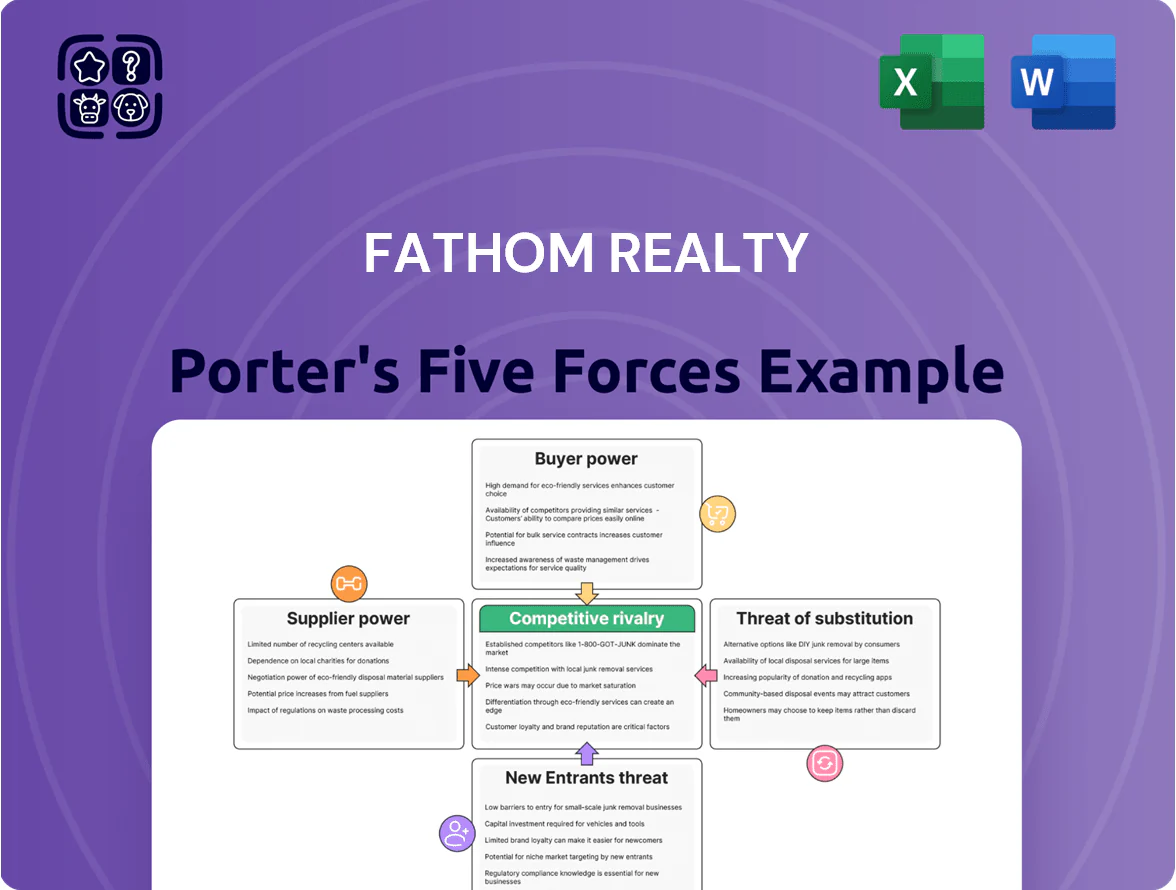

Fathom Realty Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Fathom Realty operates in a competitive, fragmented brokerage market where moderate buyer power, low supplier leverage, and significant threat from low-cost tech-enabled entrants shape margins and growth prospects; network effects and brand differentiation provide defensive advantages but escalating regulatory scrutiny and market cyclicality are real risks—this brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fathom Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on High-Performing Real Estate Agents

Fathom Realty depends on agents for listings and revenue; agents act as suppliers of labor and can move easily to flat-fee or cloud brokerages, giving them leverage.

By late 2025 top-tier agent scarcity rose—industry reports show U.S. agent headcount fell ~3% 2023–25—so Fathom must boost compensation and intelliAgent features to retain producers.

Reliance on Third-Party Cloud Infrastructure Providers

Fathom Realty runs on cloud platforms like Amazon Web Services (AWS) and Microsoft Azure, which supply its virtual office and data systems; in 2025 AWS and Azure together held ~60% of global cloud IaaS market, concentrating supplier power.

Switching clouds incurs high technical debt—migration often costs millions and takes months—so these providers can raise prices, feeding into Fathom’s operating margins and variable costs.

Influence of National and Local MLS Organizations

Multiple Listing Services (MLS) and the National Association of Realtors (NAR) supply core market data and legitimacy; Fathom pays MLS/NAR fees—often $500–$2,500 per office annually—and follows access rules so agents can list and search properties. Recent 2024–2025 legal settlements changing commission disclosures and broker compensation nudged market practices, but MLS/NAR still control distribution of 99% of US residential listings, keeping strong supplier power over Fathom’s operations.

Third-Party Lead Generation and Marketing Platforms

Agents in the Fathom Realty network often depend on third-party lead platforms like Zillow and Realtor.com, which together accounted for an estimated 60%+ of online home searches in 2024, giving them pricing and algorithm power over lead flow.

These suppliers can raise cost-per-lead (Zillow’s Premier Agent avg CPL rose ~15% in 2023–24) or tweak rankings, directly lowering agent productivity and ROI.

Fathom provides internal CRM, lead routing, and paid-ad tools to reduce dependence, but the dominance of external search platforms in consumer behavior keeps supplier power high.

- Third-party platforms drive 60%+ of searches (2024)

- Zillow Premier Agent CPL up ~15% (2023–24)

- Fathom tools: CRM, lead routing, paid-ad integrations

- Supplier power remains high due to consumer search habits

Professional Services and Compliance Vendors

Fathom relies on specialized suppliers for E&O insurance, legal compliance, and financial audits; as a public company these providers are critical for regulatory risk control, especially after 2023 SEC rule changes increasing disclosure and audit scrutiny.

The limited pool of national firms able to manage large real-estate volumes gives vendors moderate–high bargaining power, often commanding premiums; E&O rates for large brokerages rose ~12% in 2024 per industry reports.

- Essential services: E&O, legal, audit

- Public-company rules raise dependency

- Few national specialists → moderate–high leverage

- Industry E&O rates +12% in 2024

Supplier Power Squeezes Fathom: Rising Costs, Agent Shortage Threaten Margins

Suppliers—agents, cloud providers (AWS/Azure ~60% IaaS 2025), MLS/NAR (control ~99% listings), Zillow/Realtor.com (~60% searches 2024), and E&O/legal firms—hold high bargaining power; agent scarcity (-3% headcount 2023–25) and rising costs (Zillow CPL +15% 2023–24; E&O +12% 2024) pressure Fathom’s margins and require higher pay and tech investment.

| Supplier | Key metric |

|---|---|

| AWS/Azure | ~60% IaaS (2025) |

| MLS/NAR | ~99% listings |

| Zillow/Realtor | ~60% searches (2024) |

| Agents | -3% headcount (2023–25) |

| Costs | CPL +15% (2023–24); E&O +12% (2024) |

What is included in the product

Tailored Porter's Five Forces for Fathom Realty that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitutes—highlighting disruptive threats, pricing pressure, and strategic protections to inform investor, boardroom, or academic use.

One-sheet Porter’s Five Forces summary that clarifies competitive pressures instantly—ideal for fast, confident strategic decisions and slide-ready presentations.

Customers Bargaining Power

Agent Mobility and Low Switching Costs

In Fathom Realty’s model the agents are the paying customers, and industry data show 60–70% of U.S. agents consider platform fees when switching firms, so agent mobility is high. Moving to flat-fee or low-split rivals like eXp Realty or Real Brokerage often costs under $1,000 and hours of admin, making switching easy. This low switching cost forces Fathom to keep its $499–$2,999 fee tiers competitive and invest in tech: Fathom reported $24M tech spend in 2024 to curb churn.

Consumer Demand for Commission Transparency

By end-2025, survey data show 68% of US home sellers cite commission transparency as a key decision factor, making buyers and sellers more price-sensitive and able to demand lower fees from Fathom Realty agents; this erodes the brokerage’s gross commission income (Fathom reported $153.6M revenue in 2024) and forces agents to protect margins, risking demands for higher splits or extra services from Fathom if their take-home falls.

Influence of Large Productive Agent Teams

Large agent teams that produce 50%+ of a brokerage’s transactions, like Fathom Realty’s reported top teams contributing ~40–55% of unit volume in 2024, hold strong bargaining power and can demand bespoke admin support, lower per-transaction caps, or dedicated marketing funds. These mega-teams often generate outsized revenue—example: a 100-agent team closing 1,200 sides/year at a $3,000 average commission equals $3.6M gross—so Fathom must weigh concessions against platform-wide profitability. Balancing tailored deals for high-leverage teams while protecting average margins is critical to sustaining a scalable model.

Widespread Access to Real Estate Data

Widespread access to public portals like Zillow and Realtor.com has cut brokerages' info advantage; 89% of U.S. buyers used online sites in 2024, per NAR, so customers now know comps and trends before contacting agents.

For Fathom Realty this means agents must shift toward advisory work—pricing strategy, negotiation, and staging—to justify commissions; firms reporting higher agent advisory time saw 12–18% higher close rates in 2023.

- 89% buyers used online listings (NAR 2024)

- Clients arrive with comps, reducing info rent

- Advisory services raise close rates ~12–18%

Economic Sensitivity to Interest Rates and Inventory

By late 2025, US mortgage rates averaging ~7.1% and national housing inventory down ~12% year-over-year shrink the buyer/seller pool, raising competition per lead for Fathom Realty and similar brokers.

Fewer active customers gain leverage to demand lower fees and premium services; conversion costs rise as agents spend more touchpoints per closed deal.

- Mortgage rate (Q3–Q4 2025): ~7.1%

- Inventory change YoY: −12%

- Fewer leads → higher acquisition cost per sale

- Customers push for fee cuts and higher service

Fathom fights churn with $499–$2,999 tiers, $24M tech push amid rising fee pressure

Agents are Fathom’s paying customers and switching is easy—60–70% consider fees when switching; rivals under $1,000 lower cost to move—so Fathom keeps $499–$2,999 tiers competitive and spent $24M on tech in 2024 to curb churn. Commission transparency (68% of sellers care by 2025) and portals (89% buyers used online listings in 2024) raise price pressure; top teams (40–55% volume) demand bespoke deals, squeezing margins.

| Metric | Value |

|---|---|

| Agent fee tiers (2024) | $499–$2,999 |

| Tech spend (Fathom 2024) | $24M |

| Revenue (Fathom 2024) | $153.6M |

| Buyers using portals (NAR 2024) | 89% |

| Sellers valuing transparency (2025) | 68% |

| Top teams' volume share (2024) | 40–55% |

Preview Before You Purchase

Fathom Realty Porter's Five Forces Analysis

This preview shows the exact Fathom Realty Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready to download immediately after purchase.

No placeholders, no samples: the document displayed here is the final deliverable and is identical to the file delivered upon payment.

You’re viewing the complete analysis—professional, actionable, and available for instant use the moment you complete your purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Fathom Realty operates in a competitive, fragmented brokerage market where moderate buyer power, low supplier leverage, and significant threat from low-cost tech-enabled entrants shape margins and growth prospects; network effects and brand differentiation provide defensive advantages but escalating regulatory scrutiny and market cyclicality are real risks—this brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fathom Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on High-Performing Real Estate Agents

Fathom Realty depends on agents for listings and revenue; agents act as suppliers of labor and can move easily to flat-fee or cloud brokerages, giving them leverage.

By late 2025 top-tier agent scarcity rose—industry reports show U.S. agent headcount fell ~3% 2023–25—so Fathom must boost compensation and intelliAgent features to retain producers.

Reliance on Third-Party Cloud Infrastructure Providers

Fathom Realty runs on cloud platforms like Amazon Web Services (AWS) and Microsoft Azure, which supply its virtual office and data systems; in 2025 AWS and Azure together held ~60% of global cloud IaaS market, concentrating supplier power.

Switching clouds incurs high technical debt—migration often costs millions and takes months—so these providers can raise prices, feeding into Fathom’s operating margins and variable costs.

Influence of National and Local MLS Organizations

Multiple Listing Services (MLS) and the National Association of Realtors (NAR) supply core market data and legitimacy; Fathom pays MLS/NAR fees—often $500–$2,500 per office annually—and follows access rules so agents can list and search properties. Recent 2024–2025 legal settlements changing commission disclosures and broker compensation nudged market practices, but MLS/NAR still control distribution of 99% of US residential listings, keeping strong supplier power over Fathom’s operations.

Third-Party Lead Generation and Marketing Platforms

Agents in the Fathom Realty network often depend on third-party lead platforms like Zillow and Realtor.com, which together accounted for an estimated 60%+ of online home searches in 2024, giving them pricing and algorithm power over lead flow.

These suppliers can raise cost-per-lead (Zillow’s Premier Agent avg CPL rose ~15% in 2023–24) or tweak rankings, directly lowering agent productivity and ROI.

Fathom provides internal CRM, lead routing, and paid-ad tools to reduce dependence, but the dominance of external search platforms in consumer behavior keeps supplier power high.

- Third-party platforms drive 60%+ of searches (2024)

- Zillow Premier Agent CPL up ~15% (2023–24)

- Fathom tools: CRM, lead routing, paid-ad integrations

- Supplier power remains high due to consumer search habits

Professional Services and Compliance Vendors

Fathom relies on specialized suppliers for E&O insurance, legal compliance, and financial audits; as a public company these providers are critical for regulatory risk control, especially after 2023 SEC rule changes increasing disclosure and audit scrutiny.

The limited pool of national firms able to manage large real-estate volumes gives vendors moderate–high bargaining power, often commanding premiums; E&O rates for large brokerages rose ~12% in 2024 per industry reports.

- Essential services: E&O, legal, audit

- Public-company rules raise dependency

- Few national specialists → moderate–high leverage

- Industry E&O rates +12% in 2024

Supplier Power Squeezes Fathom: Rising Costs, Agent Shortage Threaten Margins

Suppliers—agents, cloud providers (AWS/Azure ~60% IaaS 2025), MLS/NAR (control ~99% listings), Zillow/Realtor.com (~60% searches 2024), and E&O/legal firms—hold high bargaining power; agent scarcity (-3% headcount 2023–25) and rising costs (Zillow CPL +15% 2023–24; E&O +12% 2024) pressure Fathom’s margins and require higher pay and tech investment.

| Supplier | Key metric |

|---|---|

| AWS/Azure | ~60% IaaS (2025) |

| MLS/NAR | ~99% listings |

| Zillow/Realtor | ~60% searches (2024) |

| Agents | -3% headcount (2023–25) |

| Costs | CPL +15% (2023–24); E&O +12% (2024) |

What is included in the product

Tailored Porter's Five Forces for Fathom Realty that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitutes—highlighting disruptive threats, pricing pressure, and strategic protections to inform investor, boardroom, or academic use.

One-sheet Porter’s Five Forces summary that clarifies competitive pressures instantly—ideal for fast, confident strategic decisions and slide-ready presentations.

Customers Bargaining Power

Agent Mobility and Low Switching Costs

In Fathom Realty’s model the agents are the paying customers, and industry data show 60–70% of U.S. agents consider platform fees when switching firms, so agent mobility is high. Moving to flat-fee or low-split rivals like eXp Realty or Real Brokerage often costs under $1,000 and hours of admin, making switching easy. This low switching cost forces Fathom to keep its $499–$2,999 fee tiers competitive and invest in tech: Fathom reported $24M tech spend in 2024 to curb churn.

Consumer Demand for Commission Transparency

By end-2025, survey data show 68% of US home sellers cite commission transparency as a key decision factor, making buyers and sellers more price-sensitive and able to demand lower fees from Fathom Realty agents; this erodes the brokerage’s gross commission income (Fathom reported $153.6M revenue in 2024) and forces agents to protect margins, risking demands for higher splits or extra services from Fathom if their take-home falls.

Influence of Large Productive Agent Teams

Large agent teams that produce 50%+ of a brokerage’s transactions, like Fathom Realty’s reported top teams contributing ~40–55% of unit volume in 2024, hold strong bargaining power and can demand bespoke admin support, lower per-transaction caps, or dedicated marketing funds. These mega-teams often generate outsized revenue—example: a 100-agent team closing 1,200 sides/year at a $3,000 average commission equals $3.6M gross—so Fathom must weigh concessions against platform-wide profitability. Balancing tailored deals for high-leverage teams while protecting average margins is critical to sustaining a scalable model.

Widespread Access to Real Estate Data

Widespread access to public portals like Zillow and Realtor.com has cut brokerages' info advantage; 89% of U.S. buyers used online sites in 2024, per NAR, so customers now know comps and trends before contacting agents.

For Fathom Realty this means agents must shift toward advisory work—pricing strategy, negotiation, and staging—to justify commissions; firms reporting higher agent advisory time saw 12–18% higher close rates in 2023.

- 89% buyers used online listings (NAR 2024)

- Clients arrive with comps, reducing info rent

- Advisory services raise close rates ~12–18%

Economic Sensitivity to Interest Rates and Inventory

By late 2025, US mortgage rates averaging ~7.1% and national housing inventory down ~12% year-over-year shrink the buyer/seller pool, raising competition per lead for Fathom Realty and similar brokers.

Fewer active customers gain leverage to demand lower fees and premium services; conversion costs rise as agents spend more touchpoints per closed deal.

- Mortgage rate (Q3–Q4 2025): ~7.1%

- Inventory change YoY: −12%

- Fewer leads → higher acquisition cost per sale

- Customers push for fee cuts and higher service

Fathom fights churn with $499–$2,999 tiers, $24M tech push amid rising fee pressure

Agents are Fathom’s paying customers and switching is easy—60–70% consider fees when switching; rivals under $1,000 lower cost to move—so Fathom keeps $499–$2,999 tiers competitive and spent $24M on tech in 2024 to curb churn. Commission transparency (68% of sellers care by 2025) and portals (89% buyers used online listings in 2024) raise price pressure; top teams (40–55% volume) demand bespoke deals, squeezing margins.

| Metric | Value |

|---|---|

| Agent fee tiers (2024) | $499–$2,999 |

| Tech spend (Fathom 2024) | $24M |

| Revenue (Fathom 2024) | $153.6M |

| Buyers using portals (NAR 2024) | 89% |

| Sellers valuing transparency (2025) | 68% |

| Top teams' volume share (2024) | 40–55% |

Preview Before You Purchase

Fathom Realty Porter's Five Forces Analysis

This preview shows the exact Fathom Realty Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready to download immediately after purchase.

No placeholders, no samples: the document displayed here is the final deliverable and is identical to the file delivered upon payment.

You’re viewing the complete analysis—professional, actionable, and available for instant use the moment you complete your purchase.