Federated Hermes SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Federated Hermes faces a complex mix of strengths—diversified asset management capabilities and ESG leadership—counterbalanced by fee pressure and market sensitivity; our full SWOT unpacks these dynamics with financial context and strategic implications. Purchase the complete SWOT analysis to receive a professionally written, editable report and Excel matrix that equips investors, analysts, and strategists to plan and act with confidence.

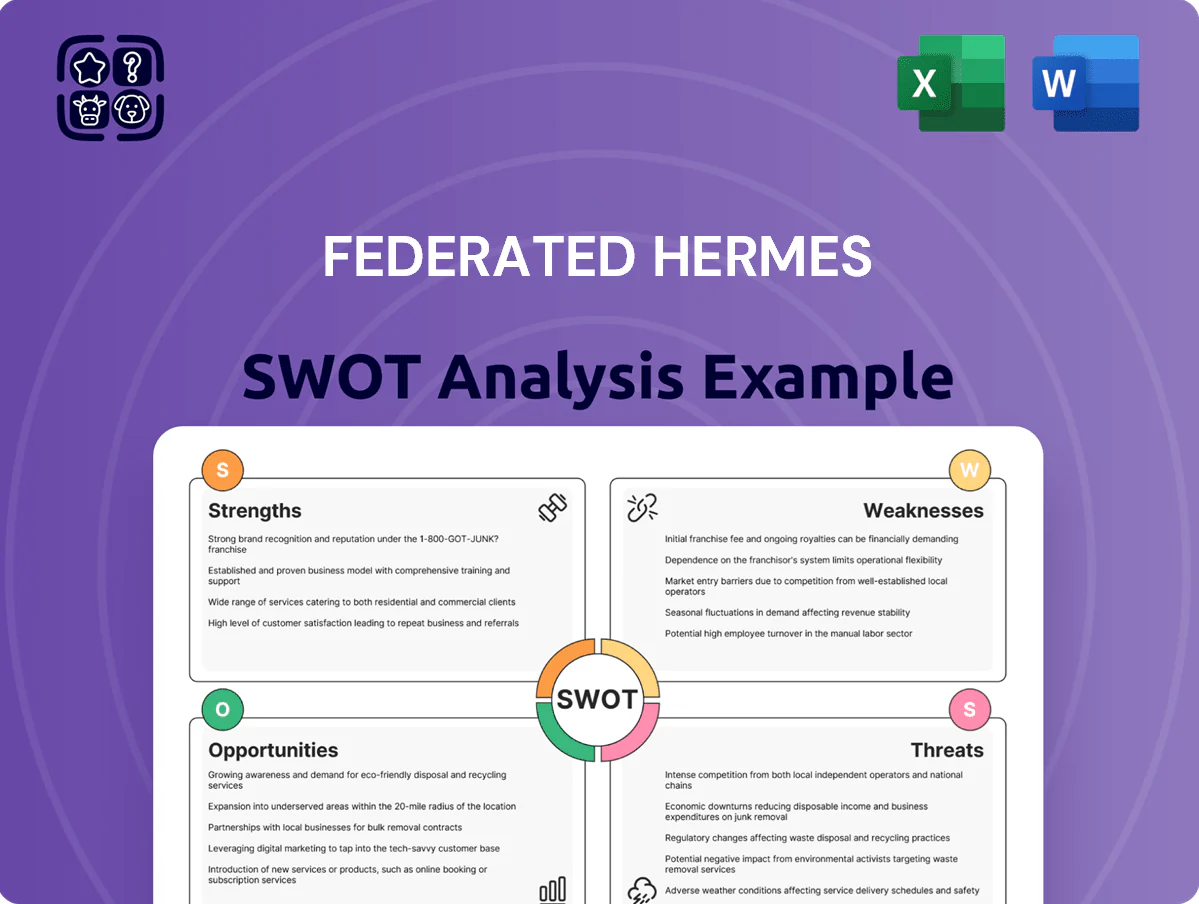

Strengths

Leadership in Liquidity Management

Federated Hermes held about $220 billion in money market and liquidity AUM by December 2025, sustaining market-leading scale that underpins stable fee income and redemption capacity.

That scale lets the firm offer competitive yields—its institutional prime funds returned ~2.1% in 2025—and keeps deep ties with ~600 institutional treasury clients and corporates.

During 2022–2025 stress periods, Federated Hermes remained a top liquidity provider, handling peak daily flows above $12 billion without disrupting NAV stability.

Pioneering ESG and Stewardship Integration

The Hermes Investment Management merger (completed 2020) strengthened Federated Hermes as a global ESG engagement leader, with EOS Stewardship advising on stewardship for £1.5tn+ of assets under influence as of 2025, boosting long-term client retention.

EOS provides active engagement and voting services valued by pension funds and insurers, driving fee-premium mandates and differentiating the firm from peers that mainly offer passive ESG screening.

Diversified Product Suite Across Asset Classes

Federated Hermes offers equity, fixed income, and alternatives—including $604bn AUM as of 2025—spreading risk so underperformance in one asset class has limited portfolio impact.

Mixing traditional mutual funds with private markets (private credit and real assets made up ~18% of AUM in 2024) helps capture more of the investor wallet and steadies fee revenue.

Robust Distribution Network

Federated Hermes operates a global distribution network covering financial intermediaries, banks, and broker-dealers, supporting $610 billion in assets under management as of Dec 31, 2025 and enabling fast capital raises and product launches across retail and institutional channels.

These long-standing professional ties deliver recurring access to diversified capital pools and helped the firm place $8.2 billion in net flows in 2025, showing distribution effectiveness.

- Global reach: intermediaries, banks, broker-dealers

- AUM: $610 billion (Dec 31, 2025)

- 2025 net flows: $8.2 billion

- Fast product launch capability via existing channels

Integrated Fund Administration Services

- Fee diversification: ~22% of revenue from service-based fees (2024)

- AUM: $612 billion at end-2024, down 8% year-over-year

- Benefit: more predictable cash flow, higher retention

Federated Hermes: $610B AUM, $220B money-market, $8.2B net flows (2025)

Federated Hermes: $610bn AUM (Dec 31, 2025); $220bn money-market AUM (2025); $604bn cross-asset AUM (2025); $8.2bn net flows (2025); EOS stewardship influence £1.5tn+ (2025); fee services ~22% revenue (2024); handled >$12bn peak daily liquidity flows (2022–25).

| Metric | Value |

|---|---|

| AUM (Dec 31, 2025) | $610bn |

| Money-market AUM (2025) | $220bn |

| Net flows (2025) | $8.2bn |

What is included in the product

Delivers a concise SWOT overview of Federated Hermes, outlining its core strengths and weaknesses while identifying key market opportunities and external threats shaping its competitive position.

Delivers a concise Federation Hermes SWOT snapshot for rapid strategic alignment, ideal for executives and teams needing a clear, editable view to streamline decision-making and stakeholder presentations.

Weaknesses

Heavy Reliance on Money Market Assets

About 45% of Federated Hermes’s $660 billion AUM (2025 Q1) sits in liquidity/money-market products, making revenue highly rate-sensitive; when Fed cuts push short rates toward zero the firm has historically implemented fee waivers to keep net yields positive, reducing management fee income. This concentration raises earnings volatility versus peers with larger equity franchises and compresses margins during prolonged low-rate periods.

Brand Complexity Post-Merger

Federated Hermes’s dual identity breeds market confusion: a 2024 client survey found 22% of institutional clients globally uncertain whether the firm’s strength lies in active US equity or European stewardship strategies. Managing legacy US-based Federated and UK-based Hermes cultures adds cost and attention—integration expenses reached $48m in 2023—and can slow unified marketing or fast strategic pivots in growth markets.

Higher Expense Ratios Relative to Passive Rivals

As an active manager, Federated Hermes faces pressure from the shift to low-cost passive indexing and ETFs; by end-2024 U.S. passive AUM hit $17.2 trillion vs. $18.1 trillion active, highlighting market momentum. Many flagship funds charge management fees around 0.60–0.85% vs. 0.03–0.15% for large-cap ETFs, creating a clear cost gap. That disparity makes attracting price-sensitive retail investors harder in today’s transparent fee environment.

Performance Variability in Active Equities

Federated Hermes' reliance on active equity management ties outcomes to manager skill; from 2023–2025 several flagship U.S. equity funds trailed benchmarks by 2–4% annualized, hurting net flows—AUM fell 6% in 2024 for underperforming equity strategies.

Periods of multi-quarter underperformance trigger outsized redemptions and reputational risk; keeping across-house desks top quartile in efficient markets is an ongoing operational strain.

- Active-only exposure: higher flow volatility

- 2024: AUM -6% in weak equity products

- Underperformance: 2–4% annualized vs benchmarks (2023–25)

- Operational burden to sustain top-quartile returns

Geographic Concentration in the United States

Despite growing international operations, Federated Hermes still derives roughly 78% of revenue and about 72% of assets under management from the United States as of year-end 2024, leaving it heavily tied to US monetary policy, fiscal shifts, and SEC rule changes.

That concentration raises earnings and AUM volatility risk during US recessions or regulatory shocks; a 5% US market drawdown could disproportionately cut fees and flows versus more balanced peers.

Further geographic diversification—targeting Asia and Europe to raise non-US AUM above 35% within 3–5 years—would better insulate revenue and reduce single-market exposure.

- ~78% revenue from US (2024)

- ~72% AUM in US (2024)

- High sensitivity to US policy and cycles

- Goal: non-US AUM >35% in 3–5 years

Liquidity-heavy $660B AUM, US-centric revenue, integration costs and flagships lagging

About 45% of $660bn AUM (2025 Q1) in cash/liquidity makes revenue highly rate-sensitive; fee waivers in low-rate periods cut mgmt fees and margins. Dual Federated (US) and Hermes (UK) brands cause client confusion and added integration costs ($48m in 2023). Active-only bias and 2023–25 flagship underperformance (2–4% annualized) drove AUM -6% in 2024, and ~72% AUM /78% revenue remained US-concentrated (2024).

| Metric | Value |

|---|---|

| Total AUM (Q1 2025) | $660bn |

| Liquidity AUM | 45% |

| Integration costs (2023) | $48m |

| AUM change (2024) | -6% |

| Flagship vs benchmark (2023–25) | -2–4% ann. |

| US share of AUM (2024) | 72% |

| US share of revenue (2024) | 78% |

Same Document Delivered

Federated Hermes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Federated Hermes faces a complex mix of strengths—diversified asset management capabilities and ESG leadership—counterbalanced by fee pressure and market sensitivity; our full SWOT unpacks these dynamics with financial context and strategic implications. Purchase the complete SWOT analysis to receive a professionally written, editable report and Excel matrix that equips investors, analysts, and strategists to plan and act with confidence.

Strengths

Leadership in Liquidity Management

Federated Hermes held about $220 billion in money market and liquidity AUM by December 2025, sustaining market-leading scale that underpins stable fee income and redemption capacity.

That scale lets the firm offer competitive yields—its institutional prime funds returned ~2.1% in 2025—and keeps deep ties with ~600 institutional treasury clients and corporates.

During 2022–2025 stress periods, Federated Hermes remained a top liquidity provider, handling peak daily flows above $12 billion without disrupting NAV stability.

Pioneering ESG and Stewardship Integration

The Hermes Investment Management merger (completed 2020) strengthened Federated Hermes as a global ESG engagement leader, with EOS Stewardship advising on stewardship for £1.5tn+ of assets under influence as of 2025, boosting long-term client retention.

EOS provides active engagement and voting services valued by pension funds and insurers, driving fee-premium mandates and differentiating the firm from peers that mainly offer passive ESG screening.

Diversified Product Suite Across Asset Classes

Federated Hermes offers equity, fixed income, and alternatives—including $604bn AUM as of 2025—spreading risk so underperformance in one asset class has limited portfolio impact.

Mixing traditional mutual funds with private markets (private credit and real assets made up ~18% of AUM in 2024) helps capture more of the investor wallet and steadies fee revenue.

Robust Distribution Network

Federated Hermes operates a global distribution network covering financial intermediaries, banks, and broker-dealers, supporting $610 billion in assets under management as of Dec 31, 2025 and enabling fast capital raises and product launches across retail and institutional channels.

These long-standing professional ties deliver recurring access to diversified capital pools and helped the firm place $8.2 billion in net flows in 2025, showing distribution effectiveness.

- Global reach: intermediaries, banks, broker-dealers

- AUM: $610 billion (Dec 31, 2025)

- 2025 net flows: $8.2 billion

- Fast product launch capability via existing channels

Integrated Fund Administration Services

- Fee diversification: ~22% of revenue from service-based fees (2024)

- AUM: $612 billion at end-2024, down 8% year-over-year

- Benefit: more predictable cash flow, higher retention

Federated Hermes: $610B AUM, $220B money-market, $8.2B net flows (2025)

Federated Hermes: $610bn AUM (Dec 31, 2025); $220bn money-market AUM (2025); $604bn cross-asset AUM (2025); $8.2bn net flows (2025); EOS stewardship influence £1.5tn+ (2025); fee services ~22% revenue (2024); handled >$12bn peak daily liquidity flows (2022–25).

| Metric | Value |

|---|---|

| AUM (Dec 31, 2025) | $610bn |

| Money-market AUM (2025) | $220bn |

| Net flows (2025) | $8.2bn |

What is included in the product

Delivers a concise SWOT overview of Federated Hermes, outlining its core strengths and weaknesses while identifying key market opportunities and external threats shaping its competitive position.

Delivers a concise Federation Hermes SWOT snapshot for rapid strategic alignment, ideal for executives and teams needing a clear, editable view to streamline decision-making and stakeholder presentations.

Weaknesses

Heavy Reliance on Money Market Assets

About 45% of Federated Hermes’s $660 billion AUM (2025 Q1) sits in liquidity/money-market products, making revenue highly rate-sensitive; when Fed cuts push short rates toward zero the firm has historically implemented fee waivers to keep net yields positive, reducing management fee income. This concentration raises earnings volatility versus peers with larger equity franchises and compresses margins during prolonged low-rate periods.

Brand Complexity Post-Merger

Federated Hermes’s dual identity breeds market confusion: a 2024 client survey found 22% of institutional clients globally uncertain whether the firm’s strength lies in active US equity or European stewardship strategies. Managing legacy US-based Federated and UK-based Hermes cultures adds cost and attention—integration expenses reached $48m in 2023—and can slow unified marketing or fast strategic pivots in growth markets.

Higher Expense Ratios Relative to Passive Rivals

As an active manager, Federated Hermes faces pressure from the shift to low-cost passive indexing and ETFs; by end-2024 U.S. passive AUM hit $17.2 trillion vs. $18.1 trillion active, highlighting market momentum. Many flagship funds charge management fees around 0.60–0.85% vs. 0.03–0.15% for large-cap ETFs, creating a clear cost gap. That disparity makes attracting price-sensitive retail investors harder in today’s transparent fee environment.

Performance Variability in Active Equities

Federated Hermes' reliance on active equity management ties outcomes to manager skill; from 2023–2025 several flagship U.S. equity funds trailed benchmarks by 2–4% annualized, hurting net flows—AUM fell 6% in 2024 for underperforming equity strategies.

Periods of multi-quarter underperformance trigger outsized redemptions and reputational risk; keeping across-house desks top quartile in efficient markets is an ongoing operational strain.

- Active-only exposure: higher flow volatility

- 2024: AUM -6% in weak equity products

- Underperformance: 2–4% annualized vs benchmarks (2023–25)

- Operational burden to sustain top-quartile returns

Geographic Concentration in the United States

Despite growing international operations, Federated Hermes still derives roughly 78% of revenue and about 72% of assets under management from the United States as of year-end 2024, leaving it heavily tied to US monetary policy, fiscal shifts, and SEC rule changes.

That concentration raises earnings and AUM volatility risk during US recessions or regulatory shocks; a 5% US market drawdown could disproportionately cut fees and flows versus more balanced peers.

Further geographic diversification—targeting Asia and Europe to raise non-US AUM above 35% within 3–5 years—would better insulate revenue and reduce single-market exposure.

- ~78% revenue from US (2024)

- ~72% AUM in US (2024)

- High sensitivity to US policy and cycles

- Goal: non-US AUM >35% in 3–5 years

Liquidity-heavy $660B AUM, US-centric revenue, integration costs and flagships lagging

About 45% of $660bn AUM (2025 Q1) in cash/liquidity makes revenue highly rate-sensitive; fee waivers in low-rate periods cut mgmt fees and margins. Dual Federated (US) and Hermes (UK) brands cause client confusion and added integration costs ($48m in 2023). Active-only bias and 2023–25 flagship underperformance (2–4% annualized) drove AUM -6% in 2024, and ~72% AUM /78% revenue remained US-concentrated (2024).

| Metric | Value |

|---|---|

| Total AUM (Q1 2025) | $660bn |

| Liquidity AUM | 45% |

| Integration costs (2023) | $48m |

| AUM change (2024) | -6% |

| Flagship vs benchmark (2023–25) | -2–4% ann. |

| US share of AUM (2024) | 72% |

| US share of revenue (2024) | 78% |

Same Document Delivered

Federated Hermes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.