FAIST PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological advances are reshaping FAIST’s competitive landscape in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access deep-dive insights, risk assessments, and strategic recommendations formatted for immediate use in reports and presentations.

Political factors

Geopolitical trade stability

The stability of international trade agreements is vital for FAIST, which exports industrial plants and equipment to over 40 countries; disruptions could raise logistics and tariff costs, with EU trade policy shifts potentially altering tariffs on steel and aluminum—components accounting for roughly 18–22% of BOM for heavy equipment. Changes in transatlantic relations could affect demand and financing terms for US/EU projects, while 2024 regional tensions in manufacturing hubs (e.g., Red Sea shipping incidents increased freight rates by ~35% in 2023) may force FAIST to diversify suppliers and reroute shipments to maintain continuity.

Industrial subsidy programs

Governmental support for the energy transition and aerospace sectors boosts demand for FAIST's thermal insulation and acoustic solutions; EU Green Deal and REPowerEU directed over €350 billion in 2024–25 to clean energy projects, creating direct procurement needs for industrial insulation. Subsidies for green infrastructure and high-tech manufacturing—e.g., US CHIPS+ clean-energy tie-ins with $100+ billion incentives in 2024—sustain project pipelines. Political leadership changes can swing funding: IMF-tracked fiscal reallocations showed ±12% variance in industrial stimulus across major economies in 2024.

Defense spending priorities

As a supplier to aerospace and energy, FAIST is exposed to defense budgets; US defense R&D and procurement rose to $858B in 2024, with aerospace programs driving increased demand for test cells and acoustic enclosures.

European defense spending hit €312B in 2024, and regional reshoring policies—e.g., EU Critical Raw Materials Act and US CHIPS/Industrial incentives—boost domestic plant builds, creating larger localized contracts for FAIST.

Labor and migration policies

The availability of skilled engineering talent depends on political decisions on technical education and migration; EU data shows 22% of engineering roles in 2024 were filled by migrants in key markets, impacting FAIST's project staffing.

Policies easing cross-border movement of specialized technicians reduce lead times for international installations; restrictive laws can raise labor costs by 8-12% and delay turnkey deliveries by months.

- 22% of engineering hires in 2024 from migrants in target markets

- Labor cost increases of 8-12% under restrictive regimes

- Potential project delays measured in months for complex deliveries

Global regulatory harmonization

Political moves toward regulatory harmonization—such as the EU-Japan Mutual Recognition Agreement and discussions in US-EU trade talks—lower FAIST’s engineering costs by reducing market-specific redesigns; harmonized standards can cut NPI compliance expenses by an estimated 10–15% based on industry benchmarks (2024).

Conversely, episodes of political volatility (e.g., 2023–2025 trade frictions) that cause regulatory divergence force FAIST to increase spending on customized compliance engineering, potentially raising product rollout costs by 8–12% and extending time-to-market.

- Harmonization: ~10–15% lower NPI compliance costs (2024 benchmarks)

- Divergence: +8–12% product rollout cost and delays (2023–2025 trade data)

- Strategy: monitor trade agreements and budget for region-specific compliance

Policy shifts drive FAIST costs, demand, and local aerospace growth

Political stability and trade agreements shape FAIST’s costs and market access: tariff shifts on steel/aluminum (18–22% of BOM) and 35% freight spikes (2023) increase logistics and input expenses; green transition funding (€350B EU 2024–25, $100B+ US incentives 2024) lifts insulation demand; defense spend (€312B EU, $858B US in 2024) and reshoring policies create local contract growth; migration/education policies (22% migrant engineers 2024) and harmonization cut NPI costs ~10–15% while divergence raises rollout costs 8–12%.

| Factor | 2024–25 Data | Impact on FAIST |

|---|---|---|

| Tariffs & freight | 18–22% BOM; +35% freight | Higher input/logistics costs |

| Green funding | €350B EU; $100B+ US | Increased demand |

| Defense spend | €312B EU; $858B US | More aerospace contracts |

| Skilled migration | 22% engineers | Affects staffing/lead times |

| Regulatory | Harmonization −10–15%; Divergence +8–12% | Alters NPI/compliance costs |

What is included in the product

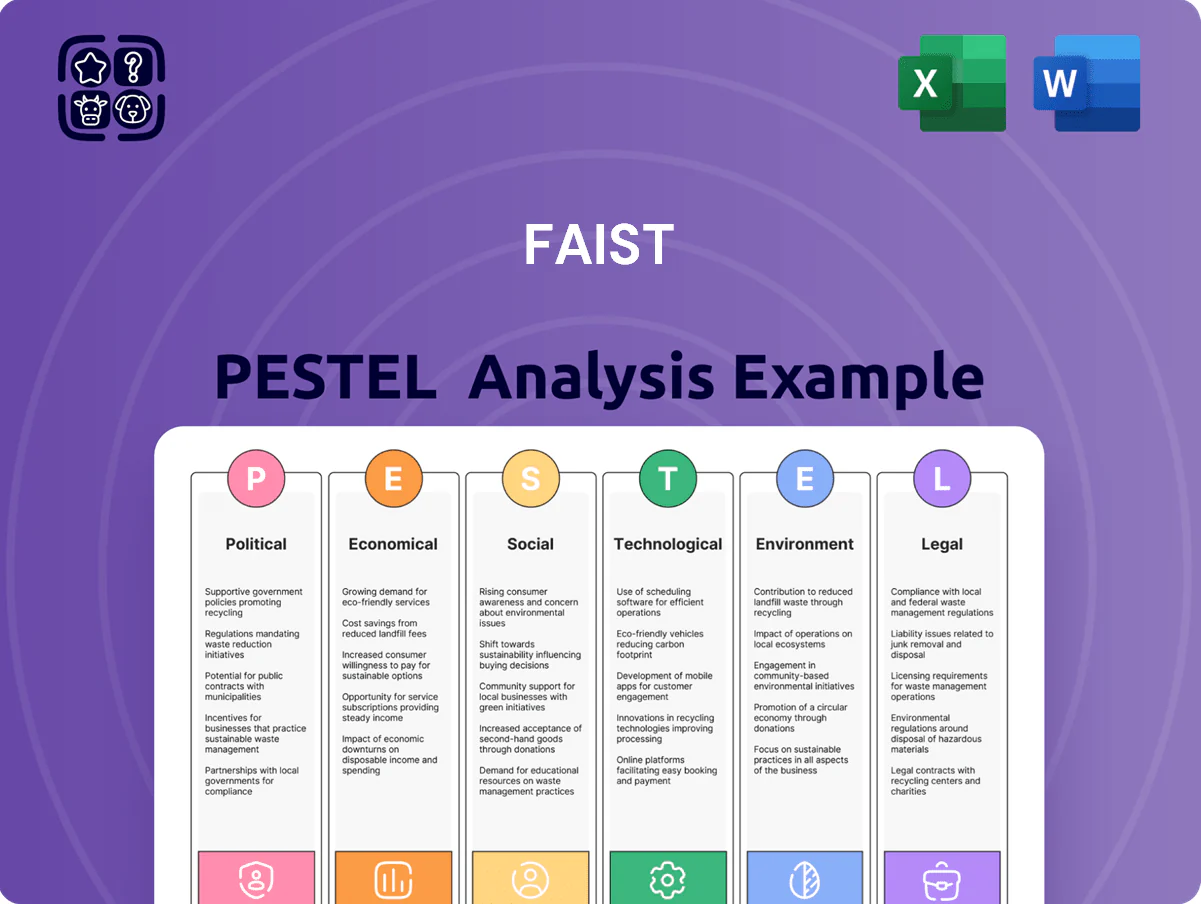

Explores how external macro-environmental factors uniquely affect the FAIST across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to identify threats and opportunities.

FAIST PESTLE delivers a concise, visually segmented summary of external factors for quick reference in meetings or presentations, easily shareable across teams and customizable with notes for regional or business-line context.

Economic factors

Global industrial capital expenditure

The demand for FAIST's large-scale industrial plants closely follows capex cycles in automotive and energy: global manufacturing capex rose 3.8% in 2024 but semiconductor and EV-related investments drove a 12% regional surge in Europe and China, supporting orders for acoustic enclosures and cleanrooms. High interest rates—global policy rates averaged ~3.5% in 2024—have slowed corporate capex, delaying procurement cycles. During GDP growth (global GDP +3.1% in 2024) manufacturers increasingly upgrade facilities with advanced soundproofing and thermal tech.

Raw material price volatility

Fluctuations in steel, aluminum and insulation prices drive FAIST’s manufacturing costs—steel rose ~15% in 2024 and aluminum 10%, raising input spend by an estimated 8–12% for comparable projects. Commodity-market volatility in 2023–2025 narrowed gross margins by up to 3 percentage points on fixed-price contracts when no escalation clauses existed. Absence of flexible pricing exposes FAIST to squeezed margins; monitoring global supply-demand and LME/COMEX price trends is essential to preserve competitive pricing and liquidity.

Currency exchange rate fluctuations

As an international player, FAIST faces FX risk that can alter bid competitiveness; a 10% EUR appreciation vs USD in 2024 would raise euro-priced system costs for US buyers similarly, risking lost tenders. A weaker euro could boost exports—Germany's goods exports rose 3.5% in 2024—but raises imported component costs, where imported input share for aero suppliers often exceeds 40%. Active hedging (forwards/options) is essential to protect project margins.

Energy cost trends

Rising energy prices—EU industrial gas up ~30% in 2024 vs 2021 and global industrial electricity tariffs rising ~12% YoY in 2023—boost demand for FAIST thermal insulation as firms seek lower overheads and higher process efficiency.

High energy costs drive manufacturers to buy turnkey systems that cut heat loss; studies show insulation can reduce thermal energy use by 10–25%, supporting FAIST’s advanced, energy-efficient components.

- EU industrial gas +30% (2024 vs 2021)

- Global industrial electricity +12% YoY (2023)

- Insulation reduces thermal energy use 10–25%

Labor cost inflation

The rising cost of specialized engineering and manufacturing labor in developed markets—wages up ~4.5% YoY in EU manufacturing in 2024—squeezes FAIST's operational budget, forcing a trade-off between premium German engineering and cost-efficient production.

Sustained wage inflation (e.g., Germany average hourly labor costs +5.1% in 2024) requires FAIST to accelerate automation and lean process gains to preserve margins.

- EU manufacturing wages +4.5% YoY (2024)

- Germany hourly labor costs +5.1% (2024)

- Target: 10–20% automation CAPEX to offset labor inflation

Capex surge, rising input costs squeeze margins—hedge FX as energy fuels insulation demand

Global capex and EV/semiconductor investment (+12% regional surge in 2024) bolster FAIST orders; global GDP +3.1% (2024). Steel +15% and aluminum +10% (2024) raised input costs, narrowing margins ~3pp. EUR FX moves (10% swing) materially affect bid competitiveness; hedging recommended. Energy/gas hikes (EU gas +30% vs 2021) increase demand for insulation (saves 10–25% thermal use); EU wages +4.5% (2024).

| Metric | 2024/2023 |

|---|---|

| Global GDP | +3.1% (2024) |

| Regional capex (EV/semicon) | +12% (2024) |

| Steel | +15% (2024) |

| Aluminum | +10% (2024) |

| EU gas vs 2021 | +30% |

| Insulation savings | 10–25% |

| EU wages | +4.5% (2024) |

Preview Before You Purchase

FAIST PESTLE Analysis

The preview shown here is the exact FAIST PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and structure visible here are identical to the file you’ll download immediately after payment, so what you see is exactly what you’ll own and apply.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological advances are reshaping FAIST’s competitive landscape in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access deep-dive insights, risk assessments, and strategic recommendations formatted for immediate use in reports and presentations.

Political factors

Geopolitical trade stability

The stability of international trade agreements is vital for FAIST, which exports industrial plants and equipment to over 40 countries; disruptions could raise logistics and tariff costs, with EU trade policy shifts potentially altering tariffs on steel and aluminum—components accounting for roughly 18–22% of BOM for heavy equipment. Changes in transatlantic relations could affect demand and financing terms for US/EU projects, while 2024 regional tensions in manufacturing hubs (e.g., Red Sea shipping incidents increased freight rates by ~35% in 2023) may force FAIST to diversify suppliers and reroute shipments to maintain continuity.

Industrial subsidy programs

Governmental support for the energy transition and aerospace sectors boosts demand for FAIST's thermal insulation and acoustic solutions; EU Green Deal and REPowerEU directed over €350 billion in 2024–25 to clean energy projects, creating direct procurement needs for industrial insulation. Subsidies for green infrastructure and high-tech manufacturing—e.g., US CHIPS+ clean-energy tie-ins with $100+ billion incentives in 2024—sustain project pipelines. Political leadership changes can swing funding: IMF-tracked fiscal reallocations showed ±12% variance in industrial stimulus across major economies in 2024.

Defense spending priorities

As a supplier to aerospace and energy, FAIST is exposed to defense budgets; US defense R&D and procurement rose to $858B in 2024, with aerospace programs driving increased demand for test cells and acoustic enclosures.

European defense spending hit €312B in 2024, and regional reshoring policies—e.g., EU Critical Raw Materials Act and US CHIPS/Industrial incentives—boost domestic plant builds, creating larger localized contracts for FAIST.

Labor and migration policies

The availability of skilled engineering talent depends on political decisions on technical education and migration; EU data shows 22% of engineering roles in 2024 were filled by migrants in key markets, impacting FAIST's project staffing.

Policies easing cross-border movement of specialized technicians reduce lead times for international installations; restrictive laws can raise labor costs by 8-12% and delay turnkey deliveries by months.

- 22% of engineering hires in 2024 from migrants in target markets

- Labor cost increases of 8-12% under restrictive regimes

- Potential project delays measured in months for complex deliveries

Global regulatory harmonization

Political moves toward regulatory harmonization—such as the EU-Japan Mutual Recognition Agreement and discussions in US-EU trade talks—lower FAIST’s engineering costs by reducing market-specific redesigns; harmonized standards can cut NPI compliance expenses by an estimated 10–15% based on industry benchmarks (2024).

Conversely, episodes of political volatility (e.g., 2023–2025 trade frictions) that cause regulatory divergence force FAIST to increase spending on customized compliance engineering, potentially raising product rollout costs by 8–12% and extending time-to-market.

- Harmonization: ~10–15% lower NPI compliance costs (2024 benchmarks)

- Divergence: +8–12% product rollout cost and delays (2023–2025 trade data)

- Strategy: monitor trade agreements and budget for region-specific compliance

Policy shifts drive FAIST costs, demand, and local aerospace growth

Political stability and trade agreements shape FAIST’s costs and market access: tariff shifts on steel/aluminum (18–22% of BOM) and 35% freight spikes (2023) increase logistics and input expenses; green transition funding (€350B EU 2024–25, $100B+ US incentives 2024) lifts insulation demand; defense spend (€312B EU, $858B US in 2024) and reshoring policies create local contract growth; migration/education policies (22% migrant engineers 2024) and harmonization cut NPI costs ~10–15% while divergence raises rollout costs 8–12%.

| Factor | 2024–25 Data | Impact on FAIST |

|---|---|---|

| Tariffs & freight | 18–22% BOM; +35% freight | Higher input/logistics costs |

| Green funding | €350B EU; $100B+ US | Increased demand |

| Defense spend | €312B EU; $858B US | More aerospace contracts |

| Skilled migration | 22% engineers | Affects staffing/lead times |

| Regulatory | Harmonization −10–15%; Divergence +8–12% | Alters NPI/compliance costs |

What is included in the product

Explores how external macro-environmental factors uniquely affect the FAIST across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to identify threats and opportunities.

FAIST PESTLE delivers a concise, visually segmented summary of external factors for quick reference in meetings or presentations, easily shareable across teams and customizable with notes for regional or business-line context.

Economic factors

Global industrial capital expenditure

The demand for FAIST's large-scale industrial plants closely follows capex cycles in automotive and energy: global manufacturing capex rose 3.8% in 2024 but semiconductor and EV-related investments drove a 12% regional surge in Europe and China, supporting orders for acoustic enclosures and cleanrooms. High interest rates—global policy rates averaged ~3.5% in 2024—have slowed corporate capex, delaying procurement cycles. During GDP growth (global GDP +3.1% in 2024) manufacturers increasingly upgrade facilities with advanced soundproofing and thermal tech.

Raw material price volatility

Fluctuations in steel, aluminum and insulation prices drive FAIST’s manufacturing costs—steel rose ~15% in 2024 and aluminum 10%, raising input spend by an estimated 8–12% for comparable projects. Commodity-market volatility in 2023–2025 narrowed gross margins by up to 3 percentage points on fixed-price contracts when no escalation clauses existed. Absence of flexible pricing exposes FAIST to squeezed margins; monitoring global supply-demand and LME/COMEX price trends is essential to preserve competitive pricing and liquidity.

Currency exchange rate fluctuations

As an international player, FAIST faces FX risk that can alter bid competitiveness; a 10% EUR appreciation vs USD in 2024 would raise euro-priced system costs for US buyers similarly, risking lost tenders. A weaker euro could boost exports—Germany's goods exports rose 3.5% in 2024—but raises imported component costs, where imported input share for aero suppliers often exceeds 40%. Active hedging (forwards/options) is essential to protect project margins.

Energy cost trends

Rising energy prices—EU industrial gas up ~30% in 2024 vs 2021 and global industrial electricity tariffs rising ~12% YoY in 2023—boost demand for FAIST thermal insulation as firms seek lower overheads and higher process efficiency.

High energy costs drive manufacturers to buy turnkey systems that cut heat loss; studies show insulation can reduce thermal energy use by 10–25%, supporting FAIST’s advanced, energy-efficient components.

- EU industrial gas +30% (2024 vs 2021)

- Global industrial electricity +12% YoY (2023)

- Insulation reduces thermal energy use 10–25%

Labor cost inflation

The rising cost of specialized engineering and manufacturing labor in developed markets—wages up ~4.5% YoY in EU manufacturing in 2024—squeezes FAIST's operational budget, forcing a trade-off between premium German engineering and cost-efficient production.

Sustained wage inflation (e.g., Germany average hourly labor costs +5.1% in 2024) requires FAIST to accelerate automation and lean process gains to preserve margins.

- EU manufacturing wages +4.5% YoY (2024)

- Germany hourly labor costs +5.1% (2024)

- Target: 10–20% automation CAPEX to offset labor inflation

Capex surge, rising input costs squeeze margins—hedge FX as energy fuels insulation demand

Global capex and EV/semiconductor investment (+12% regional surge in 2024) bolster FAIST orders; global GDP +3.1% (2024). Steel +15% and aluminum +10% (2024) raised input costs, narrowing margins ~3pp. EUR FX moves (10% swing) materially affect bid competitiveness; hedging recommended. Energy/gas hikes (EU gas +30% vs 2021) increase demand for insulation (saves 10–25% thermal use); EU wages +4.5% (2024).

| Metric | 2024/2023 |

|---|---|

| Global GDP | +3.1% (2024) |

| Regional capex (EV/semicon) | +12% (2024) |

| Steel | +15% (2024) |

| Aluminum | +10% (2024) |

| EU gas vs 2021 | +30% |

| Insulation savings | 10–25% |

| EU wages | +4.5% (2024) |

Preview Before You Purchase

FAIST PESTLE Analysis

The preview shown here is the exact FAIST PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and structure visible here are identical to the file you’ll download immediately after payment, so what you see is exactly what you’ll own and apply.