FedEx Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

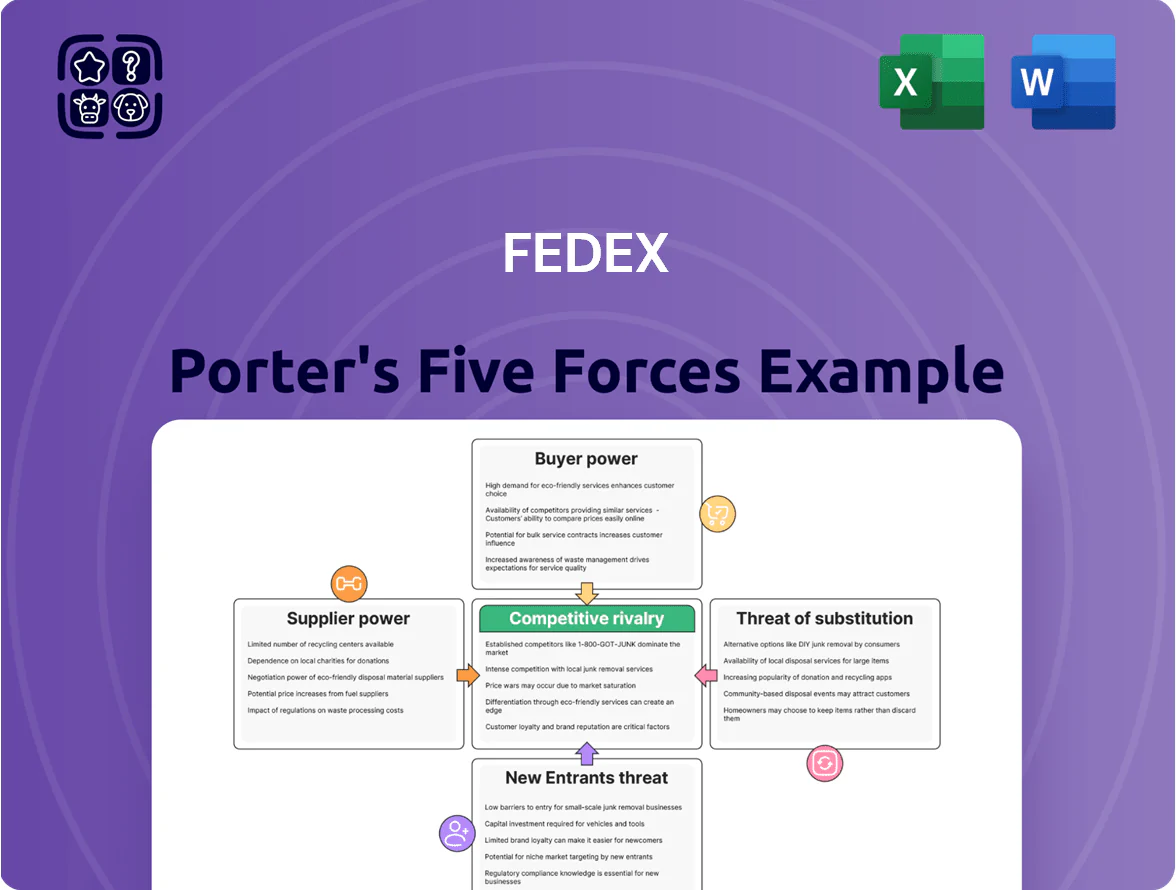

FedEx faces intense rivalry from global carriers, significant buyer power from large shippers, moderate supplier leverage in fuel and aircraft, low threat of new entrants due to high capital barriers, and rising substitution risks from digitization and regional couriers; this snapshot highlights strategic pressures shaping margins and growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FedEx’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility

FedEx relies heavily on fuel for ~80% of its air fleet and ~60% of ground energy use, so oil price swings directly raise operating costs; Brent averaged $86/bbl in 2025 YTD, up 14% vs 2024. Fuel surcharges blunt impact—fuel and related services were 16% of 2024 operating expenses—but suppliers still wield indirect pricing power over base margins. The 2025 shift to sustainable aviation fuel (SAF) concentrates supply: global SAF production met <0.1% of jet demand in 2024, creating a small pool of specialized, costlier suppliers.

Aircraft Manufacturing Duopoly

Labor and Specialized Talent

Technological Infrastructure Providers

FedEx depends heavily on major cloud providers and enterprise-software firms for real-time tracking and logistics AI; in 2024 FedEx reported cloud-related IT spend rising ~18% year-over-year to support these systems.

Those suppliers are critical to automated sorting and route optimization, and as FedEx folds deep-learning into its DRIVE initiative, platform lock-in and integration costs push switching costs higher.

- Cloud/AI spend up ~18% in 2024

- Drive deep-learning increases integration depth

- Automated sorting/route optimization depend on vendor tech

- Switching costs and vendor lock-in rising

Airport and Hub Infrastructure

Airport authorities and port operators control slots and land critical for FedEx’s global sorting; limited prime space at hubs like Memphis (MEM), Indianapolis (IND), and Paris CDG gives suppliers leverage in lease and expansion talks.

In 2024 FedEx reported capital leases and right-of-use assets of $7.9 billion, reflecting high real-estate exposure; losing hub access would directly harm time-definite promise and route density economics.

- Control of slots and land = high supplier leverage

- Prime hub scarcity raises renewal costs

- $7.9B capital lease exposure (2024)

- Hub loss → missed delivery guarantees, higher costs

Rising fuel, SAF scarcity and labor squeeze tighten carrier costs and hub leverage

Suppliers exert moderate-to-high power: fuel volatility (Brent $86/bbl 2025 YTD, +14% vs 2024) and SAF scarcity (<0.1% jet demand 2024) raise costs; Boeing/Airbus supply >95% of freighters, limiting switching; labor shortages pushed FedEx 2024 labor expense to $28.4B (+6%); cloud/IT spend rose ~18% in 2024; $7.9B capital lease exposure tightens hub leverage.

| Item | Metric (year) |

|---|---|

| Brent | $86/bbl (2025 YTD) |

| SAF supply | <0.1% jet demand (2024) |

| Labor expense | $28.4B (2024) |

| Cloud/IT spend | +18% YoY (2024) |

| Capital leases | $7.9B (2024) |

What is included in the product

Tailored exclusively for FedEx, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, barriers deterring new entrants, substitutes and emerging disruptors shaping FedEx’s pricing, profitability and strategic positioning.

Concise Porter's Five Forces snapshot for FedEx—quickly pinpoint competitive pressures and strategic levers to relieve operational and margin pain points.

Customers Bargaining Power

Low Switching Costs for Retail Users

Individual consumers and small businesses face low switching costs and can jump between FedEx, UPS, and USPS after seeing rates; in 2024 parcel price comparison sites showed up to 22% cost variance on small parcels, pushing FedEx to match discounts and keep on-time delivery over 94% to avoid churn.

Volume Leverage of E-commerce Giants

Price Sensitivity in Post-Inflationary Markets

In 2025’s post-inflationary market, 62% of US consumers say they choose cheaper shipping for non-essential goods, pushing average revenue per FedEx package down as economy parcels undercut premium overnight rates by ~30% in ticket price.

FedEx must tweak service tiers and yield-management—economy pricing grew 14% YoY in 2024—so it grabs price-sensitive volume without eroding express margins, which still deliver ~40% of operating income.

Demand for Deep Technical Integration

Large corporate clients demand deep technical integration and real-time visibility; in 2024, 62% of enterprise shippers ranked API connectivity as a top-three carrier requirement, forcing FedEx to treat tech as a customer mandate.

Without seamless APIs and end-to-end tracking, clients can shift volume to tech-forward rivals; FedEx reported a 3.5% revenue impact in select verticals when integrations lagged in 2023.

This dynamic converts IT from cost center to strategic retention tool: high-touch contracts now include SLAs for data transparency and integration timelines under 14 days to avoid churn.

- 62% of enterprise shippers prioritize API connectivity

- 3.5% revenue hit in impacted verticals (2023)

- SLA demand: real-time visibility, integration <14 days

Rise of Regional Delivery Alternatives

The rise of regional delivery startups and gig platforms (eg, GoShare, Roadie, local couriers) expanded urban choices, cutting last-mile share for national carriers; in 2024 US same-day/local delivery grew ~18% YoY and accounted for ~12% of parcel volume, eroding unit economics for FedEx on short trips.

Customers now unbundle services—using FedEx for long-haul and local players for rapid city delivery—reducing switching costs and increasing price sensitivity in dense markets.

- Local same-day delivery up ~18% (2024)

- Local share ≈12% of parcel volume (2024)

- Lower switching costs for urban customers

- FedEx retains long-haul strength, loses short-haul margins

Retail Giants & Price-Sensitive Shoppers Squeeze FedEx Ground Margins

Customers hold strong bargaining power: retail giants (Walmart ~2.5B orders, Target ~1B in 2024) extract steep Ground discounts, pressuring FedEx’s 7.1% Ground margin (FY2024); price-sensitive consumers (62% choose cheaper shipping in 2025) and 12% local same-day share (2024) force yield-management and API/SLAs to retain volume.

| Metric | Value |

|---|---|

| Walmart orders (2024) | 2.5B |

| Target orders (2024) | ~1B |

| FedEx Ground margin (FY2024) | 7.1% |

| Consumers choosing cheaper shipping (2025) | 62% |

| Local same-day share (2024) | 12% |

Preview the Actual Deliverable

FedEx Porter's Five Forces Analysis

This preview shows the exact FedEx Porter's Five Forces analysis you'll receive—fully written, professionally formatted, and ready for download the moment you purchase.

No mockups or samples: the document displayed here is the complete deliverable with the same content and layout you'll get instantly after payment.

Use it immediately for strategy, valuation, or presentation—what you see is exactly what you’ll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

FedEx faces intense rivalry from global carriers, significant buyer power from large shippers, moderate supplier leverage in fuel and aircraft, low threat of new entrants due to high capital barriers, and rising substitution risks from digitization and regional couriers; this snapshot highlights strategic pressures shaping margins and growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FedEx’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility

FedEx relies heavily on fuel for ~80% of its air fleet and ~60% of ground energy use, so oil price swings directly raise operating costs; Brent averaged $86/bbl in 2025 YTD, up 14% vs 2024. Fuel surcharges blunt impact—fuel and related services were 16% of 2024 operating expenses—but suppliers still wield indirect pricing power over base margins. The 2025 shift to sustainable aviation fuel (SAF) concentrates supply: global SAF production met <0.1% of jet demand in 2024, creating a small pool of specialized, costlier suppliers.

Aircraft Manufacturing Duopoly

Labor and Specialized Talent

Technological Infrastructure Providers

FedEx depends heavily on major cloud providers and enterprise-software firms for real-time tracking and logistics AI; in 2024 FedEx reported cloud-related IT spend rising ~18% year-over-year to support these systems.

Those suppliers are critical to automated sorting and route optimization, and as FedEx folds deep-learning into its DRIVE initiative, platform lock-in and integration costs push switching costs higher.

- Cloud/AI spend up ~18% in 2024

- Drive deep-learning increases integration depth

- Automated sorting/route optimization depend on vendor tech

- Switching costs and vendor lock-in rising

Airport and Hub Infrastructure

Airport authorities and port operators control slots and land critical for FedEx’s global sorting; limited prime space at hubs like Memphis (MEM), Indianapolis (IND), and Paris CDG gives suppliers leverage in lease and expansion talks.

In 2024 FedEx reported capital leases and right-of-use assets of $7.9 billion, reflecting high real-estate exposure; losing hub access would directly harm time-definite promise and route density economics.

- Control of slots and land = high supplier leverage

- Prime hub scarcity raises renewal costs

- $7.9B capital lease exposure (2024)

- Hub loss → missed delivery guarantees, higher costs

Rising fuel, SAF scarcity and labor squeeze tighten carrier costs and hub leverage

Suppliers exert moderate-to-high power: fuel volatility (Brent $86/bbl 2025 YTD, +14% vs 2024) and SAF scarcity (<0.1% jet demand 2024) raise costs; Boeing/Airbus supply >95% of freighters, limiting switching; labor shortages pushed FedEx 2024 labor expense to $28.4B (+6%); cloud/IT spend rose ~18% in 2024; $7.9B capital lease exposure tightens hub leverage.

| Item | Metric (year) |

|---|---|

| Brent | $86/bbl (2025 YTD) |

| SAF supply | <0.1% jet demand (2024) |

| Labor expense | $28.4B (2024) |

| Cloud/IT spend | +18% YoY (2024) |

| Capital leases | $7.9B (2024) |

What is included in the product

Tailored exclusively for FedEx, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, barriers deterring new entrants, substitutes and emerging disruptors shaping FedEx’s pricing, profitability and strategic positioning.

Concise Porter's Five Forces snapshot for FedEx—quickly pinpoint competitive pressures and strategic levers to relieve operational and margin pain points.

Customers Bargaining Power

Low Switching Costs for Retail Users

Individual consumers and small businesses face low switching costs and can jump between FedEx, UPS, and USPS after seeing rates; in 2024 parcel price comparison sites showed up to 22% cost variance on small parcels, pushing FedEx to match discounts and keep on-time delivery over 94% to avoid churn.

Volume Leverage of E-commerce Giants

Price Sensitivity in Post-Inflationary Markets

In 2025’s post-inflationary market, 62% of US consumers say they choose cheaper shipping for non-essential goods, pushing average revenue per FedEx package down as economy parcels undercut premium overnight rates by ~30% in ticket price.

FedEx must tweak service tiers and yield-management—economy pricing grew 14% YoY in 2024—so it grabs price-sensitive volume without eroding express margins, which still deliver ~40% of operating income.

Demand for Deep Technical Integration

Large corporate clients demand deep technical integration and real-time visibility; in 2024, 62% of enterprise shippers ranked API connectivity as a top-three carrier requirement, forcing FedEx to treat tech as a customer mandate.

Without seamless APIs and end-to-end tracking, clients can shift volume to tech-forward rivals; FedEx reported a 3.5% revenue impact in select verticals when integrations lagged in 2023.

This dynamic converts IT from cost center to strategic retention tool: high-touch contracts now include SLAs for data transparency and integration timelines under 14 days to avoid churn.

- 62% of enterprise shippers prioritize API connectivity

- 3.5% revenue hit in impacted verticals (2023)

- SLA demand: real-time visibility, integration <14 days

Rise of Regional Delivery Alternatives

The rise of regional delivery startups and gig platforms (eg, GoShare, Roadie, local couriers) expanded urban choices, cutting last-mile share for national carriers; in 2024 US same-day/local delivery grew ~18% YoY and accounted for ~12% of parcel volume, eroding unit economics for FedEx on short trips.

Customers now unbundle services—using FedEx for long-haul and local players for rapid city delivery—reducing switching costs and increasing price sensitivity in dense markets.

- Local same-day delivery up ~18% (2024)

- Local share ≈12% of parcel volume (2024)

- Lower switching costs for urban customers

- FedEx retains long-haul strength, loses short-haul margins

Retail Giants & Price-Sensitive Shoppers Squeeze FedEx Ground Margins

Customers hold strong bargaining power: retail giants (Walmart ~2.5B orders, Target ~1B in 2024) extract steep Ground discounts, pressuring FedEx’s 7.1% Ground margin (FY2024); price-sensitive consumers (62% choose cheaper shipping in 2025) and 12% local same-day share (2024) force yield-management and API/SLAs to retain volume.

| Metric | Value |

|---|---|

| Walmart orders (2024) | 2.5B |

| Target orders (2024) | ~1B |

| FedEx Ground margin (FY2024) | 7.1% |

| Consumers choosing cheaper shipping (2025) | 62% |

| Local same-day share (2024) | 12% |

Preview the Actual Deliverable

FedEx Porter's Five Forces Analysis

This preview shows the exact FedEx Porter's Five Forces analysis you'll receive—fully written, professionally formatted, and ready for download the moment you purchase.

No mockups or samples: the document displayed here is the complete deliverable with the same content and layout you'll get instantly after payment.

Use it immediately for strategy, valuation, or presentation—what you see is exactly what you’ll own.