Fannie Mae PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, housing-market cycles, and technological disruption are reshaping Fannie Mae’s strategy and risk profile; our concise PESTLE snapshot highlights the key external forces you need to monitor. Purchase the full PESTLE analysis for a complete, actionable breakdown—formatted for immediate use in investment memos, strategy decks, or board briefings.

Political factors

Conservatorship Status

Fannie Mae remained under FHFA conservatorship through late 2025, tying strategic choices to executive branch priorities and federal housing policy shifts; the conservatorship has conserved $112.5 billion in cumulative dividends to Treasury since 2008 and constrained capital deployment.

Federal Housing Policy

The administration’s push for affordability reinforces Fannie Mae’s mission-driven goals and duty-to-serve obligations, directing $2.5B in 2024-25 initiatives toward low-income and affordable housing programs; recent electoral shifts have prompted potential legislative changes that could expand support for first-time buyers, impacting guarantee fee policies and purchase caps; political pressure forces Fannie Mae to balance broader credit access with maintaining a 2025 CET1-like capital resilience and caution in credit risk standards.

FHFA Oversight

The Federal Housing Finance Agency controls Fannie Mae’s executive pay, capital requirements and eligible product scope; as of 2025 FHFA set minimum capital buffer guidance targeting a 4.5% risk-based requirement and tight limits on high‑LTV products. Changes in FHFA leadership have often triggered rapid underwriting shifts or new guarantee fee (g‑fee) regimes—g‑fees rose ~15 basis points industry‑wide in 2024 after policy reviews. This supervisory relationship is the dominant determinant of Fannie Mae’s long‑term business model and return on equity targets.

GSE Reform Legislation

Ongoing Congressional debates over GSE reform keep long-term structure of the secondary mortgage market uncertain; as of 2025, Fannie Mae and Freddie Mac remain in conservatorship with combined retained portfolios and mortgage guarantees exceeding $5.6 trillion, fueling policy stakes.

Proposals to formalize federal backing versus privatization materially influence investor confidence in MBS yields and spreads; since 2022 MBS spreads have shown heightened volatility tied to reform rhetoric, with RMBS spreads widening by ~15–25 basis points during key hearings.

Political gridlock has repeatedly stalled legislation, maintaining de facto government support and taxpayer exposure—conservatorship status persists despite over a decade of reform talks and no enacted permanent framework.

- Combined Fannie/Freddie guarantees ≈ $5.6 trillion (2025)

- MBS spreads moved ~15–25 bps on reform news (2022–2025)

- Conservatorship ongoing since 2008; no permanent reform passed

International Relations

International relations affect global demand for U.S. Agency mortgage-backed securities (MBS); foreign holdings stood at about $2.6 trillion in U.S. Treasuries and agencies combined as of Q4 2025, reflecting sensitivity to diplomatic trust and financial stability perceptions.

Political tensions can trigger volatility if foreign central banks or sovereign wealth funds cut agency MBS allocations—foreign official holdings of U.S. agencies fell 3.1% in 2024 during geopolitical strains.

Preserving agency MBS as safe-haven assets is a policy priority, with U.S. officials citing their role in market stability after foreign demand fluctuations in 2022–2025.

- Foreign official holdings ~ $2.6T (Q4 2025)

- Agency holdings down 3.1% in 2024 amid tensions

- Safe-haven status central to U.S. policy 2022–2025

FHFA Conservatorship Keeps Fannie Tied to Policy as GSE Guarantees Hit $5.6T

FHFA conservatorship through 2025 ties Fannie Mae to federal housing priorities, limiting capital deployment despite $112.5B in cumulative Treasury dividends since 2008; combined GSE guarantees ≈ $5.6T (2025). Political pushes for affordability directed $2.5B to low‑income programs (2024–25) and drove ~15 bps g‑fee rise in 2024; MBS spreads moved 15–25 bps on reform news (2022–25).

| Metric | Value |

|---|---|

| Cumulative dividends to Treasury | $112.5B (2008–2025) |

| Combined GSE guarantees | $5.6T (2025) |

| Affordability funding | $2.5B (2024–25) |

| G‑fee change | +~15 bps (2024) |

| MBS spread volatility | ~15–25 bps (2022–25) |

What is included in the product

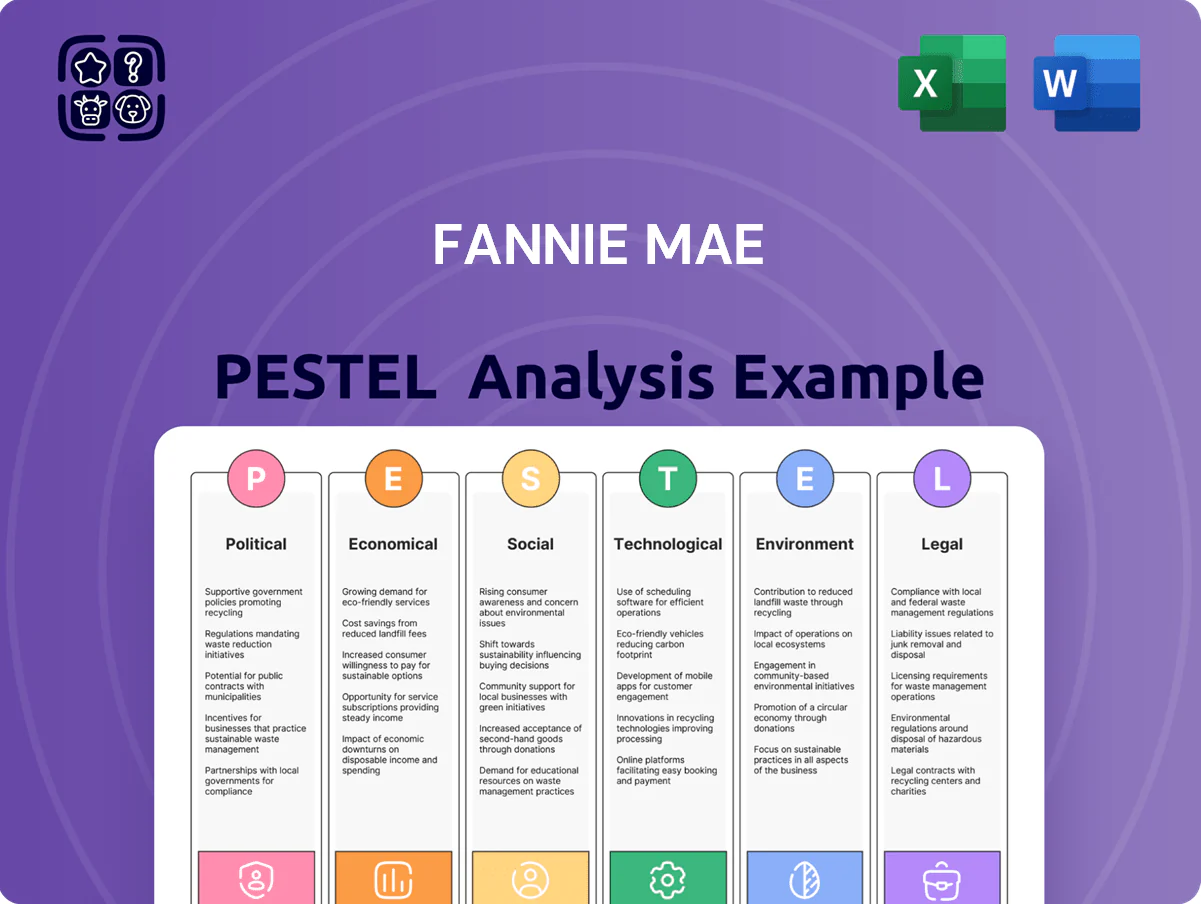

Explores how macro-environmental factors specifically impact Fannie Mae across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to surface risks and opportunities.

Condenses Fannie Mae's full PESTLE into a single, easily shareable summary—visually segmented by category and written in clear language—so teams can quickly align on external risks, market positioning, and regional nuances during meetings or client presentations.

Economic factors

Interest Rate Volatility

Fluctuations in the Federal Funds Rate in 2025—which ranged from 5.25% to 5.50% in Q1 and saw policy commentary pointing to potential cuts later in the year—drove a 12% year‑over‑year decline in mortgage applications and a 28% drop in refinance activity through June 2025, directly pressuring originations for Fannie Mae.

Higher market rates compressed net interest margins and reduced new-loan supply, with mortgage purchase volumes down roughly 15% YTD, limiting Fannie Mae’s pool for purchase and securitization.

To manage shifting yield curves and hedging costs that rose ~40% vs. 2024, the enterprise must deploy sophisticated interest‑rate hedges, duration management, and counterparty diversification to protect earnings and capital.

Inflationary Pressures

Persistent inflation has pushed US construction costs up about 18% from 2019–2023, squeezing housing supply and affordability as median home prices rose ~25% over the same period; higher living costs and rising 2024–25 consumer price trends risk worsening borrower debt-to-income ratios and pressure credit quality in Fannie Mae’s loan portfolio. Economic instability could raise default rates, threatening the guarantee business that relies on low delinquencies.

Housing Supply Constraints

Secondary Market Liquidity

Secondary market liquidity: institutional demand for agency MBS sets pricing and mortgage credit availability; in 2024 agency MBS holdings by US mutual funds and ETFs exceeded $2.3 trillion, driving spread compression. Economic downturns or liquidity shocks can widen TBM spreads—2023 peak TBA spread volatility raised funding costs markedly, increasing Fannie Mae's guarantee fee pressure. Maintaining an efficient To-Be-Announced market is central to its mission.

- Institutional MBS demand (> $2.3T in 2024) influences pricing

- Liquidity crunches widen TBA spreads, raising funding costs

- Efficient TBA market is core to Fannie Mae's role

Labor Market Conditions

National employment and wage growth drive mortgage repayment capacity and homebuying; as of Q4 2025 US unemployment was 3.7% and average hourly earnings rose 4.1% year-over-year, supporting demand and borrower cash flows for Fannie Mae.

A robust labor market reduces loan modifications and foreclosures, stabilizing Fannie Mae’s guarantee revenues, while a sharp unemployment uptick would increase credit losses and strain guarantee obligations.

- Unemployment 3.7% (Q4 2025)

- Average hourly earnings +4.1% YoY (Q4 2025)

- Lower foreclosures/loan mods when employment strong

- Unemployment spike = systemic credit risk

Higher rates curb originations; tight supply lifts prices and credit-duration risk

Rising 2024–25 rates and higher hedging costs cut originations (~15% purchase decline YTD, 28% refinance drop through Jun‑25), while tight housing supply (1.1 months inventory in 2023) and higher prices (median $390,600 in 2024) raised loan sizes but reduced volumes, increasing guarantee-duration and credit-risk exposure; strong labor (unemp 3.7% Q4‑25; AHE +4.1% YoY) partly offsets credit pressure.

| Metric | Value |

|---|---|

| Purchase volumes YTD | -15% |

| Refinance activity (through Jun‑25) | -28% |

| Inventory (2023) | 1.1 months |

| Median home price (2024) | $390,600 |

| Unemployment (Q4‑25) | 3.7% |

| AHE YoY (Q4‑25) | +4.1% |

Preview Before You Purchase

Fannie Mae PESTLE Analysis

The preview shown here is the exact Fannie Mae PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, housing-market cycles, and technological disruption are reshaping Fannie Mae’s strategy and risk profile; our concise PESTLE snapshot highlights the key external forces you need to monitor. Purchase the full PESTLE analysis for a complete, actionable breakdown—formatted for immediate use in investment memos, strategy decks, or board briefings.

Political factors

Conservatorship Status

Fannie Mae remained under FHFA conservatorship through late 2025, tying strategic choices to executive branch priorities and federal housing policy shifts; the conservatorship has conserved $112.5 billion in cumulative dividends to Treasury since 2008 and constrained capital deployment.

Federal Housing Policy

The administration’s push for affordability reinforces Fannie Mae’s mission-driven goals and duty-to-serve obligations, directing $2.5B in 2024-25 initiatives toward low-income and affordable housing programs; recent electoral shifts have prompted potential legislative changes that could expand support for first-time buyers, impacting guarantee fee policies and purchase caps; political pressure forces Fannie Mae to balance broader credit access with maintaining a 2025 CET1-like capital resilience and caution in credit risk standards.

FHFA Oversight

The Federal Housing Finance Agency controls Fannie Mae’s executive pay, capital requirements and eligible product scope; as of 2025 FHFA set minimum capital buffer guidance targeting a 4.5% risk-based requirement and tight limits on high‑LTV products. Changes in FHFA leadership have often triggered rapid underwriting shifts or new guarantee fee (g‑fee) regimes—g‑fees rose ~15 basis points industry‑wide in 2024 after policy reviews. This supervisory relationship is the dominant determinant of Fannie Mae’s long‑term business model and return on equity targets.

GSE Reform Legislation

Ongoing Congressional debates over GSE reform keep long-term structure of the secondary mortgage market uncertain; as of 2025, Fannie Mae and Freddie Mac remain in conservatorship with combined retained portfolios and mortgage guarantees exceeding $5.6 trillion, fueling policy stakes.

Proposals to formalize federal backing versus privatization materially influence investor confidence in MBS yields and spreads; since 2022 MBS spreads have shown heightened volatility tied to reform rhetoric, with RMBS spreads widening by ~15–25 basis points during key hearings.

Political gridlock has repeatedly stalled legislation, maintaining de facto government support and taxpayer exposure—conservatorship status persists despite over a decade of reform talks and no enacted permanent framework.

- Combined Fannie/Freddie guarantees ≈ $5.6 trillion (2025)

- MBS spreads moved ~15–25 bps on reform news (2022–2025)

- Conservatorship ongoing since 2008; no permanent reform passed

International Relations

International relations affect global demand for U.S. Agency mortgage-backed securities (MBS); foreign holdings stood at about $2.6 trillion in U.S. Treasuries and agencies combined as of Q4 2025, reflecting sensitivity to diplomatic trust and financial stability perceptions.

Political tensions can trigger volatility if foreign central banks or sovereign wealth funds cut agency MBS allocations—foreign official holdings of U.S. agencies fell 3.1% in 2024 during geopolitical strains.

Preserving agency MBS as safe-haven assets is a policy priority, with U.S. officials citing their role in market stability after foreign demand fluctuations in 2022–2025.

- Foreign official holdings ~ $2.6T (Q4 2025)

- Agency holdings down 3.1% in 2024 amid tensions

- Safe-haven status central to U.S. policy 2022–2025

FHFA Conservatorship Keeps Fannie Tied to Policy as GSE Guarantees Hit $5.6T

FHFA conservatorship through 2025 ties Fannie Mae to federal housing priorities, limiting capital deployment despite $112.5B in cumulative Treasury dividends since 2008; combined GSE guarantees ≈ $5.6T (2025). Political pushes for affordability directed $2.5B to low‑income programs (2024–25) and drove ~15 bps g‑fee rise in 2024; MBS spreads moved 15–25 bps on reform news (2022–25).

| Metric | Value |

|---|---|

| Cumulative dividends to Treasury | $112.5B (2008–2025) |

| Combined GSE guarantees | $5.6T (2025) |

| Affordability funding | $2.5B (2024–25) |

| G‑fee change | +~15 bps (2024) |

| MBS spread volatility | ~15–25 bps (2022–25) |

What is included in the product

Explores how macro-environmental factors specifically impact Fannie Mae across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to surface risks and opportunities.

Condenses Fannie Mae's full PESTLE into a single, easily shareable summary—visually segmented by category and written in clear language—so teams can quickly align on external risks, market positioning, and regional nuances during meetings or client presentations.

Economic factors

Interest Rate Volatility

Fluctuations in the Federal Funds Rate in 2025—which ranged from 5.25% to 5.50% in Q1 and saw policy commentary pointing to potential cuts later in the year—drove a 12% year‑over‑year decline in mortgage applications and a 28% drop in refinance activity through June 2025, directly pressuring originations for Fannie Mae.

Higher market rates compressed net interest margins and reduced new-loan supply, with mortgage purchase volumes down roughly 15% YTD, limiting Fannie Mae’s pool for purchase and securitization.

To manage shifting yield curves and hedging costs that rose ~40% vs. 2024, the enterprise must deploy sophisticated interest‑rate hedges, duration management, and counterparty diversification to protect earnings and capital.

Inflationary Pressures

Persistent inflation has pushed US construction costs up about 18% from 2019–2023, squeezing housing supply and affordability as median home prices rose ~25% over the same period; higher living costs and rising 2024–25 consumer price trends risk worsening borrower debt-to-income ratios and pressure credit quality in Fannie Mae’s loan portfolio. Economic instability could raise default rates, threatening the guarantee business that relies on low delinquencies.

Housing Supply Constraints

Secondary Market Liquidity

Secondary market liquidity: institutional demand for agency MBS sets pricing and mortgage credit availability; in 2024 agency MBS holdings by US mutual funds and ETFs exceeded $2.3 trillion, driving spread compression. Economic downturns or liquidity shocks can widen TBM spreads—2023 peak TBA spread volatility raised funding costs markedly, increasing Fannie Mae's guarantee fee pressure. Maintaining an efficient To-Be-Announced market is central to its mission.

- Institutional MBS demand (> $2.3T in 2024) influences pricing

- Liquidity crunches widen TBA spreads, raising funding costs

- Efficient TBA market is core to Fannie Mae's role

Labor Market Conditions

National employment and wage growth drive mortgage repayment capacity and homebuying; as of Q4 2025 US unemployment was 3.7% and average hourly earnings rose 4.1% year-over-year, supporting demand and borrower cash flows for Fannie Mae.

A robust labor market reduces loan modifications and foreclosures, stabilizing Fannie Mae’s guarantee revenues, while a sharp unemployment uptick would increase credit losses and strain guarantee obligations.

- Unemployment 3.7% (Q4 2025)

- Average hourly earnings +4.1% YoY (Q4 2025)

- Lower foreclosures/loan mods when employment strong

- Unemployment spike = systemic credit risk

Higher rates curb originations; tight supply lifts prices and credit-duration risk

Rising 2024–25 rates and higher hedging costs cut originations (~15% purchase decline YTD, 28% refinance drop through Jun‑25), while tight housing supply (1.1 months inventory in 2023) and higher prices (median $390,600 in 2024) raised loan sizes but reduced volumes, increasing guarantee-duration and credit-risk exposure; strong labor (unemp 3.7% Q4‑25; AHE +4.1% YoY) partly offsets credit pressure.

| Metric | Value |

|---|---|

| Purchase volumes YTD | -15% |

| Refinance activity (through Jun‑25) | -28% |

| Inventory (2023) | 1.1 months |

| Median home price (2024) | $390,600 |

| Unemployment (Q4‑25) | 3.7% |

| AHE YoY (Q4‑25) | +4.1% |

Preview Before You Purchase

Fannie Mae PESTLE Analysis

The preview shown here is the exact Fannie Mae PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.