Ferrari Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

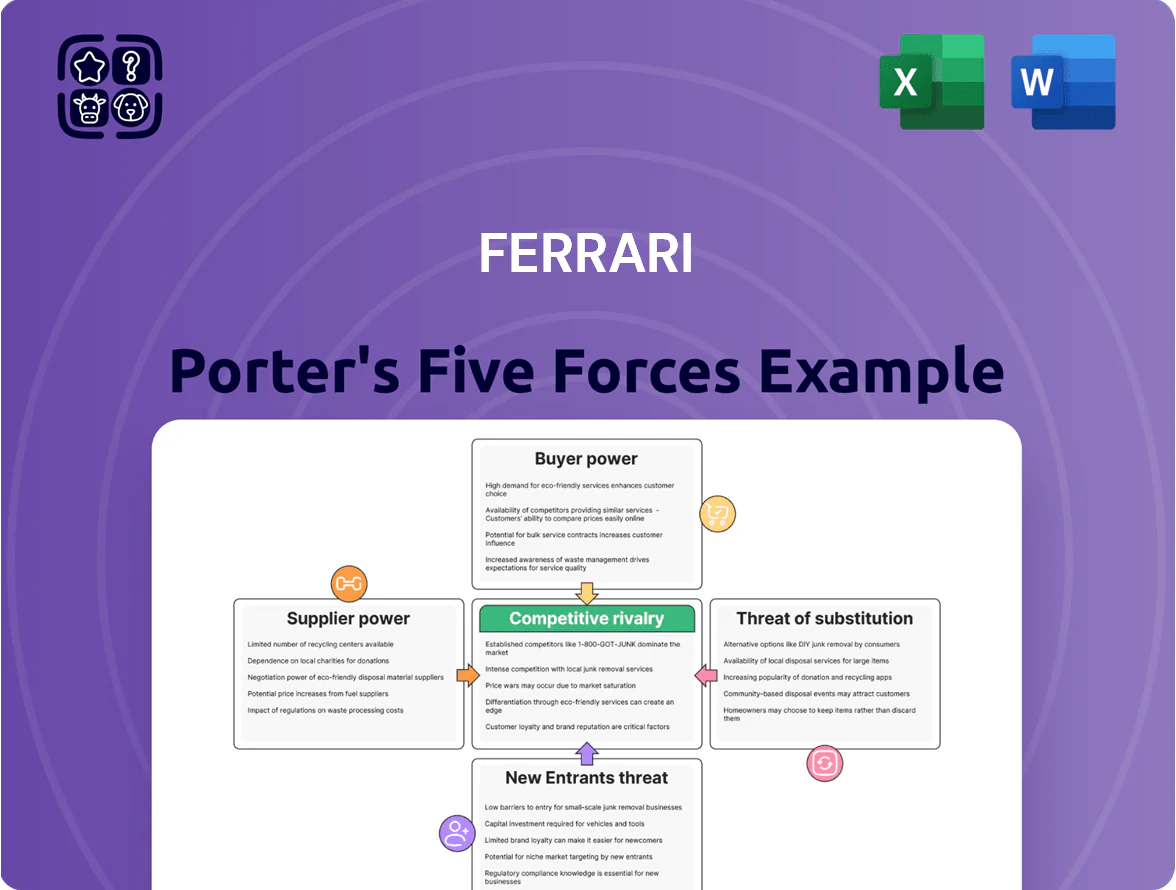

Ferrari operates in a niche luxury-performance segment where brand prestige, high switching costs, and limited substitute appeal strengthen its position, but regulatory pressures and technological shifts (EVs) raise competitive stakes.

Supplier concentration for specialized components and dealer dynamics influence margins, while customer power remains muted by affluent, brand-loyal buyers and constrained volume growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ferrari’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Core Components

Ferrari makes core components—engines and transaxles—in-house, producing over 90% of powertrain units at Maranello facilities, which cuts reliance on external vendors for tech-critical parts. This vertical integration centralizes IP and manufacturing know-how, lowering suppliers’ bargaining power for these systems. In 2024 Ferrari spent €1.1bn on R&D and maintained a gross margin of 45.7%, reflecting value capture from internally produced technology. That control lets Ferrari negotiate tougher terms with remaining suppliers.

Prestige and Brand Association

Suppliers view Ferrari partnership as a prestige endorsement that boosts their brand; 2024 data show Ferrari sourced €1.8bn in components, and many vendors cite Ferrari on marketing materials to win clients. This prestige gives Ferrari leverage in pricing and contract terms, with suppliers often accepting 5–15% lower margins to join the Ferrari ecosystem. That willingness lets Ferrari demand bespoke components and strict quality SLAs while keeping supplier costs down.

Specialized Raw Material Requirements

Ferrari needs high-grade inputs—carbon fiber, specialized aluminum alloys, and luxury leathers—mostly from a few niche suppliers, creating supplier power despite low annual volumes (Ferrari delivered 13,056 cars in 2024). Ferrari reduces risk via long-term contracts and co-development; for example, the firm reports supplier-related quality investments of €120m in 2024 to secure premium materials and continuity.

Transition to Electric Vehicle Components

Ferrari's late-2025 electrification adds battery-cell and power-electronics suppliers, who hold elevated leverage because few firms make high-performance cells for supercars; BloombergNEF cited 2025 supply constraints with high-nickel cells priced 15–25% above mainstream EV cells.

Ferrari counters by signing joint development deals—e.g., multi-year R&D partnerships covering cell chemistry and inverter design—to secure roadmap influence and cap unit costs, targeting a 10–15% battery cost reduction by 2028 per internal forecast.

- New specialist suppliers: higher bargaining power

- 2025 premium high-performance cells: +15–25% price

- Ferrari strategy: joint R&D deals, multi-year contracts

- Target battery cost cut: 10–15% by 2028

Geographic Concentration in Motor Valley

Geographic concentration in Italy’s Motor Valley—home to 60–70% of Ferrari’s tier-1 suppliers—creates a dense pool of artisans and engineers, enabling close collaboration and faster design cycles versus global sourcing.

Proximity cuts logistics and lead times; Ferrari reported supplier logistics savings of ~8% in 2024 versus a global benchmark, and many firms are specialized to Ferrari’s specs, limiting their bargaining leverage.

- 60–70% of tier-1 suppliers in Motor Valley

- ~8% reported logistics savings (2024)

- High supplier specialization reduces supplier bargaining power

Ferrari cuts supplier risk via 90% in‑house powertrains, €1.1bn R&D and supplier pacts

Ferrari’s vertical integration (90% powertrains), €1.1bn R&D (2024), and Motor Valley sourcing (60–70% tier‑1) reduce supplier power, but niche materials and 2025 high‑performance cells (+15–25% price) raise leverage; mitigants: long‑term contracts, €120m supplier investments (2024), and joint R&D aiming 10–15% battery cost cuts by 2028.

| Metric | Value |

|---|---|

| Powertrains in‑house | ≈90% |

| R&D (2024) | €1.1bn |

| Supplier spend (2024) | €1.8bn |

| Deliveries (2024) | 13,056 cars |

| Supplier investments (2024) | €120m |

What is included in the product

Concise Porter's Five Forces analysis tailored to Ferrari, revealing competitive pressures, customer and supplier power, entry barriers, and substitution threats that shape its pricing, profitability, and strategic resilience.

Compact Porter's Five Forces analysis for Ferrari—quickly spot threats from rivals, suppliers, buyers, substitutes, and entrants to inform strategic moves and investor decisions.

Customers Bargaining Power

Exclusivity and Controlled Scarcity

Ferrari caps annual production at about 10,000 cars (2024 guidance ~9,500) so demand outstrips supply, creating multi-year waiting lists and resale premiums often 20–50% above invoice; that scarcity erodes customer bargaining power.

High Brand Loyalty and Community

The Ferrari owner community shows extreme brand loyalty tied to Scuderia Ferrari racing history; as of FY2024 Ferrari reported roughly 60% repeat buyers and a 90% satisfaction rate among Maranello Club members, reflecting deep emotional ties.

Owners treat Ferrari as club membership, not just transport, so switching costs are psychological and social, reducing typical customer bargaining power versus rivals in the luxury sports-car market.

Bespoke Customization and Personalization

Ferrari’s Tailor Made program lets buyers create near-unique cars, driving personalization revenues that can add 10–25% to transaction price; in 2024 Ferrari reported €1.9 billion from ‘specialty’ cars and customization services, up 14% year-over-year. Once customers invest months and deposits in bespoke configs their purchase commitment becomes effectively irreversible, reducing price negotiation leverage. High-margin options lift gross margin—Ferrari’s 2024 adjusted EBIT margin was 28.6%—so customization dampens customer pressure on base prices.

Investment Value and Resale Strength

Many Ferrari models, including limited-run variants like the 250 GTO and modern icons such as the LaFerrari, have shown strong appreciation—collector 250 GTOs sold for over $48m in 2018 and limited modern Ferraris often outperform typical new-car depreciation, so buyers view them as appreciating assets.

This investment framing lets Ferrari set strict pricing and allocation terms with little pushback; strong auction and private-sale results (millions per unit) reinforce premium positioning and reduce customer leverage for discounts.

- Limited production boosts resale value

- High-net-worth buyers accept firm pricing

- Secondary market sales in 2024–25 remain robust

Fragmented Global Customer Base

Ferrari sells mainly to a fragmented, global pool of ultra-high-net-worth individuals, so no single customer or small group drives more than a tiny share of 2024 revenue (total 2024 group revenues €5.2bn; top-10 customers immaterial).

This dispersion prevents collective bargaining or pressure on pricing; buyers act as price-takers where exclusivity and brand cachet, not price discounts, motivate purchase.

- 2024 revenue €5.2bn; retail largely individualized

- No major customer concentration reported

- Ownership prestige > price sensitivity

Scarcity-driven pricing: 9,500-cap, €5.2bn rev, 60% repeat, 28.6% EBIT—buyers are price-takers

Scarcity, club-like loyalty, high personalization and strong resale lift reduce customer bargaining power; 2024 guidance ~9,500 units vs demand, 60% repeat buyers, €5.2bn revenue, €1.9bn customization sales, 28.6% adj. EBIT margin—buyers are price-takers.

| Metric | 2024 |

|---|---|

| Production cap | ~9,500 |

| Repeat buyers | 60% |

| Revenue | €5.2bn |

| Customization | €1.9bn |

| Adj. EBIT | 28.6% |

Preview the Actual Deliverable

Ferrari Porter's Five Forces Analysis

This preview shows the exact Ferrari Porter's Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

You're viewing the final, professionally written document that will be delivered to you instantly upon completion of payment, complete and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Ferrari operates in a niche luxury-performance segment where brand prestige, high switching costs, and limited substitute appeal strengthen its position, but regulatory pressures and technological shifts (EVs) raise competitive stakes.

Supplier concentration for specialized components and dealer dynamics influence margins, while customer power remains muted by affluent, brand-loyal buyers and constrained volume growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ferrari’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Core Components

Ferrari makes core components—engines and transaxles—in-house, producing over 90% of powertrain units at Maranello facilities, which cuts reliance on external vendors for tech-critical parts. This vertical integration centralizes IP and manufacturing know-how, lowering suppliers’ bargaining power for these systems. In 2024 Ferrari spent €1.1bn on R&D and maintained a gross margin of 45.7%, reflecting value capture from internally produced technology. That control lets Ferrari negotiate tougher terms with remaining suppliers.

Prestige and Brand Association

Suppliers view Ferrari partnership as a prestige endorsement that boosts their brand; 2024 data show Ferrari sourced €1.8bn in components, and many vendors cite Ferrari on marketing materials to win clients. This prestige gives Ferrari leverage in pricing and contract terms, with suppliers often accepting 5–15% lower margins to join the Ferrari ecosystem. That willingness lets Ferrari demand bespoke components and strict quality SLAs while keeping supplier costs down.

Specialized Raw Material Requirements

Ferrari needs high-grade inputs—carbon fiber, specialized aluminum alloys, and luxury leathers—mostly from a few niche suppliers, creating supplier power despite low annual volumes (Ferrari delivered 13,056 cars in 2024). Ferrari reduces risk via long-term contracts and co-development; for example, the firm reports supplier-related quality investments of €120m in 2024 to secure premium materials and continuity.

Transition to Electric Vehicle Components

Ferrari's late-2025 electrification adds battery-cell and power-electronics suppliers, who hold elevated leverage because few firms make high-performance cells for supercars; BloombergNEF cited 2025 supply constraints with high-nickel cells priced 15–25% above mainstream EV cells.

Ferrari counters by signing joint development deals—e.g., multi-year R&D partnerships covering cell chemistry and inverter design—to secure roadmap influence and cap unit costs, targeting a 10–15% battery cost reduction by 2028 per internal forecast.

- New specialist suppliers: higher bargaining power

- 2025 premium high-performance cells: +15–25% price

- Ferrari strategy: joint R&D deals, multi-year contracts

- Target battery cost cut: 10–15% by 2028

Geographic Concentration in Motor Valley

Geographic concentration in Italy’s Motor Valley—home to 60–70% of Ferrari’s tier-1 suppliers—creates a dense pool of artisans and engineers, enabling close collaboration and faster design cycles versus global sourcing.

Proximity cuts logistics and lead times; Ferrari reported supplier logistics savings of ~8% in 2024 versus a global benchmark, and many firms are specialized to Ferrari’s specs, limiting their bargaining leverage.

- 60–70% of tier-1 suppliers in Motor Valley

- ~8% reported logistics savings (2024)

- High supplier specialization reduces supplier bargaining power

Ferrari cuts supplier risk via 90% in‑house powertrains, €1.1bn R&D and supplier pacts

Ferrari’s vertical integration (90% powertrains), €1.1bn R&D (2024), and Motor Valley sourcing (60–70% tier‑1) reduce supplier power, but niche materials and 2025 high‑performance cells (+15–25% price) raise leverage; mitigants: long‑term contracts, €120m supplier investments (2024), and joint R&D aiming 10–15% battery cost cuts by 2028.

| Metric | Value |

|---|---|

| Powertrains in‑house | ≈90% |

| R&D (2024) | €1.1bn |

| Supplier spend (2024) | €1.8bn |

| Deliveries (2024) | 13,056 cars |

| Supplier investments (2024) | €120m |

What is included in the product

Concise Porter's Five Forces analysis tailored to Ferrari, revealing competitive pressures, customer and supplier power, entry barriers, and substitution threats that shape its pricing, profitability, and strategic resilience.

Compact Porter's Five Forces analysis for Ferrari—quickly spot threats from rivals, suppliers, buyers, substitutes, and entrants to inform strategic moves and investor decisions.

Customers Bargaining Power

Exclusivity and Controlled Scarcity

Ferrari caps annual production at about 10,000 cars (2024 guidance ~9,500) so demand outstrips supply, creating multi-year waiting lists and resale premiums often 20–50% above invoice; that scarcity erodes customer bargaining power.

High Brand Loyalty and Community

The Ferrari owner community shows extreme brand loyalty tied to Scuderia Ferrari racing history; as of FY2024 Ferrari reported roughly 60% repeat buyers and a 90% satisfaction rate among Maranello Club members, reflecting deep emotional ties.

Owners treat Ferrari as club membership, not just transport, so switching costs are psychological and social, reducing typical customer bargaining power versus rivals in the luxury sports-car market.

Bespoke Customization and Personalization

Ferrari’s Tailor Made program lets buyers create near-unique cars, driving personalization revenues that can add 10–25% to transaction price; in 2024 Ferrari reported €1.9 billion from ‘specialty’ cars and customization services, up 14% year-over-year. Once customers invest months and deposits in bespoke configs their purchase commitment becomes effectively irreversible, reducing price negotiation leverage. High-margin options lift gross margin—Ferrari’s 2024 adjusted EBIT margin was 28.6%—so customization dampens customer pressure on base prices.

Investment Value and Resale Strength

Many Ferrari models, including limited-run variants like the 250 GTO and modern icons such as the LaFerrari, have shown strong appreciation—collector 250 GTOs sold for over $48m in 2018 and limited modern Ferraris often outperform typical new-car depreciation, so buyers view them as appreciating assets.

This investment framing lets Ferrari set strict pricing and allocation terms with little pushback; strong auction and private-sale results (millions per unit) reinforce premium positioning and reduce customer leverage for discounts.

- Limited production boosts resale value

- High-net-worth buyers accept firm pricing

- Secondary market sales in 2024–25 remain robust

Fragmented Global Customer Base

Ferrari sells mainly to a fragmented, global pool of ultra-high-net-worth individuals, so no single customer or small group drives more than a tiny share of 2024 revenue (total 2024 group revenues €5.2bn; top-10 customers immaterial).

This dispersion prevents collective bargaining or pressure on pricing; buyers act as price-takers where exclusivity and brand cachet, not price discounts, motivate purchase.

- 2024 revenue €5.2bn; retail largely individualized

- No major customer concentration reported

- Ownership prestige > price sensitivity

Scarcity-driven pricing: 9,500-cap, €5.2bn rev, 60% repeat, 28.6% EBIT—buyers are price-takers

Scarcity, club-like loyalty, high personalization and strong resale lift reduce customer bargaining power; 2024 guidance ~9,500 units vs demand, 60% repeat buyers, €5.2bn revenue, €1.9bn customization sales, 28.6% adj. EBIT margin—buyers are price-takers.

| Metric | 2024 |

|---|---|

| Production cap | ~9,500 |

| Repeat buyers | 60% |

| Revenue | €5.2bn |

| Customization | €1.9bn |

| Adj. EBIT | 28.6% |

Preview the Actual Deliverable

Ferrari Porter's Five Forces Analysis

This preview shows the exact Ferrari Porter's Five Forces analysis you'll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

You're viewing the final, professionally written document that will be delivered to you instantly upon completion of payment, complete and ready for use.