Fannie Mae Business Model Canvas

Fannie Mae: Complete Business Model Canvas & Toolkit for Investors and Strategists

Unlock the full strategic blueprint behind Fannie Mae's business model—our in-depth Business Model Canvas maps value propositions, partner ecosystems, revenue drivers, and risk controls to show how the company scales and sustains market leadership; download the full Word & Excel package for a section-by-section breakdown ideal for investors, consultants, and strategists seeking actionable insights.

Partnerships

Primary Mortgage Lenders

Fannie Mae works with thousands of commercial banks, credit unions, and mortgage firms that originate loans and sell them to the enterprise; in 2024 these sellers accounted for roughly $2.1 trillion in acquisitions that funded Fannie Mae’s guarantee book. By buying loans, Fannie Mae lets originators reduce credit exposure and free up capital—enabling an estimated $500+ billion in new mortgage originations annually tied to its secondary-market activity.

Federal Housing Finance Agency

As conservator and primary regulator, the Federal Housing Finance Agency (FHFA) sets Fannie Mae’s capital, liquidity, and mission rules—mandating 2024 capital stress tests where Fannie reported $237 billion in retained mortgage book risk exposure and met required buffers. This oversight preserves market stability and enforces housing goals (affordable and multifamily targets), defining the legal and operational boundaries for the enterprise’s activities.

Global Institutional Investors

Fannie Mae taps a global investor base—pension funds, central banks, insurers—that held roughly $1.3 trillion of agency MBS at end-2024, providing vital liquidity that recycles into U.S. mortgages.

Preserving this funding depends on transparency, monthly disclosures, and the implicit credit support that underpins market confidence and tightens primary-secondary spreads.

Mortgage Servicers

Third-party mortgage servicers manage day-to-day loans in Fannie Mae’s portfolio—collecting borrower payments, running escrow accounts, and handling delinquencies and foreclosures—directly affecting asset quality and investor cash flows.

As of FY 2024, servicers handled roughly $2.3 trillion of Fannie Mae-related unpaid principal balance, and servicer performance metrics (e.g., 90+ day delinquency rates) correlate with RMBS coupon yields and credit loss assumptions.

- Servicers handle collections, escrow, delinquencies

- Performance affects asset quality and cash-flow timing

- FY 2024: ≈ $2.3 trillion UPB serviced

- 90+ day delinquency rates drive credit loss and yields

Technology and Data Providers

Strategic alliances with fintechs and data analytics firms improve Fannie Mae’s Desktop Underwriter and risk tools, enabling automation of credit checks and modernization of the mortgage lifecycle; by late 2025 these partnerships helped cut loan manufacturing defects by ~18% and increased automated underwriting acceptance to ~62% of deliveries.

- Reduced defects ~18% (2025)

- Automated underwriting ~62% of deliveries (2025)

- Faster credit decisions: median decision time <24 hrs

Fannie Mae ecosystem: $2.1T lenders, $237B FHFA risk, $1.3T MBS, $2.3T servicers, fintech gains

Fannie Mae partners with ~5,000 lenders (2024 sellers funded $2.1T), FHFA regulator (sets capital/liquidity—2024 stress tests, $237B retained risk), global investors holding $1.3T agency MBS (end-2024), servicers managing ~$2.3T UPB (FY2024), and fintechs improving underwriting (2025: defects −18%, automated acceptance ~62%).

| Partner | Key 2024–25 Metric |

|---|---|

| Lenders | $2.1T acquisitions (2024) |

| FHFA | $237B retained risk (2024) |

| Investors | $1.3T agency MBS (end‑2024) |

| Servicers | $2.3T UPB (FY2024) |

| Fintechs | Defects −18%, AU ~62% (2025) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Fannie Mae detailing customer segments, channels, value propositions, revenue and cost structures, key activities, resources, partnerships, and governance to reflect real-world mortgage finance operations and strategic priorities.

High-level view of Fannie Mae’s business model with editable cells, helping teams quickly map mortgage guarantee, capital markets, and risk-management functions. Great for boardrooms or training, saving hours of structuring while enabling easy comparison and collaborative adaptation.

Activities

Mortgage Acquisition and Securitization

Fannie Mae buys mortgages from lenders and pools them into mortgage-backed securities (MBS), turning illiquid home loans into standardized, tradable assets; in 2024 Fannie issued or guaranteed roughly $1.2 trillion in single-family MBS, supporting secondary market liquidity. Securitization lets Fannie back the 30-year fixed-rate mortgage by converting cash-flow from many borrowers into highly liquid securities sold to global investors.

Credit Risk Management

Fannie Mae continuously assesses borrower creditworthiness and collateral quality using models that in 2024 estimated single-family serious delinquency at 0.9% and projected default severities under stressed scenarios up to 25%; these forecasts inform capital overlays and pricing for its $3.5 trillion mortgage portfolio. Managing credit risk protects the company’s capital and preserves liquidity in the secondary market, keeping investor confidence and access to mortgage financing.

Issuing Credit Guarantees

Fannie Mae guarantees timely principal and interest on its mortgage-backed securities (MBS), absorbing borrower default risk so investors receive scheduled payments; this credit enhancement helped MBS yields trade within ~20–60 basis points of US Treasuries in 2024. This guarantee is the core value driver—2024 MBS outstanding backed by Fannie Mae totaled about $2.2 trillion, underpinning investor confidence and market liquidity.

Market Liquidity Support

By buying and guaranteeing mortgages in the secondary market, Fannie Mae keeps credit flowing nationwide through cycles—backstopping about $3.3 trillion in mortgage-backed securities outstanding as of Q4 2025 and supporting roughly 40% of US single-family originations in 2024.

This market liquidity support stabilizes housing finance in stress periods by replacing retreating private capital and helping sustain affordable monthly payments for millions.

- ~$3.3T MBS outstanding (Q4 2025)

- ~40% share of single-family originations (2024)

- Provides countercyclical funding in downturns

Regulatory Compliance and Reporting

Fannie Mae performs rigorous reporting and compliance to meet FHFA and Treasury rules, including maintaining capital buffers—$20.6 billion conservatorship capital requirement as of 2024—and meeting annual affordable housing goals (e.g., millions of affordable loans targeted) plus transparent SEC-style financial disclosures.

- Maintains $20.6B conservatorship capital target (2024)

- Meets FHFA/Treasury affordable housing targets annually

- Files comprehensive financial disclosures with investors and regulators

- Compliance required to keep GSE status and social license

Massive $3.3T MBS engine: 40% of originations, low 0.9% delinquencies

Buys/guarantees mortgages, pools into MBS ($3.3T outstanding Q4 2025), supports ~40% of 2024 single-family originations, guarantees timely P&I (MBS yields ~20–60 bps over Treasuries in 2024), manages credit (0.9% serious delinquency 2024) and holds conservatorship capital target $20.6B (2024).

| Metric | Value |

|---|---|

| MBS outstanding | $3.3T (Q4 2025) |

| Origination share | ~40% (2024) |

| Serious delinquency | 0.9% (2024) |

| Capital target | $20.6B (2024) |

What You See Is What You Get

Business Model Canvas

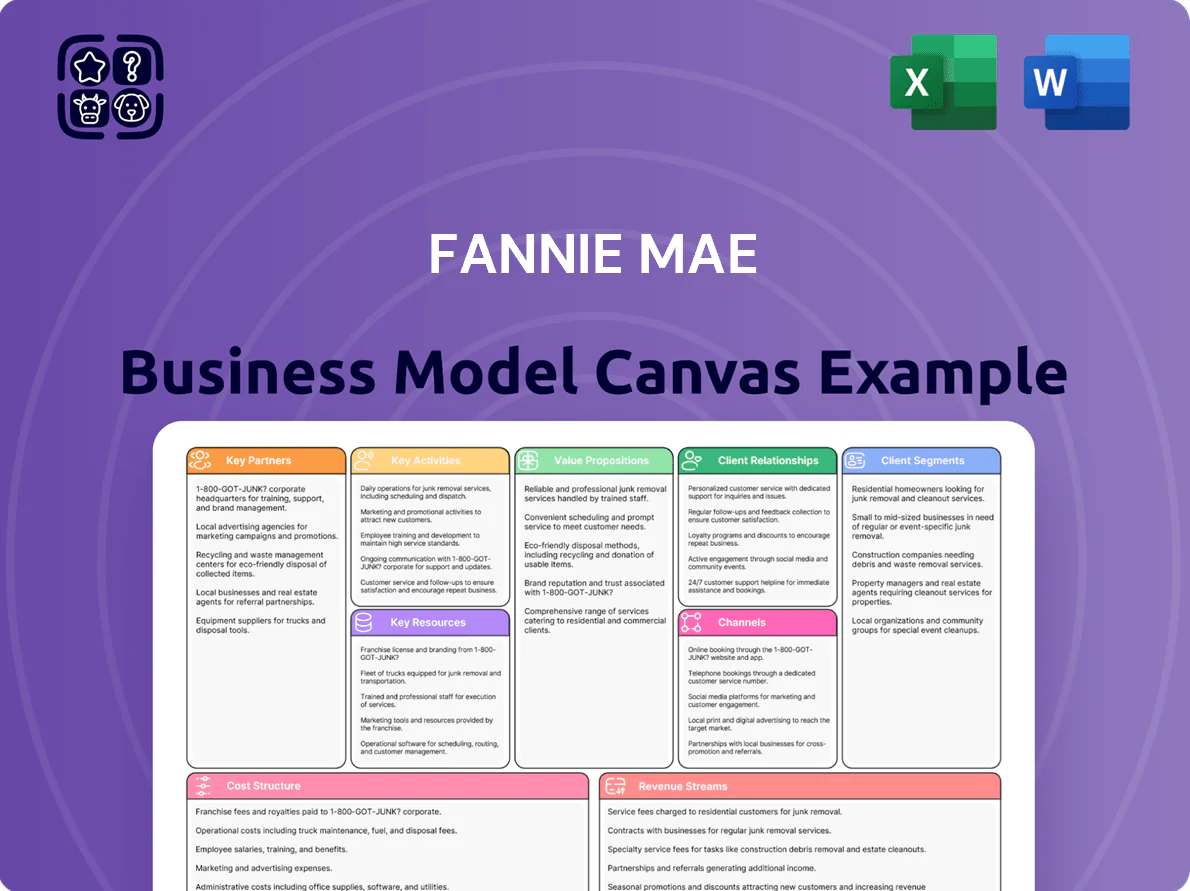

The document you're previewing is the exact Fannie Mae Business Model Canvas you’ll receive—no mockup, no filler—showing real sections from the final file.

When you purchase, you'll get this same complete, professionally formatted document ready to download and edit in Word and Excel.

We provide full transparency: what you see is what you’ll own, instantly accessible and presentation-ready upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Fannie Mae: Complete Business Model Canvas & Toolkit for Investors and Strategists

Unlock the full strategic blueprint behind Fannie Mae's business model—our in-depth Business Model Canvas maps value propositions, partner ecosystems, revenue drivers, and risk controls to show how the company scales and sustains market leadership; download the full Word & Excel package for a section-by-section breakdown ideal for investors, consultants, and strategists seeking actionable insights.

Partnerships

Primary Mortgage Lenders

Fannie Mae works with thousands of commercial banks, credit unions, and mortgage firms that originate loans and sell them to the enterprise; in 2024 these sellers accounted for roughly $2.1 trillion in acquisitions that funded Fannie Mae’s guarantee book. By buying loans, Fannie Mae lets originators reduce credit exposure and free up capital—enabling an estimated $500+ billion in new mortgage originations annually tied to its secondary-market activity.

Federal Housing Finance Agency

As conservator and primary regulator, the Federal Housing Finance Agency (FHFA) sets Fannie Mae’s capital, liquidity, and mission rules—mandating 2024 capital stress tests where Fannie reported $237 billion in retained mortgage book risk exposure and met required buffers. This oversight preserves market stability and enforces housing goals (affordable and multifamily targets), defining the legal and operational boundaries for the enterprise’s activities.

Global Institutional Investors

Fannie Mae taps a global investor base—pension funds, central banks, insurers—that held roughly $1.3 trillion of agency MBS at end-2024, providing vital liquidity that recycles into U.S. mortgages.

Preserving this funding depends on transparency, monthly disclosures, and the implicit credit support that underpins market confidence and tightens primary-secondary spreads.

Mortgage Servicers

Third-party mortgage servicers manage day-to-day loans in Fannie Mae’s portfolio—collecting borrower payments, running escrow accounts, and handling delinquencies and foreclosures—directly affecting asset quality and investor cash flows.

As of FY 2024, servicers handled roughly $2.3 trillion of Fannie Mae-related unpaid principal balance, and servicer performance metrics (e.g., 90+ day delinquency rates) correlate with RMBS coupon yields and credit loss assumptions.

- Servicers handle collections, escrow, delinquencies

- Performance affects asset quality and cash-flow timing

- FY 2024: ≈ $2.3 trillion UPB serviced

- 90+ day delinquency rates drive credit loss and yields

Technology and Data Providers

Strategic alliances with fintechs and data analytics firms improve Fannie Mae’s Desktop Underwriter and risk tools, enabling automation of credit checks and modernization of the mortgage lifecycle; by late 2025 these partnerships helped cut loan manufacturing defects by ~18% and increased automated underwriting acceptance to ~62% of deliveries.

- Reduced defects ~18% (2025)

- Automated underwriting ~62% of deliveries (2025)

- Faster credit decisions: median decision time <24 hrs

Fannie Mae ecosystem: $2.1T lenders, $237B FHFA risk, $1.3T MBS, $2.3T servicers, fintech gains

Fannie Mae partners with ~5,000 lenders (2024 sellers funded $2.1T), FHFA regulator (sets capital/liquidity—2024 stress tests, $237B retained risk), global investors holding $1.3T agency MBS (end-2024), servicers managing ~$2.3T UPB (FY2024), and fintechs improving underwriting (2025: defects −18%, automated acceptance ~62%).

| Partner | Key 2024–25 Metric |

|---|---|

| Lenders | $2.1T acquisitions (2024) |

| FHFA | $237B retained risk (2024) |

| Investors | $1.3T agency MBS (end‑2024) |

| Servicers | $2.3T UPB (FY2024) |

| Fintechs | Defects −18%, AU ~62% (2025) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Fannie Mae detailing customer segments, channels, value propositions, revenue and cost structures, key activities, resources, partnerships, and governance to reflect real-world mortgage finance operations and strategic priorities.

High-level view of Fannie Mae’s business model with editable cells, helping teams quickly map mortgage guarantee, capital markets, and risk-management functions. Great for boardrooms or training, saving hours of structuring while enabling easy comparison and collaborative adaptation.

Activities

Mortgage Acquisition and Securitization

Fannie Mae buys mortgages from lenders and pools them into mortgage-backed securities (MBS), turning illiquid home loans into standardized, tradable assets; in 2024 Fannie issued or guaranteed roughly $1.2 trillion in single-family MBS, supporting secondary market liquidity. Securitization lets Fannie back the 30-year fixed-rate mortgage by converting cash-flow from many borrowers into highly liquid securities sold to global investors.

Credit Risk Management

Fannie Mae continuously assesses borrower creditworthiness and collateral quality using models that in 2024 estimated single-family serious delinquency at 0.9% and projected default severities under stressed scenarios up to 25%; these forecasts inform capital overlays and pricing for its $3.5 trillion mortgage portfolio. Managing credit risk protects the company’s capital and preserves liquidity in the secondary market, keeping investor confidence and access to mortgage financing.

Issuing Credit Guarantees

Fannie Mae guarantees timely principal and interest on its mortgage-backed securities (MBS), absorbing borrower default risk so investors receive scheduled payments; this credit enhancement helped MBS yields trade within ~20–60 basis points of US Treasuries in 2024. This guarantee is the core value driver—2024 MBS outstanding backed by Fannie Mae totaled about $2.2 trillion, underpinning investor confidence and market liquidity.

Market Liquidity Support

By buying and guaranteeing mortgages in the secondary market, Fannie Mae keeps credit flowing nationwide through cycles—backstopping about $3.3 trillion in mortgage-backed securities outstanding as of Q4 2025 and supporting roughly 40% of US single-family originations in 2024.

This market liquidity support stabilizes housing finance in stress periods by replacing retreating private capital and helping sustain affordable monthly payments for millions.

- ~$3.3T MBS outstanding (Q4 2025)

- ~40% share of single-family originations (2024)

- Provides countercyclical funding in downturns

Regulatory Compliance and Reporting

Fannie Mae performs rigorous reporting and compliance to meet FHFA and Treasury rules, including maintaining capital buffers—$20.6 billion conservatorship capital requirement as of 2024—and meeting annual affordable housing goals (e.g., millions of affordable loans targeted) plus transparent SEC-style financial disclosures.

- Maintains $20.6B conservatorship capital target (2024)

- Meets FHFA/Treasury affordable housing targets annually

- Files comprehensive financial disclosures with investors and regulators

- Compliance required to keep GSE status and social license

Massive $3.3T MBS engine: 40% of originations, low 0.9% delinquencies

Buys/guarantees mortgages, pools into MBS ($3.3T outstanding Q4 2025), supports ~40% of 2024 single-family originations, guarantees timely P&I (MBS yields ~20–60 bps over Treasuries in 2024), manages credit (0.9% serious delinquency 2024) and holds conservatorship capital target $20.6B (2024).

| Metric | Value |

|---|---|

| MBS outstanding | $3.3T (Q4 2025) |

| Origination share | ~40% (2024) |

| Serious delinquency | 0.9% (2024) |

| Capital target | $20.6B (2024) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Fannie Mae Business Model Canvas you’ll receive—no mockup, no filler—showing real sections from the final file.

When you purchase, you'll get this same complete, professionally formatted document ready to download and edit in Word and Excel.

We provide full transparency: what you see is what you’ll own, instantly accessible and presentation-ready upon purchase.