Festo PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

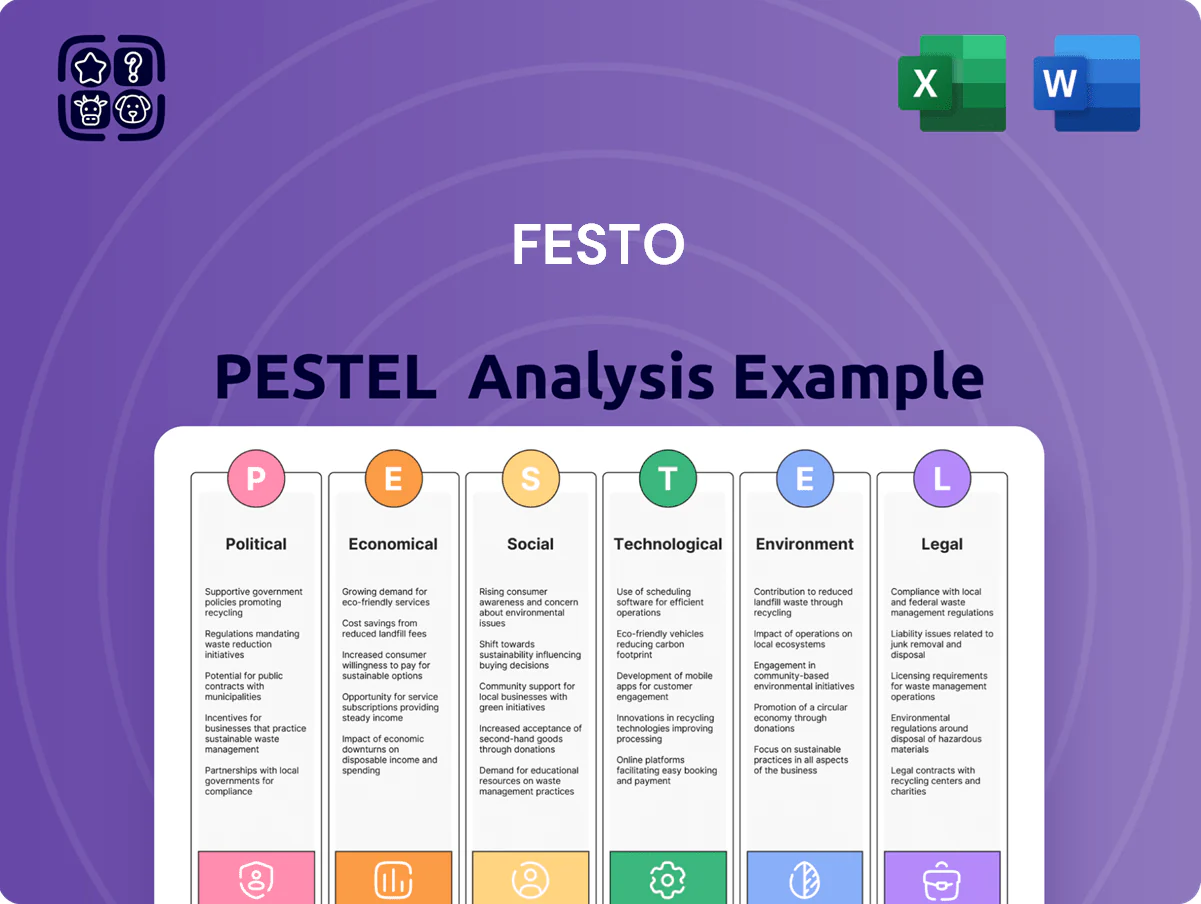

Unlock strategic advantage with our concise PESTLE Analysis of Festo—highlighting political, economic, social, technological, legal, and environmental forces that will shape its trajectory; ideal for investors, consultants, and managers. Purchase the full report to access actionable insights, editable charts, and risk/opportunity forecasts you can use immediately.

Political factors

Global Trade Policies and Tariffs

Trade tensions between the US, China and EU have raised average applied tariffs on industrial components by 1.8 percentage points since 2018, disrupting Festo’s global supply chain and increasing landed costs for pneumatic and electrical parts by an estimated 3–5% in 2023–24.

Fluctuating tariff regimes force Festo to keep a flexible manufacturing footprint; by 2024 the firm reported reallocating 12% of production capacity across regions to mitigate tariff exposure and logistics bottlenecks.

Strategic localization accelerated: by end‑2025 Festo aimed to localize production of 60% of pneumatic and electrical components in key markets, reducing tariff-related cost volatility and protecting margins against rising protectionism.

Government Subsidies for Digital Transformation

Geopolitical Stability and Supply Chain Resilience

Political instability in regions supplying 28% of Festo’s components can disrupt raw material and finished-goods flows, prompting diversification of suppliers across 12 countries to reduce single-source risk.

Regional conflicts and diplomatic shifts have previously delayed shipments by up to 14% in 2023, risking access to emerging markets where Festo recorded 18% of 2024 revenue, requiring proactive logistics rerouting and trade-compliance measures.

Strengthening regional headquarters—in 2024 Festo expanded 3 regional hubs—keeps the firm close to local decision-makers, improving responsiveness to regulatory changes and tailoring offerings to regional technical standards and procurement rules.

Export Controls on Dual-Use Technologies

- Dual-use expansion: robotics/AI now often regulated

- High penalties: tech export fines reached $2.3B (2023)

- Compliance costs: firms increased budgets 12–20% (2024)

- Action: licensing, screening, end‑use verification required

Regional Industrial Sovereignty Initiatives

- 27% of OECD/G20 states tightened procurement rules in 2024

- Festo APAC public-sector revenue +12% in 2024 from localization

- Festo Didactic trained 3,500 students across 22 countries in 2024

Tariffs, localization & compliance reshape supply chains—Industry 4.0 fuels digital spend

Trade tensions raised tariffs +1.8pp since 2018, increasing landed costs 3–5% (2023–24); Festo reallocated 12% capacity and targets 60% localization by 2025. €3.8bn Germany Industry 4.0 (2024) and 12% YoY digitalization investment growth expand demand; 28% supply exposure and export controls (Wassenaar, fines up to $2.3B) drive higher compliance spend (+12–20% in 2024).

| Metric | Value (year) |

|---|---|

| Tariff change | +1.8pp (since 2018) |

| Landed cost rise | 3–5% (2023–24) |

| Reallocated capacity | 12% (2024) |

| Localization target | 60% (2025) |

| Germany Industry 4.0 | €3.8bn (2024) |

| Digitalization investment | +12% YoY (2024) |

| Supply exposure | 28% |

| Compliance spend rise | +12–20% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Festo across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify specific threats and opportunities.

Concise, visually segmented PESTLE summary for Festo that you can drop into presentations or planning sessions to quickly align teams, highlight external risks and market positioning, and add context-specific notes for regional or business-line relevance.

Economic factors

Global Capital Expenditure Trends

The demand for Festo’s automation solutions tracks capex cycles in automotive and electronics, with global manufacturing capex falling 3.2% in 2023 but rebounding an estimated 4.5% in 2024, influencing order flow for pneumatic and electric drive systems.

Economic slowdowns in China and Europe in 2023 led many OEMs to defer production-line investments, contributing to Festo-like suppliers seeing mid-single-digit revenue dips; recovery phases historically drive sharp order increases.

Labor Shortages and Wage Inflation

Persistent global manufacturing labor shortages—OECD reports 2024 vacancy rates near record highs and the ILO estimates 2024 skilled labor gaps at ~20% in key markets—drive companies toward Festo automation as wages rise (manufacturing wages up 4–6% YoY in 2023–24 in US/EU) and skilled availability falls, turning automation from optional to essential and underpinning sustained demand for Festo’s products.

Energy Price Volatility in Industrial Markets

Rising European industrial energy prices—wholesale gas up ~60% in 2024 vs 2020 and industrial electricity averaging €0.18–0.22/kWh in 2024—compress margins and shift procurement toward energy-efficient automation.

Festo’s low-air-consumption pneumatic modules and electric drives reducing kWh per cycle offer a measurable advantage as buyers prioritize total cost of ownership; energy savings can cut operating costs by an estimated 10–25% depending on application.

Fluctuations in Raw Material Costs

Fluctuations in aluminum, steel and engineering plastics—aluminum prices rose ~18% in 2023 while steel HRC averaged +12% YoY—directly affect Festo’s component costs; raw materials account for an estimated 20–30% of manufacturing COGS in automation suppliers.

Maintaining price competitiveness and margins in a crowded industrial automation market requires tight input-cost control; a 5–10% commodity spike can erode margins materially.

Festo deploys sophisticated procurement (hedging, index-linked pricing) and long-term supplier contracts covering ~60–80% of volume to mitigate price spikes and stabilize input costs.

- Aluminum +18% (2023); steel +12% (2023)

- Raw materials ≈20–30% of COGS

- Hedging and contracts cover ~60–80% of volumes

Currency Exchange Rate Risks

As a global player in over 60 countries, Festo faces notable currency translation and transaction risks; FY2024 reported ~28% of revenues outside the eurozone, amplifying exposure to USD and CNY swings.

Euro volatility vs. the dollar or renminbi can erode export price competitiveness and alter reported international earnings—EUR/USD moved ~5.4% and EUR/CNY ~6.1% intrayear in 2024.

Festo uses hedging (forward contracts covering a significant portion of short-term exposures) and local production sites—over 70% of sales served from regional plants—to mitigate currency impacts and stabilize margins.

- 60+ countries footprint; ~28% non-eurozone revenue (FY2024)

- EUR/USD ~5.4% and EUR/CNY ~6.1% volatility in 2024

- Hedging via forwards; >70% regional production to reduce transaction risk

Capex Rebound Spurs Automation Demand as Costs, Labor Gaps Pressure Margins

Manufacturing capex rebounded ~4.5% in 2024, driving orders for Festo’s pneumatic/electric drives; labor shortages (ILO ~20% skilled gaps) and wage inflation (US/EU manufacturing wages +4–6% YoY) push automation demand; energy costs (industrial electricity €0.18–0.22/kWh in 2024) and raw-materials (Al +18%, Steel +12% in 2023) pressure margins; hedging/long-term contracts cover ~60–80% volumes and >70% regional production mitigate FX and input risks.

| Metric | Value |

|---|---|

| Manufacturing capex 2024 | +4.5% |

| Skilled labor gap | ~20% |

| Wage growth 2023–24 | +4–6% YoY |

| Industrial electricity 2024 | €0.18–0.22/kWh |

| Al/Steel 2023 | Al +18%, Steel +12% |

| Hedging/contract coverage | 60–80% |

| Regional production | >70% sales served locally |

Full Version Awaits

Festo PESTLE Analysis

The preview shown here is the exact Festo PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our concise PESTLE Analysis of Festo—highlighting political, economic, social, technological, legal, and environmental forces that will shape its trajectory; ideal for investors, consultants, and managers. Purchase the full report to access actionable insights, editable charts, and risk/opportunity forecasts you can use immediately.

Political factors

Global Trade Policies and Tariffs

Trade tensions between the US, China and EU have raised average applied tariffs on industrial components by 1.8 percentage points since 2018, disrupting Festo’s global supply chain and increasing landed costs for pneumatic and electrical parts by an estimated 3–5% in 2023–24.

Fluctuating tariff regimes force Festo to keep a flexible manufacturing footprint; by 2024 the firm reported reallocating 12% of production capacity across regions to mitigate tariff exposure and logistics bottlenecks.

Strategic localization accelerated: by end‑2025 Festo aimed to localize production of 60% of pneumatic and electrical components in key markets, reducing tariff-related cost volatility and protecting margins against rising protectionism.

Government Subsidies for Digital Transformation

Geopolitical Stability and Supply Chain Resilience

Political instability in regions supplying 28% of Festo’s components can disrupt raw material and finished-goods flows, prompting diversification of suppliers across 12 countries to reduce single-source risk.

Regional conflicts and diplomatic shifts have previously delayed shipments by up to 14% in 2023, risking access to emerging markets where Festo recorded 18% of 2024 revenue, requiring proactive logistics rerouting and trade-compliance measures.

Strengthening regional headquarters—in 2024 Festo expanded 3 regional hubs—keeps the firm close to local decision-makers, improving responsiveness to regulatory changes and tailoring offerings to regional technical standards and procurement rules.

Export Controls on Dual-Use Technologies

- Dual-use expansion: robotics/AI now often regulated

- High penalties: tech export fines reached $2.3B (2023)

- Compliance costs: firms increased budgets 12–20% (2024)

- Action: licensing, screening, end‑use verification required

Regional Industrial Sovereignty Initiatives

- 27% of OECD/G20 states tightened procurement rules in 2024

- Festo APAC public-sector revenue +12% in 2024 from localization

- Festo Didactic trained 3,500 students across 22 countries in 2024

Tariffs, localization & compliance reshape supply chains—Industry 4.0 fuels digital spend

Trade tensions raised tariffs +1.8pp since 2018, increasing landed costs 3–5% (2023–24); Festo reallocated 12% capacity and targets 60% localization by 2025. €3.8bn Germany Industry 4.0 (2024) and 12% YoY digitalization investment growth expand demand; 28% supply exposure and export controls (Wassenaar, fines up to $2.3B) drive higher compliance spend (+12–20% in 2024).

| Metric | Value (year) |

|---|---|

| Tariff change | +1.8pp (since 2018) |

| Landed cost rise | 3–5% (2023–24) |

| Reallocated capacity | 12% (2024) |

| Localization target | 60% (2025) |

| Germany Industry 4.0 | €3.8bn (2024) |

| Digitalization investment | +12% YoY (2024) |

| Supply exposure | 28% |

| Compliance spend rise | +12–20% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Festo across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify specific threats and opportunities.

Concise, visually segmented PESTLE summary for Festo that you can drop into presentations or planning sessions to quickly align teams, highlight external risks and market positioning, and add context-specific notes for regional or business-line relevance.

Economic factors

Global Capital Expenditure Trends

The demand for Festo’s automation solutions tracks capex cycles in automotive and electronics, with global manufacturing capex falling 3.2% in 2023 but rebounding an estimated 4.5% in 2024, influencing order flow for pneumatic and electric drive systems.

Economic slowdowns in China and Europe in 2023 led many OEMs to defer production-line investments, contributing to Festo-like suppliers seeing mid-single-digit revenue dips; recovery phases historically drive sharp order increases.

Labor Shortages and Wage Inflation

Persistent global manufacturing labor shortages—OECD reports 2024 vacancy rates near record highs and the ILO estimates 2024 skilled labor gaps at ~20% in key markets—drive companies toward Festo automation as wages rise (manufacturing wages up 4–6% YoY in 2023–24 in US/EU) and skilled availability falls, turning automation from optional to essential and underpinning sustained demand for Festo’s products.

Energy Price Volatility in Industrial Markets

Rising European industrial energy prices—wholesale gas up ~60% in 2024 vs 2020 and industrial electricity averaging €0.18–0.22/kWh in 2024—compress margins and shift procurement toward energy-efficient automation.

Festo’s low-air-consumption pneumatic modules and electric drives reducing kWh per cycle offer a measurable advantage as buyers prioritize total cost of ownership; energy savings can cut operating costs by an estimated 10–25% depending on application.

Fluctuations in Raw Material Costs

Fluctuations in aluminum, steel and engineering plastics—aluminum prices rose ~18% in 2023 while steel HRC averaged +12% YoY—directly affect Festo’s component costs; raw materials account for an estimated 20–30% of manufacturing COGS in automation suppliers.

Maintaining price competitiveness and margins in a crowded industrial automation market requires tight input-cost control; a 5–10% commodity spike can erode margins materially.

Festo deploys sophisticated procurement (hedging, index-linked pricing) and long-term supplier contracts covering ~60–80% of volume to mitigate price spikes and stabilize input costs.

- Aluminum +18% (2023); steel +12% (2023)

- Raw materials ≈20–30% of COGS

- Hedging and contracts cover ~60–80% of volumes

Currency Exchange Rate Risks

As a global player in over 60 countries, Festo faces notable currency translation and transaction risks; FY2024 reported ~28% of revenues outside the eurozone, amplifying exposure to USD and CNY swings.

Euro volatility vs. the dollar or renminbi can erode export price competitiveness and alter reported international earnings—EUR/USD moved ~5.4% and EUR/CNY ~6.1% intrayear in 2024.

Festo uses hedging (forward contracts covering a significant portion of short-term exposures) and local production sites—over 70% of sales served from regional plants—to mitigate currency impacts and stabilize margins.

- 60+ countries footprint; ~28% non-eurozone revenue (FY2024)

- EUR/USD ~5.4% and EUR/CNY ~6.1% volatility in 2024

- Hedging via forwards; >70% regional production to reduce transaction risk

Capex Rebound Spurs Automation Demand as Costs, Labor Gaps Pressure Margins

Manufacturing capex rebounded ~4.5% in 2024, driving orders for Festo’s pneumatic/electric drives; labor shortages (ILO ~20% skilled gaps) and wage inflation (US/EU manufacturing wages +4–6% YoY) push automation demand; energy costs (industrial electricity €0.18–0.22/kWh in 2024) and raw-materials (Al +18%, Steel +12% in 2023) pressure margins; hedging/long-term contracts cover ~60–80% volumes and >70% regional production mitigate FX and input risks.

| Metric | Value |

|---|---|

| Manufacturing capex 2024 | +4.5% |

| Skilled labor gap | ~20% |

| Wage growth 2023–24 | +4–6% YoY |

| Industrial electricity 2024 | €0.18–0.22/kWh |

| Al/Steel 2023 | Al +18%, Steel +12% |

| Hedging/contract coverage | 60–80% |

| Regional production | >70% sales served locally |

Full Version Awaits

Festo PESTLE Analysis

The preview shown here is the exact Festo PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.