Federal Boston Consulting Group Matrix

See the Bigger Picture

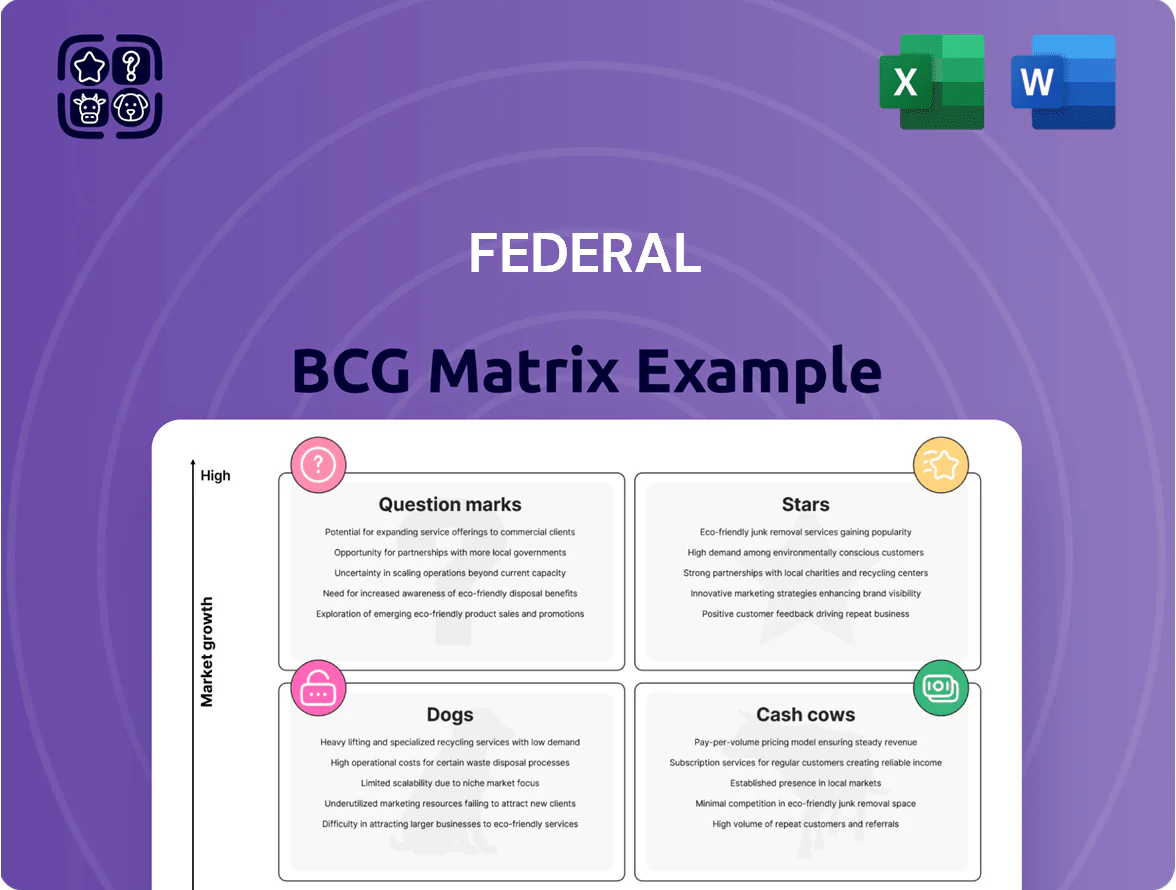

The Federal BCG Matrix snapshot highlights where key products sit across Stars, Cash Cows, Question Marks, and Dogs—revealing market share dynamics and growth potential to inform strategic moves. This preview outlines high-level placements and implications for capital allocation, but the full BCG Matrix provides quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide investment and product decisions. Purchase the complete report for a comprehensive, presentation-ready strategic tool.

Stars

Mixed-Use Premier Destinations

Mixed-Use Premier Destinations like Santana Row (San Jose) and Pike & Rose (North Bethesda) sit in Federal’s BCG Stars: they blend retail, office, and residential and deliver premium rents—average asking rents reached $89/SF for retail and $62/SF for office in 2024—and sustain >95% occupancy in affluent submarkets. Federal invested $220M in 2023–24 capital improvements to expand experiential offerings, keeping NOI growth near 8% year-over-year and defending market share.

Luxury Coastal Retail Clusters

Luxury coastal retail clusters in Southern California and the Northeast corridor act as Stars in the Federal BCG Matrix, driving growth with avg. annual NOI (net operating income) growth ~6–8% and rent CAGR ~4.5% since 2019; these markets account for ~28% of portfolio value and deliver top-quartile returns.

Integrated Residential Developments

Integrated residential developments—luxury units above or beside retail—are a high-growth segment for Federal, targeting a 12–15% CAGR in recurring revenue and leveraging a 2025 urban rental vacancy drop to 3.8% (CBRE, Q4 2024).

They diversify cash flow away from retail rent by adding longer-term rental income, with projected NOI margins of 30% once stabilized and yields modeled at 4.5% cap rates for prime assets in 2025.

Construction requires heavy cash: Federal estimates HKD 2.1–3.5 billion per project and negative FCF for 24–36 months, but market-share aims place these projects as leaders in the luxury rental niche.

Silicon Valley Commercial Assets

Silicon Valley Commercial Assets rank as Stars in Federal Realty’s BCG matrix, driven by $1,200+ median household incomes within a 3-mile radius and vacancy rates under 6% in 2024, signaling high growth and strong cash reinvestment potential.

Federal prioritizes redevelopment and amenity upgrades—added 120k sq ft of mixed-use space in 2023—targeting tech tenants and affluent consumers to sustain rent premiums and capture resilient demand.

- High-earning catchment: $1,200+ median monthly household income (2024)

- Low vacancy: <6% (2024)

- Recent redeploy: 120,000 sq ft added (2023)

- Focus: redevelopment, premium amenities, mixed-use

Sustainable Green-Certified Hubs

Federal’s LEED-certified hubs are market leaders as 78% of institutional tenants ranked ESG a top-3 lease factor in 2024, letting the trust command 7–12% rent premiums vs non-certified assets.

High upfront green capex (avg $30–60/sqft) is offset by rising demand: certified assets grew 22% market share in major CBDs from 2020–2024, boosting NOI and valuation multiples.

- 78% of tenants cite ESG top-3 (2024)

- 7–12% rent premium vs non-certified

- $30–60/sqft typical green capex

- 22% market-share growth (2020–2024)

Coastal & Mixed‑Use Drive Strong Cashflow: 6–8% NOI, 95% Occupancy, 4.5% Rent CAGR

Stars: mixed‑use and coastal luxury assets drive 6–8% NOI growth, 4.5% rent CAGR, ~95% occupancy; portfolio weight ~28%; LEED assets earn 7–12% rent premium; redevelopment capex HKD 2.1–3.5B/project, green capex $30–60/SF; Silicon Valley assets: <6% vacancy, $1,200+ median monthly household income (2024).

| Metric | Value |

|---|---|

| NOI growth | 6–8% |

| Rent CAGR | 4.5% |

| Occupancy | ~95% |

| Portfolio share | 28% |

What is included in the product

Comprehensive BCG Matrix review of the Federal's units with strategic guidance—invest, hold, or divest—plus trend-driven risks and advantages.

One-page federal BCG Matrix mapping agencies by mandate and budget to clarify strategy and resource allocation

Cash Cows

Grocery-Anchored Neighborhood Centers

Grocery-anchored neighborhood centers form the portfolio bedrock, delivering stable cash flow: average same-center NOI (net operating income) grew 3.4% in 2024 and occupancy stayed at 96.2% nationwide through Q4 2024.

These necessity-driven assets need little repositioning or heavy marketing, showing median lease renewals of 7.8 years and rent spread resilience during 2023–2024 disinflation.

Federal uses cash from these mature centers to fund new developments and pay steady dividends, with centers contributing roughly 41% of 2024 distributable cash flow to shareholders.

Established DC Metro Corridor Holdings

Established DC Metro Corridor Holdings are high-share assets in a low-growth market: occupancy averaged 96% in 2024 and same-store NOI rose 4.2% year-over-year, driven by federal tenancy that accounts for ~42% of rent roll.

Stable government presence and affluent local incomes—median household income $122,000 in 2023—produce steady foot traffic and a 2024 average rent premium of $4.50/sqft vs. suburban peers.

Capital expenditure needs are low: 2024 capex was 2.1% of gross asset value, enabling free cash flow margins near 58% and sustained dividend coverage.

Long-Term Triple Net Lease Portfolios

Federal manages over 1,200 long-term triple net (NNN) lease properties leased to investment-grade tenants, generating roughly $185M annual rent with average lease terms of 15–20 years, creating stable, low-volatility cash flows.

NNN leases shift taxes, insurance, and maintenance to tenants, producing net margins above 75% and predictable Free Cash Flow that supports dividends and debt service.

These assets need minimal oversight—occupancy >98% and annual capex per property under $400—so Federal can redeploy capital and management toward higher-growth, higher-return initiatives.

Mature Suburban Power Centers

Mature suburban power centers in affluent suburbs—e.g., U.S. metros with median household income >100k—have saturated demand and face limited competition due to scarce land, keeping vacancy around 4% nationally (Q4 2024, CBRE).

These assets produce net operating income well above capex needs since development costs were amortized years ago; typical stabilized NOI margins ~60% and cap rates 5.5% (2024 market median), so they generate excess cash flow.

Surplus liquidity from these centers funds corporate debt service—average interest coverage ratios >4x for REITs focused on power centers—and bankrolls strategic investments and store-format R&D.

- Low vacancy (~4%), high NOI margin (~60%)

- Cap rates ~5.5% (2024 median)

- Interest coverage >4x for specialized REITs

- Stable tenant turnover, long leases

Legacy Urban Retail Strips

Federal’s Legacy Urban Retail Strips have stable, loyal customer bases and sit in mature markets where annual footfall growth is under 1% and same-store NOI (net operating income) growth averages 2.2% (2024), making them predictable cash cows.

These assets deliver strong returns with cap rates near 5.5% (2024 market comps) and require modest maintenance CAPEX ~0.8% of asset value annually, preserving FFO while funding targeted upgrades.

- Stable NOI growth 2.2% (2024)

- Cap rate ~5.5% (2024 comps)

- Maintenance CAPEX ~0.8% of asset value

- Footfall growth <1% in mature markets

Grocery-Anchored Power Centers: Stable 2024 Cash Flow—NOI +3.4%, 96% Occupancy

Grocery-anchored and NNN suburban power centers delivered stable cash: 2024 same-center NOI +3.4%, occupancy 96.2%, cap rates ~5.5%, capex 2.1% of GAV, free cash flow margin ~58%, and they supplied ~41% of 2024 distributable cash flow.

| Metric | 2024 Value |

|---|---|

| Same-center NOI growth | +3.4% |

| Occupancy | 96.2% |

| Cap rate (median) | 5.5% |

| Capex/GAV | 2.1% |

| FCF margin | ~58% |

| Share of DCF | ~41% |

Full Transparency, Always

Federal BCG Matrix

The file you're previewing on this page is the final Federal BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready report designed for clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

The Federal BCG Matrix snapshot highlights where key products sit across Stars, Cash Cows, Question Marks, and Dogs—revealing market share dynamics and growth potential to inform strategic moves. This preview outlines high-level placements and implications for capital allocation, but the full BCG Matrix provides quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide investment and product decisions. Purchase the complete report for a comprehensive, presentation-ready strategic tool.

Stars

Mixed-Use Premier Destinations

Mixed-Use Premier Destinations like Santana Row (San Jose) and Pike & Rose (North Bethesda) sit in Federal’s BCG Stars: they blend retail, office, and residential and deliver premium rents—average asking rents reached $89/SF for retail and $62/SF for office in 2024—and sustain >95% occupancy in affluent submarkets. Federal invested $220M in 2023–24 capital improvements to expand experiential offerings, keeping NOI growth near 8% year-over-year and defending market share.

Luxury Coastal Retail Clusters

Luxury coastal retail clusters in Southern California and the Northeast corridor act as Stars in the Federal BCG Matrix, driving growth with avg. annual NOI (net operating income) growth ~6–8% and rent CAGR ~4.5% since 2019; these markets account for ~28% of portfolio value and deliver top-quartile returns.

Integrated Residential Developments

Integrated residential developments—luxury units above or beside retail—are a high-growth segment for Federal, targeting a 12–15% CAGR in recurring revenue and leveraging a 2025 urban rental vacancy drop to 3.8% (CBRE, Q4 2024).

They diversify cash flow away from retail rent by adding longer-term rental income, with projected NOI margins of 30% once stabilized and yields modeled at 4.5% cap rates for prime assets in 2025.

Construction requires heavy cash: Federal estimates HKD 2.1–3.5 billion per project and negative FCF for 24–36 months, but market-share aims place these projects as leaders in the luxury rental niche.

Silicon Valley Commercial Assets

Silicon Valley Commercial Assets rank as Stars in Federal Realty’s BCG matrix, driven by $1,200+ median household incomes within a 3-mile radius and vacancy rates under 6% in 2024, signaling high growth and strong cash reinvestment potential.

Federal prioritizes redevelopment and amenity upgrades—added 120k sq ft of mixed-use space in 2023—targeting tech tenants and affluent consumers to sustain rent premiums and capture resilient demand.

- High-earning catchment: $1,200+ median monthly household income (2024)

- Low vacancy: <6% (2024)

- Recent redeploy: 120,000 sq ft added (2023)

- Focus: redevelopment, premium amenities, mixed-use

Sustainable Green-Certified Hubs

Federal’s LEED-certified hubs are market leaders as 78% of institutional tenants ranked ESG a top-3 lease factor in 2024, letting the trust command 7–12% rent premiums vs non-certified assets.

High upfront green capex (avg $30–60/sqft) is offset by rising demand: certified assets grew 22% market share in major CBDs from 2020–2024, boosting NOI and valuation multiples.

- 78% of tenants cite ESG top-3 (2024)

- 7–12% rent premium vs non-certified

- $30–60/sqft typical green capex

- 22% market-share growth (2020–2024)

Coastal & Mixed‑Use Drive Strong Cashflow: 6–8% NOI, 95% Occupancy, 4.5% Rent CAGR

Stars: mixed‑use and coastal luxury assets drive 6–8% NOI growth, 4.5% rent CAGR, ~95% occupancy; portfolio weight ~28%; LEED assets earn 7–12% rent premium; redevelopment capex HKD 2.1–3.5B/project, green capex $30–60/SF; Silicon Valley assets: <6% vacancy, $1,200+ median monthly household income (2024).

| Metric | Value |

|---|---|

| NOI growth | 6–8% |

| Rent CAGR | 4.5% |

| Occupancy | ~95% |

| Portfolio share | 28% |

What is included in the product

Comprehensive BCG Matrix review of the Federal's units with strategic guidance—invest, hold, or divest—plus trend-driven risks and advantages.

One-page federal BCG Matrix mapping agencies by mandate and budget to clarify strategy and resource allocation

Cash Cows

Grocery-Anchored Neighborhood Centers

Grocery-anchored neighborhood centers form the portfolio bedrock, delivering stable cash flow: average same-center NOI (net operating income) grew 3.4% in 2024 and occupancy stayed at 96.2% nationwide through Q4 2024.

These necessity-driven assets need little repositioning or heavy marketing, showing median lease renewals of 7.8 years and rent spread resilience during 2023–2024 disinflation.

Federal uses cash from these mature centers to fund new developments and pay steady dividends, with centers contributing roughly 41% of 2024 distributable cash flow to shareholders.

Established DC Metro Corridor Holdings

Established DC Metro Corridor Holdings are high-share assets in a low-growth market: occupancy averaged 96% in 2024 and same-store NOI rose 4.2% year-over-year, driven by federal tenancy that accounts for ~42% of rent roll.

Stable government presence and affluent local incomes—median household income $122,000 in 2023—produce steady foot traffic and a 2024 average rent premium of $4.50/sqft vs. suburban peers.

Capital expenditure needs are low: 2024 capex was 2.1% of gross asset value, enabling free cash flow margins near 58% and sustained dividend coverage.

Long-Term Triple Net Lease Portfolios

Federal manages over 1,200 long-term triple net (NNN) lease properties leased to investment-grade tenants, generating roughly $185M annual rent with average lease terms of 15–20 years, creating stable, low-volatility cash flows.

NNN leases shift taxes, insurance, and maintenance to tenants, producing net margins above 75% and predictable Free Cash Flow that supports dividends and debt service.

These assets need minimal oversight—occupancy >98% and annual capex per property under $400—so Federal can redeploy capital and management toward higher-growth, higher-return initiatives.

Mature Suburban Power Centers

Mature suburban power centers in affluent suburbs—e.g., U.S. metros with median household income >100k—have saturated demand and face limited competition due to scarce land, keeping vacancy around 4% nationally (Q4 2024, CBRE).

These assets produce net operating income well above capex needs since development costs were amortized years ago; typical stabilized NOI margins ~60% and cap rates 5.5% (2024 market median), so they generate excess cash flow.

Surplus liquidity from these centers funds corporate debt service—average interest coverage ratios >4x for REITs focused on power centers—and bankrolls strategic investments and store-format R&D.

- Low vacancy (~4%), high NOI margin (~60%)

- Cap rates ~5.5% (2024 median)

- Interest coverage >4x for specialized REITs

- Stable tenant turnover, long leases

Legacy Urban Retail Strips

Federal’s Legacy Urban Retail Strips have stable, loyal customer bases and sit in mature markets where annual footfall growth is under 1% and same-store NOI (net operating income) growth averages 2.2% (2024), making them predictable cash cows.

These assets deliver strong returns with cap rates near 5.5% (2024 market comps) and require modest maintenance CAPEX ~0.8% of asset value annually, preserving FFO while funding targeted upgrades.

- Stable NOI growth 2.2% (2024)

- Cap rate ~5.5% (2024 comps)

- Maintenance CAPEX ~0.8% of asset value

- Footfall growth <1% in mature markets

Grocery-Anchored Power Centers: Stable 2024 Cash Flow—NOI +3.4%, 96% Occupancy

Grocery-anchored and NNN suburban power centers delivered stable cash: 2024 same-center NOI +3.4%, occupancy 96.2%, cap rates ~5.5%, capex 2.1% of GAV, free cash flow margin ~58%, and they supplied ~41% of 2024 distributable cash flow.

| Metric | 2024 Value |

|---|---|

| Same-center NOI growth | +3.4% |

| Occupancy | 96.2% |

| Cap rate (median) | 5.5% |

| Capex/GAV | 2.1% |

| FCF margin | ~58% |

| Share of DCF | ~41% |

Full Transparency, Always

Federal BCG Matrix

The file you're previewing on this page is the final Federal BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, strategy-ready report designed for clarity and immediate use.