Forum Energy Technologies PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

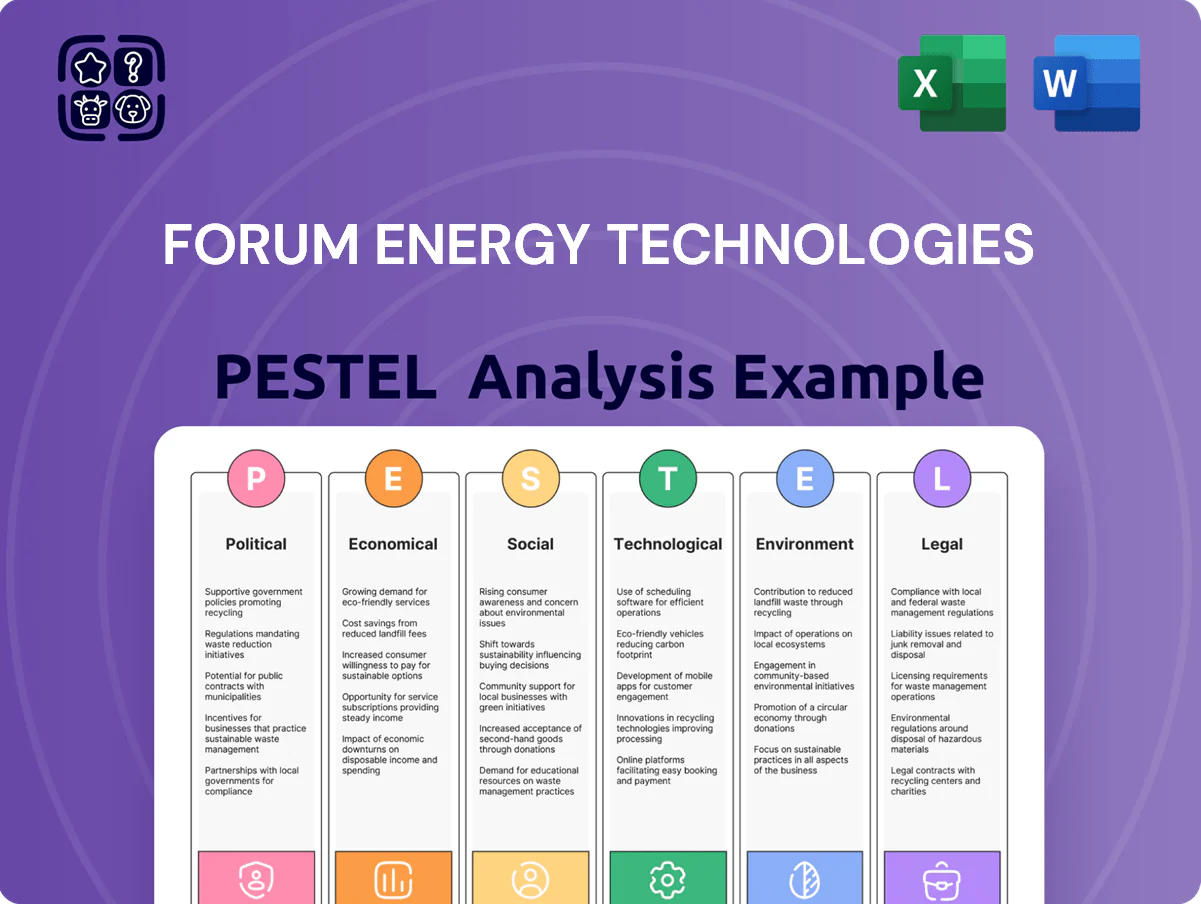

Gain a competitive edge with our PESTLE Analysis of Forum Energy Technologies—revealing how political shifts, economic cycles, regulatory changes, and technological advances shape its prospects; buy the full report to access actionable intelligence, ready-to-use charts, and strategic recommendations for investors and planners.

Political factors

Geopolitical Stability in Oil-Producing Regions

Ongoing geopolitical tensions in the Middle East and Eastern Europe as of late 2025 keep energy supply chains disrupted, contributing to oil price volatility—Brent averaged about 86 USD/bbl in 2025 YTD, up 12% year-over-year—affecting demand for drilling and subsea services. Forum Energy Technologies must navigate sanctions, trade restrictions and shifting alliance dynamics that influence contract flows and equipment exports to sensitive corridors. Political instability can trigger abrupt project delays or contract suspensions, risking revenue volatility given FET’s 2024 revenue mix with ~58% tied to upstream services.

US Federal Energy Leasing and Permitting Policies

The US political landscape affects Forum Energy through federal leasing changes: the Biden administration paused new offshore leases in 2021 but 2023 policy shifts reopened areas, influencing demand for drilling equipment; US onshore lease sales totaled 3,800 parcels in 2024, boosting service opportunities. Regulatory permit trends—pipeline approvals down 18% in 2023 vs 2022—can constrain demand for pipeline products and export terminal equipment. Forum remains exposed to administration choices that favor fossil fuel expansion or accelerate clean energy transition, impacting revenue mix and capex demand.

International Trade Tariffs and Sanctions

Trade policies and sanctions shape Forum Energy Technologies market reach; for example, US steel tariffs raised input costs by roughly 10-25% for manufacturers in recent years, affecting margins on rigs and subsea hardware. Sanctions on nations such as Russia and Iran can bar sales of specialized drilling and subsea equipment, potentially reducing addressable markets by several percentage points in affected regions. Maintaining a flexible global supply chain and dual-sourcing steel and components helped similar OEMs trim tariff-driven cost increases by ~5% and limit revenue disruption.

Energy Security and National Priorities

Governments prioritizing energy security have increased support for domestic oil and gas, boosting capital expenditure in upstream sectors by about 12% globally in 2024, aiding Forum Energy Technologies' drilling and completions revenues (FY2024 drilling-related sales up ~9%).

Forum aligns products to state-owned and independent operators, capturing demand for rugged drilling tools and completion systems as national policies favor onshore and shallow-water projects.

- Global upstream capex +12% (2024)

- FET drilling sales +9% (FY2024)

- Focus on onshore/shallow-water solutions

- Alignment with state-owned operator procurement

Government Subsidies for Energy Transition

Political incentives and subsidies for CCUS and offshore wind—such as the US IRA tax credits up to $85/ton for DAC and expanded 45V/45Y credits—are accelerating demand for energy-transition technologies, benefiting suppliers like Forum Energy Technologies seeking CCUS and turbine-related contracts.

Forum is diversifying into subsea systems and carbon-handling equipment to capture projected CCUS market growth to $6–10 billion by 2030 and >$20 billion by 2040, reducing exposure to declining hydrocarbon investments.

- US IRA/45Q expansions increase CCUS project economics; credits now exceed $85/ton for some projects

- Global offshore wind capacity reached ~85 GW in 2024, supporting subsea equipment demand

- CCUS market forecast $6–10B by 2030, >$20B by 2040

Oil volatility hits FET: upstream risk, tariffs up, CCUS offers diversification

Geopolitical tensions and sanctions drive oil price volatility (Brent ~86 USD/bbl 2025 YTD) and export restrictions, risking FET revenue (~58% upstream exposure in 2024); US lease policy and onshore parcel sales (3,800 in 2024) lift demand; tariffs raised input costs ~10–25%; IRA/45Q boosts CCUS economics (>85 USD/ton), aiding FET diversification into subsea and carbon-handling.

| Metric | Value |

|---|---|

| Brent 2025 YTD | ~86 USD/bbl |

| FET upstream rev (2024) | ~58% |

| US onshore parcels (2024) | 3,800 |

| Tariff impact | +10–25% input cost |

| IRA/45Q value | >85 USD/ton |

What is included in the product

Explores how macro-environmental factors uniquely affect Forum Energy Technologies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Concise PESTLE summary of Forum Energy Technologies that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning, risk discussions, and client reports.

Economic factors

Global Crude Oil and Natural Gas Price Volatility

Forum Energy Technologies revenue and backlog move with oil and gas prices; Brent averaged about 86 USD/bbl and Henry Hub natural gas near 3.50 USD/MMBtu in 2024, supporting higher E&P capex and stronger demand for FET drilling and subsea equipment.

When prices fell to averages near 60 USD/bbl in 2020–2022, FET saw order deferrals and reduced service hours; prolonged downturns similarly compress margins as customers cut budgets and delay purchases.

Capital Expenditure Cycles in Exploration and Production

The cyclical nature of the energy industry means FETs revenue is highly tied to operators capex cycles; global upstream capex was forecast at about $440 billion in 2025, down from peak years, constraining large equipment orders. As of end-2025 many firms balance production growth with shareholder capital discipline and dividends—US independents returned over $60 billion to shareholders in 2025—reducing discretionary spending. This balancing act compresses order volumes and shifts demand toward maintenance and life-extension services, which accounted for roughly 35% of service revenues for peers in 2025.

Interest Rate Environment and Financing Costs

The prevailing interest rate environment raises Forum Energy Technologies' cost of capital and affects its customers' project financing; US 10-year Treasury yields averaged about 4.2% in 2025 Q1, pushing corporate borrowing spreads higher. Higher rates increased debt service for Forum—long-term debt was roughly $300m in 2024—while many customers delayed CAPEX as bank lending standards tightened. As central banks targeted inflation through 2025, access to affordable credit remained critical for timing of infrastructure projects and equipment upgrades.

Inflationary Pressures on Manufacturing Inputs

Inflation raised FET manufacturing costs in 2024–2025: nickel and titanium alloys climbed 18–25% year-on-year while semiconductors saw 12% price increases, squeezing margins for subsea robotics and drilling tools.

If FET cannot fully pass costs to customers, operating margins could fall from 11% (2023) toward industry mid-single digits; strategic sourcing, hedging and selective price adjustments are required.

- Alloys +18–25% y/y (2024–25)

- Electronic components +12% y/y

- 2023 operating margin 11% — downside risk to mid-single digits

- Mitigations: strategic sourcing, hedging, selective pricing

Emerging Market Demand and Economic Growth

- 60%+ of 2024 energy demand growth from emerging markets

- Asia GDP ~4–5% (2024), Latin America ~2–3% (2024)

- Regional expansion reduces reliance on domestic cycles

Energy cycle lifts 2024 capex but inflation, rates threaten margins; EM demand surges

Energy price cycles drive FET revenue: Brent ~86 USD/bbl and Henry Hub ~3.50 USD/MMBtu in 2024 boosted capex; downturns (60 USD/bbl in 2020–22) cut orders. Inflation (alloys +18–25%, electronics +12% y/y) and higher rates (US 10y ~4.2% in 2025 Q1) raise costs and debt service; 2023 margin 11% risks mid-single digits unless pricing, hedging, sourcing mitigate; emerging markets >60% demand growth.

| Metric | Value |

|---|---|

| Brent 2024 | ~86 USD/bbl |

| Henry Hub 2024 | ~3.50 USD/MMBtu |

| Alloy price change | +18–25% y/y |

| Electronics | +12% y/y |

| US 10y (2025 Q1) | ~4.2% |

| 2023 operating margin | 11% |

| Emerging market demand | >60% |

What You See Is What You Get

Forum Energy Technologies PESTLE Analysis

The preview shown here is the exact Forum Energy Technologies PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see is the final document with real content and layout, delivered exactly as displayed with no placeholders or surprises. After checkout you’ll be able to download this same file immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of Forum Energy Technologies—revealing how political shifts, economic cycles, regulatory changes, and technological advances shape its prospects; buy the full report to access actionable intelligence, ready-to-use charts, and strategic recommendations for investors and planners.

Political factors

Geopolitical Stability in Oil-Producing Regions

Ongoing geopolitical tensions in the Middle East and Eastern Europe as of late 2025 keep energy supply chains disrupted, contributing to oil price volatility—Brent averaged about 86 USD/bbl in 2025 YTD, up 12% year-over-year—affecting demand for drilling and subsea services. Forum Energy Technologies must navigate sanctions, trade restrictions and shifting alliance dynamics that influence contract flows and equipment exports to sensitive corridors. Political instability can trigger abrupt project delays or contract suspensions, risking revenue volatility given FET’s 2024 revenue mix with ~58% tied to upstream services.

US Federal Energy Leasing and Permitting Policies

The US political landscape affects Forum Energy through federal leasing changes: the Biden administration paused new offshore leases in 2021 but 2023 policy shifts reopened areas, influencing demand for drilling equipment; US onshore lease sales totaled 3,800 parcels in 2024, boosting service opportunities. Regulatory permit trends—pipeline approvals down 18% in 2023 vs 2022—can constrain demand for pipeline products and export terminal equipment. Forum remains exposed to administration choices that favor fossil fuel expansion or accelerate clean energy transition, impacting revenue mix and capex demand.

International Trade Tariffs and Sanctions

Trade policies and sanctions shape Forum Energy Technologies market reach; for example, US steel tariffs raised input costs by roughly 10-25% for manufacturers in recent years, affecting margins on rigs and subsea hardware. Sanctions on nations such as Russia and Iran can bar sales of specialized drilling and subsea equipment, potentially reducing addressable markets by several percentage points in affected regions. Maintaining a flexible global supply chain and dual-sourcing steel and components helped similar OEMs trim tariff-driven cost increases by ~5% and limit revenue disruption.

Energy Security and National Priorities

Governments prioritizing energy security have increased support for domestic oil and gas, boosting capital expenditure in upstream sectors by about 12% globally in 2024, aiding Forum Energy Technologies' drilling and completions revenues (FY2024 drilling-related sales up ~9%).

Forum aligns products to state-owned and independent operators, capturing demand for rugged drilling tools and completion systems as national policies favor onshore and shallow-water projects.

- Global upstream capex +12% (2024)

- FET drilling sales +9% (FY2024)

- Focus on onshore/shallow-water solutions

- Alignment with state-owned operator procurement

Government Subsidies for Energy Transition

Political incentives and subsidies for CCUS and offshore wind—such as the US IRA tax credits up to $85/ton for DAC and expanded 45V/45Y credits—are accelerating demand for energy-transition technologies, benefiting suppliers like Forum Energy Technologies seeking CCUS and turbine-related contracts.

Forum is diversifying into subsea systems and carbon-handling equipment to capture projected CCUS market growth to $6–10 billion by 2030 and >$20 billion by 2040, reducing exposure to declining hydrocarbon investments.

- US IRA/45Q expansions increase CCUS project economics; credits now exceed $85/ton for some projects

- Global offshore wind capacity reached ~85 GW in 2024, supporting subsea equipment demand

- CCUS market forecast $6–10B by 2030, >$20B by 2040

Oil volatility hits FET: upstream risk, tariffs up, CCUS offers diversification

Geopolitical tensions and sanctions drive oil price volatility (Brent ~86 USD/bbl 2025 YTD) and export restrictions, risking FET revenue (~58% upstream exposure in 2024); US lease policy and onshore parcel sales (3,800 in 2024) lift demand; tariffs raised input costs ~10–25%; IRA/45Q boosts CCUS economics (>85 USD/ton), aiding FET diversification into subsea and carbon-handling.

| Metric | Value |

|---|---|

| Brent 2025 YTD | ~86 USD/bbl |

| FET upstream rev (2024) | ~58% |

| US onshore parcels (2024) | 3,800 |

| Tariff impact | +10–25% input cost |

| IRA/45Q value | >85 USD/ton |

What is included in the product

Explores how macro-environmental factors uniquely affect Forum Energy Technologies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Concise PESTLE summary of Forum Energy Technologies that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning, risk discussions, and client reports.

Economic factors

Global Crude Oil and Natural Gas Price Volatility

Forum Energy Technologies revenue and backlog move with oil and gas prices; Brent averaged about 86 USD/bbl and Henry Hub natural gas near 3.50 USD/MMBtu in 2024, supporting higher E&P capex and stronger demand for FET drilling and subsea equipment.

When prices fell to averages near 60 USD/bbl in 2020–2022, FET saw order deferrals and reduced service hours; prolonged downturns similarly compress margins as customers cut budgets and delay purchases.

Capital Expenditure Cycles in Exploration and Production

The cyclical nature of the energy industry means FETs revenue is highly tied to operators capex cycles; global upstream capex was forecast at about $440 billion in 2025, down from peak years, constraining large equipment orders. As of end-2025 many firms balance production growth with shareholder capital discipline and dividends—US independents returned over $60 billion to shareholders in 2025—reducing discretionary spending. This balancing act compresses order volumes and shifts demand toward maintenance and life-extension services, which accounted for roughly 35% of service revenues for peers in 2025.

Interest Rate Environment and Financing Costs

The prevailing interest rate environment raises Forum Energy Technologies' cost of capital and affects its customers' project financing; US 10-year Treasury yields averaged about 4.2% in 2025 Q1, pushing corporate borrowing spreads higher. Higher rates increased debt service for Forum—long-term debt was roughly $300m in 2024—while many customers delayed CAPEX as bank lending standards tightened. As central banks targeted inflation through 2025, access to affordable credit remained critical for timing of infrastructure projects and equipment upgrades.

Inflationary Pressures on Manufacturing Inputs

Inflation raised FET manufacturing costs in 2024–2025: nickel and titanium alloys climbed 18–25% year-on-year while semiconductors saw 12% price increases, squeezing margins for subsea robotics and drilling tools.

If FET cannot fully pass costs to customers, operating margins could fall from 11% (2023) toward industry mid-single digits; strategic sourcing, hedging and selective price adjustments are required.

- Alloys +18–25% y/y (2024–25)

- Electronic components +12% y/y

- 2023 operating margin 11% — downside risk to mid-single digits

- Mitigations: strategic sourcing, hedging, selective pricing

Emerging Market Demand and Economic Growth

- 60%+ of 2024 energy demand growth from emerging markets

- Asia GDP ~4–5% (2024), Latin America ~2–3% (2024)

- Regional expansion reduces reliance on domestic cycles

Energy cycle lifts 2024 capex but inflation, rates threaten margins; EM demand surges

Energy price cycles drive FET revenue: Brent ~86 USD/bbl and Henry Hub ~3.50 USD/MMBtu in 2024 boosted capex; downturns (60 USD/bbl in 2020–22) cut orders. Inflation (alloys +18–25%, electronics +12% y/y) and higher rates (US 10y ~4.2% in 2025 Q1) raise costs and debt service; 2023 margin 11% risks mid-single digits unless pricing, hedging, sourcing mitigate; emerging markets >60% demand growth.

| Metric | Value |

|---|---|

| Brent 2024 | ~86 USD/bbl |

| Henry Hub 2024 | ~3.50 USD/MMBtu |

| Alloy price change | +18–25% y/y |

| Electronics | +12% y/y |

| US 10y (2025 Q1) | ~4.2% |

| 2023 operating margin | 11% |

| Emerging market demand | >60% |

What You See Is What You Get

Forum Energy Technologies PESTLE Analysis

The preview shown here is the exact Forum Energy Technologies PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. What you see is the final document with real content and layout, delivered exactly as displayed with no placeholders or surprises. After checkout you’ll be able to download this same file immediately.