Fastenal Boston Consulting Group Matrix

Download Your Competitive Advantage

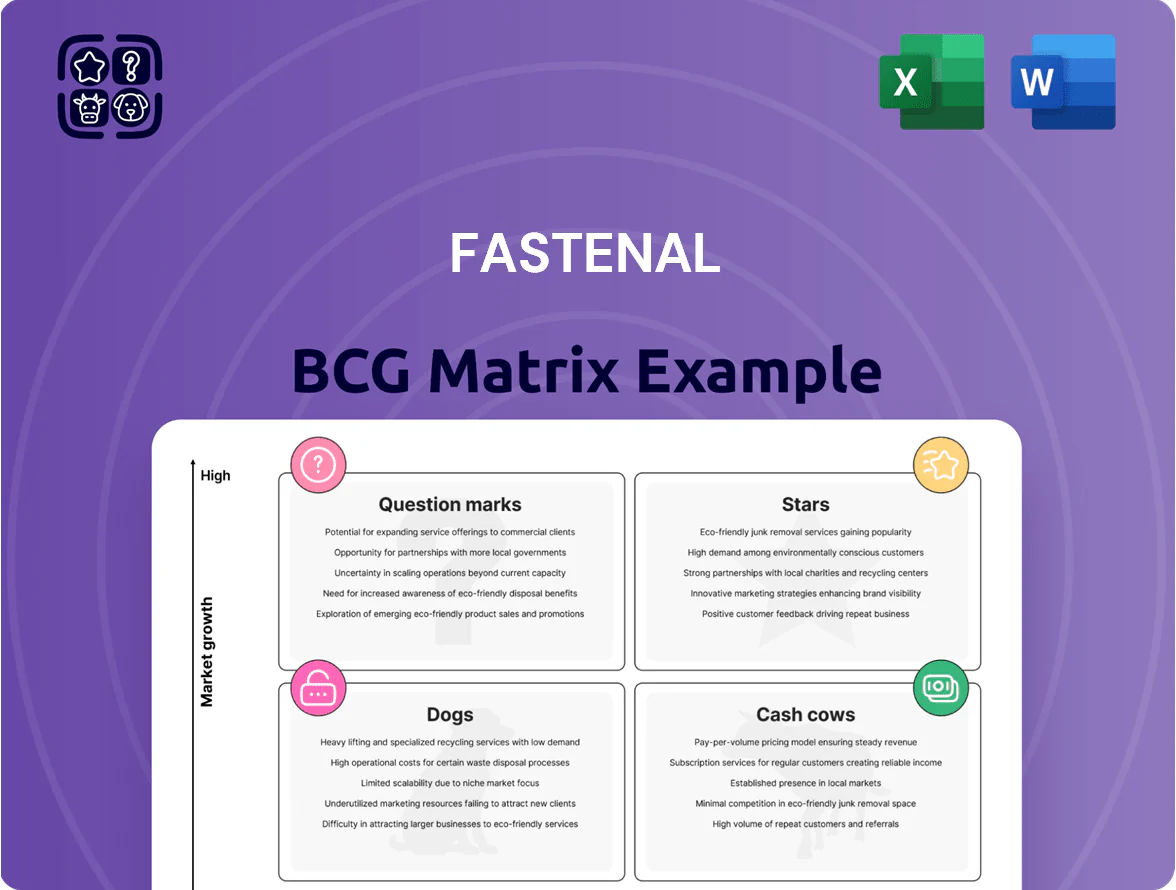

Fastenal’s BCG Matrix preview highlights how its product lines and distribution channels map across market growth and relative share—spotting Stars in industrial fasteners, Cash Cows in established MRO supplies, and potential Question Marks in newer safety and supply-chain services. This snapshot reveals capital allocation priorities and where divestment or investment could move the needle. Purchase the full BCG Matrix for quadrant-level placements, data-driven recommendations, and a ready-to-use Word + Excel deliverable to guide strategic and investment decisions.

Stars

Onsite Service Locations

Onsite Service Locations are Fastenal's primary growth engine, embedding service centers inside customer plants to manage dedicated inventory and supply-chain tasks; in late 2025 these sites posted high double-digit sales growth, driven largely by large manufacturing accounts spending over $50,000 monthly.

Safety Supplies and PPE

Safety Supplies and PPE are a star for Fastenal, accounting for 22.2% of 2025 sales and growing faster than many legacy industrial lines, with PPE revenue rising about 18% year-over-year in 2024–25.

Regulatory tailwinds—OSHA updates and state-level mandates—boost demand, and Fastenal’s ~300 regional safety specialists won multiple large accounts, contributing roughly $350 million in contract-based revenue in 2025.

Fastenal is reinvesting aggressively: capex and sales support for safety rose ~12% in 2025, widening the gap versus smaller regional distributors and generalist MROs on pricing, service and compliance capabilities.

FMI Vending and Bin Technology

FMI Vending and RFID bin systems sit in the Stars quadrant as Fastenal’s high-growth, high-share digital segment, driving real-time inventory data and sticky customer relationships; by end-2025, these devices helped deliver much of Fastenal’s 61.4% digital sales mix and supported replenishment velocity gains of ~18% YoY.

Large Enterprise National Accounts

Large Enterprise National Accounts grew to 65% of Fastenal total sales by end-2025, driven by a strategic shift to high-value, multi-site contracts that raised share in manufacturing to an estimated 28% of sector spend.

These accounts showed resilient revenue growth—annualized same-account sales up ~9% 2023–2025—even during weak industrial production, making them Stars in the BCG matrix.

Fastenal priorities: heavy investment in dedicated account managers and customized supply-chain integration to convert Stars into stable Cash Cows.

- 65% of sales by end-2025

- ~9% annualized same-account sales growth (2023–2025)

- ~28% share of manufacturing sector spend

- Investment: dedicated AMs + supply-chain integration

eBusiness and Digital Solutions

Fastenal’s eBusiness (website ordering plus EDI) grew double-digits as customers moved to automated procurement; by late 2025 digitally enabled sales were about 62% of total revenue, showing dominant share in B2B eCommerce.

Fastenal increased IT spend—capex and cloud/SaaS—boosting UX and supply-chain visibility to counter digital-native rivals and protect margins.

- Digitally enabled sales ~62% of revenue (late 2025)

- eBusiness double-digit YoY growth (2023–2025)

- Higher IT/capex allocation for UX, EDI, cloud

Fastenal Stars: 65% Sales, 62% Digital, Safety 22% — 9% Same-Account Growth

Fastenal Stars: Onsite service, Safety/PPE, FMI vending/RFID, and Large Enterprise accounts drove high-share, high-growth—65% company sales by 2025, digital sales ~62%, Safety = 22.2% of sales, PPE +18% YoY (2024–25), same-account growth ~9% annualized (2023–25); capex/IT +12% to protect share and convert Stars to Cash Cows.

| Metric | Value (2025) |

|---|---|

| Share of sales | 65% |

| Digital sales | 62% |

| Safety sales | 22.2% |

| PPE YoY growth | 18% |

| Same-account growth | ~9% annualized |

What is included in the product

BCG Matrix review of Fastenal’s units: Stars to invest, Cash Cows to harvest, Question Marks to evaluate, Dogs to divest; includes SWOT and trend context.

One-page Fastenal BCG Matrix placing each business unit in a quadrant for quick strategic decision-making.

Cash Cows

Core Fastener Product Line

Core fastener products remain Fastenal’s cash cow, driving 30.5% of total sales in 2025 and producing high gross margins (~38% reported in FY2025) and strong operating cash flow used to fund growth categories.

North American Branch Network

Fastenal’s North American branch network—over 1,500 traditional branches across the US, Canada, and Mexico—sits as a classic Cash Cow in the BCG matrix, delivering mature, high-share revenue streams. These branches act as local fulfillment terminals that support fast-growing Onsite and Fastenal Managed Inventory (FMI) programs while sustaining steady branch-level margins. Optimized over decades, branch operations generated roughly $2.7 billion in fiscal 2024 operating cash flow, funding dividends and debt service.

MRO Maintenance and Repair Supplies

MRO maintenance, repair, and operations supplies form a mature, high–market-share category for Fastenal, covering consumables like fasteners, abrasives, and lubricants that keep factories running and generate predictable, low-volatility demand; Industrial MRO spending in the US was ~140 billion USD in 2024, supporting steady order volumes. The segment’s gross margins historically exceed Fastenal’s company average by ~200–300 basis points, making it a reliable cash generator. With annual growth under 3% (relative market growth), MRO’s high cash conversion funds R&D and Fastenal’s digital push—Fastenal invested $150 million in tech and automation in 2024. What this estimate hides: regional mix and backlog can shift short-term demand.

Heavy Manufacturing End Market

Fastenal’s Heavy Manufacturing end market is its largest and most established segment, driving nearly 43% of total sales by year-end 2025 and delivering steady cash flow from market-leading industrial clients.

Long-term contracts and high barriers to entry create customer stickiness and allow Fastenal to capture the lion’s share of spend; operating leverage in distribution and vending boosts margins versus peers.

Growth tracks macro cycles—manufacturing PMI and capex swings—but Fastenal’s scale and service model preserve share during downturns, keeping this a classic Cash Cow in the BCG matrix.

- 43% of sales by end-2025

- High customer stickiness via long-term relationships

- High barriers to entry, strong market share

- High operational leverage improves margins

Private Label Brands

Fastenal’s private-label brands—which include Core, Value, and Pro lines—deliver higher gross margins (often 30–40% vs ~20% for national brands) across mature categories like hand tools and janitorial supplies, driving superior profitability within its installed base.

These brands hold dominant share in Fastenal catalogs and account for an estimated 25–30% of product margin dollars in 2024, needing minimal incremental marketing or capex and generating steady internal cash flow.

- Higher gross margin: ~30–40%

- Share of product margin dollars: ~25–30% (2024)

- Low incremental investment: integrated catalog and distribution

- Stable cash generation: repeat purchases in mature categories

Fastenal: Core fasteners & NA branches fuel $2.7B cash flow, high-margin private labels

Fastenal’s cash cows: core fasteners/MRO and North American branches drive stable cash flow—30.5% of sales from core fasteners (2025), 43% of sales from heavy manufacturing end market (YE2025), ~$2.7B operating cash flow (FY2024), private-label margins ~30–40% and 25–30% share of product margin dollars (2024).

| Metric | Value |

|---|---|

| Core fasteners % sales (2025) | 30.5% |

| Heavy mfg % sales (YE2025) | 43% |

| Op cash flow (FY2024) | $2.7B |

| Private-label margin (2024) | 30–40% |

| Private-label margin share (2024) | 25–30% |

Preview = Final Product

Fastenal BCG Matrix

The file you're previewing on this page is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Fastenal’s BCG Matrix preview highlights how its product lines and distribution channels map across market growth and relative share—spotting Stars in industrial fasteners, Cash Cows in established MRO supplies, and potential Question Marks in newer safety and supply-chain services. This snapshot reveals capital allocation priorities and where divestment or investment could move the needle. Purchase the full BCG Matrix for quadrant-level placements, data-driven recommendations, and a ready-to-use Word + Excel deliverable to guide strategic and investment decisions.

Stars

Onsite Service Locations

Onsite Service Locations are Fastenal's primary growth engine, embedding service centers inside customer plants to manage dedicated inventory and supply-chain tasks; in late 2025 these sites posted high double-digit sales growth, driven largely by large manufacturing accounts spending over $50,000 monthly.

Safety Supplies and PPE

Safety Supplies and PPE are a star for Fastenal, accounting for 22.2% of 2025 sales and growing faster than many legacy industrial lines, with PPE revenue rising about 18% year-over-year in 2024–25.

Regulatory tailwinds—OSHA updates and state-level mandates—boost demand, and Fastenal’s ~300 regional safety specialists won multiple large accounts, contributing roughly $350 million in contract-based revenue in 2025.

Fastenal is reinvesting aggressively: capex and sales support for safety rose ~12% in 2025, widening the gap versus smaller regional distributors and generalist MROs on pricing, service and compliance capabilities.

FMI Vending and Bin Technology

FMI Vending and RFID bin systems sit in the Stars quadrant as Fastenal’s high-growth, high-share digital segment, driving real-time inventory data and sticky customer relationships; by end-2025, these devices helped deliver much of Fastenal’s 61.4% digital sales mix and supported replenishment velocity gains of ~18% YoY.

Large Enterprise National Accounts

Large Enterprise National Accounts grew to 65% of Fastenal total sales by end-2025, driven by a strategic shift to high-value, multi-site contracts that raised share in manufacturing to an estimated 28% of sector spend.

These accounts showed resilient revenue growth—annualized same-account sales up ~9% 2023–2025—even during weak industrial production, making them Stars in the BCG matrix.

Fastenal priorities: heavy investment in dedicated account managers and customized supply-chain integration to convert Stars into stable Cash Cows.

- 65% of sales by end-2025

- ~9% annualized same-account sales growth (2023–2025)

- ~28% share of manufacturing sector spend

- Investment: dedicated AMs + supply-chain integration

eBusiness and Digital Solutions

Fastenal’s eBusiness (website ordering plus EDI) grew double-digits as customers moved to automated procurement; by late 2025 digitally enabled sales were about 62% of total revenue, showing dominant share in B2B eCommerce.

Fastenal increased IT spend—capex and cloud/SaaS—boosting UX and supply-chain visibility to counter digital-native rivals and protect margins.

- Digitally enabled sales ~62% of revenue (late 2025)

- eBusiness double-digit YoY growth (2023–2025)

- Higher IT/capex allocation for UX, EDI, cloud

Fastenal Stars: 65% Sales, 62% Digital, Safety 22% — 9% Same-Account Growth

Fastenal Stars: Onsite service, Safety/PPE, FMI vending/RFID, and Large Enterprise accounts drove high-share, high-growth—65% company sales by 2025, digital sales ~62%, Safety = 22.2% of sales, PPE +18% YoY (2024–25), same-account growth ~9% annualized (2023–25); capex/IT +12% to protect share and convert Stars to Cash Cows.

| Metric | Value (2025) |

|---|---|

| Share of sales | 65% |

| Digital sales | 62% |

| Safety sales | 22.2% |

| PPE YoY growth | 18% |

| Same-account growth | ~9% annualized |

What is included in the product

BCG Matrix review of Fastenal’s units: Stars to invest, Cash Cows to harvest, Question Marks to evaluate, Dogs to divest; includes SWOT and trend context.

One-page Fastenal BCG Matrix placing each business unit in a quadrant for quick strategic decision-making.

Cash Cows

Core Fastener Product Line

Core fastener products remain Fastenal’s cash cow, driving 30.5% of total sales in 2025 and producing high gross margins (~38% reported in FY2025) and strong operating cash flow used to fund growth categories.

North American Branch Network

Fastenal’s North American branch network—over 1,500 traditional branches across the US, Canada, and Mexico—sits as a classic Cash Cow in the BCG matrix, delivering mature, high-share revenue streams. These branches act as local fulfillment terminals that support fast-growing Onsite and Fastenal Managed Inventory (FMI) programs while sustaining steady branch-level margins. Optimized over decades, branch operations generated roughly $2.7 billion in fiscal 2024 operating cash flow, funding dividends and debt service.

MRO Maintenance and Repair Supplies

MRO maintenance, repair, and operations supplies form a mature, high–market-share category for Fastenal, covering consumables like fasteners, abrasives, and lubricants that keep factories running and generate predictable, low-volatility demand; Industrial MRO spending in the US was ~140 billion USD in 2024, supporting steady order volumes. The segment’s gross margins historically exceed Fastenal’s company average by ~200–300 basis points, making it a reliable cash generator. With annual growth under 3% (relative market growth), MRO’s high cash conversion funds R&D and Fastenal’s digital push—Fastenal invested $150 million in tech and automation in 2024. What this estimate hides: regional mix and backlog can shift short-term demand.

Heavy Manufacturing End Market

Fastenal’s Heavy Manufacturing end market is its largest and most established segment, driving nearly 43% of total sales by year-end 2025 and delivering steady cash flow from market-leading industrial clients.

Long-term contracts and high barriers to entry create customer stickiness and allow Fastenal to capture the lion’s share of spend; operating leverage in distribution and vending boosts margins versus peers.

Growth tracks macro cycles—manufacturing PMI and capex swings—but Fastenal’s scale and service model preserve share during downturns, keeping this a classic Cash Cow in the BCG matrix.

- 43% of sales by end-2025

- High customer stickiness via long-term relationships

- High barriers to entry, strong market share

- High operational leverage improves margins

Private Label Brands

Fastenal’s private-label brands—which include Core, Value, and Pro lines—deliver higher gross margins (often 30–40% vs ~20% for national brands) across mature categories like hand tools and janitorial supplies, driving superior profitability within its installed base.

These brands hold dominant share in Fastenal catalogs and account for an estimated 25–30% of product margin dollars in 2024, needing minimal incremental marketing or capex and generating steady internal cash flow.

- Higher gross margin: ~30–40%

- Share of product margin dollars: ~25–30% (2024)

- Low incremental investment: integrated catalog and distribution

- Stable cash generation: repeat purchases in mature categories

Fastenal: Core fasteners & NA branches fuel $2.7B cash flow, high-margin private labels

Fastenal’s cash cows: core fasteners/MRO and North American branches drive stable cash flow—30.5% of sales from core fasteners (2025), 43% of sales from heavy manufacturing end market (YE2025), ~$2.7B operating cash flow (FY2024), private-label margins ~30–40% and 25–30% share of product margin dollars (2024).

| Metric | Value |

|---|---|

| Core fasteners % sales (2025) | 30.5% |

| Heavy mfg % sales (YE2025) | 43% |

| Op cash flow (FY2024) | $2.7B |

| Private-label margin (2024) | 30–40% |

| Private-label margin share (2024) | 25–30% |

Preview = Final Product

Fastenal BCG Matrix

The file you're previewing on this page is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.