Fanuc Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

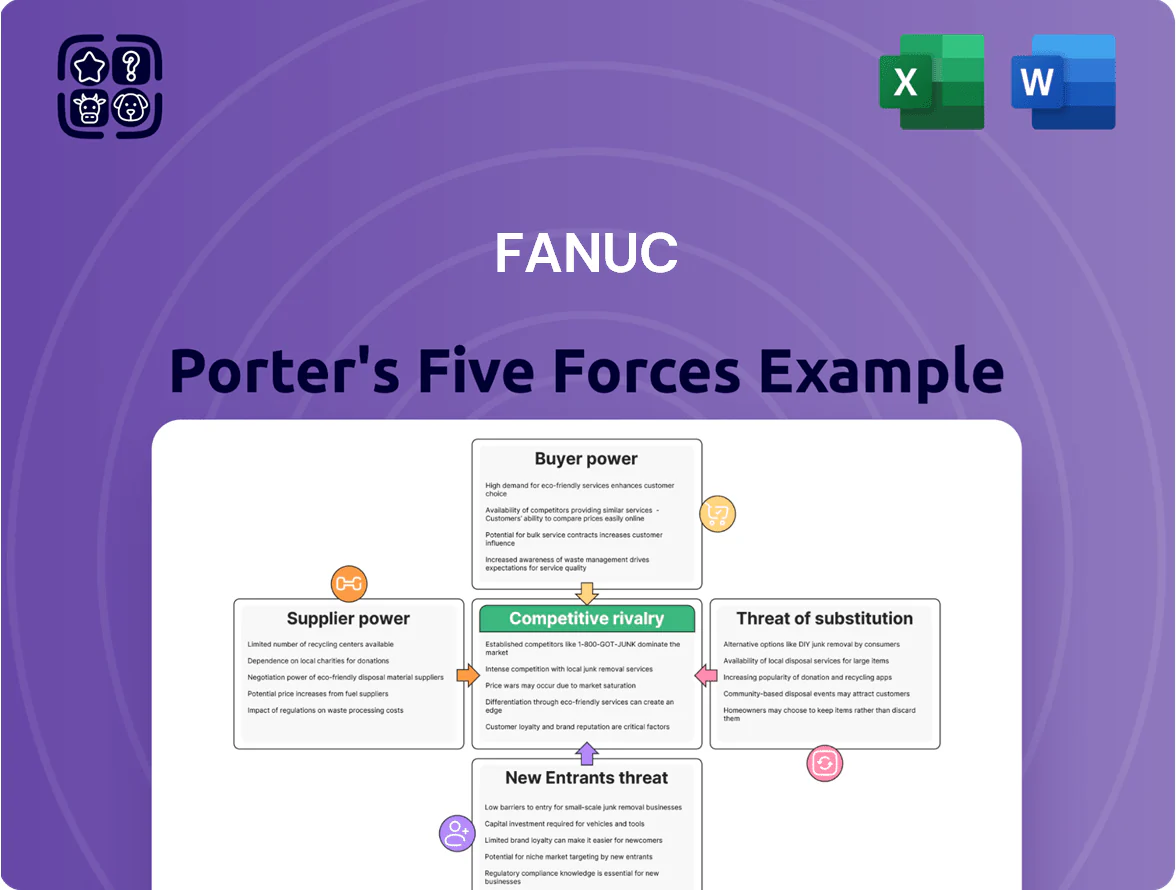

Fanuc faces moderate rivalry from global automation players, strong supplier power in specialized components, and growing buyer expectations for integrated solutions—while high entry barriers and limited substitutes support its pricing strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fanuc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

Fanuc vertically integrates by producing its own servo motors, encoders, and sensors, cutting external vendor dependence and lowering supplier bargaining power.

In 2024 Fanuc reported operating margin of ~27% and gross margin of ~58%, metrics supported by in‑house component production that trims input costs and boosts pricing leverage.

This control over critical parts shortens lead times and inventory days; Fanuc’s ROE of ~21% in FY2024 shows the financial payoff versus peers who outsource key components.

Semiconductor Dependency

Specialized Raw Materials

Production of Fanuc's servo motors relies on rare earths like neodymium and dysprosium; China supplied ~60–70% of global rare-earth oxide in 2024, driving price swings up 25% year-over-year in 2024 and raising input-cost risk for Fanuc.

Because these minerals are essential, upstream suppliers exert notable bargaining power over Fanuc's cost base, potentially compressing gross margins if spot prices spike.

Fanuc mitigates this via diversified sourcing—contracts in Japan, Australia, and recycling—and material science R&D that cut specific rare-earth use by ~10–15% in prototype motors in 2023–2024.

Energy and Utility Costs

As a mass-automation manufacturer with large factories in Japan, Fanuc is sensitive to regional energy pricing; Japan industrial electricity averaged about 24.5 JPY/kWh (2024 METI data), higher than OECD peers, so utility costs materially affect COGS during high-volume runs.

Energy price volatility—spot LNG and power peak events—can raise variable production costs; Fanuc either absorbs these or passes them to customers, since utilities are non-negotiable suppliers.

- Japan industrial power ~24.5 JPY/kWh (2024)

- High production weeks amplify COGS exposure

- Utilities = non-negotiable, limited bargaining leverage

- Pass-through risk to pricing and margins

Logistics and Global Shipping

- Specialized carriers limited: ~15–25%

- Airfreight spike: +22% (2023–24)

- Special surcharges: +8–12%

- Higher SLA leverage → raised logistics OPEX

Fanuc: high margins and vertical control, but semiconductor & rare-earth concentration risks

Fanuc’s vertical integration lowers supplier power—own servo, encoder, sensor production; FY2024 gross ~58%, operating ~27%, ROE ~21%—but reliance on a few semiconductor suppliers and China-dominated rare earths (60–70% supply in 2024) preserves concentration risk; multiyear chip deals cover ~70% of needs by late 2025; chip costs ≈12% BOM; Japan power ~24.5 JPY/kWh (2024).

| Metric | Value |

|---|---|

| Gross margin FY2024 | ~58% |

| Operating margin FY2024 | ~27% |

| ROE FY2024 | ~21% |

| Rare-earth supply (China, 2024) | 60–70% |

| Chip coverage (late 2025) | ~70% |

| Chip cost share BOM FY2024 | ~12% |

| Japan industrial power (2024) | 24.5 JPY/kWh |

What is included in the product

Tailored Porter's Five Forces assessment for Fanuc, uncovering competitive pressures, buyer and supplier influence, entry barriers and substitute threats, with strategic insights on how these forces shape Fanuc’s pricing power, profitability, and market defenses.

Concise Porter's Five Forces snapshot tailored for Fanuc—quickly spot competitive pressures and relief strategies to support faster, confident decisions.

Customers Bargaining Power

High Switching Costs

Customers using Fanuc’s proprietary CNC and programming environment face massive retraining costs—estimates show shop-floor retraining can exceed $50,000 per line and 4–8 weeks of downtime—creating a lock-in that often spans the 10–20 year machinery lifecycle. This operational embedding reduces buyers’ bargaining power, so firms rarely negotiate solely on price or credibly threaten switching, which helps Fanuc sustain aftermarket parts and service margins above industry averages (20–40%).

Sector Concentration

A large portion of FANUC’s revenue comes from automotive and electronics OEMs; in FY2024 FANUC reported ¥593.6bn in machine tool and robot sales, with roughly 45–55% tied to those sectors, so a few global buyers hold outsized share. These OEMs order high volumes, demand customization, and secure steep volume discounts, pressuring margins on bulk contracts. Their input shapes FANUC’s roadmap—new robot cadence and IPC features often track top-customer specs.

Demand for Open Architecture

By 2025, 62% of manufacturers surveyed by McKinsey prefer open, interoperable software for smart factories, pressuring Fanuc to ease proprietary locks and adopt standards like OPC UA and ROS 2.

Customers use open-architecture demands as leverage in procurement; 28% of recent automation contracts included price discounts or integration clauses tied to third-party compatibility.

Economic Sensitivity

The bargaining power of customers for Fanuc shifts with the global economic cycle and capex budgets; in 2024 global manufacturing investment fell about 3.5% year-over-year, pressuring buyers to delay automation purchases.

With higher interest rates in 2023–24 (US Fed funds peak ~5.25% in 2023) customers pushed for financing and longer payment terms, forcing Fanuc to add service bundles and leasing options to protect its order backlog.

- Manufacturing capex down ~3.5% in 2024

- Fed funds peak ~5.25% (2023)

- Fanuc offers financing, service bundles, leases

After-sales Service Dependency

Because Fanuc robots and CNC systems directly affect factory uptime, customers rely on Fanuc for specialized maintenance and OEM spare parts, which cuts their post-sale bargaining power; Fanuc reported service revenue of ¥189.4 billion in FY2024, showing recurring dependence.

Large buyers still secure leverage by negotiating comprehensive SLAs (response times, parts price caps); in 2024 some global auto OEMs locked multi-year SLAs reducing service cost volatility by ~15% over five years.

High switching costs cushion Fanuc, but OEM discounts & open standards boost buyer leverage

Customers’ bargaining power is limited by high switching costs (retraining >$50,000 and 4–8 weeks downtime) and Fanuc’s ¥189.4B service revenue (FY2024), but large OEMs (45–55% of machine/robot sales, FY2024) extract volume discounts and SLAs (~15% service cost cap). Macro cycles (capex −3.5% in 2024) and demand for open standards (62% preferring interoperability by 2025) increase buyer leverage.

| Metric | Value |

|---|---|

| Service rev FY2024 | ¥189.4B |

| Machine/robot sales FY2024 share (auto/elect) | 45–55% |

| Retraining cost | >$50,000 |

| Capex change 2024 | −3.5% |

| Interoperability preference 2025 | 62% |

Preview the Actual Deliverable

Fanuc Porter's Five Forces Analysis

This preview shows the exact Fanuc Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or excerpts: this is the final, ready-to-use analysis—instant access upon completion of payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Fanuc faces moderate rivalry from global automation players, strong supplier power in specialized components, and growing buyer expectations for integrated solutions—while high entry barriers and limited substitutes support its pricing strength.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fanuc’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

Fanuc vertically integrates by producing its own servo motors, encoders, and sensors, cutting external vendor dependence and lowering supplier bargaining power.

In 2024 Fanuc reported operating margin of ~27% and gross margin of ~58%, metrics supported by in‑house component production that trims input costs and boosts pricing leverage.

This control over critical parts shortens lead times and inventory days; Fanuc’s ROE of ~21% in FY2024 shows the financial payoff versus peers who outsource key components.

Semiconductor Dependency

Specialized Raw Materials

Production of Fanuc's servo motors relies on rare earths like neodymium and dysprosium; China supplied ~60–70% of global rare-earth oxide in 2024, driving price swings up 25% year-over-year in 2024 and raising input-cost risk for Fanuc.

Because these minerals are essential, upstream suppliers exert notable bargaining power over Fanuc's cost base, potentially compressing gross margins if spot prices spike.

Fanuc mitigates this via diversified sourcing—contracts in Japan, Australia, and recycling—and material science R&D that cut specific rare-earth use by ~10–15% in prototype motors in 2023–2024.

Energy and Utility Costs

As a mass-automation manufacturer with large factories in Japan, Fanuc is sensitive to regional energy pricing; Japan industrial electricity averaged about 24.5 JPY/kWh (2024 METI data), higher than OECD peers, so utility costs materially affect COGS during high-volume runs.

Energy price volatility—spot LNG and power peak events—can raise variable production costs; Fanuc either absorbs these or passes them to customers, since utilities are non-negotiable suppliers.

- Japan industrial power ~24.5 JPY/kWh (2024)

- High production weeks amplify COGS exposure

- Utilities = non-negotiable, limited bargaining leverage

- Pass-through risk to pricing and margins

Logistics and Global Shipping

- Specialized carriers limited: ~15–25%

- Airfreight spike: +22% (2023–24)

- Special surcharges: +8–12%

- Higher SLA leverage → raised logistics OPEX

Fanuc: high margins and vertical control, but semiconductor & rare-earth concentration risks

Fanuc’s vertical integration lowers supplier power—own servo, encoder, sensor production; FY2024 gross ~58%, operating ~27%, ROE ~21%—but reliance on a few semiconductor suppliers and China-dominated rare earths (60–70% supply in 2024) preserves concentration risk; multiyear chip deals cover ~70% of needs by late 2025; chip costs ≈12% BOM; Japan power ~24.5 JPY/kWh (2024).

| Metric | Value |

|---|---|

| Gross margin FY2024 | ~58% |

| Operating margin FY2024 | ~27% |

| ROE FY2024 | ~21% |

| Rare-earth supply (China, 2024) | 60–70% |

| Chip coverage (late 2025) | ~70% |

| Chip cost share BOM FY2024 | ~12% |

| Japan industrial power (2024) | 24.5 JPY/kWh |

What is included in the product

Tailored Porter's Five Forces assessment for Fanuc, uncovering competitive pressures, buyer and supplier influence, entry barriers and substitute threats, with strategic insights on how these forces shape Fanuc’s pricing power, profitability, and market defenses.

Concise Porter's Five Forces snapshot tailored for Fanuc—quickly spot competitive pressures and relief strategies to support faster, confident decisions.

Customers Bargaining Power

High Switching Costs

Customers using Fanuc’s proprietary CNC and programming environment face massive retraining costs—estimates show shop-floor retraining can exceed $50,000 per line and 4–8 weeks of downtime—creating a lock-in that often spans the 10–20 year machinery lifecycle. This operational embedding reduces buyers’ bargaining power, so firms rarely negotiate solely on price or credibly threaten switching, which helps Fanuc sustain aftermarket parts and service margins above industry averages (20–40%).

Sector Concentration

A large portion of FANUC’s revenue comes from automotive and electronics OEMs; in FY2024 FANUC reported ¥593.6bn in machine tool and robot sales, with roughly 45–55% tied to those sectors, so a few global buyers hold outsized share. These OEMs order high volumes, demand customization, and secure steep volume discounts, pressuring margins on bulk contracts. Their input shapes FANUC’s roadmap—new robot cadence and IPC features often track top-customer specs.

Demand for Open Architecture

By 2025, 62% of manufacturers surveyed by McKinsey prefer open, interoperable software for smart factories, pressuring Fanuc to ease proprietary locks and adopt standards like OPC UA and ROS 2.

Customers use open-architecture demands as leverage in procurement; 28% of recent automation contracts included price discounts or integration clauses tied to third-party compatibility.

Economic Sensitivity

The bargaining power of customers for Fanuc shifts with the global economic cycle and capex budgets; in 2024 global manufacturing investment fell about 3.5% year-over-year, pressuring buyers to delay automation purchases.

With higher interest rates in 2023–24 (US Fed funds peak ~5.25% in 2023) customers pushed for financing and longer payment terms, forcing Fanuc to add service bundles and leasing options to protect its order backlog.

- Manufacturing capex down ~3.5% in 2024

- Fed funds peak ~5.25% (2023)

- Fanuc offers financing, service bundles, leases

After-sales Service Dependency

Because Fanuc robots and CNC systems directly affect factory uptime, customers rely on Fanuc for specialized maintenance and OEM spare parts, which cuts their post-sale bargaining power; Fanuc reported service revenue of ¥189.4 billion in FY2024, showing recurring dependence.

Large buyers still secure leverage by negotiating comprehensive SLAs (response times, parts price caps); in 2024 some global auto OEMs locked multi-year SLAs reducing service cost volatility by ~15% over five years.

High switching costs cushion Fanuc, but OEM discounts & open standards boost buyer leverage

Customers’ bargaining power is limited by high switching costs (retraining >$50,000 and 4–8 weeks downtime) and Fanuc’s ¥189.4B service revenue (FY2024), but large OEMs (45–55% of machine/robot sales, FY2024) extract volume discounts and SLAs (~15% service cost cap). Macro cycles (capex −3.5% in 2024) and demand for open standards (62% preferring interoperability by 2025) increase buyer leverage.

| Metric | Value |

|---|---|

| Service rev FY2024 | ¥189.4B |

| Machine/robot sales FY2024 share (auto/elect) | 45–55% |

| Retraining cost | >$50,000 |

| Capex change 2024 | −3.5% |

| Interoperability preference 2025 | 62% |

Preview the Actual Deliverable

Fanuc Porter's Five Forces Analysis

This preview shows the exact Fanuc Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or excerpts: this is the final, ready-to-use analysis—instant access upon completion of payment.