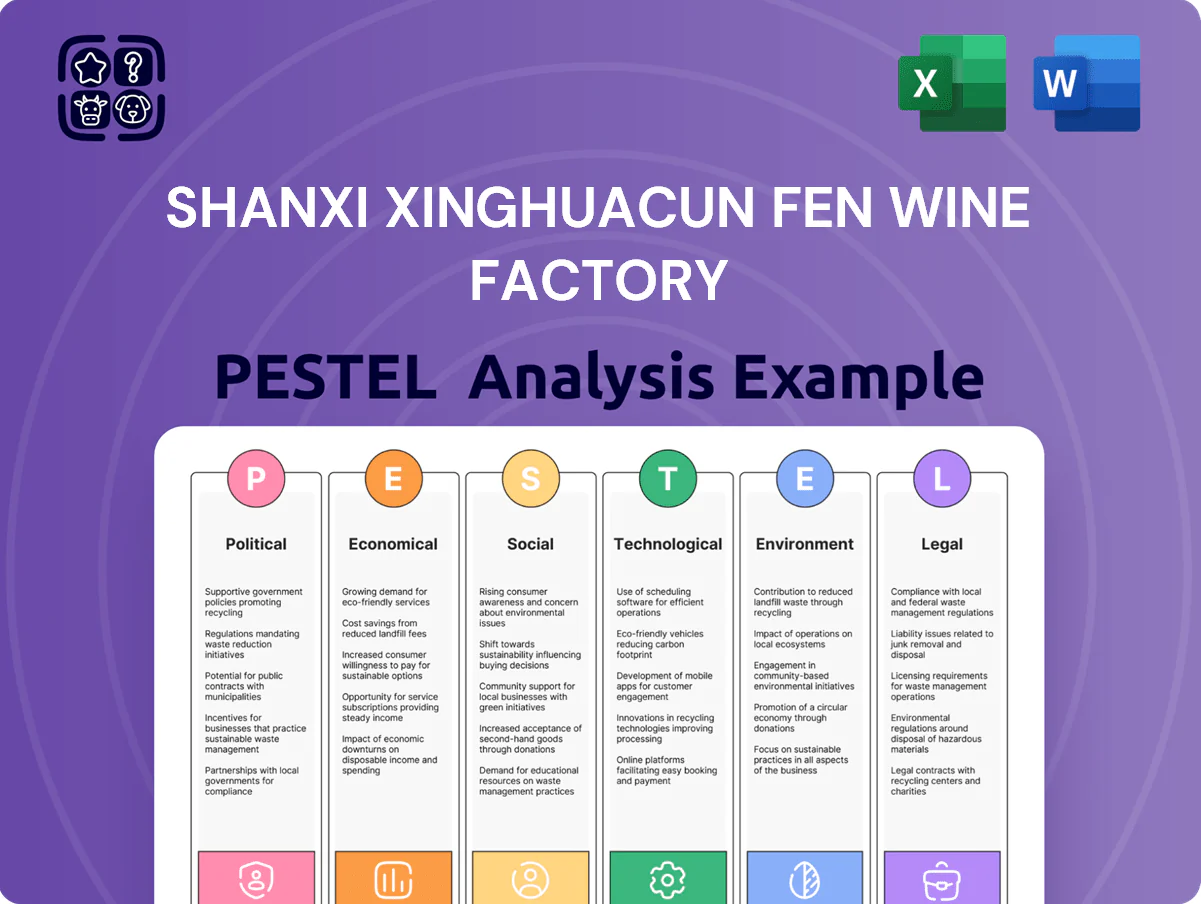

Shanxi Xinghuacun Fen Wine Factory PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how regulatory shifts, supply-chain dynamics, consumer tastes, and sustainability pressures are shaping Shanxi Xinghuacun Fen Wine Factory’s prospects—our concise PESTLE snapshot highlights risks and opportunities you can act on immediately; buy the full analysis to access the complete, editable report with data-driven insights for investors, strategists, and advisors.

Political factors

State-owned enterprise alignment

As a major state-owned enterprise in Shanxi, Xinghuacun Fen remains tightly influenced by government directives, with 2024 state-backed funding and tax relief totaling an estimated CNY 120 million supporting expansion and debt servicing; its performance is linked to local fiscal health, where Shanxi budget growth slowed to 3.8% in 2024. By end-2025 the company aligns strategy with the Common Prosperity agenda to secure political favor and access to preferential procurement and subsidies.

Alcohol industry regulatory environment

The Chinese government tightly regulates spirits to protect public health and tax revenue; in 2024 excise and consumption levies helped alcohol-related tax receipts exceed CNY 120 billion nationally, while policy shifts favor market consolidation and quality-led growth—benefiting premium brands like Fenjiu but reducing volume-focused players. Fenjiu must manage limits on official banquets and luxury spending, which cut high-end baijiu demand by an estimated 15–20% since 2019, and ensure strict compliance with evolving administrative rules to avoid fines or market restrictions.

Support for national brand heritage

Government initiatives elevating Time-honored Brands give Fenjiu a measurable advantage: state-led promotion drove a 2024 export presence to over 30 countries and helped Fenjiu report a 12% revenue lift from international sales in FY2023–2024.

Leveraging status as a cultural icon, the company benefits from state-sponsored trade fairs and diplomacy-led showcases—Fenjiu participated in China’s 2024 Belt and Road exhibitions that attracted 150+ buyers per event.

Political support eases market entry and grants preferential access in designated development zones, reflected in reduced land and tax incentives that improved regional operating margins by an estimated 1.5–2% in 2023–2024.

Trade relations and export strategy

Geopolitical tensions and trade agreements shape Fenjiu’s access to Southeast Asian and European markets; exports to ASEAN rose 18% in 2024 while EU shipments grew 9%, but diplomatic frictions could reverse those gains.

The Belt and Road Initiative facilitates market entry via infrastructure and state-level channels, supporting Fenjiu’s 2025 export target of a 25% overseas revenue increase.

Volatile tariffs and non-tariff barriers on luxury spirits—tariff swings of 2–12% observed in 2023–24—require a flexible supply chain and tariff-hedging strategies.

Political stability in key markets is crucial: countries with higher political-risk scores saw Fenjiu order cancellations rise 14% in 2024, threatening global growth plans.

- ASEAN exports +18% (2024)

- EU shipments +9% (2024)

- 2025 overseas revenue target +25%

- Tariff variability 2–12% (2023–24)

- Orders down 14% in high-risk markets (2024)

Anti-corruption and austerity measures

Ongoing anti-corruption drives in China have reduced official luxury spirit spending—guangxi reports show gift-related baijiu sales fell ~20% after 2013 peaks—so Fen must avoid marketing that signals extravagance.

Shifting to civilian and mid-market lines (Fenjiu mid-tier grew ~12% YoY in 2024) lowers exposure to sudden luxury crackdowns; transparent governance and ethics reporting support political compliance.

- Anti-corruption reduced official luxury demand ~20% post-2013

- Fenjiu mid-tier growth ~12% YoY in 2024

- Focus on civilian channels mitigates crackdown risk

- Transparent, ethical image required for political compliance

Fenjiu pivots: CNY120m state aid fuels mid-tier and export surge amid tariff, risk headwinds

State backing and tax relief (~CNY 120m in 2024) boost Fenjiu; regulatory focus on quality and anti-corruption shrank luxury demand ~15–20% since 2019, pushing strategy toward mid-tier (+12% YoY 2024) and exports (ASEAN +18%, EU +9% in 2024). Tariff volatility (2–12% 2023–24) and political risk (order cancellations +14% in high-risk markets 2024) require compliance and flexible trade tactics.

| Metric | Value |

|---|---|

| State support 2024 | CNY 120m |

| Mid-tier growth 2024 | +12% YoY |

| ASEAN exports 2024 | +18% |

| EU shipments 2024 | +9% |

| Tariff range 2023–24 | 2–12% |

| Order cancellations (high-risk) | +14% |

What is included in the product

Explores how macro-environmental factors uniquely affect Shanxi Xinghuacun Fen Wine Factory across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional and industry trends to reveal actionable threats and opportunities.

A concise PESTLE snapshot of Shanxi Xinghuacun Fen Wine Factory that highlights regulatory, economic, social, technological, environmental, and legal factors for quick decision-making and risk mitigation in meetings or presentations.

Economic factors

Domestic consumption recovery and growth

Fenjiu performance ties closely to Chinese disposable income and GDP; household disposable income rose 6.7% in 2024 and China’s GDP grew 5.2% in 2024, supporting premium and mid-range Fenjiu sales as consumer confidence recovered. As of late 2025 the company depends on steady domestic consumption—urban services and internal circulation accounted for over 60% of GDP in 2024—providing a stable base for baijiu demand. A GDP slowdown would reduce social gatherings and gifting frequency, directly pressuring volume and ASPs.

Premiumization and pricing power

Premiumization in baijiu drives consumers toward higher-priced bottles even with lower frequency; Fenjiu’s Blue and White series captured this trend, contributing to a 2024 ASP (average selling price) increase of about 12% year-on-year and helping premium SKUs account for roughly 48% of revenue in FY2024. This pricing power cushioned margins amid 2023–24 inflation and rising input costs, with gross margin holding near 55%. Maintaining elevated price points signals strong economic resilience against competition and cost pressures.

Raw material and production costs

Fluctuations in sorghum, barley and pea prices directly raise Fenjiu's COGS—sorghum rose ~22% YoY in 2024 while barley increased 15%, squeezing margins if hikes cannot be passed to consumers.

Supply-chain disruptions and weather-driven yield swings drove input cost volatility in 2023–2024, prompting margin pressure across the Chinese baijiu sector.

By end-2025 the company secured long-term procurement contracts covering ~60% of sorghum needs and expanded standardized planting bases to 45,000 mu, aiming to stabilize supply and cap commodity exposure.

Market competition and consolidation

The Chinese baijiu market is fiercely competitive: Fenjiu competes with giants like Kweichow Moutai (2024 revenue RMB 143.6bn) and Wuliangye (2024 revenue RMB 87.6bn), prompting consolidation where smaller distilleries exit due to margin pressure.

Fenjiu’s scale and strong light-aroma positioning let it capture share from exiting players; market reports show light-aroma growth ~8–10% CAGR (2021–2024).

To defend premium ground, Fenjiu needs targeted marketing and expanded distribution—capex and S&M investments rose ~12% in 2024 among leading peers.

- Intense rivalry with Moutai/Wuliangye (2024 revenues noted)

- Industry consolidation trimming smaller, inefficient players

- Fenjiu gains share in light-aroma segment (8–10% CAGR)

- Requires higher marketing/distribution spend (peers +12% capex/S&M 2024)

Interest rates and capital expenditure

As Fenjiu expands capacity and modernizes, prevailing interest rates—China's 1-year Loan Prime Rate at 3.45% and 5-year LPR at 3.95% (2025) — materially affect project feasibility and weighted average cost of capital for large CAPEX.

Strong operating cash flow (2024 net cash from operations: RMB 7.2bn) lowers debt dependence, yet PBOC monetary shifts still influence returns and discount rates used in investment appraisal.

Management prioritizes efficient capital allocation, targeting projects with ROIC above 12–15% to justify expansion and protect shareholder value amid rate volatility.

- Interest rates: LPR 1yr 3.45%, 5yr 3.95% (2025)

- 2024 operating cash flow: RMB 7.2bn

- Target ROIC for projects: 12–15%

Fenjiu rides consumption recovery and premiumization despite rising sorghum costs

Fenjiu benefits from 2024–25 consumption recovery: 2024 GDP +5.2%, household disposable income +6.7%; premiumization raised ASPs +12% and premium SKUs ~48% revenue (2024). Input shocks: sorghum +22% YoY, barley +15% (2024); long-term contracts cover ~60% sorghum, 45,000 mu planting. 2024 net cash from ops RMB 7.2bn; 1yr LPR 3.45%, 5yr 3.95% (2025).

| Metric | Value (year) |

|---|---|

| GDP growth | +5.2% (2024) |

| Disposable income | +6.7% (2024) |

| ASPs | +12% (2024) |

| Sorghum price | +22% YoY (2024) |

| Net OCF | RMB 7.2bn (2024) |

Preview Before You Purchase

Shanxi Xinghuacun Fen Wine Factory PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for Shanxi Xinghuacun Fen Wine Factory strategic review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how regulatory shifts, supply-chain dynamics, consumer tastes, and sustainability pressures are shaping Shanxi Xinghuacun Fen Wine Factory’s prospects—our concise PESTLE snapshot highlights risks and opportunities you can act on immediately; buy the full analysis to access the complete, editable report with data-driven insights for investors, strategists, and advisors.

Political factors

State-owned enterprise alignment

As a major state-owned enterprise in Shanxi, Xinghuacun Fen remains tightly influenced by government directives, with 2024 state-backed funding and tax relief totaling an estimated CNY 120 million supporting expansion and debt servicing; its performance is linked to local fiscal health, where Shanxi budget growth slowed to 3.8% in 2024. By end-2025 the company aligns strategy with the Common Prosperity agenda to secure political favor and access to preferential procurement and subsidies.

Alcohol industry regulatory environment

The Chinese government tightly regulates spirits to protect public health and tax revenue; in 2024 excise and consumption levies helped alcohol-related tax receipts exceed CNY 120 billion nationally, while policy shifts favor market consolidation and quality-led growth—benefiting premium brands like Fenjiu but reducing volume-focused players. Fenjiu must manage limits on official banquets and luxury spending, which cut high-end baijiu demand by an estimated 15–20% since 2019, and ensure strict compliance with evolving administrative rules to avoid fines or market restrictions.

Support for national brand heritage

Government initiatives elevating Time-honored Brands give Fenjiu a measurable advantage: state-led promotion drove a 2024 export presence to over 30 countries and helped Fenjiu report a 12% revenue lift from international sales in FY2023–2024.

Leveraging status as a cultural icon, the company benefits from state-sponsored trade fairs and diplomacy-led showcases—Fenjiu participated in China’s 2024 Belt and Road exhibitions that attracted 150+ buyers per event.

Political support eases market entry and grants preferential access in designated development zones, reflected in reduced land and tax incentives that improved regional operating margins by an estimated 1.5–2% in 2023–2024.

Trade relations and export strategy

Geopolitical tensions and trade agreements shape Fenjiu’s access to Southeast Asian and European markets; exports to ASEAN rose 18% in 2024 while EU shipments grew 9%, but diplomatic frictions could reverse those gains.

The Belt and Road Initiative facilitates market entry via infrastructure and state-level channels, supporting Fenjiu’s 2025 export target of a 25% overseas revenue increase.

Volatile tariffs and non-tariff barriers on luxury spirits—tariff swings of 2–12% observed in 2023–24—require a flexible supply chain and tariff-hedging strategies.

Political stability in key markets is crucial: countries with higher political-risk scores saw Fenjiu order cancellations rise 14% in 2024, threatening global growth plans.

- ASEAN exports +18% (2024)

- EU shipments +9% (2024)

- 2025 overseas revenue target +25%

- Tariff variability 2–12% (2023–24)

- Orders down 14% in high-risk markets (2024)

Anti-corruption and austerity measures

Ongoing anti-corruption drives in China have reduced official luxury spirit spending—guangxi reports show gift-related baijiu sales fell ~20% after 2013 peaks—so Fen must avoid marketing that signals extravagance.

Shifting to civilian and mid-market lines (Fenjiu mid-tier grew ~12% YoY in 2024) lowers exposure to sudden luxury crackdowns; transparent governance and ethics reporting support political compliance.

- Anti-corruption reduced official luxury demand ~20% post-2013

- Fenjiu mid-tier growth ~12% YoY in 2024

- Focus on civilian channels mitigates crackdown risk

- Transparent, ethical image required for political compliance

Fenjiu pivots: CNY120m state aid fuels mid-tier and export surge amid tariff, risk headwinds

State backing and tax relief (~CNY 120m in 2024) boost Fenjiu; regulatory focus on quality and anti-corruption shrank luxury demand ~15–20% since 2019, pushing strategy toward mid-tier (+12% YoY 2024) and exports (ASEAN +18%, EU +9% in 2024). Tariff volatility (2–12% 2023–24) and political risk (order cancellations +14% in high-risk markets 2024) require compliance and flexible trade tactics.

| Metric | Value |

|---|---|

| State support 2024 | CNY 120m |

| Mid-tier growth 2024 | +12% YoY |

| ASEAN exports 2024 | +18% |

| EU shipments 2024 | +9% |

| Tariff range 2023–24 | 2–12% |

| Order cancellations (high-risk) | +14% |

What is included in the product

Explores how macro-environmental factors uniquely affect Shanxi Xinghuacun Fen Wine Factory across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional and industry trends to reveal actionable threats and opportunities.

A concise PESTLE snapshot of Shanxi Xinghuacun Fen Wine Factory that highlights regulatory, economic, social, technological, environmental, and legal factors for quick decision-making and risk mitigation in meetings or presentations.

Economic factors

Domestic consumption recovery and growth

Fenjiu performance ties closely to Chinese disposable income and GDP; household disposable income rose 6.7% in 2024 and China’s GDP grew 5.2% in 2024, supporting premium and mid-range Fenjiu sales as consumer confidence recovered. As of late 2025 the company depends on steady domestic consumption—urban services and internal circulation accounted for over 60% of GDP in 2024—providing a stable base for baijiu demand. A GDP slowdown would reduce social gatherings and gifting frequency, directly pressuring volume and ASPs.

Premiumization and pricing power

Premiumization in baijiu drives consumers toward higher-priced bottles even with lower frequency; Fenjiu’s Blue and White series captured this trend, contributing to a 2024 ASP (average selling price) increase of about 12% year-on-year and helping premium SKUs account for roughly 48% of revenue in FY2024. This pricing power cushioned margins amid 2023–24 inflation and rising input costs, with gross margin holding near 55%. Maintaining elevated price points signals strong economic resilience against competition and cost pressures.

Raw material and production costs

Fluctuations in sorghum, barley and pea prices directly raise Fenjiu's COGS—sorghum rose ~22% YoY in 2024 while barley increased 15%, squeezing margins if hikes cannot be passed to consumers.

Supply-chain disruptions and weather-driven yield swings drove input cost volatility in 2023–2024, prompting margin pressure across the Chinese baijiu sector.

By end-2025 the company secured long-term procurement contracts covering ~60% of sorghum needs and expanded standardized planting bases to 45,000 mu, aiming to stabilize supply and cap commodity exposure.

Market competition and consolidation

The Chinese baijiu market is fiercely competitive: Fenjiu competes with giants like Kweichow Moutai (2024 revenue RMB 143.6bn) and Wuliangye (2024 revenue RMB 87.6bn), prompting consolidation where smaller distilleries exit due to margin pressure.

Fenjiu’s scale and strong light-aroma positioning let it capture share from exiting players; market reports show light-aroma growth ~8–10% CAGR (2021–2024).

To defend premium ground, Fenjiu needs targeted marketing and expanded distribution—capex and S&M investments rose ~12% in 2024 among leading peers.

- Intense rivalry with Moutai/Wuliangye (2024 revenues noted)

- Industry consolidation trimming smaller, inefficient players

- Fenjiu gains share in light-aroma segment (8–10% CAGR)

- Requires higher marketing/distribution spend (peers +12% capex/S&M 2024)

Interest rates and capital expenditure

As Fenjiu expands capacity and modernizes, prevailing interest rates—China's 1-year Loan Prime Rate at 3.45% and 5-year LPR at 3.95% (2025) — materially affect project feasibility and weighted average cost of capital for large CAPEX.

Strong operating cash flow (2024 net cash from operations: RMB 7.2bn) lowers debt dependence, yet PBOC monetary shifts still influence returns and discount rates used in investment appraisal.

Management prioritizes efficient capital allocation, targeting projects with ROIC above 12–15% to justify expansion and protect shareholder value amid rate volatility.

- Interest rates: LPR 1yr 3.45%, 5yr 3.95% (2025)

- 2024 operating cash flow: RMB 7.2bn

- Target ROIC for projects: 12–15%

Fenjiu rides consumption recovery and premiumization despite rising sorghum costs

Fenjiu benefits from 2024–25 consumption recovery: 2024 GDP +5.2%, household disposable income +6.7%; premiumization raised ASPs +12% and premium SKUs ~48% revenue (2024). Input shocks: sorghum +22% YoY, barley +15% (2024); long-term contracts cover ~60% sorghum, 45,000 mu planting. 2024 net cash from ops RMB 7.2bn; 1yr LPR 3.45%, 5yr 3.95% (2025).

| Metric | Value (year) |

|---|---|

| GDP growth | +5.2% (2024) |

| Disposable income | +6.7% (2024) |

| ASPs | +12% (2024) |

| Sorghum price | +22% YoY (2024) |

| Net OCF | RMB 7.2bn (2024) |

Preview Before You Purchase

Shanxi Xinghuacun Fen Wine Factory PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for Shanxi Xinghuacun Fen Wine Factory strategic review.