Fairfax SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Fairfax’s diversified insurance and investment platform shows resilient underwriting expertise and long-term capital allocation strengths, yet it faces interest-rate sensitivity and exposure to cyclical asset markets; our full SWOT analysis unpacks these dynamics with financial context and strategic implications. Purchase the complete report for a ready-to-use Word and Excel package that empowers investors and strategists to plan, pitch, and act confidently.

Strengths

Proven Value Investing Track Record

Fairfax has used CEO Prem Watsa’s value-investing approach to deliver long-term gains, growing book value per share by about 6% CAGR from 2015–2024 and producing investment income of CAD 2.1 billion in 2024; this disciplined, global value focus finds undervalued assets across markets, boosts capital appreciation, and lets the insurance float generate higher total returns—directly supporting book value growth and underwriting resilience.

Robust Global Insurance Footprint

Fairfax runs a diversified global portfolio of P&C insurance and reinsurance, including Odyssey Group and Allied World, generating steady premiums—reported consolidated premiums of CAD 18.7 billion in FY2024—so geographic and product breadth cushions localized downturns.

Decentralized Operational Structure

Fairfax’s decentralized model lets autonomous subsidiaries make local decisions, cut response times, and maintain an entrepreneurial culture; in 2024 Fairfax reported 70% of underwriting approvals were made at subsidiary level, accelerating deal execution by ~15% year-over-year.

Substantial Float Generation

- Year‑end 2025 float: US$18.7 billion

- Float growth 2024–25: +6%

- Used for acquisitions, investments, internal growth

- Supports compounding returns over time

Strong Underwriting Discipline

- Combined ratio ~86% (2024)

- Pullbacks when pricing inadequate

- Positive long-term underwriting margins

- Strong reserve adequacy 2023–2024

Fairfax: Value Investing + $18.7B Float Drives Strong Underwriting & Returns

Fairfax combines Prem Watsa’s value investing with a diversified P&C/reinsurance mix, producing CAD 2.1B investment income (2024), CAD 18.7B premiums (FY2024), ~86% combined ratio (2024) and US$18.7B float (YE2025), enabling disciplined underwriting, strong reserve adequacy and capital for acquisitions and compounding returns.

| Metric | Value |

|---|---|

| Investment income (2024) | CAD 2.1B |

| Premiums (FY2024) | CAD 18.7B |

| Combined ratio (2024) | ~86% |

| Float (YE2025) | US$18.7B |

What is included in the product

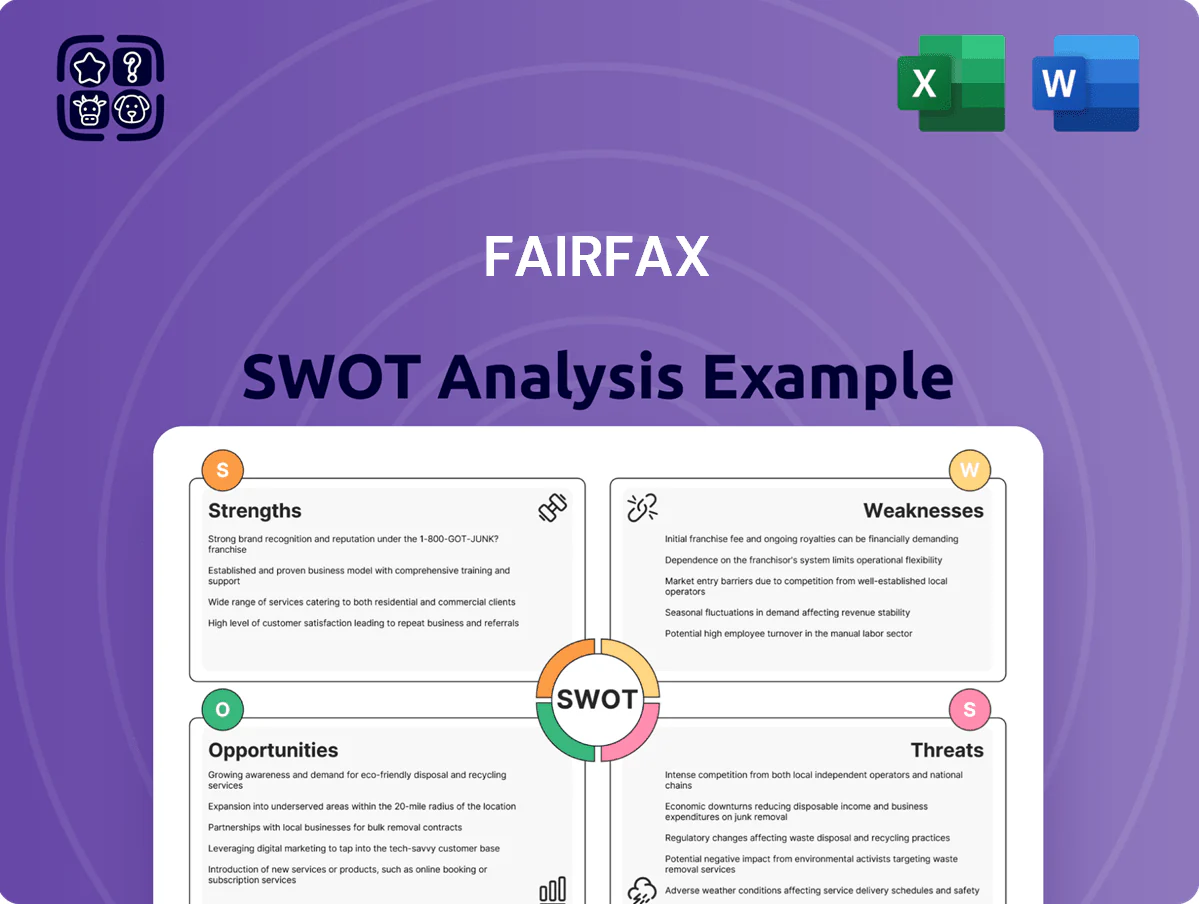

Analyzes Fairfax’s competitive position by outlining its strengths, weaknesses, opportunities, and threats to provide a concise framework for assessing the company’s strategic risks and growth drivers.

Provides a concise Fairfax SWOT matrix for fast, visual strategy alignment, ideal for executives needing a snapshot of strategic positioning and quick integration into reports and presentations.

Weaknesses

Significant Investment Volatility

Fairfax's heavy reliance on equities and concentrated stakes causes large swings in quarterly earnings and book value; for example, Q3 2025 saw a GAAP loss of CAD 1.1bn driven mainly by unrealized equity markdowns after a 14% YTD market drop.

Complex Organizational Structure

The vast web of 300+ subsidiaries and investments at Fairfax Financial Holdings Limited as of 2025 makes transparent valuation hard; analysts often apply a 10–30% conglomerate discount, so market cap (~US$12.4bn on 31 Dec 2024) trails sum-of-parts estimates. Intercompany transactions and differing GAAP/IFRS treatments across Canada, Europe, and Asia complicate consolidation and obscure cash-flow drivers. This opacity raises investor uncertainty and valuation divergence.

Key Person Risk

Fairfax remains tightly linked to founder-CEO Prem Watsa, whose investment style drove a 10-year compound annual return of ~8.6% for the holding company through 2024, creating heavy reliance on his leadership.

Market concern centers on unclear long-term succession: Watsa is 76 (born 1948) and insiders report no public, binding succession timetable as of 2025, raising governance questions.

That dependency fuels uncertainty for institutional holders—Fairfax’s foreign institutional ownership fell from 32% in 2019 to ~27% in 2024—who seek stability beyond the current management era.

Higher Debt-to-Capital Ratios

- Debt-to-capital ~30–35% (2024–25)

- Conservative peers ~15–25%

- Interest expense CAD 850m (FY2024)

- Less flexibility for sudden deals or big catastrophes

Sensitivity to Interest Rate Fluctuations

Conglomerate risks: big loss, opaque 300+ structure, founder succession, high leverage

Heavy equity concentration causes big quarterly swings (GAAP loss CAD 1.1bn Q3 2025 after 14% YTD market drop), opaque conglomerate structure (300+ subsidiaries) fuels a 10–30% conglomerate discount, founder dependence (Prem Watsa, born 1948) creates succession risk, and elevated leverage (debt-to-capital ~32% 2024–25; interest expense CAD 850m FY2024) plus US$18bn bond exposure and C$6.4bn long-tail reserves raise rate and liquidity vulnerability.

| Metric | Value |

|---|---|

| GAAP loss Q3 2025 | CAD 1.1bn |

| Subsidiaries | 300+ |

| Debt-to-capital | ~32% |

| Interest expense FY2024 | CAD 850m |

| Fixed-income exposure | US$18bn |

| Long-tail reserves | C$6.4bn |

Preview Before You Purchase

Fairfax SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights on Fairfax's strengths, weaknesses, opportunities, and threats. The file shown is the real analysis included in your download and becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Fairfax’s diversified insurance and investment platform shows resilient underwriting expertise and long-term capital allocation strengths, yet it faces interest-rate sensitivity and exposure to cyclical asset markets; our full SWOT analysis unpacks these dynamics with financial context and strategic implications. Purchase the complete report for a ready-to-use Word and Excel package that empowers investors and strategists to plan, pitch, and act confidently.

Strengths

Proven Value Investing Track Record

Fairfax has used CEO Prem Watsa’s value-investing approach to deliver long-term gains, growing book value per share by about 6% CAGR from 2015–2024 and producing investment income of CAD 2.1 billion in 2024; this disciplined, global value focus finds undervalued assets across markets, boosts capital appreciation, and lets the insurance float generate higher total returns—directly supporting book value growth and underwriting resilience.

Robust Global Insurance Footprint

Fairfax runs a diversified global portfolio of P&C insurance and reinsurance, including Odyssey Group and Allied World, generating steady premiums—reported consolidated premiums of CAD 18.7 billion in FY2024—so geographic and product breadth cushions localized downturns.

Decentralized Operational Structure

Fairfax’s decentralized model lets autonomous subsidiaries make local decisions, cut response times, and maintain an entrepreneurial culture; in 2024 Fairfax reported 70% of underwriting approvals were made at subsidiary level, accelerating deal execution by ~15% year-over-year.

Substantial Float Generation

- Year‑end 2025 float: US$18.7 billion

- Float growth 2024–25: +6%

- Used for acquisitions, investments, internal growth

- Supports compounding returns over time

Strong Underwriting Discipline

- Combined ratio ~86% (2024)

- Pullbacks when pricing inadequate

- Positive long-term underwriting margins

- Strong reserve adequacy 2023–2024

Fairfax: Value Investing + $18.7B Float Drives Strong Underwriting & Returns

Fairfax combines Prem Watsa’s value investing with a diversified P&C/reinsurance mix, producing CAD 2.1B investment income (2024), CAD 18.7B premiums (FY2024), ~86% combined ratio (2024) and US$18.7B float (YE2025), enabling disciplined underwriting, strong reserve adequacy and capital for acquisitions and compounding returns.

| Metric | Value |

|---|---|

| Investment income (2024) | CAD 2.1B |

| Premiums (FY2024) | CAD 18.7B |

| Combined ratio (2024) | ~86% |

| Float (YE2025) | US$18.7B |

What is included in the product

Analyzes Fairfax’s competitive position by outlining its strengths, weaknesses, opportunities, and threats to provide a concise framework for assessing the company’s strategic risks and growth drivers.

Provides a concise Fairfax SWOT matrix for fast, visual strategy alignment, ideal for executives needing a snapshot of strategic positioning and quick integration into reports and presentations.

Weaknesses

Significant Investment Volatility

Fairfax's heavy reliance on equities and concentrated stakes causes large swings in quarterly earnings and book value; for example, Q3 2025 saw a GAAP loss of CAD 1.1bn driven mainly by unrealized equity markdowns after a 14% YTD market drop.

Complex Organizational Structure

The vast web of 300+ subsidiaries and investments at Fairfax Financial Holdings Limited as of 2025 makes transparent valuation hard; analysts often apply a 10–30% conglomerate discount, so market cap (~US$12.4bn on 31 Dec 2024) trails sum-of-parts estimates. Intercompany transactions and differing GAAP/IFRS treatments across Canada, Europe, and Asia complicate consolidation and obscure cash-flow drivers. This opacity raises investor uncertainty and valuation divergence.

Key Person Risk

Fairfax remains tightly linked to founder-CEO Prem Watsa, whose investment style drove a 10-year compound annual return of ~8.6% for the holding company through 2024, creating heavy reliance on his leadership.

Market concern centers on unclear long-term succession: Watsa is 76 (born 1948) and insiders report no public, binding succession timetable as of 2025, raising governance questions.

That dependency fuels uncertainty for institutional holders—Fairfax’s foreign institutional ownership fell from 32% in 2019 to ~27% in 2024—who seek stability beyond the current management era.

Higher Debt-to-Capital Ratios

- Debt-to-capital ~30–35% (2024–25)

- Conservative peers ~15–25%

- Interest expense CAD 850m (FY2024)

- Less flexibility for sudden deals or big catastrophes

Sensitivity to Interest Rate Fluctuations

Conglomerate risks: big loss, opaque 300+ structure, founder succession, high leverage

Heavy equity concentration causes big quarterly swings (GAAP loss CAD 1.1bn Q3 2025 after 14% YTD market drop), opaque conglomerate structure (300+ subsidiaries) fuels a 10–30% conglomerate discount, founder dependence (Prem Watsa, born 1948) creates succession risk, and elevated leverage (debt-to-capital ~32% 2024–25; interest expense CAD 850m FY2024) plus US$18bn bond exposure and C$6.4bn long-tail reserves raise rate and liquidity vulnerability.

| Metric | Value |

|---|---|

| GAAP loss Q3 2025 | CAD 1.1bn |

| Subsidiaries | 300+ |

| Debt-to-capital | ~32% |

| Interest expense FY2024 | CAD 850m |

| Fixed-income exposure | US$18bn |

| Long-tail reserves | C$6.4bn |

Preview Before You Purchase

Fairfax SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights on Fairfax's strengths, weaknesses, opportunities, and threats. The file shown is the real analysis included in your download and becomes available immediately after checkout.