Shanxi Xinghuacun Fen Wine Factory Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Shanxi Xinghuacun Fen Wine Factory operates in a concentrated baijiu market where strong brand loyalty and scale advantages limit new entrants but intensify rivalry among incumbents.

Supplier power is moderate—grain inputs are commoditized, yet premium packaging and distribution partnerships raise switching costs and margin pressure.

Substitute threats from wine and spirits are growing with younger consumers, while buyers wield rising influence through e-commerce transparency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanxi Xinghuacun Fen Wine Factory’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented agricultural supply base

The primary raw materials for Fenjiu—sorghum, barley, peas—come from a fragmented network of small-to-mid farmers, so no single supplier wields major leverage over Shanxi Xinghuacun; suppliers’ bargaining power is low. The company runs its own production bases and had 2024 procurement contracts covering roughly 40–50% of grain needs, stabilizing prices and quality. This mix limits suppliers’ ability to raise prices or change terms suddenly.

Importance of specialized packaging materials

Packaging is vital for high-end Fenjiu; specialized glass, porcelain bottles and decorative boxes drive perceived value and can add 10–15% to unit cost—China lists ~1,200 packaging firms but only ~40 meet premium spirits standards for Fenjiu’s specs.

Fenjiu’s scale—producing ~60 million liters annually in 2024—gives negotiating power to secure volume discounts and net terms, cutting packaging spend by an estimated 5–8%.

Supplier vertical integration risk is low: packaging manufacturers lack distillation, aging, and brand heritage skills central to Shanxi Xinghuacun’s spirit production, so takeover threat is minimal.

Water and unique yeast culture requirements

Fenjiu’s light-aroma depends on local spring water and proprietary Daqu yeast tied to Xinghuacun’s land rights and in-house production, so these inputs avoid open-market sourcing.

Internal control cuts supplier leverage: third-party yeast or water suppliers represent <5% of fermentation input value; 2024 capex ¥120m expanded Daqu capacity, lowering external dependency.

Energy costs and utility dependence

Production of distilled spirits is energy-heavy, needing steady electricity and natural gas for heating and distillation, and rates are set mainly by state-owned utilities so Shanxi Xinghuacun has almost no bargaining power.

Energy costs form a sizable, stable portion of COGS across Chinese baijiu makers; in 2024 provincial industrial electricity tariffs in Shanxi averaged ~0.57 CNY/kWh and industrial natural gas ~2.1 CNY/m3.

To limit exposure, by 2025 Xinghuacun invested in heat-recovery, variable-speed drives, and upgraded boilers, cutting energy intensity an estimated 8–12%.

- Energy intensity high: major overhead

- Supplier power: state monopolies, low negotiation

- 2024 tariffs: ~0.57 CNY/kWh, gas ~2.1 CNY/m3

- 2025 efficiency gains: ~8–12% reduction

Switching costs for raw commodities

The switching costs for standard grains like sorghum are low because they are widely traded; in 2024 China produced 44.5 million tonnes of sorghum, so Shanxi Xinghuacun can pivot among certified bases if quality or prices falter.

This flexibility stops any regional supplier from exerting pricing power, and input standardization keeps the company dominant in the buyer-seller relationship.

- China sorghum supply 2024: 44.5 Mt

- Low switching cost → limited supplier power

- Multiple certified bases across provinces

- Standardized input preserves buyer dominance

Low supplier power as scale, contracts and efficiency cut costs amid energy risk

Suppliers’ bargaining power is low: fragmented grain base, in-house Daqu and 40–50% contracted procurement in 2024 cut dependence; scale (≈60m L output 2024) wins packaging discounts (5–8%). Energy is the main supplier risk—2024 Shanxi tariffs ~0.57 CNY/kWh and gas ~2.1 CNY/m3—though 2025 efficiency upgrades trimmed energy intensity ~8–12%.

| Metric | 2024 value |

|---|---|

| Output | ≈60m L |

| Contracted grain | 40–50% |

| Sorghum supply China | 44.5 Mt |

| Electricity tariff Shanxi | ~0.57 CNY/kWh |

| Natural gas | ~2.1 CNY/m3 |

| Packaging cost cut | 5–8% |

| Energy intensity reduction (2025) | 8–12% |

What is included in the product

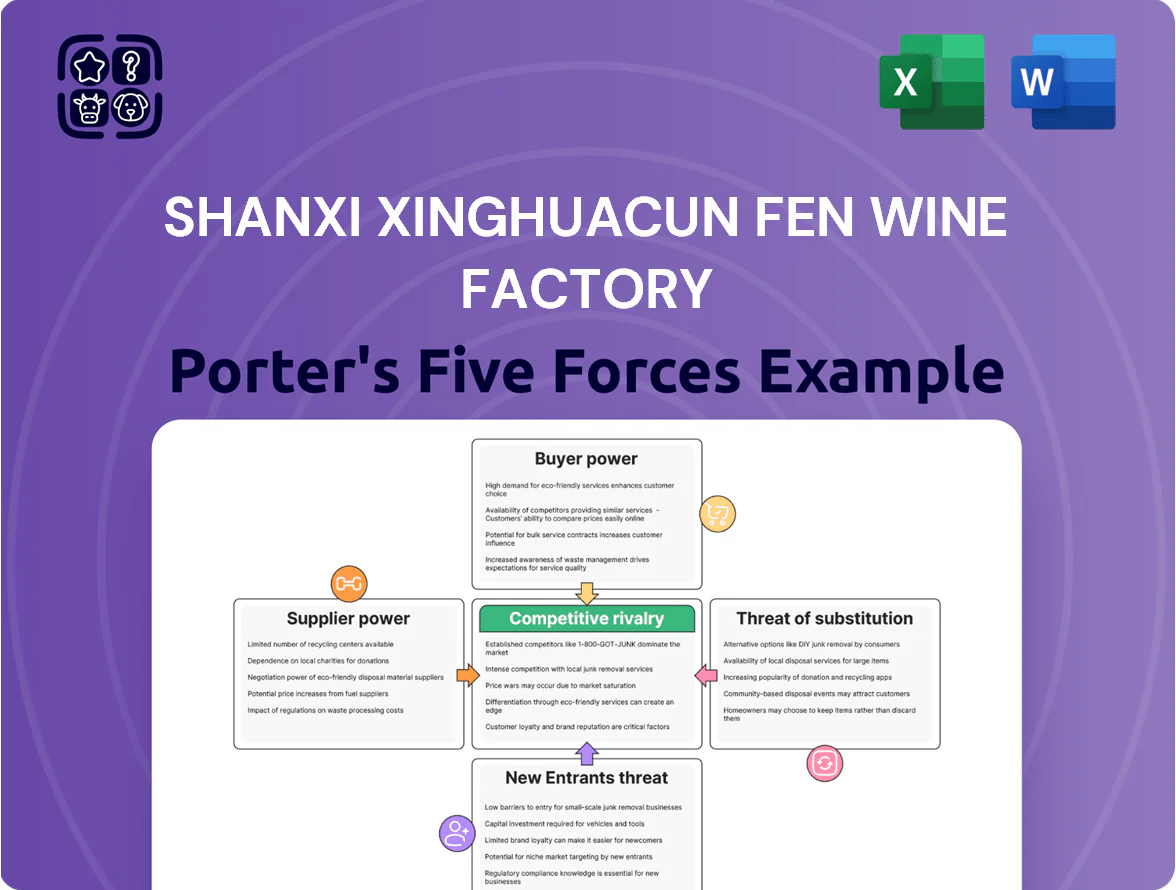

Tailored Porter’s Five Forces analysis for Shanxi Xinghuacun Fen Wine Factory uncovering competitive rivalry, buyer and supplier bargaining power, threat of new entrants and substitutes, and identifying disruptive forces and market entry barriers that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for Shanxi Xinghuacun Fen Wine Factory—fast clarity on supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and risk mitigation.

Customers Bargaining Power

Dominance of large scale distributors

High brand loyalty among retail consumers

Individual consumers of premium light-aroma baijiu show strong brand loyalty, cutting collective bargaining power; Fenjiu held about 21% market share in light-aroma premium baijiu in 2024, so few high-end substitutes exist for its taste.

That market dominance lets Shanxi Xinghuacun Fen Wine Factory keep premium pricing—average retail price rose 8% in 2024—even in downturns.

The Time-Honored cultural status drives price-inelastic demand among core buyers; repeat purchase rates exceed 60% annually.

Transparency in digital pricing

E-commerce has raised price transparency, with 72% of Chinese liquor buyers using online price comparison tools in 2024, making regional price gaps harder to sustain and forcing Shanxi Xinghuacun Fen Wine Factory to push unified pricing across channels.

Easy cross-retailer comparison gives consumers more information power than in the retail era, pressuring margins as online average selling price variance fell to 6% in 2024 from 14% in 2019.

To protect perceived value the company sells exclusive online editions and ran loyalty programs—online limited releases grew 18% of digital revenue in 2024, helping defend brand premium.

Corporate and institutional buyer influence

Corporate and institutional buyers—about 30–40% of Fenjiu sales in provincial channels in 2024—buy large volumes for banquets and gifting, securing volume discounts and bespoke service that raise their bargaining power above retail customers.

Their demand tracks GDP and government hospitality policy; Fenjiu reported a 12% year-on-year institutional channel drop in 2023 during anti-extravagance restrictions, then recovered 8% in 2024 as policies eased.

Shanxi Xinghuacun reduces dependence by diversifying SKUs toward younger private-sector professionals and collectors, launching premium boutique lines that grew direct-to-consumer revenue 18% in 2024.

- Institutional share ~30–40%

- Institutional revenue swing: -12% (2023), +8% (2024)

- D2C/premium SKU growth: +18% (2024)

Low switching costs in the mid-range segment

While premium Fenjiu sees strong brand loyalty, bargaining power of customers rises in the mid-to-low segments where switching costs are low and price sensitivity is high; industry data shows mid-range baijiu prices fell 2.3% in 2024 as promotions surged.

Consumers can move to other light-aroma brands or regional players if Fenjiu hikes prices, so the firm must refresh marketing, SKUs, and packaging—Fenjiu’s mid-tier volume fell 4% in H1 2025 versus premium steady growth.

This pressure caps Fenjiu’s pricing power in mass-market channels, forcing trade discounts and local promotions that compress gross margins by an estimated 120–180 basis points relative to premium lines.

- Low switching costs increase customer bargaining power

- Mid-tier price sensitivity: 2.3% price decline 2024

- Fenjiu mid-tier volume -4% H1 2025

- Margin compression ~120–180 bps in mass market

Fenjiu: distributor pressure trims mass margins despite strong premium share

| Metric | 2023/2024 |

|---|---|

| Revenue via distributors | 58% of ¥14.2bn (2024) |

| Premium market share | 21% (2024) |

| Repeat rate | >60% annual |

| Online price comparison users | 72% (2024) |

| Online ASP variance | 6% (2024) |

| Institutional share | 30–40% |

| Mass‑market margin hit | −120–180 bps |

Preview the Actual Deliverable

Shanxi Xinghuacun Fen Wine Factory Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shanxi Xinghuacun Fen Wine Factory you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Shanxi Xinghuacun Fen Wine Factory operates in a concentrated baijiu market where strong brand loyalty and scale advantages limit new entrants but intensify rivalry among incumbents.

Supplier power is moderate—grain inputs are commoditized, yet premium packaging and distribution partnerships raise switching costs and margin pressure.

Substitute threats from wine and spirits are growing with younger consumers, while buyers wield rising influence through e-commerce transparency.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanxi Xinghuacun Fen Wine Factory’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented agricultural supply base

The primary raw materials for Fenjiu—sorghum, barley, peas—come from a fragmented network of small-to-mid farmers, so no single supplier wields major leverage over Shanxi Xinghuacun; suppliers’ bargaining power is low. The company runs its own production bases and had 2024 procurement contracts covering roughly 40–50% of grain needs, stabilizing prices and quality. This mix limits suppliers’ ability to raise prices or change terms suddenly.

Importance of specialized packaging materials

Packaging is vital for high-end Fenjiu; specialized glass, porcelain bottles and decorative boxes drive perceived value and can add 10–15% to unit cost—China lists ~1,200 packaging firms but only ~40 meet premium spirits standards for Fenjiu’s specs.

Fenjiu’s scale—producing ~60 million liters annually in 2024—gives negotiating power to secure volume discounts and net terms, cutting packaging spend by an estimated 5–8%.

Supplier vertical integration risk is low: packaging manufacturers lack distillation, aging, and brand heritage skills central to Shanxi Xinghuacun’s spirit production, so takeover threat is minimal.

Water and unique yeast culture requirements

Fenjiu’s light-aroma depends on local spring water and proprietary Daqu yeast tied to Xinghuacun’s land rights and in-house production, so these inputs avoid open-market sourcing.

Internal control cuts supplier leverage: third-party yeast or water suppliers represent <5% of fermentation input value; 2024 capex ¥120m expanded Daqu capacity, lowering external dependency.

Energy costs and utility dependence

Production of distilled spirits is energy-heavy, needing steady electricity and natural gas for heating and distillation, and rates are set mainly by state-owned utilities so Shanxi Xinghuacun has almost no bargaining power.

Energy costs form a sizable, stable portion of COGS across Chinese baijiu makers; in 2024 provincial industrial electricity tariffs in Shanxi averaged ~0.57 CNY/kWh and industrial natural gas ~2.1 CNY/m3.

To limit exposure, by 2025 Xinghuacun invested in heat-recovery, variable-speed drives, and upgraded boilers, cutting energy intensity an estimated 8–12%.

- Energy intensity high: major overhead

- Supplier power: state monopolies, low negotiation

- 2024 tariffs: ~0.57 CNY/kWh, gas ~2.1 CNY/m3

- 2025 efficiency gains: ~8–12% reduction

Switching costs for raw commodities

The switching costs for standard grains like sorghum are low because they are widely traded; in 2024 China produced 44.5 million tonnes of sorghum, so Shanxi Xinghuacun can pivot among certified bases if quality or prices falter.

This flexibility stops any regional supplier from exerting pricing power, and input standardization keeps the company dominant in the buyer-seller relationship.

- China sorghum supply 2024: 44.5 Mt

- Low switching cost → limited supplier power

- Multiple certified bases across provinces

- Standardized input preserves buyer dominance

Low supplier power as scale, contracts and efficiency cut costs amid energy risk

Suppliers’ bargaining power is low: fragmented grain base, in-house Daqu and 40–50% contracted procurement in 2024 cut dependence; scale (≈60m L output 2024) wins packaging discounts (5–8%). Energy is the main supplier risk—2024 Shanxi tariffs ~0.57 CNY/kWh and gas ~2.1 CNY/m3—though 2025 efficiency upgrades trimmed energy intensity ~8–12%.

| Metric | 2024 value |

|---|---|

| Output | ≈60m L |

| Contracted grain | 40–50% |

| Sorghum supply China | 44.5 Mt |

| Electricity tariff Shanxi | ~0.57 CNY/kWh |

| Natural gas | ~2.1 CNY/m3 |

| Packaging cost cut | 5–8% |

| Energy intensity reduction (2025) | 8–12% |

What is included in the product

Tailored Porter’s Five Forces analysis for Shanxi Xinghuacun Fen Wine Factory uncovering competitive rivalry, buyer and supplier bargaining power, threat of new entrants and substitutes, and identifying disruptive forces and market entry barriers that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for Shanxi Xinghuacun Fen Wine Factory—fast clarity on supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and risk mitigation.

Customers Bargaining Power

Dominance of large scale distributors

High brand loyalty among retail consumers

Individual consumers of premium light-aroma baijiu show strong brand loyalty, cutting collective bargaining power; Fenjiu held about 21% market share in light-aroma premium baijiu in 2024, so few high-end substitutes exist for its taste.

That market dominance lets Shanxi Xinghuacun Fen Wine Factory keep premium pricing—average retail price rose 8% in 2024—even in downturns.

The Time-Honored cultural status drives price-inelastic demand among core buyers; repeat purchase rates exceed 60% annually.

Transparency in digital pricing

E-commerce has raised price transparency, with 72% of Chinese liquor buyers using online price comparison tools in 2024, making regional price gaps harder to sustain and forcing Shanxi Xinghuacun Fen Wine Factory to push unified pricing across channels.

Easy cross-retailer comparison gives consumers more information power than in the retail era, pressuring margins as online average selling price variance fell to 6% in 2024 from 14% in 2019.

To protect perceived value the company sells exclusive online editions and ran loyalty programs—online limited releases grew 18% of digital revenue in 2024, helping defend brand premium.

Corporate and institutional buyer influence

Corporate and institutional buyers—about 30–40% of Fenjiu sales in provincial channels in 2024—buy large volumes for banquets and gifting, securing volume discounts and bespoke service that raise their bargaining power above retail customers.

Their demand tracks GDP and government hospitality policy; Fenjiu reported a 12% year-on-year institutional channel drop in 2023 during anti-extravagance restrictions, then recovered 8% in 2024 as policies eased.

Shanxi Xinghuacun reduces dependence by diversifying SKUs toward younger private-sector professionals and collectors, launching premium boutique lines that grew direct-to-consumer revenue 18% in 2024.

- Institutional share ~30–40%

- Institutional revenue swing: -12% (2023), +8% (2024)

- D2C/premium SKU growth: +18% (2024)

Low switching costs in the mid-range segment

While premium Fenjiu sees strong brand loyalty, bargaining power of customers rises in the mid-to-low segments where switching costs are low and price sensitivity is high; industry data shows mid-range baijiu prices fell 2.3% in 2024 as promotions surged.

Consumers can move to other light-aroma brands or regional players if Fenjiu hikes prices, so the firm must refresh marketing, SKUs, and packaging—Fenjiu’s mid-tier volume fell 4% in H1 2025 versus premium steady growth.

This pressure caps Fenjiu’s pricing power in mass-market channels, forcing trade discounts and local promotions that compress gross margins by an estimated 120–180 basis points relative to premium lines.

- Low switching costs increase customer bargaining power

- Mid-tier price sensitivity: 2.3% price decline 2024

- Fenjiu mid-tier volume -4% H1 2025

- Margin compression ~120–180 bps in mass market

Fenjiu: distributor pressure trims mass margins despite strong premium share

| Metric | 2023/2024 |

|---|---|

| Revenue via distributors | 58% of ¥14.2bn (2024) |

| Premium market share | 21% (2024) |

| Repeat rate | >60% annual |

| Online price comparison users | 72% (2024) |

| Online ASP variance | 6% (2024) |

| Institutional share | 30–40% |

| Mass‑market margin hit | −120–180 bps |

Preview the Actual Deliverable

Shanxi Xinghuacun Fen Wine Factory Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shanxi Xinghuacun Fen Wine Factory you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for download.