Federal Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

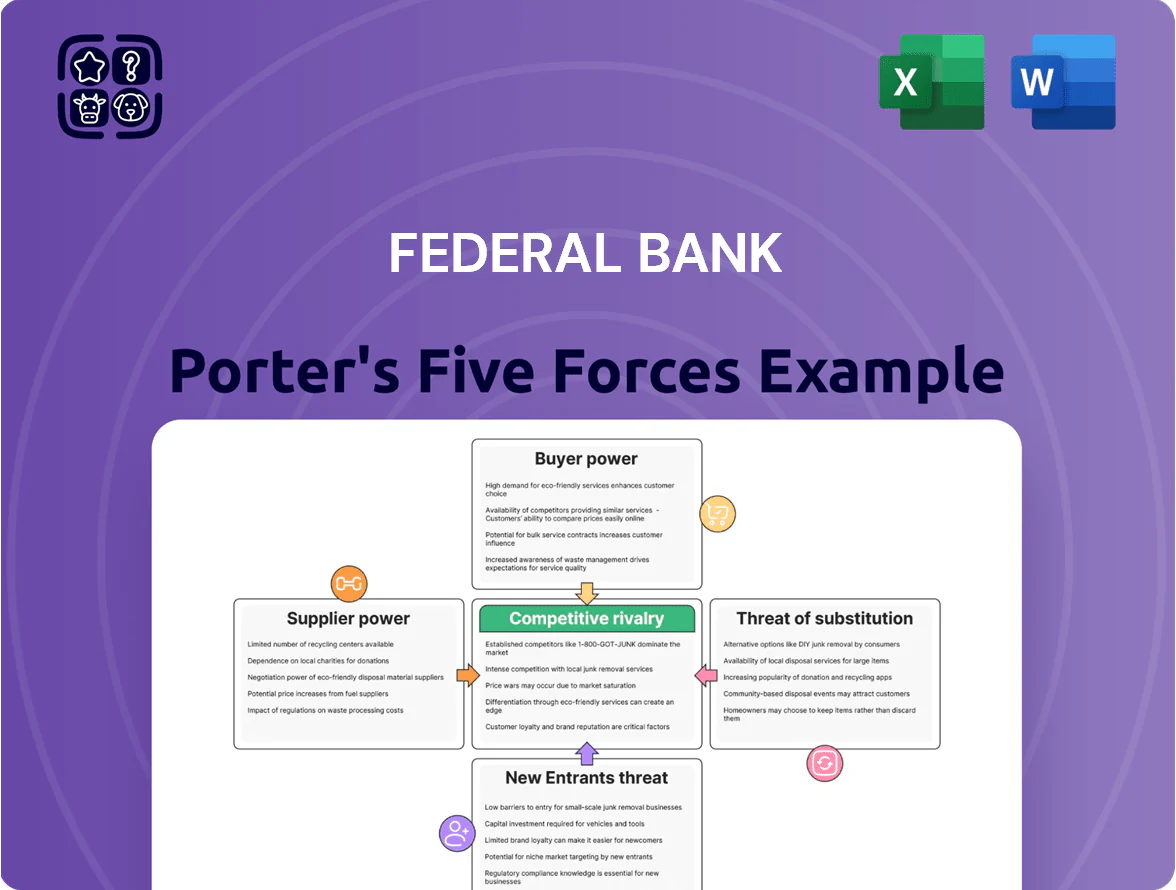

Federal Bank faces moderate competitive rivalry with strong regional presence but pressure from larger private banks and fintechs eroding margins.

Supplier power is low given diversified funding, while buyer power rises as customers demand digital services and fee transparency.

Threat of new entrants and substitutes is growing—digital challengers and NBFCs target retail segments—heightening innovation urgency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Federal Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of Skilled Labor

The primary suppliers for Federal Bank are its employees and professional talent pool; by late 2025 demand for fintech, data analytics, and risk management skills in Indian banking rose ~18% year-on-year, per Naukri Hiring Intent Index, boosting mobility. This competition gives high-performing professionals moderate bargaining power: average salary premium for specialized roles reached 22% above baseline bank roles in 2025. Retention costs rose 6–9%.

Technology and Infrastructure Providers

Federal Bank depends on third-party vendors for core banking, cloud, and cybersecurity; in 2024 it spent about ₹620 crore on IT and digital investments, increasing supplier leverage. Major global and domestic IT firms command pricing power because platform migration can cost hundreds of crores and take 12–24 months. Keeping these partnerships is vital for the bank’s digital-first strategy and operational resilience, so supplier bargaining power remains high.

Cost of Capital and Depositors

Retail and institutional depositors are Federal Bank’s primary capital suppliers; individuals have low singular power, but collective flows respond to RBI policy and the 2024-25 repo rate at 6.5%.

To protect its March 2025 CASA of ~33% and low-cost funding, Federal Bank must offer competitive deposit rates; a 50 bp hike in market rates can cut CASA growth and raise funding cost quickly.

Regulatory Compliance and Central Bank Influence

The Reserve Bank of India (RBI) functions as a supplier of regulation and liquidity; Federal Bank must hold a statutory CRR of 4.0% and SLR of 18.0% (RBI, Dec 2025), constraining deployable lendable funds and deposit pricing. Regulatory costs—compliance, reporting, and mandatory holdings—are non-negotiable and reduce loanable assets and interest margin.

- RBI-set CRR 4.0%

- SLR 18.0%

- Reduces lendable resources and NIM

- Liquidity ops via RBI open market tools

Outsourced Service Partners

Federal Bank outsources ATM maintenance, cash logistics and marketing to multiple vendors, creating dependency for physical reach and service continuity despite a crowded supplier market; in 2024~25 the bank operated ~3,500+ ATMs and handled ~₹1,200 crore cash logistics annually, which raises supplier importance.

Diversifying vendors regionally and running competitive tendering can cut supplier leverage—targeting a 20–30% supplier-share cap per region would lower disruption risk and bargaining power.

- ~3,500+ ATMs (2024–25)

- ₹1,200 crore annual cash logistics (approx.)

- Many vendors, but high dependency for operations

- Recommendation: 20–30% max supplier share per region

Mixed supplier power: high IT/talent leverage, regulatory cash constraints, 3,500 ATMs

Suppliers—employees, IT/cloud/cyber vendors, depositors, RBI, and cash/ATM vendors—exert mixed power: talent and IT vendors have moderate-to-high leverage (22% salary premium; ₹620 crore IT spend in 2024), depositors low individual power but sensitive to repo (6.5% in 2024–25), RBI mandates CRR 4.0%/SLR 18.0% (Dec 2025) constrain funds, and ~3,500 ATMs with ~₹1,200 crore cash logistics raise operational dependence.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| IT spend | ₹ crore | 620 |

| Talent premium | % over baseline | 22 |

| CASA | % (Mar 2025) | 33 |

| Repo rate | % (2024–25) | 6.5 |

| CRR / SLR | % (RBI Dec 2025) | 4.0 / 18.0 |

| ATMs | count | ~3,500 |

| Cash logistics | ₹ crore | ~1,200 |

What is included in the product

Tailored Porter's Five Forces analysis for Federal Bank revealing competitive pressures, buyer and supplier influence, entry barriers, substitutes, and potential disruptors to guide strategic positioning and profitability.

One-sheet Porter's Five Forces for Federal Bank—quickly pinpoint competitive pressures and strategies to relieve margin squeeze, with customizable force levels and a clean layout ready for decks.

Customers Bargaining Power

High Price Sensitivity in Retail Lending

Retail borrowers in India show high interest-rate sensitivity: as of FY2024 Indian banks’ average retail loan rate hovered around 9.2% (RBI data), and Federal Bank’s retail loan yield was 8.9% in FY2024, so even 20–50 bps cuts shift demand. With 20+ large public and private banks offering similar home, auto, and personal loans, switching costs are low and customers chase lower EMIs, forcing Federal Bank to keep tight pricing and boost service quality to retain retail customers.

Low Switching Costs for Digital Users

The rise of UPI (over 7.5 billion monthly transactions in India as of Dec 2025) and mobile banking apps means customers can hold multiple accounts and move funds instantly, reducing switching costs and raising their bargaining power against banks like Federal Bank. To retain users, Federal Bank has upgraded its FedMobile app and integrated services—digital CASA grew 18% YoY in FY2024—aiming to boost stickiness through payments, wealth, and loan features.

Corporate Client Negotiation Leverage

Large corporate borrowers wield strong leverage: in 2024 top 100 Indian corporates sourced over 40% of their funding via capital markets, so they press banks like Federal Bank for single-digit spreads and bespoke treasury deals.

These clients commonly negotiate lower rates and cash-management fees; Federal Bank must offer sector-specific solutions, digitized treasury platforms, and dedicated RM teams to retain accounts generating >30% of wholesale loan book income.

Access to Diverse Financial Products

Impact of Financial Literacy and Transparency

Rising financial literacy and online comparison tools mean customers choose banks with clear pricing; 58% of Indian retail borrowers used comparison sites in 2024, per a 2025 industry survey.

Transparency on fees is now expected; 72% of customers switched banks in 2023–24 citing hidden charges, so Federal Bank must publish clear fee schedules and plain disclosures.

Clear communication and fair practices cut churn risk—each 1% reduction in perceived opacity can lower retail attrition by ~0.4 percentage points, based on 2024 banking metrics.

- 58% used comparison tools (2024)

- 72% switched over hidden fees (2023–24)

- 1% opacity drop ≈ 0.4ppt lower churn

Rising customer power, tight spreads: digital churn & mutual funds squeeze bank yields

Customers hold high bargaining power: retail rate sensitivity (bank retail loan yield 8.9% FY2024) and low switching costs force tight pricing; digital channels (UPI >7.5bn monthly txn Dec 2025) and comparison tools (58% used 2024) raise churn risk; corporates demand single-digit spreads, supplying >30% wholesale loan income; mutual fund AUM Rs 48.3 tn (2025) shifts deposits to higher-yield options.

| Metric | Value |

|---|---|

| Fed Bank retail yield FY2024 | 8.9% |

| Bank retail rate avg FY2024 (India) | 9.2% |

| UPI monthly txns | 7.5bn (Dec 2025) |

| Mutual fund AUM | Rs 48.3 tn (2025) |

| Comparison tool use | 58% (2024) |

Preview the Actual Deliverable

Federal Bank Porter's Five Forces Analysis

This preview shows the exact Federal Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written analysis you'll get—fully formatted and ready to use the moment you buy. You're looking at the actual file; once you complete your purchase, you’ll get instant access to this exact document. No mockups, no samples—download-ready.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Federal Bank faces moderate competitive rivalry with strong regional presence but pressure from larger private banks and fintechs eroding margins.

Supplier power is low given diversified funding, while buyer power rises as customers demand digital services and fee transparency.

Threat of new entrants and substitutes is growing—digital challengers and NBFCs target retail segments—heightening innovation urgency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Federal Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of Skilled Labor

The primary suppliers for Federal Bank are its employees and professional talent pool; by late 2025 demand for fintech, data analytics, and risk management skills in Indian banking rose ~18% year-on-year, per Naukri Hiring Intent Index, boosting mobility. This competition gives high-performing professionals moderate bargaining power: average salary premium for specialized roles reached 22% above baseline bank roles in 2025. Retention costs rose 6–9%.

Technology and Infrastructure Providers

Federal Bank depends on third-party vendors for core banking, cloud, and cybersecurity; in 2024 it spent about ₹620 crore on IT and digital investments, increasing supplier leverage. Major global and domestic IT firms command pricing power because platform migration can cost hundreds of crores and take 12–24 months. Keeping these partnerships is vital for the bank’s digital-first strategy and operational resilience, so supplier bargaining power remains high.

Cost of Capital and Depositors

Retail and institutional depositors are Federal Bank’s primary capital suppliers; individuals have low singular power, but collective flows respond to RBI policy and the 2024-25 repo rate at 6.5%.

To protect its March 2025 CASA of ~33% and low-cost funding, Federal Bank must offer competitive deposit rates; a 50 bp hike in market rates can cut CASA growth and raise funding cost quickly.

Regulatory Compliance and Central Bank Influence

The Reserve Bank of India (RBI) functions as a supplier of regulation and liquidity; Federal Bank must hold a statutory CRR of 4.0% and SLR of 18.0% (RBI, Dec 2025), constraining deployable lendable funds and deposit pricing. Regulatory costs—compliance, reporting, and mandatory holdings—are non-negotiable and reduce loanable assets and interest margin.

- RBI-set CRR 4.0%

- SLR 18.0%

- Reduces lendable resources and NIM

- Liquidity ops via RBI open market tools

Outsourced Service Partners

Federal Bank outsources ATM maintenance, cash logistics and marketing to multiple vendors, creating dependency for physical reach and service continuity despite a crowded supplier market; in 2024~25 the bank operated ~3,500+ ATMs and handled ~₹1,200 crore cash logistics annually, which raises supplier importance.

Diversifying vendors regionally and running competitive tendering can cut supplier leverage—targeting a 20–30% supplier-share cap per region would lower disruption risk and bargaining power.

- ~3,500+ ATMs (2024–25)

- ₹1,200 crore annual cash logistics (approx.)

- Many vendors, but high dependency for operations

- Recommendation: 20–30% max supplier share per region

Mixed supplier power: high IT/talent leverage, regulatory cash constraints, 3,500 ATMs

Suppliers—employees, IT/cloud/cyber vendors, depositors, RBI, and cash/ATM vendors—exert mixed power: talent and IT vendors have moderate-to-high leverage (22% salary premium; ₹620 crore IT spend in 2024), depositors low individual power but sensitive to repo (6.5% in 2024–25), RBI mandates CRR 4.0%/SLR 18.0% (Dec 2025) constrain funds, and ~3,500 ATMs with ~₹1,200 crore cash logistics raise operational dependence.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| IT spend | ₹ crore | 620 |

| Talent premium | % over baseline | 22 |

| CASA | % (Mar 2025) | 33 |

| Repo rate | % (2024–25) | 6.5 |

| CRR / SLR | % (RBI Dec 2025) | 4.0 / 18.0 |

| ATMs | count | ~3,500 |

| Cash logistics | ₹ crore | ~1,200 |

What is included in the product

Tailored Porter's Five Forces analysis for Federal Bank revealing competitive pressures, buyer and supplier influence, entry barriers, substitutes, and potential disruptors to guide strategic positioning and profitability.

One-sheet Porter's Five Forces for Federal Bank—quickly pinpoint competitive pressures and strategies to relieve margin squeeze, with customizable force levels and a clean layout ready for decks.

Customers Bargaining Power

High Price Sensitivity in Retail Lending

Retail borrowers in India show high interest-rate sensitivity: as of FY2024 Indian banks’ average retail loan rate hovered around 9.2% (RBI data), and Federal Bank’s retail loan yield was 8.9% in FY2024, so even 20–50 bps cuts shift demand. With 20+ large public and private banks offering similar home, auto, and personal loans, switching costs are low and customers chase lower EMIs, forcing Federal Bank to keep tight pricing and boost service quality to retain retail customers.

Low Switching Costs for Digital Users

The rise of UPI (over 7.5 billion monthly transactions in India as of Dec 2025) and mobile banking apps means customers can hold multiple accounts and move funds instantly, reducing switching costs and raising their bargaining power against banks like Federal Bank. To retain users, Federal Bank has upgraded its FedMobile app and integrated services—digital CASA grew 18% YoY in FY2024—aiming to boost stickiness through payments, wealth, and loan features.

Corporate Client Negotiation Leverage

Large corporate borrowers wield strong leverage: in 2024 top 100 Indian corporates sourced over 40% of their funding via capital markets, so they press banks like Federal Bank for single-digit spreads and bespoke treasury deals.

These clients commonly negotiate lower rates and cash-management fees; Federal Bank must offer sector-specific solutions, digitized treasury platforms, and dedicated RM teams to retain accounts generating >30% of wholesale loan book income.

Access to Diverse Financial Products

Impact of Financial Literacy and Transparency

Rising financial literacy and online comparison tools mean customers choose banks with clear pricing; 58% of Indian retail borrowers used comparison sites in 2024, per a 2025 industry survey.

Transparency on fees is now expected; 72% of customers switched banks in 2023–24 citing hidden charges, so Federal Bank must publish clear fee schedules and plain disclosures.

Clear communication and fair practices cut churn risk—each 1% reduction in perceived opacity can lower retail attrition by ~0.4 percentage points, based on 2024 banking metrics.

- 58% used comparison tools (2024)

- 72% switched over hidden fees (2023–24)

- 1% opacity drop ≈ 0.4ppt lower churn

Rising customer power, tight spreads: digital churn & mutual funds squeeze bank yields

Customers hold high bargaining power: retail rate sensitivity (bank retail loan yield 8.9% FY2024) and low switching costs force tight pricing; digital channels (UPI >7.5bn monthly txn Dec 2025) and comparison tools (58% used 2024) raise churn risk; corporates demand single-digit spreads, supplying >30% wholesale loan income; mutual fund AUM Rs 48.3 tn (2025) shifts deposits to higher-yield options.

| Metric | Value |

|---|---|

| Fed Bank retail yield FY2024 | 8.9% |

| Bank retail rate avg FY2024 (India) | 9.2% |

| UPI monthly txns | 7.5bn (Dec 2025) |

| Mutual fund AUM | Rs 48.3 tn (2025) |

| Comparison tool use | 58% (2024) |

Preview the Actual Deliverable

Federal Bank Porter's Five Forces Analysis

This preview shows the exact Federal Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written analysis you'll get—fully formatted and ready to use the moment you buy. You're looking at the actual file; once you complete your purchase, you’ll get instant access to this exact document. No mockups, no samples—download-ready.