Federal Porter's Five Forces Analysis

Don't Miss the Bigger Picture

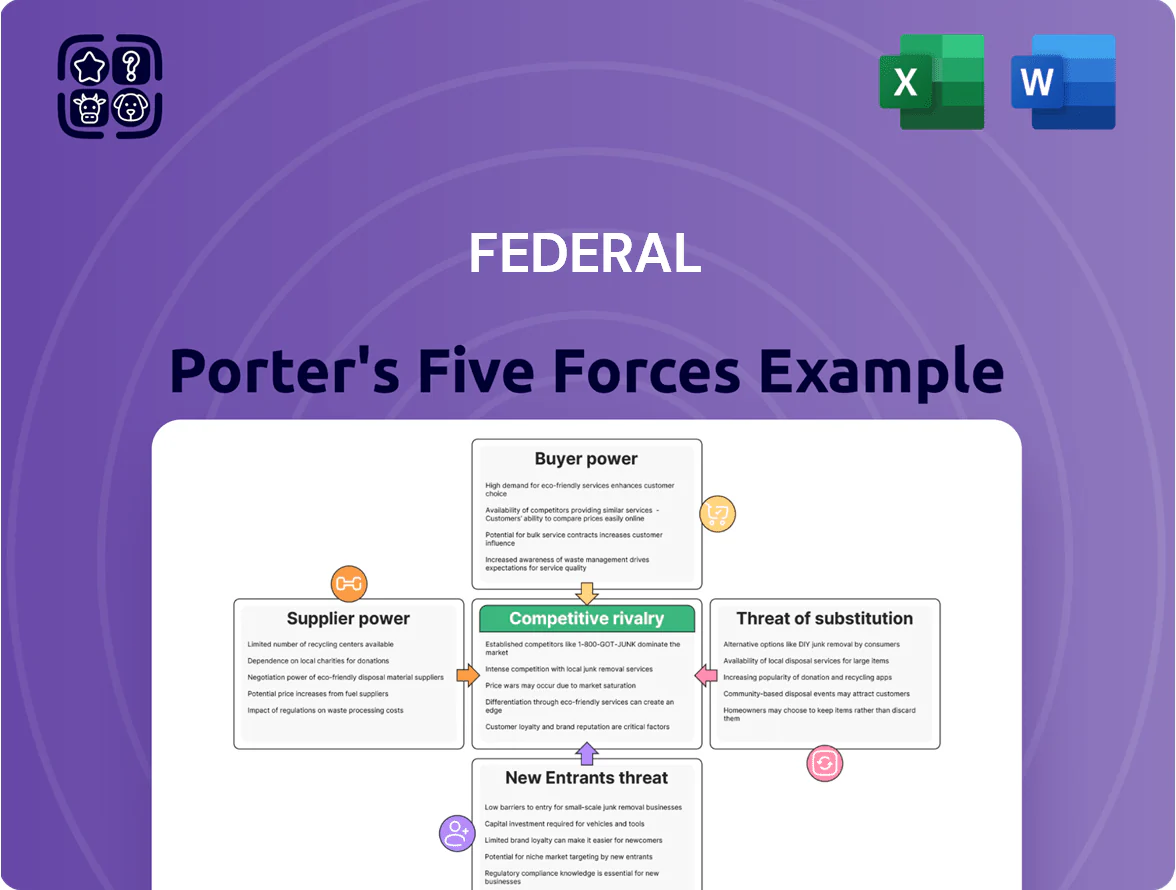

Federal’s Five Forces snapshot highlights bargaining power of buyers and suppliers, rivalry intensity, threat of new entrants, and substitute pressures shaping profitability and strategic choices.

This brief glimpse only scratches the surface—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable implications tailored to Federal for confident decision-making.

Suppliers Bargaining Power

Availability of Debt and Equity Capital

Financial institutions and bondholders supply the capital Federal Realty Trust (NYSE: FRT) needs for acquisitions and redevelopments; by Q4 2025 FRT carried about $2.8B debt and access to revolvers totaling $700M, so lenders directly shape liquidity. As interest rates stabilized in 2025 near 4.5%–5.0% for investment-grade borrowers, supplier bargaining power is moderate to high because higher cost of capital compresses FRT’s NOI spread and ROE.

Construction Labor and Material Providers

Municipalities and Regulatory Bodies

Local governments supply entitlements, zoning approvals, and building permits that can stop or delay redevelopment; in 2024 US local permitting backlogs delayed 28% of large retail projects, raising holding costs by ~1.2% of project value.

These bodies hold high bargaining power because a single denial can pause a plan; Federal Realty targets high-barrier markets like Boston and DC where it has 40+ years of collaborative approvals, reducing permit risk and shortening approval timelines by ~6 months on average.

Utility and Energy Service Providers

Utility and energy service providers supply essential power, water, and waste services to Federal Realty’s retail and residential assets; regulated monopoly pricing limits short-term supplier leverage but rising 2025–26 green mandates increase supplier influence on compliance costs.

Federal Realty’s on-site renewables — including >10 MW of solar capacity commissioned by 2025 and a 20% reduction in grid electricity use at core assets — cut dependence on external utilities and stabilize long-term OPEX.

- Regulated utilities limit immediate price swings

- 2025–26 green mandates raise compliance costs

- Federal Realty >10 MW solar by 2025, ~20% grid use cut

- On-site energy lowers supplier bargaining power long-term

Land and Property Sellers

- Finite supply → seller premiums

- Top MSA vacancy <2% (2024)

- Cap rates 50–100 bps lower

- 20% off-market deals (2024)

- ~10% below comps on acquisitions

Suppliers Hold Moderate–High Leverage Despite Renewables, Off‑Market Deals

Suppliers (lenders, contractors, utilities, landowners) exert moderate–high power: FRT had $2.8B debt + $700M revolvers (Q4 2025), steel +12% y/y (2024), coastal vacancy <2% (2024), and >10 MW solar by 2025 cutting grid use ~20%, so long-term contracts, off‑market deals (20% of 2024 acquisitions) and renewables reduce but do not eliminate supplier leverage.

| Supplier | Key 2024–25 data | Impact |

|---|---|---|

| Lenders | $2.8B debt; $700M revolvers (Q4 2025) | High liquidity influence |

| Contractors/materials | Steel +12% y/y (2024) | Timing/cost pressure |

| Landowners | Top MSA vacancy <2% (2024) | Premium pricing |

| Utilities | >10 MW solar; ~20% grid cut (2025) | Lower long-term OPEX |

What is included in the product

Concise Porter’s Five Forces assessment of Federal that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary to inform pricing, positioning, and defensive moves.

Concise five-forces summary that highlights strategic pressure points instantly—ideal for board decks and rapid decision-making.

Customers Bargaining Power

Large National Anchor Tenants

Major retailers such as Kroger, Walmart, and Target act as anchor tenants that drive roughly 40–60% of foot traffic at Federal Realty’s mixed-use centers, giving them outsized bargaining power because smaller inline rents and occupancy hinge on their draw.

By late 2025 anchors commonly secure rent abatements, percentage rent floors, or tenant improvement allowances equal to 6–12 months of free rent or $50–150 per sq ft build-outs in exchange for 10–20 year commitments.

Their leverage pushes Federal Realty to accept stricter co-tenancy clauses and exclusivity rights, which can reduce average lease spreads and compress initial yield-on-cost by 50–150 basis points on redevelopment projects.

Small and Local Boutique Retailers

Small and local boutique retailers supply the unique character and drive higher rent per square foot—Federal Realty reported average rent of $72.10/sq ft at its shopping centers in 2024—boosting mixed-use profitability despite low individual bargaining power versus anchors.

Collectively these tenants define destination vibrancy; Federal balances their limited leverage by offering premium management, marketing, and a 2024 average household income catchment of ~$210,000 that smaller landlords rarely deliver.

Residential and Office Renters

As Federal Realty expands mixed-use assets, residents and office tenants form a key segment with moderate bargaining power because luxury apartment vacancy in top US markets averaged 6.2% in 2024 and flexible office inventory grew 8% year-over-year; tenants can switch to competitors. To keep rents 5–10% above market in 2025, Federal must deliver premium amenities, curated services, and seamless retail integration that justify higher prices and lower churn.

Tenant Diversification and Lease Expirations

Federal Realty staggers lease expirations so no single year concentrates risk; in 2024 about 12% of NOI was scheduled to expire, down from 18% in 2021, lowering tenant collective leverage.

This mix across retail, residential, and office keeps cash flow steady—retail comprised 48% of 2024 rental revenue, residential 30%, office 22%—so a sector downturn cannot easily force concessions.

- 2024 expirations ~12% of NOI

- 2021 expirations ~18% of NOI

- Revenue mix: retail 48%, residential 30%, office 22%

Consumer Spending and Demographics

The affluent consumers in Federal Realty's trade areas—median household incomes often above $120,000 and trade-area daytime populations >100,000—drive demand for premium retailers able to pay top rents, so tenant sales per square foot (often $600–$1,200/sq ft) sustain high rent rolls and low vacancy.

By concentrating in dense, high-income metros (e.g., submarkets with 30–50% higher retail spend), Federal preserves tenant profitability and its leasing leverage, protecting NOI and rent growth.

- Median household income >$120,000

- Tenant sales $600–$1,200/sq ft

- Daytime population >100,000

- Higher retail spend 30–50% vs national

Anchor Retail Power Squeezes Yields While Affluent Catchments Sustain Premium Rents

Customers wield mixed bargaining power: anchor retailers (Kroger, Walmart, Target) drive 40–60% foot traffic and secure 6–12 months abatements or $50–150/sq ft TI for 10–20 year deals, squeezing yields by 50–150 bps; boutiques pay premium (avg rent $72.10/sq ft in 2024) and affluent catchments (median income >$120k, daytime pop >100k) sustain rents and limit collective tenant leverage.

| Metric | Value (2024–25) |

|---|---|

| Anchor traffic | 40–60% |

| Typical abatements/TI | 6–12 mo / $50–150/sq ft |

| Rent (avg) | $72.10/sq ft |

| Median income | >$120,000 |

Preview Before You Purchase

Federal Porter's Five Forces Analysis

This preview shows the exact Federal Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders, no edits needed; the full, professionally formatted document is ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Federal’s Five Forces snapshot highlights bargaining power of buyers and suppliers, rivalry intensity, threat of new entrants, and substitute pressures shaping profitability and strategic choices.

This brief glimpse only scratches the surface—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable implications tailored to Federal for confident decision-making.

Suppliers Bargaining Power

Availability of Debt and Equity Capital

Financial institutions and bondholders supply the capital Federal Realty Trust (NYSE: FRT) needs for acquisitions and redevelopments; by Q4 2025 FRT carried about $2.8B debt and access to revolvers totaling $700M, so lenders directly shape liquidity. As interest rates stabilized in 2025 near 4.5%–5.0% for investment-grade borrowers, supplier bargaining power is moderate to high because higher cost of capital compresses FRT’s NOI spread and ROE.

Construction Labor and Material Providers

Municipalities and Regulatory Bodies

Local governments supply entitlements, zoning approvals, and building permits that can stop or delay redevelopment; in 2024 US local permitting backlogs delayed 28% of large retail projects, raising holding costs by ~1.2% of project value.

These bodies hold high bargaining power because a single denial can pause a plan; Federal Realty targets high-barrier markets like Boston and DC where it has 40+ years of collaborative approvals, reducing permit risk and shortening approval timelines by ~6 months on average.

Utility and Energy Service Providers

Utility and energy service providers supply essential power, water, and waste services to Federal Realty’s retail and residential assets; regulated monopoly pricing limits short-term supplier leverage but rising 2025–26 green mandates increase supplier influence on compliance costs.

Federal Realty’s on-site renewables — including >10 MW of solar capacity commissioned by 2025 and a 20% reduction in grid electricity use at core assets — cut dependence on external utilities and stabilize long-term OPEX.

- Regulated utilities limit immediate price swings

- 2025–26 green mandates raise compliance costs

- Federal Realty >10 MW solar by 2025, ~20% grid use cut

- On-site energy lowers supplier bargaining power long-term

Land and Property Sellers

- Finite supply → seller premiums

- Top MSA vacancy <2% (2024)

- Cap rates 50–100 bps lower

- 20% off-market deals (2024)

- ~10% below comps on acquisitions

Suppliers Hold Moderate–High Leverage Despite Renewables, Off‑Market Deals

Suppliers (lenders, contractors, utilities, landowners) exert moderate–high power: FRT had $2.8B debt + $700M revolvers (Q4 2025), steel +12% y/y (2024), coastal vacancy <2% (2024), and >10 MW solar by 2025 cutting grid use ~20%, so long-term contracts, off‑market deals (20% of 2024 acquisitions) and renewables reduce but do not eliminate supplier leverage.

| Supplier | Key 2024–25 data | Impact |

|---|---|---|

| Lenders | $2.8B debt; $700M revolvers (Q4 2025) | High liquidity influence |

| Contractors/materials | Steel +12% y/y (2024) | Timing/cost pressure |

| Landowners | Top MSA vacancy <2% (2024) | Premium pricing |

| Utilities | >10 MW solar; ~20% grid cut (2025) | Lower long-term OPEX |

What is included in the product

Concise Porter’s Five Forces assessment of Federal that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats, with strategic commentary to inform pricing, positioning, and defensive moves.

Concise five-forces summary that highlights strategic pressure points instantly—ideal for board decks and rapid decision-making.

Customers Bargaining Power

Large National Anchor Tenants

Major retailers such as Kroger, Walmart, and Target act as anchor tenants that drive roughly 40–60% of foot traffic at Federal Realty’s mixed-use centers, giving them outsized bargaining power because smaller inline rents and occupancy hinge on their draw.

By late 2025 anchors commonly secure rent abatements, percentage rent floors, or tenant improvement allowances equal to 6–12 months of free rent or $50–150 per sq ft build-outs in exchange for 10–20 year commitments.

Their leverage pushes Federal Realty to accept stricter co-tenancy clauses and exclusivity rights, which can reduce average lease spreads and compress initial yield-on-cost by 50–150 basis points on redevelopment projects.

Small and Local Boutique Retailers

Small and local boutique retailers supply the unique character and drive higher rent per square foot—Federal Realty reported average rent of $72.10/sq ft at its shopping centers in 2024—boosting mixed-use profitability despite low individual bargaining power versus anchors.

Collectively these tenants define destination vibrancy; Federal balances their limited leverage by offering premium management, marketing, and a 2024 average household income catchment of ~$210,000 that smaller landlords rarely deliver.

Residential and Office Renters

As Federal Realty expands mixed-use assets, residents and office tenants form a key segment with moderate bargaining power because luxury apartment vacancy in top US markets averaged 6.2% in 2024 and flexible office inventory grew 8% year-over-year; tenants can switch to competitors. To keep rents 5–10% above market in 2025, Federal must deliver premium amenities, curated services, and seamless retail integration that justify higher prices and lower churn.

Tenant Diversification and Lease Expirations

Federal Realty staggers lease expirations so no single year concentrates risk; in 2024 about 12% of NOI was scheduled to expire, down from 18% in 2021, lowering tenant collective leverage.

This mix across retail, residential, and office keeps cash flow steady—retail comprised 48% of 2024 rental revenue, residential 30%, office 22%—so a sector downturn cannot easily force concessions.

- 2024 expirations ~12% of NOI

- 2021 expirations ~18% of NOI

- Revenue mix: retail 48%, residential 30%, office 22%

Consumer Spending and Demographics

The affluent consumers in Federal Realty's trade areas—median household incomes often above $120,000 and trade-area daytime populations >100,000—drive demand for premium retailers able to pay top rents, so tenant sales per square foot (often $600–$1,200/sq ft) sustain high rent rolls and low vacancy.

By concentrating in dense, high-income metros (e.g., submarkets with 30–50% higher retail spend), Federal preserves tenant profitability and its leasing leverage, protecting NOI and rent growth.

- Median household income >$120,000

- Tenant sales $600–$1,200/sq ft

- Daytime population >100,000

- Higher retail spend 30–50% vs national

Anchor Retail Power Squeezes Yields While Affluent Catchments Sustain Premium Rents

Customers wield mixed bargaining power: anchor retailers (Kroger, Walmart, Target) drive 40–60% foot traffic and secure 6–12 months abatements or $50–150/sq ft TI for 10–20 year deals, squeezing yields by 50–150 bps; boutiques pay premium (avg rent $72.10/sq ft in 2024) and affluent catchments (median income >$120k, daytime pop >100k) sustain rents and limit collective tenant leverage.

| Metric | Value (2024–25) |

|---|---|

| Anchor traffic | 40–60% |

| Typical abatements/TI | 6–12 mo / $50–150/sq ft |

| Rent (avg) | $72.10/sq ft |

| Median income | >$120,000 |

Preview Before You Purchase

Federal Porter's Five Forces Analysis

This preview shows the exact Federal Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders, no edits needed; the full, professionally formatted document is ready for instant download and use.