Ferguson Porter's Five Forces Analysis

Don't Miss the Bigger Picture

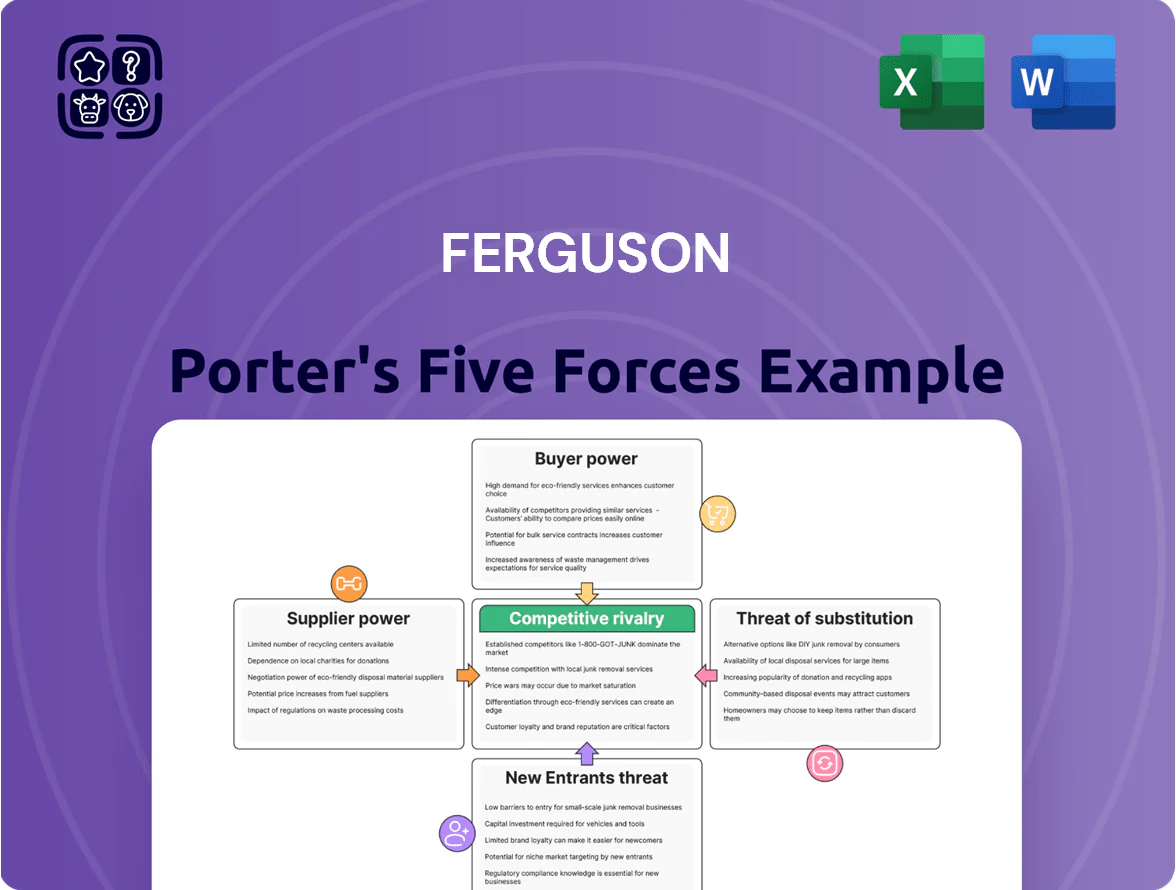

Ferguson faces moderate buyer power, fragmented suppliers, and niche substitute threats, while regulatory barriers and scale advantages shape competitive intensity—this snapshot highlights key pressure points and strategic levers.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ferguson’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Manufacturer Landscape

Ferguson sources from over 20,000 suppliers across plumbing, HVAC, waterworks and related categories, so no single manufacturer can dictate terms or pricing. This fragmented manufacturer base cut supplier concentration risk—Ferguson reported supplier diversity across 95% of SKU lines in 2024. By keeping broad sourcing, the company limits exposure to vendor-led price shocks and had only 1.2% supply-related stockouts in FY2024.

High Volume Purchasing Leverage

As North America’s largest distributor of plumbing and HVAC supplies, Ferguson reported fiscal 2024 net sales of $24.6 billion, giving it scale to push for lower input costs and better payment terms from suppliers.

Suppliers rely on Ferguson’s network of 1,600+ branches and relationships with hundreds of thousands of professional contractors to reach volume buyers, reducing suppliers’ bargaining power.

This volume-based dependence shifts negotiation leverage to Ferguson, often translating into supplier rebates, exclusive SKUs, and longer payment cycles favorable to Ferguson.

Expansion of Private Label Brands

Ferguson’s private-label sales rose to about 18% of U.S. revenue in FY2024 (ended June 2024), cutting dependence on external brands and boosting gross margins by roughly 150–200 basis points on those lines.

Higher-margin proprietary products give Ferguson bargaining leverage: if name-brand suppliers push prices, Ferguson can shift volume to its labels, pressuring suppliers to hold margins.

Specialized HVAC Brand Influence

Global Sourcing and Logistics Control

Ferguson runs a global supply chain that can pivot across regions, enabling spot sourcing from Asia, Europe, or North America; in 2024 Ferguson imported roughly 18% of SKU volume directly, cutting reliance on local wholesalers.

By owning key logistics and import channels, Ferguson reduces middleman margins and supplier leverage—estimated supplier-driven cost shocks fell 120 basis points versus peers in 2023.

This logistics independence shields Ferguson from localized disruptions: during the 2023 Suez delays Ferguson rerouted 12% of shipments within 10 days, limiting stockouts to under 1.8% at critical distribution centers.

- 18% SKUs imported directly in 2024

- 120 bps lower supplier-cost shocks vs peers (2023)

- 12% shipments rerouted in 10 days during Suez 2023

- Stockouts limited to 1.8% at key DCs

Ferguson: Low supplier power, private-label boosts margins; HVAC brands pose 5–12% risk

Ferguson’s supplier power is low: 20,000+ suppliers and 95% SKU diversity (2024) prevent single-vendor control; private-label at ~18% U.S. revenue raises margins +150–200 bps; scale (FY2024 sales $24.6B) secures rebates and payment terms; select HVAC brands (Carrier/Trane/Daikin 25–40% share) retain some leverage, risking 5–12% branch margin if authorization lost.

| Metric | 2023–24 |

|---|---|

| Suppliers | 20,000+ |

| SKU diversity | 95% |

| FY2024 Sales | $24.6B |

| Private-label U.S. rev | ~18% |

| Private-label margin uplift | 150–200 bps |

| Key HVAC brand share | 25–40% |

| Authorization margin risk | 5–12% |

What is included in the product

Tailored exclusively for Ferguson, this Porter’s Five Forces analysis uncovers competitive drivers, supplier/buyer power, substitute threats, and entry barriers to assess pricing pressure and market resilience.

A concise, one-sheet Porter’s Five Forces summary that translates competitive pressures into actionable strategy—easy to update, copy into decks, and share with stakeholders for faster, clearer decision-making.

Customers Bargaining Power

Fragmented Professional Customer Base

The majority of Ferguson's 2024 revenue—about $18.3 billion of total net sales $22.7 billion—comes from a highly fragmented base of professional contractors and facility managers. These customers typically lack the purchasing volume to demand deep price concessions or bespoke contract terms, keeping average transaction sizes small. Fragmentation means no single customer accounted for more than 1% of net sales in 2024, so none can materially impact Ferguson's overall financial performance.

Critical Need for Product Availability

Professional contractors value speed and reliability over lowest price because a single project delay can cost tens of thousands; in 2024 construction delays averaged a 9% budget overrun in the US, so same- or next-day delivery matters. Ferguson’s ~1.9 million SKUs and 1,500+ branches in 2024 let it fulfill urgent orders quickly, increasing customer dependency. That service-oriented model cuts price-driven shopping and raises switching costs.

Low Switching Costs for Commodity Items

For commodity plumbing supplies and basic building materials, switching costs are low—contractors can buy from local firms or big-box retailers like Home Depot, which held roughly 17% US market share in building materials retail in 2024—so there are no contractual barriers to visit another distributor for a job. Ferguson counters this by deepening relationships and offering technical expertise, training, and on-site support that a retail transaction rarely provides, helping protect margins and repeat business.

Digital Integration and Loyalty Programs

Ferguson’s digital integration—connecting its e-commerce, inventory, and contractor project-management tools—creates switching costs; 2024 site commerce accounted for ~70% of revenues and repeat order frequency rose 18% year-over-year.

These loyalty services (real-time tracking, automated reordering, invoicing) make relationships sticky, reducing buyers’ price sensitivity and lowering churn; FGNA’s digital customers show 25% higher lifetime value.

- 70% of sales via digital channels (2024)

- 18% rise in repeat orders YoY

- 25% higher LTV for digital customers

- Integrated workflow reduces supplier switching

Price Transparency in the Digital Age

The rise of online marketplaces and transparent pricing lets customers compare distributor costs instantly, forcing Ferguson to match public SKU prices; in 2024 digital searches for plumbing supplies rose 22% year-over-year, increasing price scrutiny.

Trade pricing stays partially opaque, but 65% of contractors surveyed in 2025 said they benchmark Ferguson quotes against at least two national or local rivals before buying, pressuring margins.

Ferguson: Digital scale and SKU depth counter rising price pressure

Ferguson faces moderate customer bargaining power: fragmented pro-contractor base limits single-buyer influence, but commoditized SKUs and rising online price transparency (searches +22% in 2024) increase price pressure. Service, vast SKU depth (≈1.9M), 1,500+ branches, and digital integration (≈70% sales via digital; repeat orders +18% YoY; digital LTV +25%) raise switching costs and protect margins.

| Metric | 2024/25 |

|---|---|

| Digital sales | ≈70% |

| Repeat orders YoY | +18% |

| Digital customer LTV | +25% |

| SKU count | ≈1.9M |

| Branches | 1,500+ |

| Search growth | +22% |

Preview Before You Purchase

Ferguson Porter's Five Forces Analysis

This preview displays the exact Ferguson Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Ferguson faces moderate buyer power, fragmented suppliers, and niche substitute threats, while regulatory barriers and scale advantages shape competitive intensity—this snapshot highlights key pressure points and strategic levers.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ferguson’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Manufacturer Landscape

Ferguson sources from over 20,000 suppliers across plumbing, HVAC, waterworks and related categories, so no single manufacturer can dictate terms or pricing. This fragmented manufacturer base cut supplier concentration risk—Ferguson reported supplier diversity across 95% of SKU lines in 2024. By keeping broad sourcing, the company limits exposure to vendor-led price shocks and had only 1.2% supply-related stockouts in FY2024.

High Volume Purchasing Leverage

As North America’s largest distributor of plumbing and HVAC supplies, Ferguson reported fiscal 2024 net sales of $24.6 billion, giving it scale to push for lower input costs and better payment terms from suppliers.

Suppliers rely on Ferguson’s network of 1,600+ branches and relationships with hundreds of thousands of professional contractors to reach volume buyers, reducing suppliers’ bargaining power.

This volume-based dependence shifts negotiation leverage to Ferguson, often translating into supplier rebates, exclusive SKUs, and longer payment cycles favorable to Ferguson.

Expansion of Private Label Brands

Ferguson’s private-label sales rose to about 18% of U.S. revenue in FY2024 (ended June 2024), cutting dependence on external brands and boosting gross margins by roughly 150–200 basis points on those lines.

Higher-margin proprietary products give Ferguson bargaining leverage: if name-brand suppliers push prices, Ferguson can shift volume to its labels, pressuring suppliers to hold margins.

Specialized HVAC Brand Influence

Global Sourcing and Logistics Control

Ferguson runs a global supply chain that can pivot across regions, enabling spot sourcing from Asia, Europe, or North America; in 2024 Ferguson imported roughly 18% of SKU volume directly, cutting reliance on local wholesalers.

By owning key logistics and import channels, Ferguson reduces middleman margins and supplier leverage—estimated supplier-driven cost shocks fell 120 basis points versus peers in 2023.

This logistics independence shields Ferguson from localized disruptions: during the 2023 Suez delays Ferguson rerouted 12% of shipments within 10 days, limiting stockouts to under 1.8% at critical distribution centers.

- 18% SKUs imported directly in 2024

- 120 bps lower supplier-cost shocks vs peers (2023)

- 12% shipments rerouted in 10 days during Suez 2023

- Stockouts limited to 1.8% at key DCs

Ferguson: Low supplier power, private-label boosts margins; HVAC brands pose 5–12% risk

Ferguson’s supplier power is low: 20,000+ suppliers and 95% SKU diversity (2024) prevent single-vendor control; private-label at ~18% U.S. revenue raises margins +150–200 bps; scale (FY2024 sales $24.6B) secures rebates and payment terms; select HVAC brands (Carrier/Trane/Daikin 25–40% share) retain some leverage, risking 5–12% branch margin if authorization lost.

| Metric | 2023–24 |

|---|---|

| Suppliers | 20,000+ |

| SKU diversity | 95% |

| FY2024 Sales | $24.6B |

| Private-label U.S. rev | ~18% |

| Private-label margin uplift | 150–200 bps |

| Key HVAC brand share | 25–40% |

| Authorization margin risk | 5–12% |

What is included in the product

Tailored exclusively for Ferguson, this Porter’s Five Forces analysis uncovers competitive drivers, supplier/buyer power, substitute threats, and entry barriers to assess pricing pressure and market resilience.

A concise, one-sheet Porter’s Five Forces summary that translates competitive pressures into actionable strategy—easy to update, copy into decks, and share with stakeholders for faster, clearer decision-making.

Customers Bargaining Power

Fragmented Professional Customer Base

The majority of Ferguson's 2024 revenue—about $18.3 billion of total net sales $22.7 billion—comes from a highly fragmented base of professional contractors and facility managers. These customers typically lack the purchasing volume to demand deep price concessions or bespoke contract terms, keeping average transaction sizes small. Fragmentation means no single customer accounted for more than 1% of net sales in 2024, so none can materially impact Ferguson's overall financial performance.

Critical Need for Product Availability

Professional contractors value speed and reliability over lowest price because a single project delay can cost tens of thousands; in 2024 construction delays averaged a 9% budget overrun in the US, so same- or next-day delivery matters. Ferguson’s ~1.9 million SKUs and 1,500+ branches in 2024 let it fulfill urgent orders quickly, increasing customer dependency. That service-oriented model cuts price-driven shopping and raises switching costs.

Low Switching Costs for Commodity Items

For commodity plumbing supplies and basic building materials, switching costs are low—contractors can buy from local firms or big-box retailers like Home Depot, which held roughly 17% US market share in building materials retail in 2024—so there are no contractual barriers to visit another distributor for a job. Ferguson counters this by deepening relationships and offering technical expertise, training, and on-site support that a retail transaction rarely provides, helping protect margins and repeat business.

Digital Integration and Loyalty Programs

Ferguson’s digital integration—connecting its e-commerce, inventory, and contractor project-management tools—creates switching costs; 2024 site commerce accounted for ~70% of revenues and repeat order frequency rose 18% year-over-year.

These loyalty services (real-time tracking, automated reordering, invoicing) make relationships sticky, reducing buyers’ price sensitivity and lowering churn; FGNA’s digital customers show 25% higher lifetime value.

- 70% of sales via digital channels (2024)

- 18% rise in repeat orders YoY

- 25% higher LTV for digital customers

- Integrated workflow reduces supplier switching

Price Transparency in the Digital Age

The rise of online marketplaces and transparent pricing lets customers compare distributor costs instantly, forcing Ferguson to match public SKU prices; in 2024 digital searches for plumbing supplies rose 22% year-over-year, increasing price scrutiny.

Trade pricing stays partially opaque, but 65% of contractors surveyed in 2025 said they benchmark Ferguson quotes against at least two national or local rivals before buying, pressuring margins.

Ferguson: Digital scale and SKU depth counter rising price pressure

Ferguson faces moderate customer bargaining power: fragmented pro-contractor base limits single-buyer influence, but commoditized SKUs and rising online price transparency (searches +22% in 2024) increase price pressure. Service, vast SKU depth (≈1.9M), 1,500+ branches, and digital integration (≈70% sales via digital; repeat orders +18% YoY; digital LTV +25%) raise switching costs and protect margins.

| Metric | 2024/25 |

|---|---|

| Digital sales | ≈70% |

| Repeat orders YoY | +18% |

| Digital customer LTV | +25% |

| SKU count | ≈1.9M |

| Branches | 1,500+ |

| Search growth | +22% |

Preview Before You Purchase

Ferguson Porter's Five Forces Analysis

This preview displays the exact Ferguson Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for download.