F5 PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic trends, and tech innovation are reshaping F5’s strategic landscape with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full PESTLE to get the complete, editable analysis and make informed decisions today.

Political factors

Geopolitical Trade Tensions

Ongoing trade friction between the US, China and EU is disrupting semiconductor supply chains critical to F5, with global chip lead times up ~22% YoY in 2024 and foundry constraints contributing to a 7% rise in F5 hardware COGS in FY2024.

US export curbs on high-end encryption to China and allied restrictions on security tech forced F5 to revise regional pricing and compliance, reducing addressable revenue in sanctioned markets by an estimated $120–180m in 2024.

These political shifts compel F5 to keep a flexible manufacturing footprint—diversifying suppliers across Taiwan, Korea and Malaysia—to hedge tariffs and localized bans and target a 15–20% reduction in single-country production reliance by 2026.

Government Cybersecurity Mandates

Governments worldwide are tightening national security directives, with the US allocating $18B to federal cybersecurity in FY2025 and the EU boosting cyber funds by 30% in 2024, driving demand for advanced application protection that benefits F5.

F5 stands to gain from increased public sector spending as agencies modernize legacy systems toward zero-trust; US federal zero-trust initiatives target 2027 full implementation across agencies.

To capture this lucrative market—US federal IT contracting exceeded $88B in cybersecurity-related awards in 2024—F5 must align its roadmap with federal certification standards such as FedRAMP to retain competitive edge and contract eligibility.

Data Sovereignty Legislation

Political moves toward digital sovereignty are pushing firms to keep data in-country, with 73% of surveyed CIOs in 2024 citing data localization as a top compliance driver; this boosts demand for F5 Distributed Cloud Services for localized app delivery and security enforcement. F5’s FY2024 infrastructure investments and channel expansion respond to fragmented regimes—requiring regional data center CAPEX and localized support teams that can raise operating costs by an estimated 8–12% in affected markets.

Public Sector Digital Transformation

National infrastructure bills and digitalization grants—US Bipartisan Infrastructure Law allocates $65B for broadband and EU Digital Decade funding targets €20B—are accelerating modernization of public services, creating demand for hybrid-cloud traffic management where F5’s ADC and security platforms fit.

F5 is positioned to capture this growth as governments shift to hybrid clouds; public sector accounted for about 12% of enterprise software spend in 2024, and stable political budget commitments correlate with multi-year procurement cycles boosting F5’s long-term public revenue.

Political stability and explicit multi-year digital infrastructure allocations (examples: US FY2025 IT budget increases ~3.5%) directly affect contract size and renewal rates, supporting predictable revenue streams for F5 in the public sector.

- Infrastructure funding: US $65B broadband, EU €20B digital targets

- Market signal: public sector ~12% of enterprise software spend (2024)

- Budget trend: US federal IT +3.5% FY2025 impacts procurement

- F5 fit: hybrid-cloud ADC, security demand from modernized services

Cyber Warfare and State Actors

The rise in state-sponsored cyberattacks has pushed application security into national defense policy; global ransomware and nation-state incidents rose 38% in 2024, driving governments to buy advanced protections.

F5’s application delivery and security portfolio, including DDoS mitigation and API protection, addresses this demand—F5 reported security revenue of $1.35B in FY2024, up 14% year-over-year.

Persistent demand for high-end security creates growth opportunities but raises the risk of F5 being a target for retaliatory digital strikes given its strategic role in national infrastructure protection.

- 38% rise in nation-state incidents in 2024

- F5 security revenue $1.35B FY2024 (+14% YoY)

- High demand for DDoS/API defenses; elevated targeting risk

F5 weathers political headwinds: higher hardware COGS, security up $1.35B

Political risks—trade frictions, export controls, data‑sovereignty rules and rising nation‑state cyberthreats—raised F5’s FY2024 hardware COGS ~7%, cut addressable China revenue ~$150m, and coincided with security revenue growth to $1.35B (+14%); public sector demand (≈12% of enterprise spend) and $65B US/€20B EU infrastructure funding support multi‑year contracts.

| Metric | Value (2024/25) |

|---|---|

| Hardware COGS impact | +7% |

| Addressable China revenue loss | $120–180m |

| Security revenue | $1.35B (+14%) |

| Public sector spend share | ≈12% |

| US broadband / EU digital | $65B / €20B |

What is included in the product

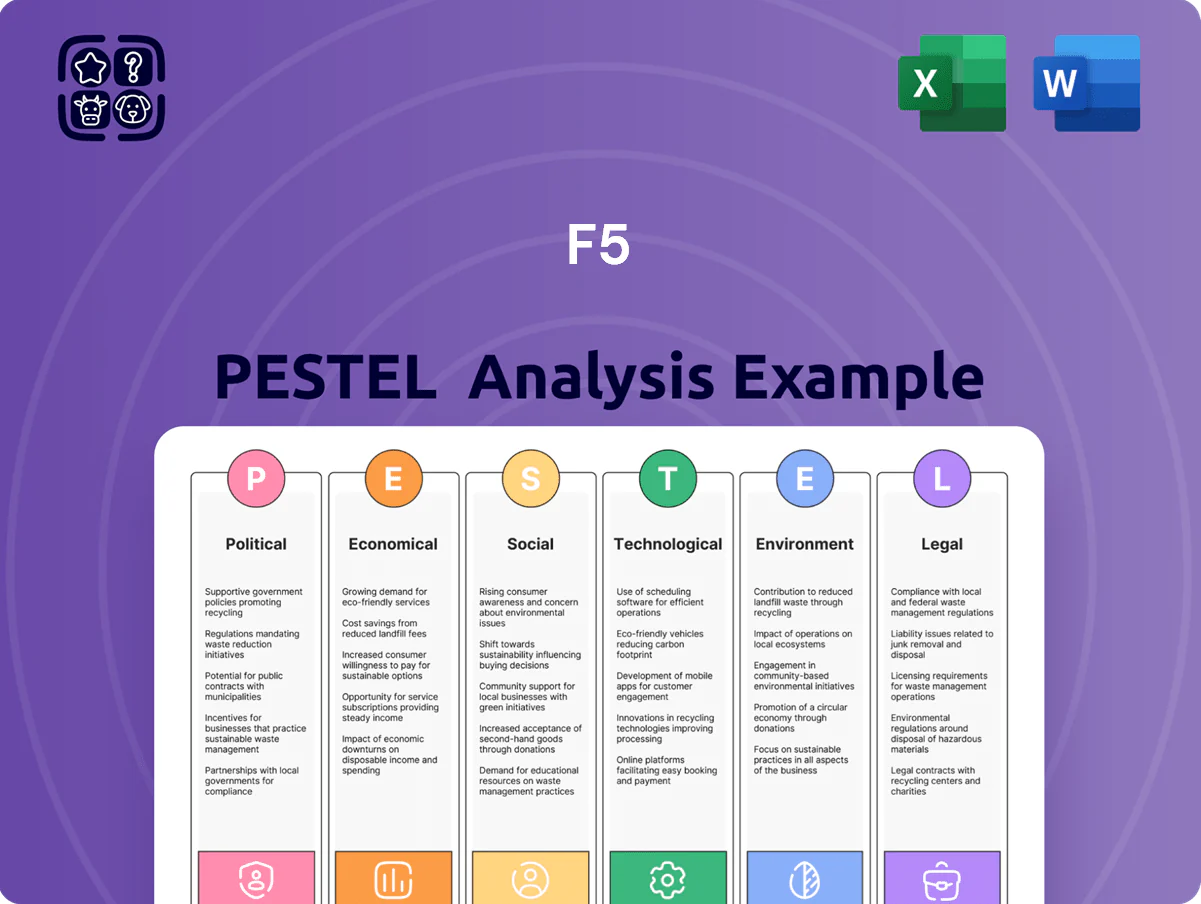

Explores how external macro-environmental factors uniquely affect F5 across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and forward-looking insights to inform strategy and scenario planning.

Visually segmented by PESTLE categories, allowing quick interpretation at a glance and easy insertion into presentations or strategy decks to streamline team alignment and risk discussions.

Economic factors

Transition to Subscription Models

F5 has shifted from hardware to recurring software/SaaS, with FY2024 subscription and services revenue reaching about $1.8B, up ~15% YoY, boosting ARR to roughly $2.1B by end-2024; this improves cash predictability and supports higher P/S multiples. The shift caused short-term GAAP EPS volatility during transition years. Investors track ARR growth as a core metric of economic health and market relevance.

Enterprise IT Budget Sensitivity

Fluctuations in global interest rates and 2024 US inflation at ~3.4% have compressed enterprise discretionary IT budgets, reducing upgrade spend; IDC reported 2024 IT spending growth slowing to 3.1%. Despite security seen as non-discretionary, large-scale ADC refresh cycles are often deferred in downturns—F5 must quantify ROI via operational efficiency gains (e.g., 20–40% app delivery cost reductions) and lower breach costs (average breach cost $4.45M in 2023) to retain allocations.

Global Currency Fluctuations

As a multinational, F5 is exposed to USD strength; a 10% appreciation of the dollar versus major currencies would have reduced 2024 non‑GAAP revenue by an estimated 3–5%, per company currency-sensitivity disclosures. Exchange-rate swings can erode international pricing competitiveness and translated foreign earnings—F5 reported a 6% FX headwind to FY2024 revenue growth. The firm uses forward contracts and options to hedge exposures, yet persistent currency headwinds remain a material factor for global financial performance.

Labor Market for Specialized Talent

The global shortage of senior software and cybersecurity talent keeps acquisition costs high; US median tech wages rose ~6.5% in 2023–2024, squeezing margins for firms like F5 (FY2024 gross margin 67.4%).

Rising wage inflation forces F5 to boost pay, benefits, and culture investments, while automation and AI tools are deployed to lift developer productivity and partially offset labor cost growth.

- Tech wage inflation ~6.5% (2023–24)

- F5 FY2024 gross margin 67.4%

- Increased spend on talent and benefits; AI/automation adoption to improve productivity

Expansion of the Edge Computing Market

The shift to edge computing opens significant revenue streams for F5 as enterprises process data near users; the global edge computing market is projected to reach USD 143.2 billion by 2027 with a 37.4% CAGR (2020–27), creating demand for F5s security and delivery offerings at the edge.

By securing and delivering services at the network edge, F5 enables customers to cut latency and bandwidth expenses—edge deployments can reduce round-trip latency by up to 50% and lower backbone bandwidth costs materially for content-heavy apps.

Edge is a high-growth segment that diversifies F5s economics beyond data centers; growing telco cloud and distributed app deployments drove F5s edge-related bookings growth in 2024, strengthening recurring revenue mix and TAM expansion.

- Global edge market ~USD 143.2B by 2027, 37.4% CAGR

- Edge can cut latency ~50% and reduce backbone bandwidth costs

- F5 saw rising edge-related bookings in 2024, boosting recurring revenue

F5’s SaaS surge: ARR ~$2.1B, subs up 15% as margins, FX and wage inflation bite

F5's SaaS shift raised FY2024 ARR to ~$2.1B with subscription/services ~$1.8B (+15% YoY), improving cash predictability; FY2024 gross margin 67.4%. 2024 US inflation ~3.4% and IT spend growth ~3.1% pressured budgets; security remains prioritized. FX cost a ~6% headwind to 2024 revenue; tech wage inflation ~6.5% raises operating costs. Edge market trillion? see table.

| Metric | Value (2024) |

|---|---|

| ARR | ~$2.1B |

| Subscr/Services | ~$1.8B (+15% YoY) |

| Gross margin | 67.4% |

| US inflation | ~3.4% |

| IT spend growth (IDC) | ~3.1% |

| FX headwind | ~6% |

| Tech wage inflation | ~6.5% |

Preview the Actual Deliverable

F5 PESTLE Analysis

The preview shown here is the exact F5 PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic trends, and tech innovation are reshaping F5’s strategic landscape with our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full PESTLE to get the complete, editable analysis and make informed decisions today.

Political factors

Geopolitical Trade Tensions

Ongoing trade friction between the US, China and EU is disrupting semiconductor supply chains critical to F5, with global chip lead times up ~22% YoY in 2024 and foundry constraints contributing to a 7% rise in F5 hardware COGS in FY2024.

US export curbs on high-end encryption to China and allied restrictions on security tech forced F5 to revise regional pricing and compliance, reducing addressable revenue in sanctioned markets by an estimated $120–180m in 2024.

These political shifts compel F5 to keep a flexible manufacturing footprint—diversifying suppliers across Taiwan, Korea and Malaysia—to hedge tariffs and localized bans and target a 15–20% reduction in single-country production reliance by 2026.

Government Cybersecurity Mandates

Governments worldwide are tightening national security directives, with the US allocating $18B to federal cybersecurity in FY2025 and the EU boosting cyber funds by 30% in 2024, driving demand for advanced application protection that benefits F5.

F5 stands to gain from increased public sector spending as agencies modernize legacy systems toward zero-trust; US federal zero-trust initiatives target 2027 full implementation across agencies.

To capture this lucrative market—US federal IT contracting exceeded $88B in cybersecurity-related awards in 2024—F5 must align its roadmap with federal certification standards such as FedRAMP to retain competitive edge and contract eligibility.

Data Sovereignty Legislation

Political moves toward digital sovereignty are pushing firms to keep data in-country, with 73% of surveyed CIOs in 2024 citing data localization as a top compliance driver; this boosts demand for F5 Distributed Cloud Services for localized app delivery and security enforcement. F5’s FY2024 infrastructure investments and channel expansion respond to fragmented regimes—requiring regional data center CAPEX and localized support teams that can raise operating costs by an estimated 8–12% in affected markets.

Public Sector Digital Transformation

National infrastructure bills and digitalization grants—US Bipartisan Infrastructure Law allocates $65B for broadband and EU Digital Decade funding targets €20B—are accelerating modernization of public services, creating demand for hybrid-cloud traffic management where F5’s ADC and security platforms fit.

F5 is positioned to capture this growth as governments shift to hybrid clouds; public sector accounted for about 12% of enterprise software spend in 2024, and stable political budget commitments correlate with multi-year procurement cycles boosting F5’s long-term public revenue.

Political stability and explicit multi-year digital infrastructure allocations (examples: US FY2025 IT budget increases ~3.5%) directly affect contract size and renewal rates, supporting predictable revenue streams for F5 in the public sector.

- Infrastructure funding: US $65B broadband, EU €20B digital targets

- Market signal: public sector ~12% of enterprise software spend (2024)

- Budget trend: US federal IT +3.5% FY2025 impacts procurement

- F5 fit: hybrid-cloud ADC, security demand from modernized services

Cyber Warfare and State Actors

The rise in state-sponsored cyberattacks has pushed application security into national defense policy; global ransomware and nation-state incidents rose 38% in 2024, driving governments to buy advanced protections.

F5’s application delivery and security portfolio, including DDoS mitigation and API protection, addresses this demand—F5 reported security revenue of $1.35B in FY2024, up 14% year-over-year.

Persistent demand for high-end security creates growth opportunities but raises the risk of F5 being a target for retaliatory digital strikes given its strategic role in national infrastructure protection.

- 38% rise in nation-state incidents in 2024

- F5 security revenue $1.35B FY2024 (+14% YoY)

- High demand for DDoS/API defenses; elevated targeting risk

F5 weathers political headwinds: higher hardware COGS, security up $1.35B

Political risks—trade frictions, export controls, data‑sovereignty rules and rising nation‑state cyberthreats—raised F5’s FY2024 hardware COGS ~7%, cut addressable China revenue ~$150m, and coincided with security revenue growth to $1.35B (+14%); public sector demand (≈12% of enterprise spend) and $65B US/€20B EU infrastructure funding support multi‑year contracts.

| Metric | Value (2024/25) |

|---|---|

| Hardware COGS impact | +7% |

| Addressable China revenue loss | $120–180m |

| Security revenue | $1.35B (+14%) |

| Public sector spend share | ≈12% |

| US broadband / EU digital | $65B / €20B |

What is included in the product

Explores how external macro-environmental factors uniquely affect F5 across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and forward-looking insights to inform strategy and scenario planning.

Visually segmented by PESTLE categories, allowing quick interpretation at a glance and easy insertion into presentations or strategy decks to streamline team alignment and risk discussions.

Economic factors

Transition to Subscription Models

F5 has shifted from hardware to recurring software/SaaS, with FY2024 subscription and services revenue reaching about $1.8B, up ~15% YoY, boosting ARR to roughly $2.1B by end-2024; this improves cash predictability and supports higher P/S multiples. The shift caused short-term GAAP EPS volatility during transition years. Investors track ARR growth as a core metric of economic health and market relevance.

Enterprise IT Budget Sensitivity

Fluctuations in global interest rates and 2024 US inflation at ~3.4% have compressed enterprise discretionary IT budgets, reducing upgrade spend; IDC reported 2024 IT spending growth slowing to 3.1%. Despite security seen as non-discretionary, large-scale ADC refresh cycles are often deferred in downturns—F5 must quantify ROI via operational efficiency gains (e.g., 20–40% app delivery cost reductions) and lower breach costs (average breach cost $4.45M in 2023) to retain allocations.

Global Currency Fluctuations

As a multinational, F5 is exposed to USD strength; a 10% appreciation of the dollar versus major currencies would have reduced 2024 non‑GAAP revenue by an estimated 3–5%, per company currency-sensitivity disclosures. Exchange-rate swings can erode international pricing competitiveness and translated foreign earnings—F5 reported a 6% FX headwind to FY2024 revenue growth. The firm uses forward contracts and options to hedge exposures, yet persistent currency headwinds remain a material factor for global financial performance.

Labor Market for Specialized Talent

The global shortage of senior software and cybersecurity talent keeps acquisition costs high; US median tech wages rose ~6.5% in 2023–2024, squeezing margins for firms like F5 (FY2024 gross margin 67.4%).

Rising wage inflation forces F5 to boost pay, benefits, and culture investments, while automation and AI tools are deployed to lift developer productivity and partially offset labor cost growth.

- Tech wage inflation ~6.5% (2023–24)

- F5 FY2024 gross margin 67.4%

- Increased spend on talent and benefits; AI/automation adoption to improve productivity

Expansion of the Edge Computing Market

The shift to edge computing opens significant revenue streams for F5 as enterprises process data near users; the global edge computing market is projected to reach USD 143.2 billion by 2027 with a 37.4% CAGR (2020–27), creating demand for F5s security and delivery offerings at the edge.

By securing and delivering services at the network edge, F5 enables customers to cut latency and bandwidth expenses—edge deployments can reduce round-trip latency by up to 50% and lower backbone bandwidth costs materially for content-heavy apps.

Edge is a high-growth segment that diversifies F5s economics beyond data centers; growing telco cloud and distributed app deployments drove F5s edge-related bookings growth in 2024, strengthening recurring revenue mix and TAM expansion.

- Global edge market ~USD 143.2B by 2027, 37.4% CAGR

- Edge can cut latency ~50% and reduce backbone bandwidth costs

- F5 saw rising edge-related bookings in 2024, boosting recurring revenue

F5’s SaaS surge: ARR ~$2.1B, subs up 15% as margins, FX and wage inflation bite

F5's SaaS shift raised FY2024 ARR to ~$2.1B with subscription/services ~$1.8B (+15% YoY), improving cash predictability; FY2024 gross margin 67.4%. 2024 US inflation ~3.4% and IT spend growth ~3.1% pressured budgets; security remains prioritized. FX cost a ~6% headwind to 2024 revenue; tech wage inflation ~6.5% raises operating costs. Edge market trillion? see table.

| Metric | Value (2024) |

|---|---|

| ARR | ~$2.1B |

| Subscr/Services | ~$1.8B (+15% YoY) |

| Gross margin | 67.4% |

| US inflation | ~3.4% |

| IT spend growth (IDC) | ~3.1% |

| FX headwind | ~6% |

| Tech wage inflation | ~6.5% |

Preview the Actual Deliverable

F5 PESTLE Analysis

The preview shown here is the exact F5 PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.