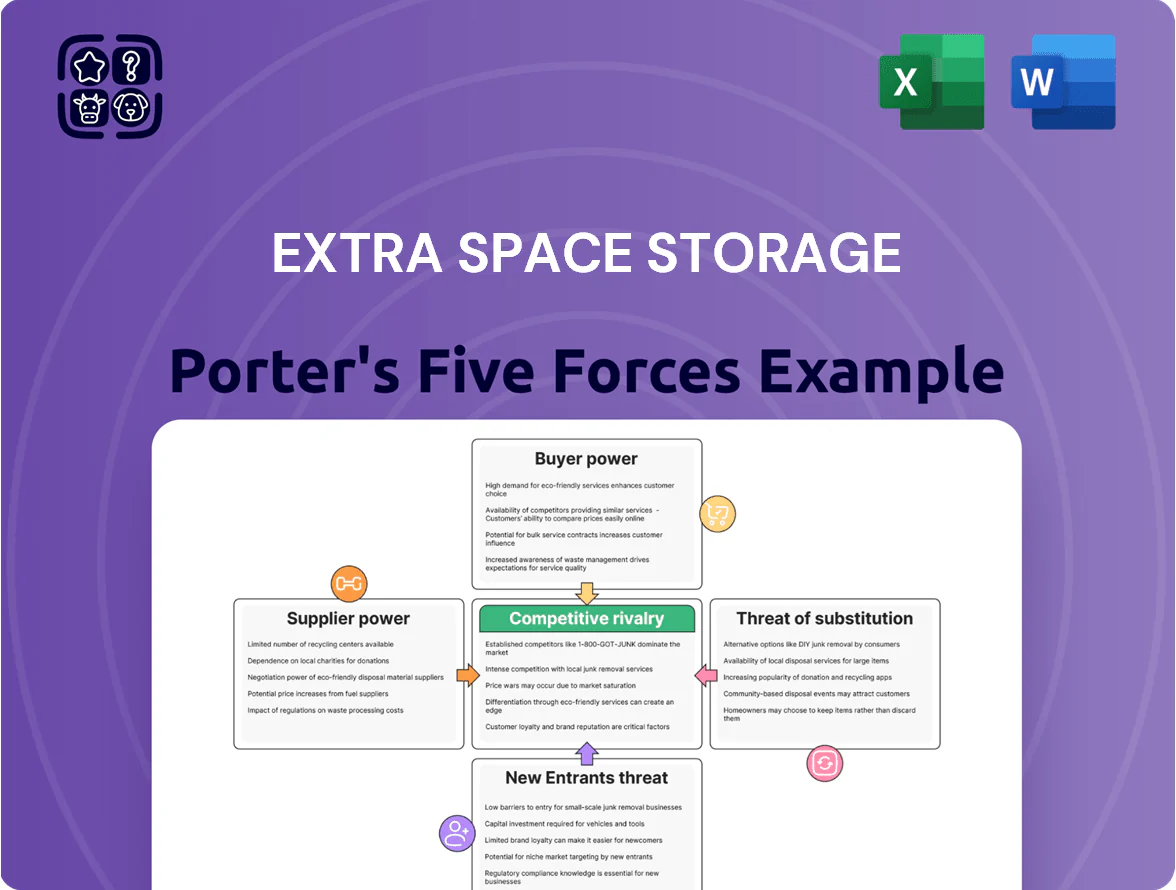

Extra Space Storage faces moderate buyer power, steady supplier influence, and a high rivalry among established REITs and local operators, while barriers to entry temper new competition and substitutes pose limited disruption—yet location and operational efficiency remain decisive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Extra Space Storage’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Land Acquisition and Real Estate Developers

Landowners and real estate developers set prices that drive Extra Space Storage’s development costs and site feasibility.

In 2025, prime urban sites are scarce: land values in top MSAs rose ~12% YoY, boosting seller leverage and acquisition premiums.

Extra Space faces bidding pressure from institutional investors and residential builders, raising per-site acquisition costs and capex needed to protect market share.

Construction and Labor Providers

The cost of steel, concrete and HVAC drives capital expenditure efficiency for climate-controlled facilities, with construction/materials inflation up ~14% from 2020–2024 and HVAC backlog adding ~6–9% to project timelines in 2024.

Suppliers hold moderate bargaining power due to global supply-chain shifts and 2023–2024 commodity volatility, but not dominant pricing power.

Extra Space Storage (EXR) offsets this by using scale—over 1,900 owned locations and $2.5B+ development pipeline in 2024—to secure volume contracts and lower per-unit build costs.

Technology and Software Vendors

PropTech and management software vendors are critical to Extra Space Storage’s ops, powering online rentals, automated gates, and AI pricing; 2024 surveys show 62% of US self-storage operators adopted dynamic pricing tools, raising SaaS spend ~8–12% of IT budgets.

Third-party Management Partners

Extra Space Storage manages ~2,200 third-party properties, generating ~15% of 2024 revenue through management fees; owners can switch platforms if occupancy or RevPAU (revenue per available unit) lags or fees rise.

Keeping occupancy above 92% and market-rate rental growth (3–6% annually in 2024) is vital to retain portfolios and protect ~$200M annual fee income.

- Third-party supply: ~2,200 properties

- Fee revenue: ~15% of 2024 total (~$200M)

- Retention trigger: occupancy <92% or weak RevPAU

- Target rent growth: 3–6% in 2024

Capital and Financial Institutions

As a REIT, Extra Space Storage depends heavily on banks and bondholders for acquisitions and refinancing; at 12/31/2025 its net debt/EBITDA was 5.1x and its S&P rating was BBB, which raises supplier leverage when rates climb.

Prevailing interest rates in 2025 averaged ~5.0% for 10‑yr treasuries; access to sub-5% unsecured/secured financing gives Extra Space a bidding edge over smaller, higher‑cost rivals.

- Net debt/EBITDA 5.1x (12/31/2025)

- S&P rating BBB (2025)

- 10‑yr Treasury ~5.0% (2025 avg)

- Low‑cost capital enables higher bid capacity

Scale and capital buffer EXR vs rising land and materials costs

Suppliers exert moderate power: land scarcity and 12% YoY MSA land value gains in 2025 and 14% materials inflation (2020–24) raise site and capex costs, but EXR’s scale (1,900+ owned sites, $2.5B development pipeline in 2024) and access to capital (net debt/EBITDA 5.1x, S&P BBB, 10‑yr ~5.0% in 2025) limit supplier pricing control.

| Metric | Value |

|---|---|

| Owned sites | 1,900+ |

| Dev pipeline | $2.5B (2024) |

| Land value change | +12% YoY (2025) |

| Materials inflation | +14% (2020–24) |

| Net debt/EBITDA | 5.1x (12/31/2025) |

| S&P rating | BBB (2025) |

| 10‑yr Treasury | ~5.0% (2025 avg) |

What is included in the product

Tailored Porter's Five Forces analysis for Extra Space Storage, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic vulnerabilities to inform investor and management decisions.

Clear, one-sheet Porter's Five Forces for Extra Space Storage—instantly spot competitive pressures and use the clean layout in decks or dashboards for faster, board-ready decisions.

Customers Bargaining Power

Low Switching Costs for Renters

Individual renters face low switching costs because month-to-month leases dominate self-storage, letting customers move if a competitor offers a better promo or closer site; Extra Space Storage reported 2024 same-store occupancy of 91.1%, so retention is key.

To offset churn, Extra Space invests in service and upkeep—2024 capital expenditures were $154.6 million—to keep facilities clean, secure, and convenient, which reduces defections despite price-sensitive renters.

Price Transparency and Digital Comparison

Online aggregators and apps let renters compare unit prices and features in real time within a radius, raising price transparency and consumer price sensitivity; a 2024 JLL report found 62% of renters used comparison tools before booking. This makes rent hikes harder without clear value. Extra Space Storage (EXR) counters with dynamic pricing algorithms that lifted 2024 revenue per available square foot (RevPAF) by ~4.5%, keeping occupancy near 95%.

Localized Market Concentration

Customer bargaining rises with storage density: studies show demand elasticity increases when 3–5 competing facilities exist within a three-mile radius, and in metro areas where Extra Space Storage (EXR) faces 4+ competitors occupancy can drop 2–4 percentage points unless pricing is competitive.

Where national and local brands cluster, renters extract move-in specials; industry data from 2024 show average promotional discounts reached 12% in highly concentrated markets.

EXR counters by choosing high-traffic sites near retail and transit; convenience explains why 62% of renters rank location as their top factor, letting EXR maintain premium rates and limit churn.

Commercial Tenant Leverage

Commercial tenants renting multiple units or large spaces have notably higher bargaining power than residential renters; Extra Space Storage reported in 2024 that institutional/commercial accounts made up roughly 9% of revenue but contributed disproportionately to occupancy stability.

These clients push for long-term leases, custom rates, and services like enhanced security and climate monitoring, often securing discounts for scale and multi-year commitments.

Targeting this segment raises portfolio stability but requires tailored CRM, dedicated account managers, and potential capex for specialized services.

- 9% revenue from commercial accounts (2024)

- Higher renewal rates, lower churn

- Requires dedicated account teams and service capex

Brand Loyalty and Trust

Extra Space Storage’s national reputation for safety, cleanliness, and reliability reduces customer price sensitivity by offering trust that many local operators lack; in 2025 the company reports 99.3% occupancy on stabilized stores and a Net Promoter Score above industry median, reinforcing premium positioning.

This perceived reliability cushions bargaining power from price-focused shoppers, as customers place higher value on secure, well-maintained facilities when storing valuable items.

- 99.3% occupancy in stabilized stores (2025)

- Higher-than-industry NPS (2025)

- Nationwide brand reduces churn vs local competitors

EXR boosts RevPAF +4.5% and commercial focus drives 99.3% stabilized occupancy

Customers have low switching costs and high price sensitivity due to month-to-month leases and comparison apps; EXR offset this with service, dynamic pricing (RevPAF +4.5% in 2024), and focus on commercial accounts (9% revenue, 2024) to stabilize occupancy (stabilized stores 99.3% occupancy, 2025).

| Metric | Value |

|---|---|

| RevPAF change (2024) | +4.5% |

| CapEx (2024) | $154.6M |

| Commercial rev (2024) | 9% |

| Stabilized occ (2025) | 99.3% |

Preview Before You Purchase

Extra Space Storage Porter's Five Forces Analysis

This preview shows the exact Extra Space Storage Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Extra Space Storage faces moderate buyer power, steady supplier influence, and a high rivalry among established REITs and local operators, while barriers to entry temper new competition and substitutes pose limited disruption—yet location and operational efficiency remain decisive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Extra Space Storage’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Land Acquisition and Real Estate Developers

Landowners and real estate developers set prices that drive Extra Space Storage’s development costs and site feasibility.

In 2025, prime urban sites are scarce: land values in top MSAs rose ~12% YoY, boosting seller leverage and acquisition premiums.

Extra Space faces bidding pressure from institutional investors and residential builders, raising per-site acquisition costs and capex needed to protect market share.

Construction and Labor Providers

The cost of steel, concrete and HVAC drives capital expenditure efficiency for climate-controlled facilities, with construction/materials inflation up ~14% from 2020–2024 and HVAC backlog adding ~6–9% to project timelines in 2024.

Suppliers hold moderate bargaining power due to global supply-chain shifts and 2023–2024 commodity volatility, but not dominant pricing power.

Extra Space Storage (EXR) offsets this by using scale—over 1,900 owned locations and $2.5B+ development pipeline in 2024—to secure volume contracts and lower per-unit build costs.

Technology and Software Vendors

PropTech and management software vendors are critical to Extra Space Storage’s ops, powering online rentals, automated gates, and AI pricing; 2024 surveys show 62% of US self-storage operators adopted dynamic pricing tools, raising SaaS spend ~8–12% of IT budgets.

Third-party Management Partners

Extra Space Storage manages ~2,200 third-party properties, generating ~15% of 2024 revenue through management fees; owners can switch platforms if occupancy or RevPAU (revenue per available unit) lags or fees rise.

Keeping occupancy above 92% and market-rate rental growth (3–6% annually in 2024) is vital to retain portfolios and protect ~$200M annual fee income.

- Third-party supply: ~2,200 properties

- Fee revenue: ~15% of 2024 total (~$200M)

- Retention trigger: occupancy <92% or weak RevPAU

- Target rent growth: 3–6% in 2024

Capital and Financial Institutions

As a REIT, Extra Space Storage depends heavily on banks and bondholders for acquisitions and refinancing; at 12/31/2025 its net debt/EBITDA was 5.1x and its S&P rating was BBB, which raises supplier leverage when rates climb.

Prevailing interest rates in 2025 averaged ~5.0% for 10‑yr treasuries; access to sub-5% unsecured/secured financing gives Extra Space a bidding edge over smaller, higher‑cost rivals.

- Net debt/EBITDA 5.1x (12/31/2025)

- S&P rating BBB (2025)

- 10‑yr Treasury ~5.0% (2025 avg)

- Low‑cost capital enables higher bid capacity

Scale and capital buffer EXR vs rising land and materials costs

Suppliers exert moderate power: land scarcity and 12% YoY MSA land value gains in 2025 and 14% materials inflation (2020–24) raise site and capex costs, but EXR’s scale (1,900+ owned sites, $2.5B development pipeline in 2024) and access to capital (net debt/EBITDA 5.1x, S&P BBB, 10‑yr ~5.0% in 2025) limit supplier pricing control.

| Metric | Value |

|---|---|

| Owned sites | 1,900+ |

| Dev pipeline | $2.5B (2024) |

| Land value change | +12% YoY (2025) |

| Materials inflation | +14% (2020–24) |

| Net debt/EBITDA | 5.1x (12/31/2025) |

| S&P rating | BBB (2025) |

| 10‑yr Treasury | ~5.0% (2025 avg) |

What is included in the product

Tailored Porter's Five Forces analysis for Extra Space Storage, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic vulnerabilities to inform investor and management decisions.

Clear, one-sheet Porter's Five Forces for Extra Space Storage—instantly spot competitive pressures and use the clean layout in decks or dashboards for faster, board-ready decisions.

Customers Bargaining Power

Low Switching Costs for Renters

Individual renters face low switching costs because month-to-month leases dominate self-storage, letting customers move if a competitor offers a better promo or closer site; Extra Space Storage reported 2024 same-store occupancy of 91.1%, so retention is key.

To offset churn, Extra Space invests in service and upkeep—2024 capital expenditures were $154.6 million—to keep facilities clean, secure, and convenient, which reduces defections despite price-sensitive renters.

Price Transparency and Digital Comparison

Online aggregators and apps let renters compare unit prices and features in real time within a radius, raising price transparency and consumer price sensitivity; a 2024 JLL report found 62% of renters used comparison tools before booking. This makes rent hikes harder without clear value. Extra Space Storage (EXR) counters with dynamic pricing algorithms that lifted 2024 revenue per available square foot (RevPAF) by ~4.5%, keeping occupancy near 95%.

Localized Market Concentration

Customer bargaining rises with storage density: studies show demand elasticity increases when 3–5 competing facilities exist within a three-mile radius, and in metro areas where Extra Space Storage (EXR) faces 4+ competitors occupancy can drop 2–4 percentage points unless pricing is competitive.

Where national and local brands cluster, renters extract move-in specials; industry data from 2024 show average promotional discounts reached 12% in highly concentrated markets.

EXR counters by choosing high-traffic sites near retail and transit; convenience explains why 62% of renters rank location as their top factor, letting EXR maintain premium rates and limit churn.

Commercial Tenant Leverage

Commercial tenants renting multiple units or large spaces have notably higher bargaining power than residential renters; Extra Space Storage reported in 2024 that institutional/commercial accounts made up roughly 9% of revenue but contributed disproportionately to occupancy stability.

These clients push for long-term leases, custom rates, and services like enhanced security and climate monitoring, often securing discounts for scale and multi-year commitments.

Targeting this segment raises portfolio stability but requires tailored CRM, dedicated account managers, and potential capex for specialized services.

- 9% revenue from commercial accounts (2024)

- Higher renewal rates, lower churn

- Requires dedicated account teams and service capex

Brand Loyalty and Trust

Extra Space Storage’s national reputation for safety, cleanliness, and reliability reduces customer price sensitivity by offering trust that many local operators lack; in 2025 the company reports 99.3% occupancy on stabilized stores and a Net Promoter Score above industry median, reinforcing premium positioning.

This perceived reliability cushions bargaining power from price-focused shoppers, as customers place higher value on secure, well-maintained facilities when storing valuable items.

- 99.3% occupancy in stabilized stores (2025)

- Higher-than-industry NPS (2025)

- Nationwide brand reduces churn vs local competitors

EXR boosts RevPAF +4.5% and commercial focus drives 99.3% stabilized occupancy

Customers have low switching costs and high price sensitivity due to month-to-month leases and comparison apps; EXR offset this with service, dynamic pricing (RevPAF +4.5% in 2024), and focus on commercial accounts (9% revenue, 2024) to stabilize occupancy (stabilized stores 99.3% occupancy, 2025).

| Metric | Value |

|---|---|

| RevPAF change (2024) | +4.5% |

| CapEx (2024) | $154.6M |

| Commercial rev (2024) | 9% |

| Stabilized occ (2025) | 99.3% |

Preview Before You Purchase

Extra Space Storage Porter's Five Forces Analysis

This preview shows the exact Extra Space Storage Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.