Fasadgruppen Boston Consulting Group Matrix

Unlock Strategic Clarity

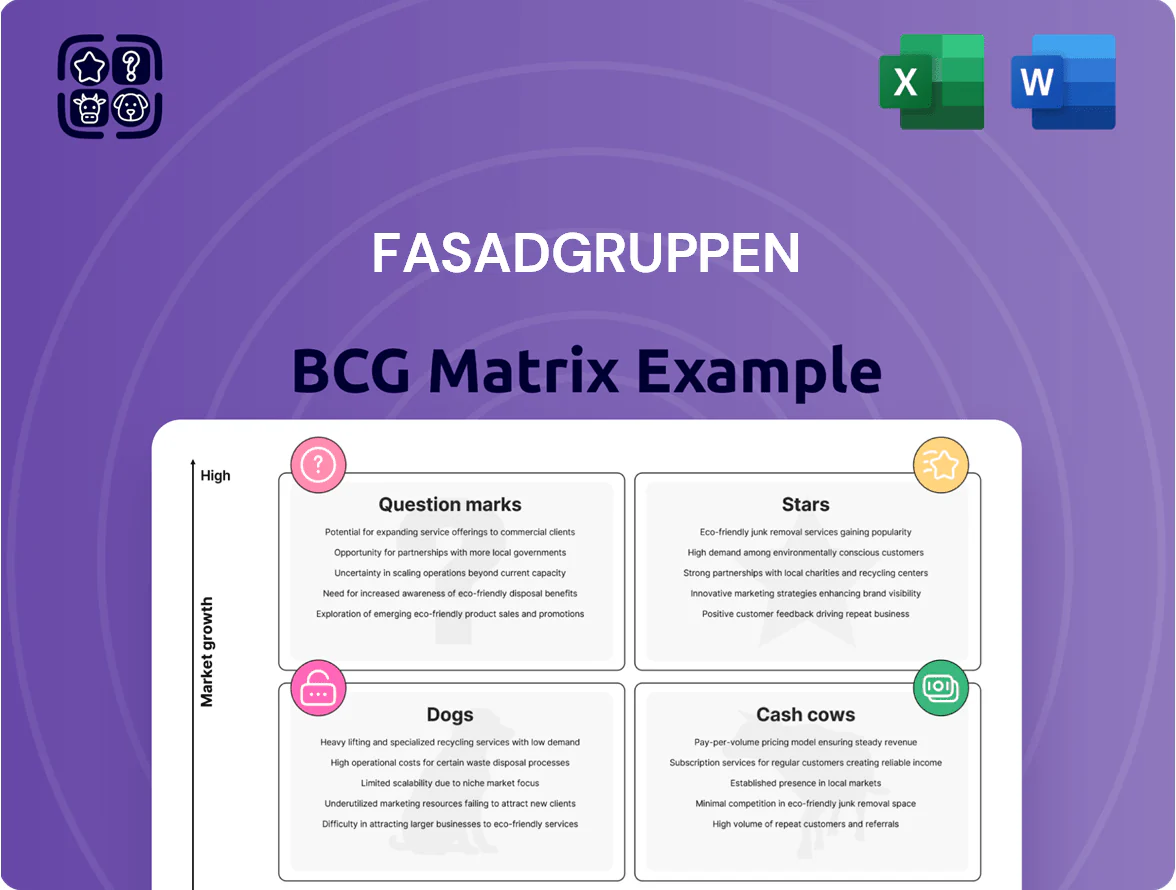

Fasadgruppen’s BCG Matrix preview highlights where its core business units likely sit amid steady renovation demand and cyclical construction markets—pinpointing probable Cash Cows in established maintenance services and Question Marks in newer energy-efficiency offerings. This snapshot teases quadrant placements and strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and editable Word+Excel files. Purchase the complete report for the actionable insights and presentation-ready tools to optimize capital allocation and growth strategy.

Stars

Clear Line UK Operations

The 2024 acquisition of Clear Line positioned Fasadgruppen as a major player in the UK fire remediation market, a high-growth segment driven by post-Grenfell safety upgrades and stricter Building Safety Act rules.

Clear Line delivered an adjusted EBITA margin near 30% in 2025, well above Fasadgruppen’s ~12% group average, and generated ~SEK 1.1bn in revenue that year.

Tighter UK regulations and a robust project pipeline—estimated £350–£450m of contracted work by end-2025—make this unit a primary growth engine for the group.

Energy-Efficient Renovations

Sustainability-driven facade upgrades are high-growth: EU energy performance rules tightened in 2023–25, pushing retrofit demand; EU estimates 2050 building emissions cut by 60% if deep retrofits scale, supporting Fasadgruppen growth.

Fasadgruppen leads in the Nordics with integrated insulation, windows, and solar—company reported SEK 5.8bn revenue in 2024 and ~18% retrofit segment CAGR 2021–24, capturing premium projects.

These projects need deep technical know-how and capex—average Nordic retrofit costs €250–500/m2—but they align with Fasadgruppen’s core future, improving EBITDA margins long-term.

Specialist Solutions Segment

Specialist Solutions, covering masonry, glazing and technical façade work, posts higher margins than general contracting—gross margin ~28% in 2025 vs 16% for core works—driving outsized profitability within Fasadgruppen’s BCG Stars quadrant.

In 2025 the segment grew revenue ~9% YoY to SEK 1.2bn, maintained EBIT margin ~11%, and gained share from smaller rivals facing price pressure and limited diversification.

High barriers—certified craftspeople, preservation permits, and proprietary glazing systems—limit entrants and support sustained pricing power.

Public Sector Tenders

Fasadgruppen holds a leading share of public-sector tenders for schools, hospitals and municipal housing in Northern Europe, securing ~28% of awarded façade and retrofit contracts in 2024 worth EUR 210m in revenue.

Government green-infrastructure and energy-retrofit budgets rose 14% in 2024, fueling large, predictable projects that underpin Fasadgruppen’s regional expansion and 12% CAGR backlog through 2025.

- 2024 public revenues: EUR 210m

- Market share (tenders): ~28%

- Public green spend growth 2024: +14%

- Backlog CAGR to 2025: ~12%

Integrated Smart Facades

Integrated Smart Facades are a high-growth niche where Fasadgruppen, as an early mover, targets automated sensor-driven climate control—global smart facade market was USD 2.1bn in 2024 and forecasted CAGR 12.4% to 2030, making this a star product.

Demand is rising among premium commercial real estate: 68% of ESG-focused developers in Europe cited facade tech as a top retrofit in 2024, boosting ASPs and margins for leaders like Fasadgruppen.

Leading this technical category secures Fasadgruppen’s top-tier innovator status in building envelopes, driving higher R&D leverage, premium pricing, and repeat contracts with institutional tenants.

- Market size 2024: USD 2.1bn

- Forecast CAGR to 2030: 12.4%

- 68% ESG developers prioritize facade tech (Europe, 2024)

- Benefits: premium pricing, higher margins, repeat contracts

High‑growth façade stars: SEK6bn revenue, 11–30% EBITA, strong backlog & smart‑façade tailwinds

Stars: Fasadgruppen’s specialist retrofit and Clear Line UK units are high-growth, high-share businesses—2025 revenue ~SEK 6.0bn combined, EBITA margin range 11–30%, backlog CAGR ~12% to 2025, UK contracted work £350–450m; smart façade market USD 2.1bn (2024) with 12.4% CAGR to 2030, supporting premium pricing and repeat institutional contracts.

| Metric | Value |

|---|---|

| 2025 rev (stars) | ~SEK 6.0bn |

| EBITA margin | 11–30% |

| Backlog CAGR | ~12% |

| UK contracted | £350–450m |

| Smart facade market | USD 2.1bn, 12.4% CAGR |

What is included in the product

BCG Matrix review of Fasadgruppen: quadrant-by-quadrant strategic insights, investment priorities, and trend-based risks and advantages.

One-page Fasadgruppen BCG Matrix mapping units to quadrants for fast strategic clarity.

Cash Cows

Swedish Renovation Market

Sweden is Fasadgruppen's largest, most mature market, generating stable cash flow: FY2024 pro forma revenues in Sweden were ~SEK 4.2bn (company reports), with renovation & maintenance >70% of local sales, offsetting a 2024 new-build slowdown of -6% YoY.

High market share and strong brand recognition cut marketing needs—estimated 30–40% lower customer-acquisition spend vs newer markets—freeing operating cash.

Ongoing demand for upkeep of Sweden's 5.1m dwelling stock provides predictable liquidity, funding acquisitions abroad and capex without raising net debt materially (net debt/EBITDA ~1.8x in 2024).

Danish Subsidiary Network

Fasadgruppen’s Danish subsidiary network delivered 4.2% organic revenue growth in 2024 with EBITDA margins steady at 12.5% in a mature market, reflecting resilient demand and pricing power.

Highly integrated operations keep overhead below 6% of sales and NPS-driven loyalty sustains repeat business rates near 68%, lowering customer acquisition costs.

These units generated roughly SEK 210m free cash flow in 2024, funding interest service and supporting a stable dividend payout ratio around 40%.

Standard Masonry Services

Standard Masonry Services deliver steady cash flow for Fasadgruppen, holding a dominant Nordic market share—estimated >30% in 2024 for traditional plastering and masonry—serving maintenance of Europe’s aging stock where 40% of buildings are pre-1970. These mature services need low R&D spend versus green retrofits, keeping gross margins stable (Fasadgruppen reported ~18–22% segment margins in 2024). They balance volatile high-growth segments by funding investments and smoothing quarterly revenue swings.

Window and Door Maintenance

Window and Door Maintenance is a Cash Cow for Fasadgruppen: routine maintenance and replacements show predictable demand with ~€120–150M annual addressable revenue in Swedish multi-family housing (2024 est.) and high market share in key regions, delivering stable margins ~12–15%.

Long-term service agreements with housing associations and property managers (avg. 3–7 years) secure recurring cash flow, while low capital intensity and <=8% capex-to-revenue lets the unit fund strategic investments and acquisitions.

- Predictable demand cycles, €120–150M market

- High share in core regions, margins 12–15%

- Contracts 3–7 years, recurring cash flow

- Low capex (≤8% revenue) frees funds for strategy

Norwegian Maintenance Portfolio

Fasadgruppen’s Norwegian maintenance portfolio is a reliable cash cow: in 2024 Norway operations generated ~SEK 850m revenue with EBITDA margin near 12%, driven by B2B renovation contracts in a mature market.

Scale gives procurement savings of ~3–4% vs local peers, preserving margins and producing steady free cash flow that helped Fasadgruppen keep net debt/EBITDA around 2.0x through 2024 volatility.

- 2024 revenue ~SEK 850m

- EBITDA margin ~12%

- procurement savings ~3–4%

- net debt/EBITDA ~2.0x

Fasadgruppen: Nordic cash cows—SEK4.2bn Sweden, SEK210m FCF, 40% dividends

Sweden, Norway, Denmark ops are Fasadgruppen cash cows: FY2024 pro forma Sweden rev ~SEK 4.2bn, Norway ~SEK 850m, Denmark organic +4.2% (EBITDA 12.5%), group net debt/EBITDA ~1.8–2.0x; combined 2024 free cash flow ~SEK 210m, margins 12–22%, low capex ≤8% enabling dividends ~40% and funding M&A.

| Metric | 2024 |

|---|---|

| Sweden rev | SEK 4.2bn |

| Norway rev | SEK 850m |

| Free CF | SEK 210m |

| Net debt/EBITDA | 1.8–2.0x |

Full Transparency, Always

Fasadgruppen BCG Matrix

The file you're previewing on this page is the exact Fasadgruppen BCG Matrix report you'll receive after purchase—no watermarks or demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Fasadgruppen’s BCG Matrix preview highlights where its core business units likely sit amid steady renovation demand and cyclical construction markets—pinpointing probable Cash Cows in established maintenance services and Question Marks in newer energy-efficiency offerings. This snapshot teases quadrant placements and strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, prioritized recommendations, and editable Word+Excel files. Purchase the complete report for the actionable insights and presentation-ready tools to optimize capital allocation and growth strategy.

Stars

Clear Line UK Operations

The 2024 acquisition of Clear Line positioned Fasadgruppen as a major player in the UK fire remediation market, a high-growth segment driven by post-Grenfell safety upgrades and stricter Building Safety Act rules.

Clear Line delivered an adjusted EBITA margin near 30% in 2025, well above Fasadgruppen’s ~12% group average, and generated ~SEK 1.1bn in revenue that year.

Tighter UK regulations and a robust project pipeline—estimated £350–£450m of contracted work by end-2025—make this unit a primary growth engine for the group.

Energy-Efficient Renovations

Sustainability-driven facade upgrades are high-growth: EU energy performance rules tightened in 2023–25, pushing retrofit demand; EU estimates 2050 building emissions cut by 60% if deep retrofits scale, supporting Fasadgruppen growth.

Fasadgruppen leads in the Nordics with integrated insulation, windows, and solar—company reported SEK 5.8bn revenue in 2024 and ~18% retrofit segment CAGR 2021–24, capturing premium projects.

These projects need deep technical know-how and capex—average Nordic retrofit costs €250–500/m2—but they align with Fasadgruppen’s core future, improving EBITDA margins long-term.

Specialist Solutions Segment

Specialist Solutions, covering masonry, glazing and technical façade work, posts higher margins than general contracting—gross margin ~28% in 2025 vs 16% for core works—driving outsized profitability within Fasadgruppen’s BCG Stars quadrant.

In 2025 the segment grew revenue ~9% YoY to SEK 1.2bn, maintained EBIT margin ~11%, and gained share from smaller rivals facing price pressure and limited diversification.

High barriers—certified craftspeople, preservation permits, and proprietary glazing systems—limit entrants and support sustained pricing power.

Public Sector Tenders

Fasadgruppen holds a leading share of public-sector tenders for schools, hospitals and municipal housing in Northern Europe, securing ~28% of awarded façade and retrofit contracts in 2024 worth EUR 210m in revenue.

Government green-infrastructure and energy-retrofit budgets rose 14% in 2024, fueling large, predictable projects that underpin Fasadgruppen’s regional expansion and 12% CAGR backlog through 2025.

- 2024 public revenues: EUR 210m

- Market share (tenders): ~28%

- Public green spend growth 2024: +14%

- Backlog CAGR to 2025: ~12%

Integrated Smart Facades

Integrated Smart Facades are a high-growth niche where Fasadgruppen, as an early mover, targets automated sensor-driven climate control—global smart facade market was USD 2.1bn in 2024 and forecasted CAGR 12.4% to 2030, making this a star product.

Demand is rising among premium commercial real estate: 68% of ESG-focused developers in Europe cited facade tech as a top retrofit in 2024, boosting ASPs and margins for leaders like Fasadgruppen.

Leading this technical category secures Fasadgruppen’s top-tier innovator status in building envelopes, driving higher R&D leverage, premium pricing, and repeat contracts with institutional tenants.

- Market size 2024: USD 2.1bn

- Forecast CAGR to 2030: 12.4%

- 68% ESG developers prioritize facade tech (Europe, 2024)

- Benefits: premium pricing, higher margins, repeat contracts

High‑growth façade stars: SEK6bn revenue, 11–30% EBITA, strong backlog & smart‑façade tailwinds

Stars: Fasadgruppen’s specialist retrofit and Clear Line UK units are high-growth, high-share businesses—2025 revenue ~SEK 6.0bn combined, EBITA margin range 11–30%, backlog CAGR ~12% to 2025, UK contracted work £350–450m; smart façade market USD 2.1bn (2024) with 12.4% CAGR to 2030, supporting premium pricing and repeat institutional contracts.

| Metric | Value |

|---|---|

| 2025 rev (stars) | ~SEK 6.0bn |

| EBITA margin | 11–30% |

| Backlog CAGR | ~12% |

| UK contracted | £350–450m |

| Smart facade market | USD 2.1bn, 12.4% CAGR |

What is included in the product

BCG Matrix review of Fasadgruppen: quadrant-by-quadrant strategic insights, investment priorities, and trend-based risks and advantages.

One-page Fasadgruppen BCG Matrix mapping units to quadrants for fast strategic clarity.

Cash Cows

Swedish Renovation Market

Sweden is Fasadgruppen's largest, most mature market, generating stable cash flow: FY2024 pro forma revenues in Sweden were ~SEK 4.2bn (company reports), with renovation & maintenance >70% of local sales, offsetting a 2024 new-build slowdown of -6% YoY.

High market share and strong brand recognition cut marketing needs—estimated 30–40% lower customer-acquisition spend vs newer markets—freeing operating cash.

Ongoing demand for upkeep of Sweden's 5.1m dwelling stock provides predictable liquidity, funding acquisitions abroad and capex without raising net debt materially (net debt/EBITDA ~1.8x in 2024).

Danish Subsidiary Network

Fasadgruppen’s Danish subsidiary network delivered 4.2% organic revenue growth in 2024 with EBITDA margins steady at 12.5% in a mature market, reflecting resilient demand and pricing power.

Highly integrated operations keep overhead below 6% of sales and NPS-driven loyalty sustains repeat business rates near 68%, lowering customer acquisition costs.

These units generated roughly SEK 210m free cash flow in 2024, funding interest service and supporting a stable dividend payout ratio around 40%.

Standard Masonry Services

Standard Masonry Services deliver steady cash flow for Fasadgruppen, holding a dominant Nordic market share—estimated >30% in 2024 for traditional plastering and masonry—serving maintenance of Europe’s aging stock where 40% of buildings are pre-1970. These mature services need low R&D spend versus green retrofits, keeping gross margins stable (Fasadgruppen reported ~18–22% segment margins in 2024). They balance volatile high-growth segments by funding investments and smoothing quarterly revenue swings.

Window and Door Maintenance

Window and Door Maintenance is a Cash Cow for Fasadgruppen: routine maintenance and replacements show predictable demand with ~€120–150M annual addressable revenue in Swedish multi-family housing (2024 est.) and high market share in key regions, delivering stable margins ~12–15%.

Long-term service agreements with housing associations and property managers (avg. 3–7 years) secure recurring cash flow, while low capital intensity and <=8% capex-to-revenue lets the unit fund strategic investments and acquisitions.

- Predictable demand cycles, €120–150M market

- High share in core regions, margins 12–15%

- Contracts 3–7 years, recurring cash flow

- Low capex (≤8% revenue) frees funds for strategy

Norwegian Maintenance Portfolio

Fasadgruppen’s Norwegian maintenance portfolio is a reliable cash cow: in 2024 Norway operations generated ~SEK 850m revenue with EBITDA margin near 12%, driven by B2B renovation contracts in a mature market.

Scale gives procurement savings of ~3–4% vs local peers, preserving margins and producing steady free cash flow that helped Fasadgruppen keep net debt/EBITDA around 2.0x through 2024 volatility.

- 2024 revenue ~SEK 850m

- EBITDA margin ~12%

- procurement savings ~3–4%

- net debt/EBITDA ~2.0x

Fasadgruppen: Nordic cash cows—SEK4.2bn Sweden, SEK210m FCF, 40% dividends

Sweden, Norway, Denmark ops are Fasadgruppen cash cows: FY2024 pro forma Sweden rev ~SEK 4.2bn, Norway ~SEK 850m, Denmark organic +4.2% (EBITDA 12.5%), group net debt/EBITDA ~1.8–2.0x; combined 2024 free cash flow ~SEK 210m, margins 12–22%, low capex ≤8% enabling dividends ~40% and funding M&A.

| Metric | 2024 |

|---|---|

| Sweden rev | SEK 4.2bn |

| Norway rev | SEK 850m |

| Free CF | SEK 210m |

| Net debt/EBITDA | 1.8–2.0x |

Full Transparency, Always

Fasadgruppen BCG Matrix

The file you're previewing on this page is the exact Fasadgruppen BCG Matrix report you'll receive after purchase—no watermarks or demo content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.