Falck Renewables Porter's Five Forces Analysis

Don't Miss the Bigger Picture

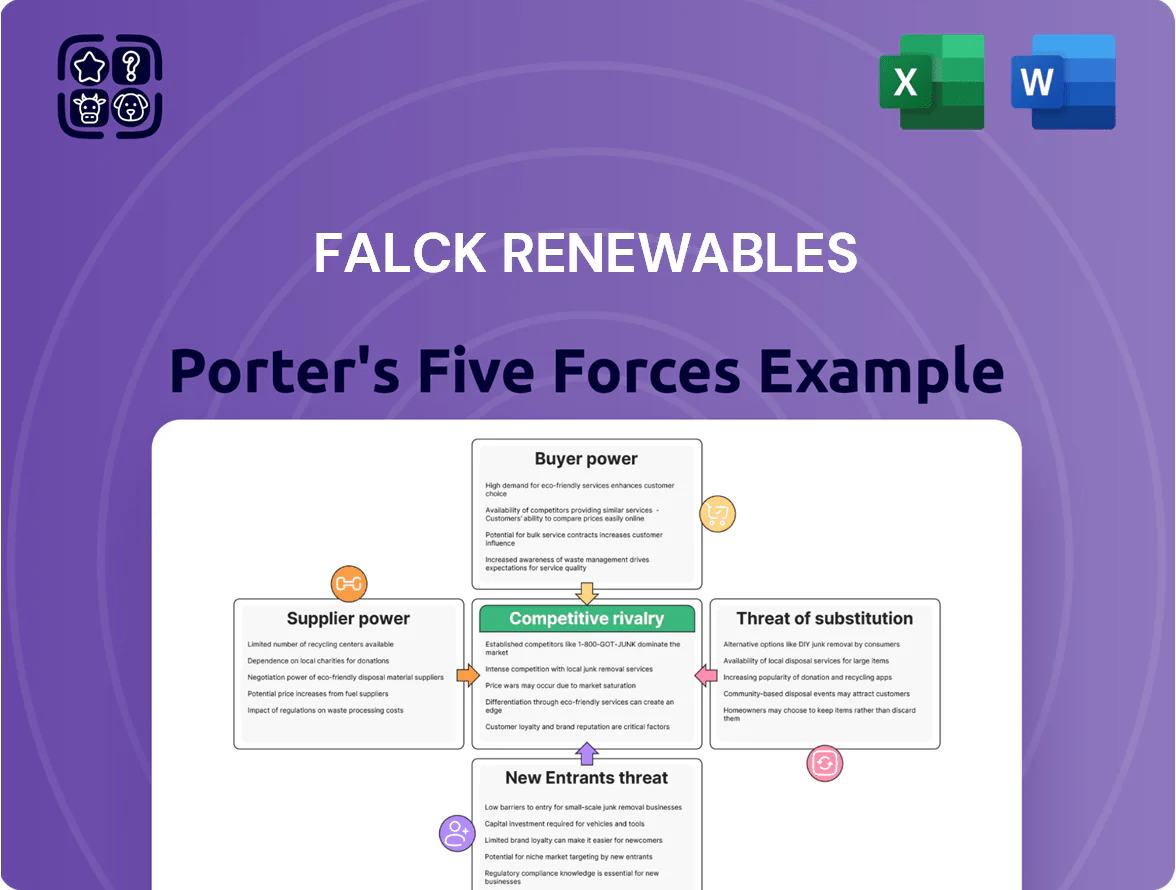

Falck Renewables faces moderate supplier power and regulatory-driven barriers, while competitive rivalry is intensifying as renewables scale and costs fall; buyer power and substitute threats remain manageable but warrant monitoring. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Falck Renewables’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Tier 1 Equipment Manufacturers

The market for high-capacity wind turbines and high-efficiency solar modules is dominated by a few OEMs—Vestas, Siemens Gamesa, and GE—who held about 55% of global wind turbine shipments in 2024, giving them strong bargaining power over Falck Renewables. Their proprietary tech drives project efficiency and O&M savings, making substitutions costly and time-consuming. By late 2025, supply constraints for rare earths tightened, pushing OEM lead times to 12–18 months and allowing price increases of 8–15% on turbine contracts. Falck faces higher capex risk and schedule exposure as a result.

Scarcity of Specialized Technical Labor

The global renewable build-out created a shortfall of about 600,000 skilled workers in 2024, so specialized contractors can push wages up 8–15% year-on-year; Falck Renewables faces higher O&M and construction costs as a result.

Volatility in Raw Material Costs

Suppliers of steel, copper and composites face global commodity swings—steel futures rose ~28% and copper ~35% in 2021–2022, and composite resin prices jumped ~20% in 2022, forcing Falck Renewables to absorb higher turbine tower and cable costs.

Strategic Control of Grid Connection Infrastructure

Strategic Control of Grid Connection Infrastructure raises supplier power for Falck Renewables because a few conglomerates (Siemens Energy, ABB, GE) dominated HV equipment supply, with global market shares ~60% in 2024 and typical margin premiums of 8–12% over peers.

These suppliers set strict technical specs and long lead times (often 12–24 months) and attach firm performance guarantees and liquidated-damage clauses, allowing higher prices and tight contract terms for project developers.

- High concentration: ~60% market share (2024)

- Lead times: 12–24 months

- Price premium: +8–12% margins

- Contract risk: strict guarantees, LD clauses

Landowner Leverage in Prime Locations

Landowners in zones with top-tier wind speeds or solar irradiance exercise strong leverage, driving up lease rates, royalty demands, or equity stakes; auction data from 2024 shows land lease premiums rose 18% year-on-year in key EU markets.

This competition for scarce prime real estate raises fixed project costs—land and access now account for up to 10–15% of upfront CAPEX on some 50–200 MW projects—eroding developer margins.

- Finite high-potential sites: multiple bidders

- Leverage tools: royalties, higher rent, equity

- 2024 lease premiums +18% in EU hotspots

- Land costs = 10–15% of CAPEX on mid-size projects

Supplier dominance squeezes wind project costs—higher prices, delays, and CAPEX hit

Suppliers (turbine OEMs, HV-equipment, specialty contractors, landowners) hold high bargaining power: OEMs ~55–60% share (2024), turbine lead times 12–18 months, price hikes +8–15% (2025); HV equipment market ~60% share with +8–12% premiums; skilled labor shortfall ~600,000 (2024) → wages +8–15% Y/Y; prime land adds 10–15% of CAPEX; strict guarantees raise contract risk.

| Supplier | Metric | 2024–25 |

|---|---|---|

| OEMs | Market share / lead time | 55–60% / 12–18m |

| HV equipment | Market share / margin premium | ~60% / +8–12% |

| Labor | Shortfall / wage rise | ~600k / +8–15% Y/Y |

| Land | Lease premium / CAPEX | +18% / 10–15% CAPEX |

What is included in the product

Tailored exclusively for Falck Renewables, this Porter’s Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive risks shaping its profitability and strategic positioning.

A one-sheet Porter's Five Forces summary for Falck Renewables—quickly highlights supplier, buyer, and regulatory pressures to speed strategic decisions.

Customers Bargaining Power

Influence of Government-Led Auctions

A large share of renewable revenues comes from government tenders and feed-in tariffs; in Europe about 40–60% of new wind and solar capacity in 2023 won auctioned contracts, forcing buyers into monopsony/oligopsony roles that cap prices and set strict delivery clauses. These auctions drove cleared prices down: EU onshore wind average auction price fell to ~EUR 45/MWh in 2023, so Falck Renewables must bid thinner margins to secure 10–15‑year contracted cashflows.

Corporate Power Purchase Agreements

Commoditization of Electricity

Electricity is a homogenous commodity: end customers cannot tell wind, solar or biomass apart, so buying hinges on price and reliability; in 2024 EU wholesale power prices ranged €50–€150/MWh, making cost decisive. This drives high buyer power as utilities and large corporate offtakers switch to lowest-cost suppliers on spot markets and PPAs. For Falck Renewables, lacking visible product differentiation raises churn risk unless it competes on price, hedging, or bundled services.

Wholesale Market Price Volatility

In merchant markets, wholesale power prices are set by grid supply and demand, limiting Falck Renewables’ pricing power; European Day-Ahead power prices averaged €84/MWh in 2024 versus €120/MWh in 2022, showing high volatility.

Large industrial buyers and utilities time purchases during high supply or use hedges—European utilities held 2024 forward hedges covering ~55% of expected load—reducing spot exposure and bargaining leverage for producers.

- 2024 EU day-ahead avg €84/MWh

- 2022 peak €120/MWh

- Utilities hedge ~55% load (2024)

- Producers can’t set independent prices

Strict Grid Operator Compliance

High customer power, low market prices and rising storage costs squeeze renewables margins

Customers hold high bargaining power: 40–60% EU auctioned renewables (2023) forced prices to ~€45/MWh; corporate PPAs hit $35–45/MWh (2024); EU day‑ahead avg €84/MWh (2024) vs €120 (2022); utilities hedge ~55% load (2024); storage CapEx €300–€450/MWh (2024) raises seller costs, squeezing Falck Renewables’ margins.

| Metric | 2023–24 |

|---|---|

| Auction share | 40–60% |

| Auction price | ~€45/MWh |

| Corp PPA | $35–45/MWh |

| Day‑ahead | €84/MWh |

| Hedge rate | ~55% |

| Storage CapEx | €300–450/MWh |

Full Version Awaits

Falck Renewables Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Falck Renewables you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy.

You're viewing the actual deliverable: a professionally written, complete analysis available for instant access after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Falck Renewables faces moderate supplier power and regulatory-driven barriers, while competitive rivalry is intensifying as renewables scale and costs fall; buyer power and substitute threats remain manageable but warrant monitoring. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Falck Renewables’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Tier 1 Equipment Manufacturers

The market for high-capacity wind turbines and high-efficiency solar modules is dominated by a few OEMs—Vestas, Siemens Gamesa, and GE—who held about 55% of global wind turbine shipments in 2024, giving them strong bargaining power over Falck Renewables. Their proprietary tech drives project efficiency and O&M savings, making substitutions costly and time-consuming. By late 2025, supply constraints for rare earths tightened, pushing OEM lead times to 12–18 months and allowing price increases of 8–15% on turbine contracts. Falck faces higher capex risk and schedule exposure as a result.

Scarcity of Specialized Technical Labor

The global renewable build-out created a shortfall of about 600,000 skilled workers in 2024, so specialized contractors can push wages up 8–15% year-on-year; Falck Renewables faces higher O&M and construction costs as a result.

Volatility in Raw Material Costs

Suppliers of steel, copper and composites face global commodity swings—steel futures rose ~28% and copper ~35% in 2021–2022, and composite resin prices jumped ~20% in 2022, forcing Falck Renewables to absorb higher turbine tower and cable costs.

Strategic Control of Grid Connection Infrastructure

Strategic Control of Grid Connection Infrastructure raises supplier power for Falck Renewables because a few conglomerates (Siemens Energy, ABB, GE) dominated HV equipment supply, with global market shares ~60% in 2024 and typical margin premiums of 8–12% over peers.

These suppliers set strict technical specs and long lead times (often 12–24 months) and attach firm performance guarantees and liquidated-damage clauses, allowing higher prices and tight contract terms for project developers.

- High concentration: ~60% market share (2024)

- Lead times: 12–24 months

- Price premium: +8–12% margins

- Contract risk: strict guarantees, LD clauses

Landowner Leverage in Prime Locations

Landowners in zones with top-tier wind speeds or solar irradiance exercise strong leverage, driving up lease rates, royalty demands, or equity stakes; auction data from 2024 shows land lease premiums rose 18% year-on-year in key EU markets.

This competition for scarce prime real estate raises fixed project costs—land and access now account for up to 10–15% of upfront CAPEX on some 50–200 MW projects—eroding developer margins.

- Finite high-potential sites: multiple bidders

- Leverage tools: royalties, higher rent, equity

- 2024 lease premiums +18% in EU hotspots

- Land costs = 10–15% of CAPEX on mid-size projects

Supplier dominance squeezes wind project costs—higher prices, delays, and CAPEX hit

Suppliers (turbine OEMs, HV-equipment, specialty contractors, landowners) hold high bargaining power: OEMs ~55–60% share (2024), turbine lead times 12–18 months, price hikes +8–15% (2025); HV equipment market ~60% share with +8–12% premiums; skilled labor shortfall ~600,000 (2024) → wages +8–15% Y/Y; prime land adds 10–15% of CAPEX; strict guarantees raise contract risk.

| Supplier | Metric | 2024–25 |

|---|---|---|

| OEMs | Market share / lead time | 55–60% / 12–18m |

| HV equipment | Market share / margin premium | ~60% / +8–12% |

| Labor | Shortfall / wage rise | ~600k / +8–15% Y/Y |

| Land | Lease premium / CAPEX | +18% / 10–15% CAPEX |

What is included in the product

Tailored exclusively for Falck Renewables, this Porter’s Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and disruptive risks shaping its profitability and strategic positioning.

A one-sheet Porter's Five Forces summary for Falck Renewables—quickly highlights supplier, buyer, and regulatory pressures to speed strategic decisions.

Customers Bargaining Power

Influence of Government-Led Auctions

A large share of renewable revenues comes from government tenders and feed-in tariffs; in Europe about 40–60% of new wind and solar capacity in 2023 won auctioned contracts, forcing buyers into monopsony/oligopsony roles that cap prices and set strict delivery clauses. These auctions drove cleared prices down: EU onshore wind average auction price fell to ~EUR 45/MWh in 2023, so Falck Renewables must bid thinner margins to secure 10–15‑year contracted cashflows.

Corporate Power Purchase Agreements

Commoditization of Electricity

Electricity is a homogenous commodity: end customers cannot tell wind, solar or biomass apart, so buying hinges on price and reliability; in 2024 EU wholesale power prices ranged €50–€150/MWh, making cost decisive. This drives high buyer power as utilities and large corporate offtakers switch to lowest-cost suppliers on spot markets and PPAs. For Falck Renewables, lacking visible product differentiation raises churn risk unless it competes on price, hedging, or bundled services.

Wholesale Market Price Volatility

In merchant markets, wholesale power prices are set by grid supply and demand, limiting Falck Renewables’ pricing power; European Day-Ahead power prices averaged €84/MWh in 2024 versus €120/MWh in 2022, showing high volatility.

Large industrial buyers and utilities time purchases during high supply or use hedges—European utilities held 2024 forward hedges covering ~55% of expected load—reducing spot exposure and bargaining leverage for producers.

- 2024 EU day-ahead avg €84/MWh

- 2022 peak €120/MWh

- Utilities hedge ~55% load (2024)

- Producers can’t set independent prices

Strict Grid Operator Compliance

High customer power, low market prices and rising storage costs squeeze renewables margins

Customers hold high bargaining power: 40–60% EU auctioned renewables (2023) forced prices to ~€45/MWh; corporate PPAs hit $35–45/MWh (2024); EU day‑ahead avg €84/MWh (2024) vs €120 (2022); utilities hedge ~55% load (2024); storage CapEx €300–€450/MWh (2024) raises seller costs, squeezing Falck Renewables’ margins.

| Metric | 2023–24 |

|---|---|

| Auction share | 40–60% |

| Auction price | ~€45/MWh |

| Corp PPA | $35–45/MWh |

| Day‑ahead | €84/MWh |

| Hedge rate | ~55% |

| Storage CapEx | €300–450/MWh |

Full Version Awaits

Falck Renewables Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Falck Renewables you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy.

You're viewing the actual deliverable: a professionally written, complete analysis available for instant access after payment.