Fast Retailing PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Explore how political shifts, consumer trends, and supply‑chain dynamics are shaping Fast Retailing’s growth and risks with our concise PESTLE snapshot—then unlock the full, actionable analysis to inform investor decisions and strategic plans. Buy the complete PESTLE now for editable, boardroom-ready insights you can deploy immediately.

Political factors

Geopolitical Trade Tensions

Geopolitical tensions between China and Western markets threaten Fast Retailing’s supply chain and sales: in FY2024 Fast Retailing sourced an estimated 40-50% of apparel from China and generated ~20% of revenue from Greater China, so tariffs, export controls or sanctions could raise COGS and logistics costs materially. Trade barriers or boycotts risk store closures or lost sales—management must balance diplomacy and local PR to protect Uniqlo’s market access and brand.

Supply Chain Diversification

Political instability in Bangladesh and Myanmar has pushed Fast Retailing to speed its China Plus One strategy, reducing reliance on those hubs after factory disruptions cut output by an estimated 8–12% in 2023; the group expanded production in Vietnam, Indonesia and Cambodia, raising SE Asia sourcing to roughly 28% of apparel manufacturing by 2024 to safeguard supply chains. This geographic shift toward nearby markets supports steadier inventory flow and lowers geopolitically driven shutdown risk.

International Trade Agreements

Changes in regional trade blocs and FTAs reshape tariff rates for Asian textile exports to Europe and North America, with tariffs falling up to 12% under recent agreements like RCEP and CPTPP expansions affecting Fast Retailing’s supply chains.

Fast Retailing closely monitors these shifts to reroute shipments and leverage rules of origin, cutting landed costs—logistics savings cited at roughly 1–2% of COGS in FY2024.

Favorable trade terms helped sustain Fast Retailing’s affordable-quality pricing, supporting 2024 global gross margin resilience near 47% despite currency and freight volatility.

Government Digitalization Initiatives

Many East Asian governments offer subsidies for digital transformation; Japan’s 2024 subsidy programs allocated about ¥1.6 trillion for DX and smart manufacturing, which Fast Retailing taps to fund AI-driven inventory and automated distribution upgrades across 200+ domestic stores and key international hubs.

Aligning with national digital agendas helps Fast Retailing secure preferential infrastructure, public–private R&D ties and partnerships with tech suppliers, reducing CAPEX by an estimated 5–8% per project in 2024 pilot rollouts.

- ¥1.6 trillion Japan DX subsidies (2024) leveraged

- 200+ domestic stores upgraded with AI/automation

- Estimated 5–8% CAPEX reduction in 2024 pilots

- Stronger public–private R&D and tech partnerships

Labor Policy Regulations

Political pressure for higher minimum wages and stronger worker rights in Bangladesh, Vietnam and Cambodia has raised garment production costs for Fast Retailing; wage hikes averaged 8-12% in 2023-24 in key sourcing countries, squeezing margins on low-price lines.

Regulators now require stricter labor standards and supplier audits—Fast Retailing reported conducting 1,200 supplier assessments in FY2024—raising compliance spend and supply-chain oversight costs.

Non-compliance risks include factory shutdowns, fines and reputational damage; in 2023 industry scandals led to multi-million-dollar remediation funds and share-price volatility across apparel peers.

- Wage hikes 8–12% in 2023–24 in key sourcing countries

- 1,200 supplier audits by Fast Retailing in FY2024

- Higher compliance spend and risk of fines, shutdowns, reputational loss

Fast Retailing faces rising COGS and compliance costs as China tensions disrupt supply

Political risks—China-West tensions, trade barriers and rising labor regulations—threaten Fast Retailing’s supply, raising COGS and compliance spend; FY2024: 40–50% sourcing from China, ~20% revenue Greater China, 1,200 supplier audits, wage hikes 8–12% in key sourcing countries, SE Asia sourcing ~28%.

| Metric | FY2024 / 2023–24 |

|---|---|

| China sourcing | 40–50% |

| Revenue Greater China | ~20% |

| Supplier audits | 1,200 |

| Wage hikes | 8–12% |

| SE Asia sourcing | ~28% |

What is included in the product

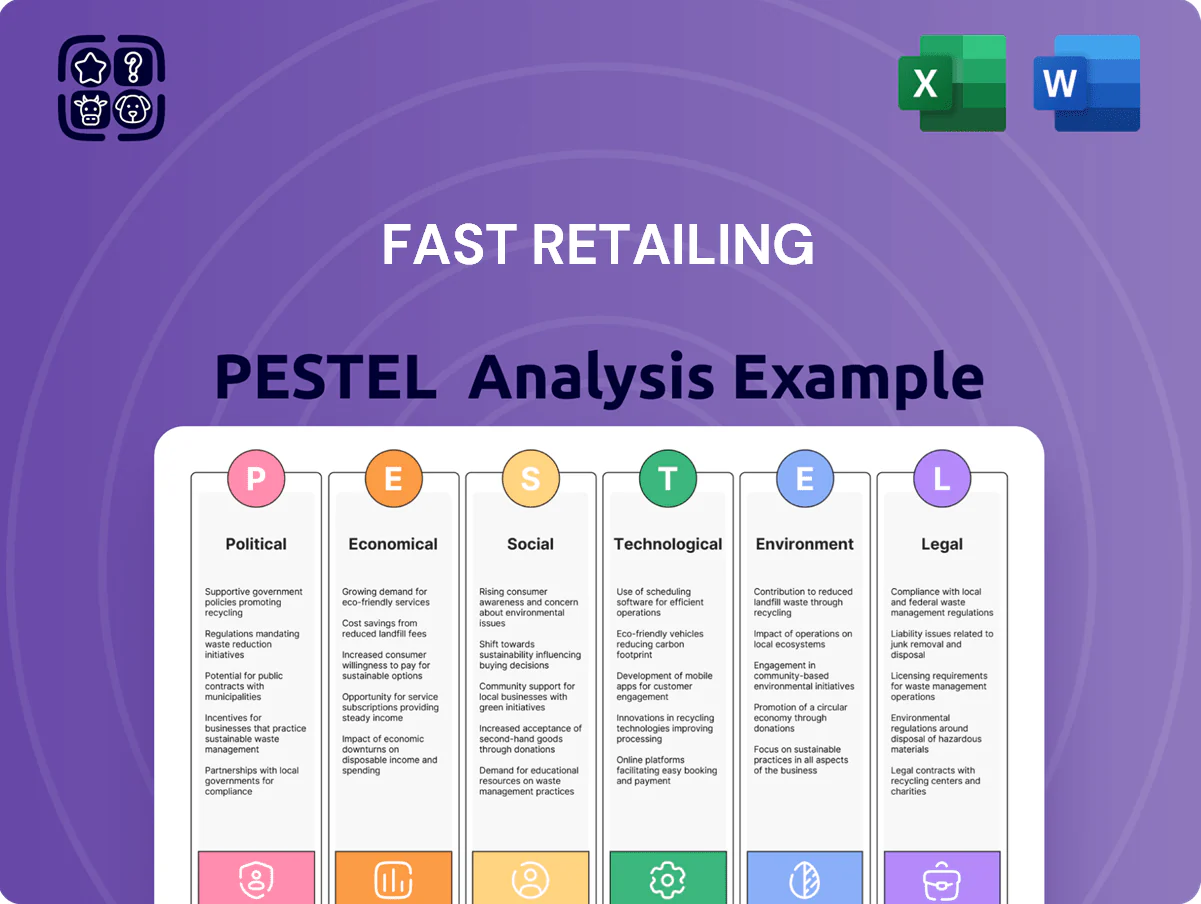

Explores how external macro-environmental factors uniquely affect Fast Retailing across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal actionable threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE snapshot of Fast Retailing that simplifies external risk assessment for quick meeting references and slide-ready inclusion.

Economic factors

Currency Exchange Volatility

As a Japan-headquartered firm, Fast Retailing faces Yen volatility versus the USD and EUR; a 2024 Yen drop ~6% vs USD raised dollar-priced fabric costs and squeezed margins in FY2024, while a 2025 Yen rebound cut translated overseas revenue (overseas sales ~85% of revenue). The group uses currency hedges, forwards and options—hedging ~50–70% of near-term FX exposure—to stabilize procurement costs and reported profits.

Global Inflationary Pressures

Rising energy, logistics and cotton costs—global cotton up about 15% in 2024 and container freight rates averaging 60% above pre-pandemic levels—squeeze retail margins; Fast Retailing reported a 2024 gross margin pressure with SG&A rising ~4% YoY. The group must weigh passing costs to consumers against its UNIQLO affordability promise, where price hikes could hurt volume. Prolonged inflation in Japan, US and Europe risks shifting demand to essential, durable apparel over trend-led items, reducing average selling price growth.

Rising Labor Costs

Economic growth in Fast Retailing’s key manufacturing hubs—Bangladesh, Vietnam, and China—has pushed garment wages up by 5–8% annually (2023–2024), squeezing margins for apparel firms. Fast Retailing counters rising payrolls by investing in automation and productivity: capital expenditure rose to ¥241.2 billion in FY2024, funding efficiency upgrades across UNIQLO factories. To preserve cost leadership the company continuously monitors wage inflation and FX in emerging labor markets to rebalance sourcing.

Consumer Spending Power

Disposable income in China and the US drives Uniqlo/GU growth; China household disposable income rose ~6.9% in 2024 while US real disposable personal income fell 0.7% in 2024, impacting demand.

Economic slowdowns cut foot traffic and average transaction value; Fast Retailing reported global same-store sales growth slowed to 1.4% in FY2024 amid weak consumer spending.

The LifeWear strategy targets budget-conscious buyers with high-utility, value-led apparel, helping maintain margins and volume during downturns.

- China disposable income +6.9% (2024)

- US real DPI -0.7% (2024)

- Fast Retailing SSS growth 1.4% (FY2024)

Interest Rate Fluctuations

Changes in central bank policies globally have raised borrowing costs, with OECD policy rates averaging about 3.2% in 2024, directly impacting Fast Retailing’s cost of capital for capex and expansion.

Higher rates increase debt service and can slow new store openings in costly urban centers, potentially delaying rollout in key markets like New York and Tokyo.

Fast Retailing held cash and equivalents of ¥1.03 trillion (FY2024), providing resilience against tightening monetary environments and liquidity to pursue strategic acquisitions.

- OECD policy rates ~3.2% (2024)

- Higher rates raise debt service, slow urban store rollouts

- Fast Retailing cash ¥1.03 trillion (FY2024)

FY2024 margins hit by yen swings, inflation and rates despite 50–70% FX hedges

Yen swings, commodity and wage inflation, and higher interest rates squeezed FY2024 margins: FX hedging covers ~50–70% exposure; cotton +15% (2024); container rates ~+60% vs pre‑pandemic; garment wages +5–8% (2023–24); OECD policy rates ~3.2% (2024); cash ¥1.03tn; SSS growth 1.4% (FY2024); China disposable income +6.9%, US real DPI −0.7% (2024).

| Metric | Value (2024) |

|---|---|

| FX hedge coverage | 50–70% |

| Cotton price change | +15% |

| Container freight vs pre‑pandemic | +60% |

| Garment wage inflation | +5–8% |

| OECD policy rates | ~3.2% |

| Cash & equivalents | ¥1.03tn |

| SSS growth | 1.4% |

| China disposable income | +6.9% |

| US real DPI | −0.7% |

Full Version Awaits

Fast Retailing PESTLE Analysis

The preview shown here is the exact Fast Retailing PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Explore how political shifts, consumer trends, and supply‑chain dynamics are shaping Fast Retailing’s growth and risks with our concise PESTLE snapshot—then unlock the full, actionable analysis to inform investor decisions and strategic plans. Buy the complete PESTLE now for editable, boardroom-ready insights you can deploy immediately.

Political factors

Geopolitical Trade Tensions

Geopolitical tensions between China and Western markets threaten Fast Retailing’s supply chain and sales: in FY2024 Fast Retailing sourced an estimated 40-50% of apparel from China and generated ~20% of revenue from Greater China, so tariffs, export controls or sanctions could raise COGS and logistics costs materially. Trade barriers or boycotts risk store closures or lost sales—management must balance diplomacy and local PR to protect Uniqlo’s market access and brand.

Supply Chain Diversification

Political instability in Bangladesh and Myanmar has pushed Fast Retailing to speed its China Plus One strategy, reducing reliance on those hubs after factory disruptions cut output by an estimated 8–12% in 2023; the group expanded production in Vietnam, Indonesia and Cambodia, raising SE Asia sourcing to roughly 28% of apparel manufacturing by 2024 to safeguard supply chains. This geographic shift toward nearby markets supports steadier inventory flow and lowers geopolitically driven shutdown risk.

International Trade Agreements

Changes in regional trade blocs and FTAs reshape tariff rates for Asian textile exports to Europe and North America, with tariffs falling up to 12% under recent agreements like RCEP and CPTPP expansions affecting Fast Retailing’s supply chains.

Fast Retailing closely monitors these shifts to reroute shipments and leverage rules of origin, cutting landed costs—logistics savings cited at roughly 1–2% of COGS in FY2024.

Favorable trade terms helped sustain Fast Retailing’s affordable-quality pricing, supporting 2024 global gross margin resilience near 47% despite currency and freight volatility.

Government Digitalization Initiatives

Many East Asian governments offer subsidies for digital transformation; Japan’s 2024 subsidy programs allocated about ¥1.6 trillion for DX and smart manufacturing, which Fast Retailing taps to fund AI-driven inventory and automated distribution upgrades across 200+ domestic stores and key international hubs.

Aligning with national digital agendas helps Fast Retailing secure preferential infrastructure, public–private R&D ties and partnerships with tech suppliers, reducing CAPEX by an estimated 5–8% per project in 2024 pilot rollouts.

- ¥1.6 trillion Japan DX subsidies (2024) leveraged

- 200+ domestic stores upgraded with AI/automation

- Estimated 5–8% CAPEX reduction in 2024 pilots

- Stronger public–private R&D and tech partnerships

Labor Policy Regulations

Political pressure for higher minimum wages and stronger worker rights in Bangladesh, Vietnam and Cambodia has raised garment production costs for Fast Retailing; wage hikes averaged 8-12% in 2023-24 in key sourcing countries, squeezing margins on low-price lines.

Regulators now require stricter labor standards and supplier audits—Fast Retailing reported conducting 1,200 supplier assessments in FY2024—raising compliance spend and supply-chain oversight costs.

Non-compliance risks include factory shutdowns, fines and reputational damage; in 2023 industry scandals led to multi-million-dollar remediation funds and share-price volatility across apparel peers.

- Wage hikes 8–12% in 2023–24 in key sourcing countries

- 1,200 supplier audits by Fast Retailing in FY2024

- Higher compliance spend and risk of fines, shutdowns, reputational loss

Fast Retailing faces rising COGS and compliance costs as China tensions disrupt supply

Political risks—China-West tensions, trade barriers and rising labor regulations—threaten Fast Retailing’s supply, raising COGS and compliance spend; FY2024: 40–50% sourcing from China, ~20% revenue Greater China, 1,200 supplier audits, wage hikes 8–12% in key sourcing countries, SE Asia sourcing ~28%.

| Metric | FY2024 / 2023–24 |

|---|---|

| China sourcing | 40–50% |

| Revenue Greater China | ~20% |

| Supplier audits | 1,200 |

| Wage hikes | 8–12% |

| SE Asia sourcing | ~28% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fast Retailing across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal actionable threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE snapshot of Fast Retailing that simplifies external risk assessment for quick meeting references and slide-ready inclusion.

Economic factors

Currency Exchange Volatility

As a Japan-headquartered firm, Fast Retailing faces Yen volatility versus the USD and EUR; a 2024 Yen drop ~6% vs USD raised dollar-priced fabric costs and squeezed margins in FY2024, while a 2025 Yen rebound cut translated overseas revenue (overseas sales ~85% of revenue). The group uses currency hedges, forwards and options—hedging ~50–70% of near-term FX exposure—to stabilize procurement costs and reported profits.

Global Inflationary Pressures

Rising energy, logistics and cotton costs—global cotton up about 15% in 2024 and container freight rates averaging 60% above pre-pandemic levels—squeeze retail margins; Fast Retailing reported a 2024 gross margin pressure with SG&A rising ~4% YoY. The group must weigh passing costs to consumers against its UNIQLO affordability promise, where price hikes could hurt volume. Prolonged inflation in Japan, US and Europe risks shifting demand to essential, durable apparel over trend-led items, reducing average selling price growth.

Rising Labor Costs

Economic growth in Fast Retailing’s key manufacturing hubs—Bangladesh, Vietnam, and China—has pushed garment wages up by 5–8% annually (2023–2024), squeezing margins for apparel firms. Fast Retailing counters rising payrolls by investing in automation and productivity: capital expenditure rose to ¥241.2 billion in FY2024, funding efficiency upgrades across UNIQLO factories. To preserve cost leadership the company continuously monitors wage inflation and FX in emerging labor markets to rebalance sourcing.

Consumer Spending Power

Disposable income in China and the US drives Uniqlo/GU growth; China household disposable income rose ~6.9% in 2024 while US real disposable personal income fell 0.7% in 2024, impacting demand.

Economic slowdowns cut foot traffic and average transaction value; Fast Retailing reported global same-store sales growth slowed to 1.4% in FY2024 amid weak consumer spending.

The LifeWear strategy targets budget-conscious buyers with high-utility, value-led apparel, helping maintain margins and volume during downturns.

- China disposable income +6.9% (2024)

- US real DPI -0.7% (2024)

- Fast Retailing SSS growth 1.4% (FY2024)

Interest Rate Fluctuations

Changes in central bank policies globally have raised borrowing costs, with OECD policy rates averaging about 3.2% in 2024, directly impacting Fast Retailing’s cost of capital for capex and expansion.

Higher rates increase debt service and can slow new store openings in costly urban centers, potentially delaying rollout in key markets like New York and Tokyo.

Fast Retailing held cash and equivalents of ¥1.03 trillion (FY2024), providing resilience against tightening monetary environments and liquidity to pursue strategic acquisitions.

- OECD policy rates ~3.2% (2024)

- Higher rates raise debt service, slow urban store rollouts

- Fast Retailing cash ¥1.03 trillion (FY2024)

FY2024 margins hit by yen swings, inflation and rates despite 50–70% FX hedges

Yen swings, commodity and wage inflation, and higher interest rates squeezed FY2024 margins: FX hedging covers ~50–70% exposure; cotton +15% (2024); container rates ~+60% vs pre‑pandemic; garment wages +5–8% (2023–24); OECD policy rates ~3.2% (2024); cash ¥1.03tn; SSS growth 1.4% (FY2024); China disposable income +6.9%, US real DPI −0.7% (2024).

| Metric | Value (2024) |

|---|---|

| FX hedge coverage | 50–70% |

| Cotton price change | +15% |

| Container freight vs pre‑pandemic | +60% |

| Garment wage inflation | +5–8% |

| OECD policy rates | ~3.2% |

| Cash & equivalents | ¥1.03tn |

| SSS growth | 1.4% |

| China disposable income | +6.9% |

| US real DPI | −0.7% |

Full Version Awaits

Fast Retailing PESTLE Analysis

The preview shown here is the exact Fast Retailing PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.