Femsa Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

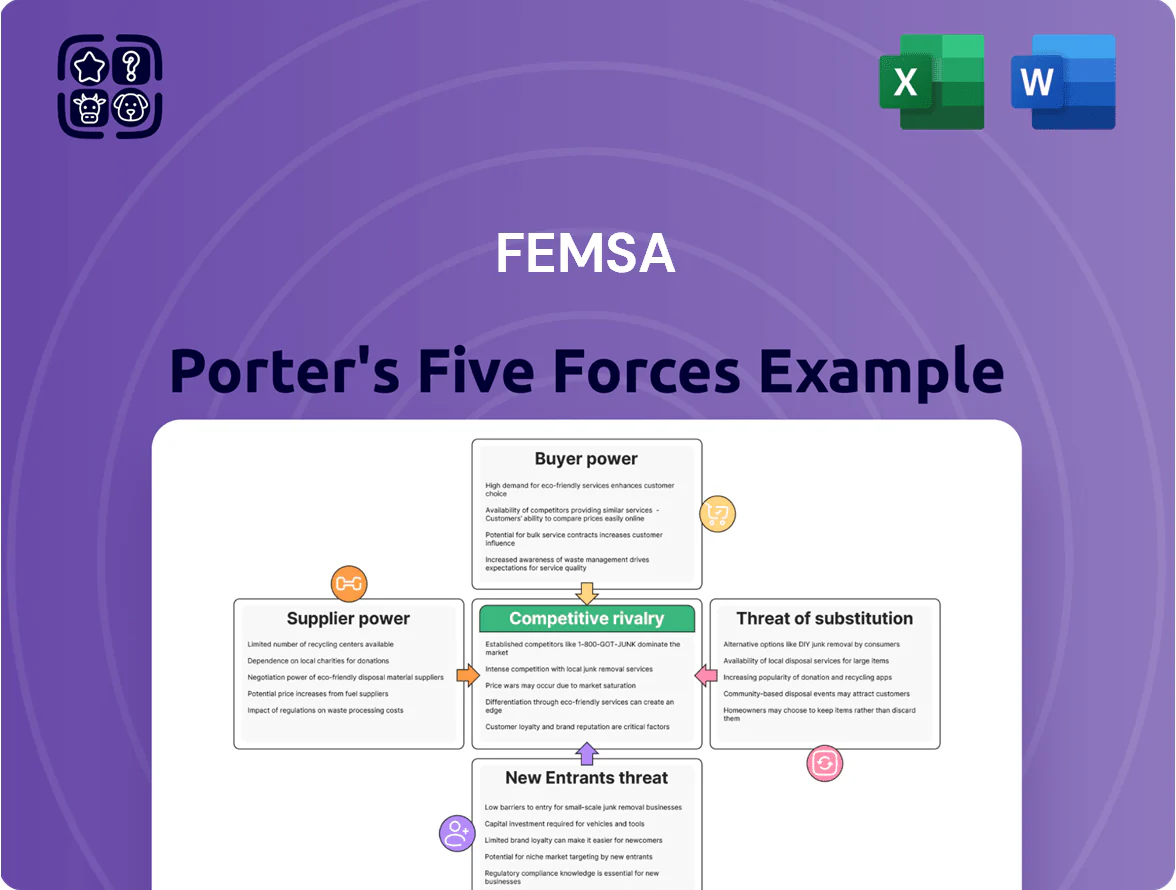

Femsa faces strong buyer power in concentrated retail channels, moderate supplier leverage for branded beverages, and notable rivalry from multinationals and regional chains—while barriers to entry limit new competitors but substitutes (local brands, private labels) pose risks; this snapshot hints at strategic pressure points. Unlock the full Porter's Five Forces Analysis to explore Femsa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of beverage concentrate supply

The Coca-Cola Company is FEMSA’s primary concentrate supplier, holding pricing and marketing leverage through long-term bottling agreements that covered roughly 70% of FEMSA Comercio de Bebidas volume in 2024; this restricts FEMSA from sourcing alternatives or negotiating materially lower concentrate costs.

Those contracts tie FEMSA to formulaic price adjustments—Coca-Cola’s global concentrate price rises of 3–6% in 2023–24 cut bottler gross margins by an estimated 150–250 basis points.

As a result, any Coca-Cola global pricing change translates almost immediately into FEMSA operating-margin volatility, given concentrated supply and limited pass-through flexibility.

Volatility in raw material procurement

FEMSA depends on large-volume suppliers for aluminum, PET resin and sweeteners, exposing cost base to global commodity swings—aluminum rose ~35% and PET resin ~28% in 2021–2022 shocks and sweetener prices jumped 15% in 2023; FEMSA hedges purchases but cannot fully offset spot moves. The sheer scale of annual packaging needs (hundreds of thousands of tonnes) gives major suppliers bargaining leverage during high inflation. The 2025 target to use recycled PET for food-grade bottles tightened supply; food-grade rPET capacity was only ~800 kt globally in 2024, constraining availability and pushing premiums of 10–20% over virgin PET.

Real estate and retail location providers

The rapid expansion of OXXO—over 22,000 stores in Mexico and 30,000+ across FEMSA’s Proximity footprint by end-2024—creates dependency on thousands of landlords, raising supplier (landlord) bargaining power.

Rising urban density in Latin America and selective European markets keeps owners’ leverage high in high-traffic zones, where vacancy rates fell below 3% in key cities in 2023.

Competition for these strategic sites pushes rents up; FEMSA reported Proximity operating margin pressure in 2024 linked to higher occupancy costs, which rose an estimated 4–7% year-on-year.

Dependence on specialized technology vendors

As FEMSA scales Spin by OXXO fintech services, dependence on specialized software and cybersecurity vendors rises, giving suppliers leverage through high switching costs and complex integrations.

By late 2025 FEMSA needs continuous digital upgrades; industry data show global fintech security spending grew ~12% YoY in 2024 to $38B, underscoring supplier bargaining power.

- High switching costs from custom integrations

- Technical complexity raises supplier leverage

- Fintech security spend $38B in 2024 (+12% YoY)

Labor market dynamics and specialized talent

- ~300,000 workforce size — high exposure

- Mexico min wage +20% in parts (2024) — cost risk

- Union reforms in Mexico/Chile — higher bargaining power

- HR spend ↑4% (2023) — talent cost pressure

Suppliers Squeeze Bottlers: Coke Concentrate, Packaging & Rents Drive Margin Pressure

Suppliers exert high bargaining power: Coca-Cola concentrate covers ~70% of 2024 beverage volume, driving 3–6% concentrate price hikes in 2023–24 that cut bottler margins ~150–250 bps; packaging commodities (aluminum +35% 2021–22; PET +28% 2021–22; rPET capacity ~800 kt in 2024, 10–20% premium) and landlord rents (vacancy <3% in key cities, occupancy costs +4–7% YoY 2024) add cost pressure.

| Metric | Value |

|---|---|

| Coca-Cola share of volume (2024) | ~70% |

| Concentrate price rise (2023–24) | 3–6% |

| Bottler margin impact | 150–250 bps |

| Aluminum change (2021–22) | +35% |

| PET change (2021–22) | +28% |

| rPET global capacity (2024) | ~800 kt |

| rPET premium vs virgin | 10–20% |

| Key-city vacancy (2023) | <3% |

| Occupancy cost change (2024) | +4–7% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Femsa that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to assess pricing power and strategic resilience.

One-sheet Porter's Five Forces for Femsa—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to inform strategic moves.

Customers Bargaining Power

Fragmented individual consumer base

The vast majority of FEMSA’s 2024 revenue—about US$30.2 billion—comes from millions of individual retail customers, each with negligible bargaining power; no single consumer can sway OXXO or Coca‑Cola FEMSA pricing or policy. Serving a mass market across ~21,000 OXXO stores and Coca‑Cola FEMSA’s 2024 volume of ~19.8 billion unit cases, customer fragmentation supports stable, uniform pricing across the network.

Low switching costs for retail shoppers

Consumers can easily switch from OXXO to competitors or mom-and-pop stores if unhappy with prices or service, keeping customer bargaining power high.

This low switching cost caps OXXO’s pricing power; a 1% price hike risks measurable foot-traffic declines seen across convenience retail.

By end-2025, digital price-comparison tools reached ~48% penetration among Mexican shoppers, raising sensitivity to small price gaps.

Price sensitivity in emerging markets

Influence of institutional healthcare buyers

- Institutional share ~35–40% of FEMSA Salud (2024 est.)

- Negotiated rebates typically 10–20% on core products

- +5 pp institutional share → ~70–120 bps margin pressure

Digital loyalty and ecosystem lock-in

FEMSA’s OXXO Premia and Spin by OXXO drove stickiness by late 2025, with OXXO Premia reporting over 20 million members and Spin 3.5 million users, bundling rewards, payments, and credit to lower churn and raise average basket value.

By integrating payments and financial services, FEMSA cuts switching incentives, increases purchase frequency by ~8% year-over-year, and reduces buyer bargaining power across its retail network.

- 20M+ OXXO Premia members (2025)

- 3.5M Spin users (2025)

- ~8% higher purchase frequency YoY

- Stronger consumer lock-in, lower churn

OXXO faces rising buyer power: digital price checks cap pricing; Salud rebates threaten margins

Customers are highly fragmented so individual retail buyers lack leverage, but low switching costs and 48% digital price-comparison penetration (2025) keep consumer bargaining power elevated, capping OXXO price hikes; institutional buyers in Salud (35–40% revenue share, 10–20% rebates) exert stronger leverage, risking 70–120 bps margin compression if their share rises 5 pp. OXXO Premia (20M) and Spin (3.5M) reduce churn and lower buyer power.

| Metric | 2024/2025 |

|---|---|

| FEMSA revenue from retail | ~US$30.2B (2024) |

| OXXO stores | ~21,000 |

| Coca‑Cola FEMSA volume | ~19.8B unit cases (2024) |

| Price-comparison penetration | ~48% (2025) |

| FEMSA Salud institutional share | 35–40% (2024 est.) |

| Typical institutional rebates | 10–20% |

| OXXO Premia members | 20M (2025) |

| Spin users | 3.5M (2025) |

Full Version Awaits

Femsa Porter's Five Forces Analysis

This preview shows the exact Femsa Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the final, professionally formatted file—ready for download and use the moment you buy, with detailed assessments of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Femsa faces strong buyer power in concentrated retail channels, moderate supplier leverage for branded beverages, and notable rivalry from multinationals and regional chains—while barriers to entry limit new competitors but substitutes (local brands, private labels) pose risks; this snapshot hints at strategic pressure points. Unlock the full Porter's Five Forces Analysis to explore Femsa’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of beverage concentrate supply

The Coca-Cola Company is FEMSA’s primary concentrate supplier, holding pricing and marketing leverage through long-term bottling agreements that covered roughly 70% of FEMSA Comercio de Bebidas volume in 2024; this restricts FEMSA from sourcing alternatives or negotiating materially lower concentrate costs.

Those contracts tie FEMSA to formulaic price adjustments—Coca-Cola’s global concentrate price rises of 3–6% in 2023–24 cut bottler gross margins by an estimated 150–250 basis points.

As a result, any Coca-Cola global pricing change translates almost immediately into FEMSA operating-margin volatility, given concentrated supply and limited pass-through flexibility.

Volatility in raw material procurement

FEMSA depends on large-volume suppliers for aluminum, PET resin and sweeteners, exposing cost base to global commodity swings—aluminum rose ~35% and PET resin ~28% in 2021–2022 shocks and sweetener prices jumped 15% in 2023; FEMSA hedges purchases but cannot fully offset spot moves. The sheer scale of annual packaging needs (hundreds of thousands of tonnes) gives major suppliers bargaining leverage during high inflation. The 2025 target to use recycled PET for food-grade bottles tightened supply; food-grade rPET capacity was only ~800 kt globally in 2024, constraining availability and pushing premiums of 10–20% over virgin PET.

Real estate and retail location providers

The rapid expansion of OXXO—over 22,000 stores in Mexico and 30,000+ across FEMSA’s Proximity footprint by end-2024—creates dependency on thousands of landlords, raising supplier (landlord) bargaining power.

Rising urban density in Latin America and selective European markets keeps owners’ leverage high in high-traffic zones, where vacancy rates fell below 3% in key cities in 2023.

Competition for these strategic sites pushes rents up; FEMSA reported Proximity operating margin pressure in 2024 linked to higher occupancy costs, which rose an estimated 4–7% year-on-year.

Dependence on specialized technology vendors

As FEMSA scales Spin by OXXO fintech services, dependence on specialized software and cybersecurity vendors rises, giving suppliers leverage through high switching costs and complex integrations.

By late 2025 FEMSA needs continuous digital upgrades; industry data show global fintech security spending grew ~12% YoY in 2024 to $38B, underscoring supplier bargaining power.

- High switching costs from custom integrations

- Technical complexity raises supplier leverage

- Fintech security spend $38B in 2024 (+12% YoY)

Labor market dynamics and specialized talent

- ~300,000 workforce size — high exposure

- Mexico min wage +20% in parts (2024) — cost risk

- Union reforms in Mexico/Chile — higher bargaining power

- HR spend ↑4% (2023) — talent cost pressure

Suppliers Squeeze Bottlers: Coke Concentrate, Packaging & Rents Drive Margin Pressure

Suppliers exert high bargaining power: Coca-Cola concentrate covers ~70% of 2024 beverage volume, driving 3–6% concentrate price hikes in 2023–24 that cut bottler margins ~150–250 bps; packaging commodities (aluminum +35% 2021–22; PET +28% 2021–22; rPET capacity ~800 kt in 2024, 10–20% premium) and landlord rents (vacancy <3% in key cities, occupancy costs +4–7% YoY 2024) add cost pressure.

| Metric | Value |

|---|---|

| Coca-Cola share of volume (2024) | ~70% |

| Concentrate price rise (2023–24) | 3–6% |

| Bottler margin impact | 150–250 bps |

| Aluminum change (2021–22) | +35% |

| PET change (2021–22) | +28% |

| rPET global capacity (2024) | ~800 kt |

| rPET premium vs virgin | 10–20% |

| Key-city vacancy (2023) | <3% |

| Occupancy cost change (2024) | +4–7% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Femsa that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to assess pricing power and strategic resilience.

One-sheet Porter's Five Forces for Femsa—quickly gauge supplier, buyer, entrant, substitute, and rivalry pressures to inform strategic moves.

Customers Bargaining Power

Fragmented individual consumer base

The vast majority of FEMSA’s 2024 revenue—about US$30.2 billion—comes from millions of individual retail customers, each with negligible bargaining power; no single consumer can sway OXXO or Coca‑Cola FEMSA pricing or policy. Serving a mass market across ~21,000 OXXO stores and Coca‑Cola FEMSA’s 2024 volume of ~19.8 billion unit cases, customer fragmentation supports stable, uniform pricing across the network.

Low switching costs for retail shoppers

Consumers can easily switch from OXXO to competitors or mom-and-pop stores if unhappy with prices or service, keeping customer bargaining power high.

This low switching cost caps OXXO’s pricing power; a 1% price hike risks measurable foot-traffic declines seen across convenience retail.

By end-2025, digital price-comparison tools reached ~48% penetration among Mexican shoppers, raising sensitivity to small price gaps.

Price sensitivity in emerging markets

Influence of institutional healthcare buyers

- Institutional share ~35–40% of FEMSA Salud (2024 est.)

- Negotiated rebates typically 10–20% on core products

- +5 pp institutional share → ~70–120 bps margin pressure

Digital loyalty and ecosystem lock-in

FEMSA’s OXXO Premia and Spin by OXXO drove stickiness by late 2025, with OXXO Premia reporting over 20 million members and Spin 3.5 million users, bundling rewards, payments, and credit to lower churn and raise average basket value.

By integrating payments and financial services, FEMSA cuts switching incentives, increases purchase frequency by ~8% year-over-year, and reduces buyer bargaining power across its retail network.

- 20M+ OXXO Premia members (2025)

- 3.5M Spin users (2025)

- ~8% higher purchase frequency YoY

- Stronger consumer lock-in, lower churn

OXXO faces rising buyer power: digital price checks cap pricing; Salud rebates threaten margins

Customers are highly fragmented so individual retail buyers lack leverage, but low switching costs and 48% digital price-comparison penetration (2025) keep consumer bargaining power elevated, capping OXXO price hikes; institutional buyers in Salud (35–40% revenue share, 10–20% rebates) exert stronger leverage, risking 70–120 bps margin compression if their share rises 5 pp. OXXO Premia (20M) and Spin (3.5M) reduce churn and lower buyer power.

| Metric | 2024/2025 |

|---|---|

| FEMSA revenue from retail | ~US$30.2B (2024) |

| OXXO stores | ~21,000 |

| Coca‑Cola FEMSA volume | ~19.8B unit cases (2024) |

| Price-comparison penetration | ~48% (2025) |

| FEMSA Salud institutional share | 35–40% (2024 est.) |

| Typical institutional rebates | 10–20% |

| OXXO Premia members | 20M (2025) |

| Spin users | 3.5M (2025) |

Full Version Awaits

Femsa Porter's Five Forces Analysis

This preview shows the exact Femsa Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the final, professionally formatted file—ready for download and use the moment you buy, with detailed assessments of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry.