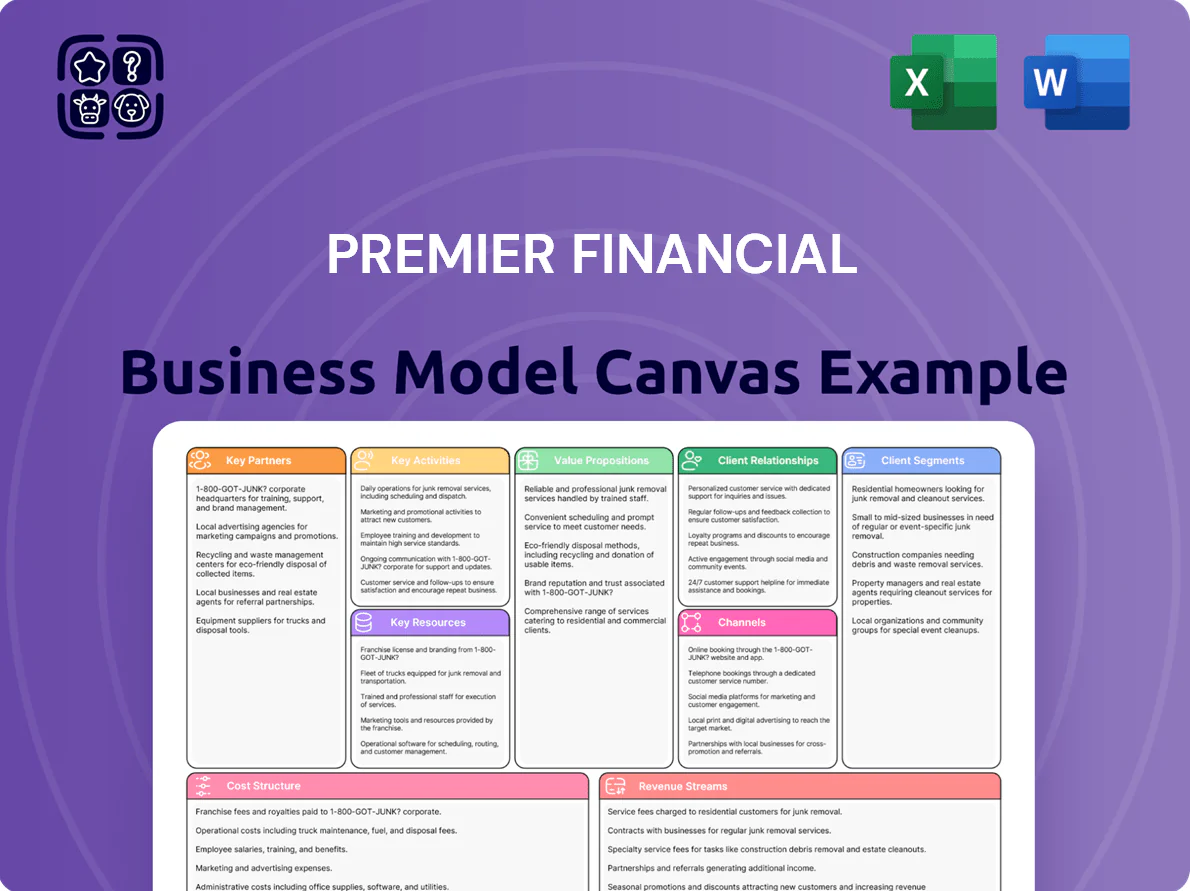

Premier Financial Business Model Canvas

Download Premier Financial’s Complete Business Model Canvas — Actionable Investor Blueprint

Unlock the full strategic blueprint behind Premier Financial’s business model—download the complete Business Model Canvas to see customer segments, value propositions, revenue streams, and cost drivers laid out with company-specific detail; ideal for investors, consultants, and founders who want actionable, ready-to-use insights to benchmark, plan, and scale.

Partnerships

Fintech and Digital Infrastructure Providers

Fintech and digital infrastructure partners supply the tech backbone for Premier Financial’s mobile and online banking, with 2024 industry stats showing banks using third-party platforms cut time-to-market by ~40% and lower infra costs by ~25%; payment processors and cybersecurity vendors (SOC 2/ISO 27001 compliant) keep retail and commercial transactions secure and efficient, supporting >99.95% uptime and handling spikes above $2B daily payment volume.

Federal Reserve and Regulatory Agencies

Maintaining close ties with the Federal Reserve and regulators secures liquidity lines and compliance; in 2024 the Fed’s standing repo facility and discount window capacity exceeded $500B, underscoring the backstop role during stress. Adhering to Fed and OCC rules—capital ratios (CET1 ≥4.5%), liquidity coverage ratio guidance, and regular supervisory exams—protects Premier Financial’s charter and legal standing.

Mortgage Secondary Market Investors

Premier sells mortgage loans to Fannie Mae and Freddie Mac, offloading roughly 60%–75% of originations in 2024 to cut balance-sheet risk and free capital for new lending.

It often keeps servicing rights, earning fee income (about 40–60 bps per loan) while lowering long-term rate exposure and preserving liquidity—cash from sales funded 18% of loan growth in 2024.

Local Community and Business Associations

Strategic alliances with Ohio, Michigan, and Indiana chambers of commerce and economic development groups surface commercial lending deals—these partnerships helped Premier Financial originate about $420M in regional commercial loans in 2024, embedding the bank in local supply chains and boosting referrals from small businesses.

They also advance Community Reinvestment Act goals by directing credit to low- and moderate-income areas; in 2024 Premier reported 18% of new business loans to LMI tracts, strengthening trust with local entrepreneurs.

- 2024 regional commercial originations: ~$420M

- Share to LMI tracts (2024): 18%

- Primary states: Ohio, Michigan, Indiana

- Partners: local chambers, economic development agencies

Wealth Management and Insurance Third-Parties

Premier partners with external investment platforms (e.g., BlackRock iShares, Vanguard personal advisor services) and insurance underwriters (top 5 life insurers) to offer a full suite of wealth-management and personal-insurance products while avoiding full underwriting exposure; in 2025 this model helped cross-sell to 38% of HNW clients, boosting fee revenue by 14% year-over-year.

- Access to diversified investments via partner platforms

- Underwriting risk transferred to insurers

- 38% HNW cross-sell rate (2025)

- 14% fee-revenue increase (2025)

Premier partners power 99.95% uptime, $2B peak payments, $420M originations

Premier’s key partners supply tech, payments, liquidity, mortgage buyers, regional development groups, and asset/insurance platforms—enabling 99.95%+ uptime, $2B+ peak daily payments, $420M regional commercial originations (2024), 18% LMI lending share (2024), 60–75% mortgage sales, 38% HNW cross-sell and +14% fee revenue (2025).

| Metric | Value |

|---|---|

| Uptime | 99.95%+ |

| Peak daily payments | $2B+ |

| Regional originations (2024) | $420M |

| LMI share (2024) | 18% |

| Mortgage sales | 60–75% |

| HNW cross-sell (2025) | 38% |

| Fee rev. growth (2025) | +14% |

What is included in the product

A comprehensive, pre-written Business Model Canvas aligned with Premier Financial’s strategy, detailing customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships with actionable insights and competitive analysis for presentations and funding discussions.

Condenses your firm's strategy into a digestible one-page Business Model Canvas with editable cells, saving hours of formatting while enabling quick comparison, team collaboration, and fast executive-ready deliverables.

Activities

Credit Underwriting and Risk Assessment

Digital Banking Development and Maintenance

As of late 2025, Premier Financial prioritizes digital banking development: rolling out mobile app upgrades quarterly, targeting 99.99% uptime, and adding real-time payments (aligned with faster-pay rails; 24% of deposits now mobile-originated).

Commercial and Agricultural Relationship Management

The bank actively manages relationships with business and farm owners via regular site visits, financial consultations, and tailored financing and treasury solutions, structuring complex loan packages that drove 18% year-over-year commercial loan growth and supported $2.4bn in farm lending in 2025; strong relationship management lifted commercial customer retention to 92% and produced 14% CAGR in commercial deposits over 2022–2025.

Regulatory Compliance and Internal Auditing

The bank must continuously monitor operations to meet evolving financial regulations and AML laws, using internal reporting, staff training, and periodic audits; non-compliance fines averaged $4.2B across banks in 2023, so rigorous controls protect capital and reputation.

Maintaining a robust compliance framework—annual audit cycles, quarterly risk reporting, and 30%+ annual training completion—reduces regulatory breach risk and operational losses.

- Continuous monitoring: real-time transaction screening

- Internal reporting: monthly compliance KPIs

- Staff training: 30%+ yearly completion rate

- Periodic audits: annual external, quarterly internal

- Goal: minimize fines (avg $4.2B in 2023)

Asset Liability Management and Treasury Operations

The firm actively manages its balance sheet to widen net interest margin, targeting a spread improvement of ~15–25 bps versus 2024 industry median by repricing loans and deposits and shifting portfolio duration as rates move.

Treasury operations maintain liquidity buffers—liquid assets at 8–12% of deposits and contingency funding lines covering 3–6 months—to meet withdrawals and fund growth.

- Target NIM lift: 15–25 bps

- Liquid assets: 8–12% of deposits

- Contingency lines: 3–6 months funding

- Duration adjusted with rate forecasts

Prudent growth: 10% loans, NPL<2%, CET1≥12%, 24% mobile deposits by 2025

| Metric | Target/2025 |

|---|---|

| NPL | <2.0% |

| ECL | <1.5% loans |

| CET1 | ≥12% |

| Loan growth | 10% YoY |

| Mobile deposits | 24% |

| Liquidity | 8–12% deposits |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the exact Premier Financial Business Model Canvas you’ll receive—no mockups or samples—showing the real structure and content from the final file.

When you purchase, you’ll get this same professional document in editable formats, fully complete and ready for use in presentations, planning, or sharing.

What’s shown here is the genuine deliverable: no surprises, no fillers—just the full, ready-to-edit Business Model Canvas as previewed.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Premier Financial’s Complete Business Model Canvas — Actionable Investor Blueprint

Unlock the full strategic blueprint behind Premier Financial’s business model—download the complete Business Model Canvas to see customer segments, value propositions, revenue streams, and cost drivers laid out with company-specific detail; ideal for investors, consultants, and founders who want actionable, ready-to-use insights to benchmark, plan, and scale.

Partnerships

Fintech and Digital Infrastructure Providers

Fintech and digital infrastructure partners supply the tech backbone for Premier Financial’s mobile and online banking, with 2024 industry stats showing banks using third-party platforms cut time-to-market by ~40% and lower infra costs by ~25%; payment processors and cybersecurity vendors (SOC 2/ISO 27001 compliant) keep retail and commercial transactions secure and efficient, supporting >99.95% uptime and handling spikes above $2B daily payment volume.

Federal Reserve and Regulatory Agencies

Maintaining close ties with the Federal Reserve and regulators secures liquidity lines and compliance; in 2024 the Fed’s standing repo facility and discount window capacity exceeded $500B, underscoring the backstop role during stress. Adhering to Fed and OCC rules—capital ratios (CET1 ≥4.5%), liquidity coverage ratio guidance, and regular supervisory exams—protects Premier Financial’s charter and legal standing.

Mortgage Secondary Market Investors

Premier sells mortgage loans to Fannie Mae and Freddie Mac, offloading roughly 60%–75% of originations in 2024 to cut balance-sheet risk and free capital for new lending.

It often keeps servicing rights, earning fee income (about 40–60 bps per loan) while lowering long-term rate exposure and preserving liquidity—cash from sales funded 18% of loan growth in 2024.

Local Community and Business Associations

Strategic alliances with Ohio, Michigan, and Indiana chambers of commerce and economic development groups surface commercial lending deals—these partnerships helped Premier Financial originate about $420M in regional commercial loans in 2024, embedding the bank in local supply chains and boosting referrals from small businesses.

They also advance Community Reinvestment Act goals by directing credit to low- and moderate-income areas; in 2024 Premier reported 18% of new business loans to LMI tracts, strengthening trust with local entrepreneurs.

- 2024 regional commercial originations: ~$420M

- Share to LMI tracts (2024): 18%

- Primary states: Ohio, Michigan, Indiana

- Partners: local chambers, economic development agencies

Wealth Management and Insurance Third-Parties

Premier partners with external investment platforms (e.g., BlackRock iShares, Vanguard personal advisor services) and insurance underwriters (top 5 life insurers) to offer a full suite of wealth-management and personal-insurance products while avoiding full underwriting exposure; in 2025 this model helped cross-sell to 38% of HNW clients, boosting fee revenue by 14% year-over-year.

- Access to diversified investments via partner platforms

- Underwriting risk transferred to insurers

- 38% HNW cross-sell rate (2025)

- 14% fee-revenue increase (2025)

Premier partners power 99.95% uptime, $2B peak payments, $420M originations

Premier’s key partners supply tech, payments, liquidity, mortgage buyers, regional development groups, and asset/insurance platforms—enabling 99.95%+ uptime, $2B+ peak daily payments, $420M regional commercial originations (2024), 18% LMI lending share (2024), 60–75% mortgage sales, 38% HNW cross-sell and +14% fee revenue (2025).

| Metric | Value |

|---|---|

| Uptime | 99.95%+ |

| Peak daily payments | $2B+ |

| Regional originations (2024) | $420M |

| LMI share (2024) | 18% |

| Mortgage sales | 60–75% |

| HNW cross-sell (2025) | 38% |

| Fee rev. growth (2025) | +14% |

What is included in the product

A comprehensive, pre-written Business Model Canvas aligned with Premier Financial’s strategy, detailing customer segments, channels, value propositions, revenue streams, cost structure, key partners, activities, resources, and customer relationships with actionable insights and competitive analysis for presentations and funding discussions.

Condenses your firm's strategy into a digestible one-page Business Model Canvas with editable cells, saving hours of formatting while enabling quick comparison, team collaboration, and fast executive-ready deliverables.

Activities

Credit Underwriting and Risk Assessment

Digital Banking Development and Maintenance

As of late 2025, Premier Financial prioritizes digital banking development: rolling out mobile app upgrades quarterly, targeting 99.99% uptime, and adding real-time payments (aligned with faster-pay rails; 24% of deposits now mobile-originated).

Commercial and Agricultural Relationship Management

The bank actively manages relationships with business and farm owners via regular site visits, financial consultations, and tailored financing and treasury solutions, structuring complex loan packages that drove 18% year-over-year commercial loan growth and supported $2.4bn in farm lending in 2025; strong relationship management lifted commercial customer retention to 92% and produced 14% CAGR in commercial deposits over 2022–2025.

Regulatory Compliance and Internal Auditing

The bank must continuously monitor operations to meet evolving financial regulations and AML laws, using internal reporting, staff training, and periodic audits; non-compliance fines averaged $4.2B across banks in 2023, so rigorous controls protect capital and reputation.

Maintaining a robust compliance framework—annual audit cycles, quarterly risk reporting, and 30%+ annual training completion—reduces regulatory breach risk and operational losses.

- Continuous monitoring: real-time transaction screening

- Internal reporting: monthly compliance KPIs

- Staff training: 30%+ yearly completion rate

- Periodic audits: annual external, quarterly internal

- Goal: minimize fines (avg $4.2B in 2023)

Asset Liability Management and Treasury Operations

The firm actively manages its balance sheet to widen net interest margin, targeting a spread improvement of ~15–25 bps versus 2024 industry median by repricing loans and deposits and shifting portfolio duration as rates move.

Treasury operations maintain liquidity buffers—liquid assets at 8–12% of deposits and contingency funding lines covering 3–6 months—to meet withdrawals and fund growth.

- Target NIM lift: 15–25 bps

- Liquid assets: 8–12% of deposits

- Contingency lines: 3–6 months funding

- Duration adjusted with rate forecasts

Prudent growth: 10% loans, NPL<2%, CET1≥12%, 24% mobile deposits by 2025

| Metric | Target/2025 |

|---|---|

| NPL | <2.0% |

| ECL | <1.5% loans |

| CET1 | ≥12% |

| Loan growth | 10% YoY |

| Mobile deposits | 24% |

| Liquidity | 8–12% deposits |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the exact Premier Financial Business Model Canvas you’ll receive—no mockups or samples—showing the real structure and content from the final file.

When you purchase, you’ll get this same professional document in editable formats, fully complete and ready for use in presentations, planning, or sharing.

What’s shown here is the genuine deliverable: no surprises, no fillers—just the full, ready-to-edit Business Model Canvas as previewed.