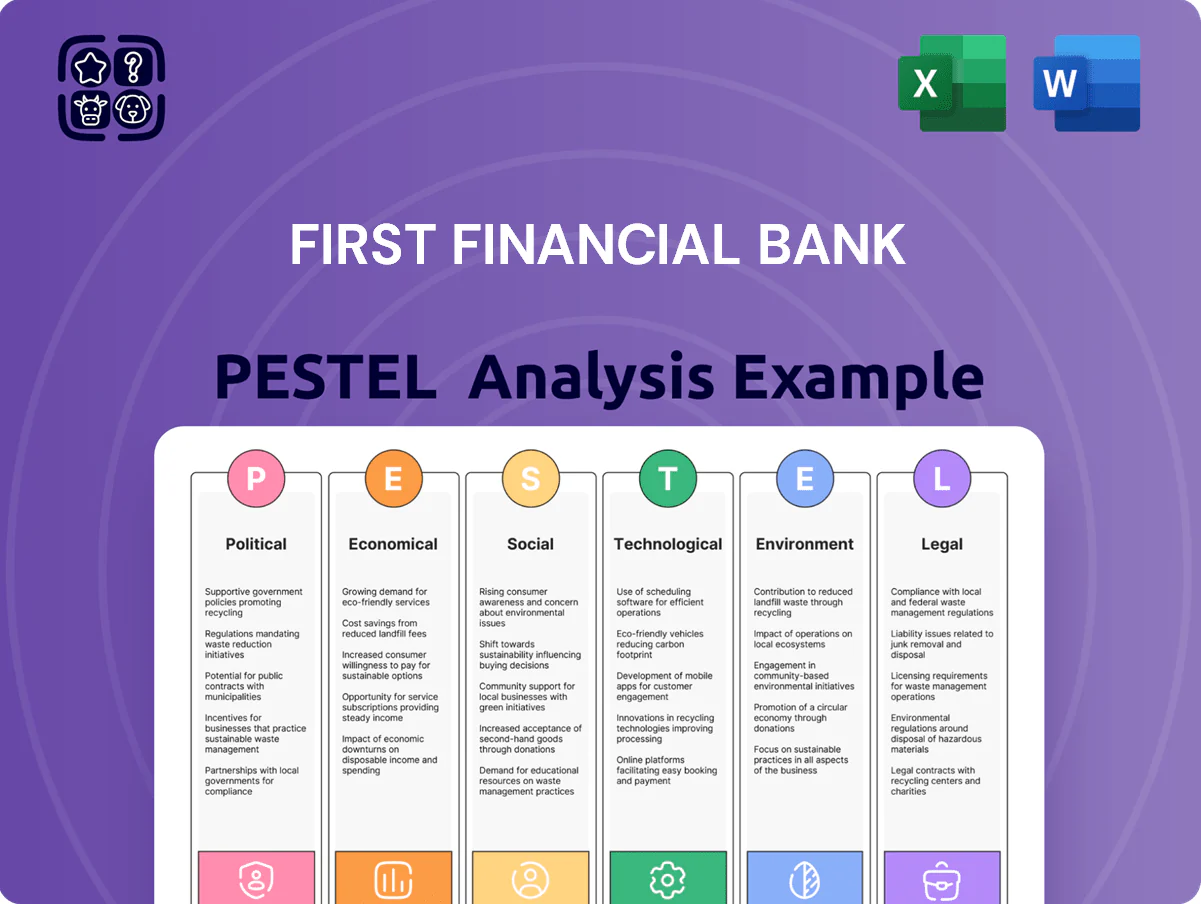

First Financial Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and tech disruption are shaping First Financial Bank’s strategic outlook in our concise PESTLE brief—perfect for investors and advisors who need immediate clarity. Purchase the full PESTLE Analysis to access detailed risk ratings, scenario impacts, and actionable recommendations you can use in reports and decision-making.

Political factors

Federal Reserve Monetary Policy Shifts

Entering 2026, First Financial Bank operates in a more stabilized rate environment after 2022–2024 volatility; the federal funds rate settled near 5.25%–5.50% in late 2025, supporting a modest rebound in NIMs (industry averages rose ~15–30 bps in 2025). Fed policy shifts directly alter loan demand and NIM, while political pressure to balance employment and 2% inflation targets remains a key planning risk.

Texas State Regulatory Environment

As a Texas-based institution, First Financial Bank benefits from the state's political stability and pro-business agenda, where Texas GDP grew 4.1% in 2024, supporting community banking expansion.

State-level deregulatory trends and incentives for corporate growth have aided regional loan origination—Texas commercial real estate lending rose 6.3% year-over-year in 2024.

However, Texas-specific mandates on financial disclosures and municipal lending—recently tightened for certain public funds in 2024—can increase compliance costs and shift competitive dynamics.

U.S. Trade Policies and Agriculture

Political shifts in U.S. trade deals and farm subsidies directly affect First Financial Bank's rural and commercial clients; Texas exported $338 billion in goods in 2023, so tariff changes can quickly alter revenues of agricultural and manufacturing borrowers.

Changes to subsidy programs (USDA outlays were about $45.5 billion in 2024) influence farm cash flow and loan performance, requiring the bank to reassess credit risk.

Rising geopolitical tensions that disrupted supply chains in 2022–24 pushed corn and soybean price volatility beyond 20%, so monitoring global risks is essential for portfolio resilience.

Government Spending and Infrastructure

Federal and Texas state allocations—Texas received about $22.3B from the 2021 Infrastructure Investment and Jobs Act and continues to tap ARPA/IIJA funds—create indirect opportunities for First Financial Bank to expand commercial lending and deposits tied to construction and contractor cash flows.

Political initiatives for rural broadband and energy (Texas broadband grants ~$1.6B 2022–24, expanding grid/clean energy investments) drive demand for localized banking services and project financing in underserved counties.

First Financial’s participation in public-private partnerships depends on political willingness for deficit spending and incentives; shifts in state budget priorities or federal appropriation timing can materially affect deal pipelines and credit exposure.

- Texas IIJA-related funding ~$22.3B — lending pipeline for construction/municipal projects

- Broadband grants ~$1.6B (2022–24) — localized deposit and SMB lending opportunities

- PPP participation tied to political appetite for deficit spending — impacts timing and volume of municipal financing

Taxation Policy Changes

Potential shifts in corporate tax rates after federal elections could change First Financial Bank's effective tax rate—raising it from 21% to, for example, 25% would cut after-tax net income by ~3.2% given 2024 pre-tax profit of $1.2B, forcing reallocation of capital and tighter ROE targets.

Altered tax incentives for real estate or small businesses (e.g., 10% reduced investment credits) would likely lower commercial mortgage and SBA loan originations from 2024 levels—originations fell 4.5% YoY when incentives were trimmed in prior cycles.

Management must stay agile, revising dividend payout (current yield ~2.1%) and reinvestment plans quickly to preserve capital and maintain Tier 1 CET1 ratio near 11.8% under shifting fiscal regimes.

- Higher corporate tax rates → lower net income, tighter capital allocation

- Reduced real estate/small business incentives → fewer loan applications, lower originations

- Need to adjust dividend policy and reinvestment to protect CET1 (~11.8%) and ROE

Stability, Fed Rates & Infrastructure Boost First Financial; Tax, Disclosure Risks Loom

Political stability in Texas, federal rate policy (fed funds ~5.25–5.50% late 2025) and IIJA/ARPA allocations (~$22.3B to TX) support First Financial’s commercial lending and deposits, while tighter state disclosure rules, potential federal tax rises (21%→25% would cut after-tax income ~3.2% on $1.2B pre-tax 2024) and farm subsidy shifts ($45.5B USDA 2024) raise compliance and credit risks.

| Factor | 2024–25 Data |

|---|---|

| Fed funds | 5.25–5.50% |

| TX IIJA | $22.3B |

| USDA outlays | $45.5B |

| Pre-tax profit (FFB 2024) | $1.2B |

What is included in the product

Explores how external macro-environmental factors uniquely affect First Financial Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific dynamics, and forward-looking insights to inform strategy, risk mitigation, and investor communications.

A concise, visually segmented PESTLE summary for First Financial Bank that’s easy to drop into presentations or strategy packs, helping teams quickly align on external risks, regulatory shifts, and market positioning while allowing for context-specific notes and on-the-go sharing.

Economic factors

Regional Economic Diversification

Texas has shifted from oil and gas toward tech and healthcare, with tech employment up 22% and healthcare employment up 14% statewide since 2015, stabilizing First Financial Bank’s risk profile.

Strong GDP growth in key markets—Fort Worth metro GDP +3.8% in 2024, Houston +3.2%, Abilene showing continued regional expansion—drives commercial and consumer banking demand.

Sector diversification reduces exposure to energy shocks, helping insulate the bank from localized downturns in any single industry.

Inflationary Trends and Cost of Living

Persistent inflation through 2025 eroded consumer purchasing power, with US CPI up ~3.4% year-over-year as of Dec 2025, pressuring deposit growth and fee income for First Financial Bank.

Rising labor costs and a ~6–8% increase in IT maintenance and cloud spend forced tighter expense management to protect efficiency ratios that hovered near mid-50s in 2024–25.

Inflation also affected collateral valuation for the bank's sizable real estate loan book; residential and commercial property price growth varied regionally, complicating LTV assessments and loss-given-default modeling.

Energy Market Volatility

Despite diversification, Texas remains sensitive to oil and gas swings; Brent fell ~45% in 2020 and energy prices still drove TX GDP volatility—energy & mining made up 7.5% of Texas GDP in 2023. First Financial Bank’s commercial portfolio has material exposure to energy services and secondary suppliers; a 30%+ price collapse historically raises charge-off risk, potentially lifting NPAs and reducing regional loan growth (Dallas Fed: energy-related bank losses spiked in 2015–16).

Labor Market Dynamics

Tight Texas labor markets lifted average wages 4.1% YoY in 2024, supporting deposit growth at First Financial Bank but raising personnel costs and compressing net interest margin.

Competition for skilled bankers and cybersecurity talent drives higher recruiting and retention spend; national vacancy rates for IT security roles hit 5.2% in 2024, pushing salaries above regional averages.

Scaling branch and digital operations hinges on local workforce availability across the bank’s Texas footprint; metropolitan areas show stronger talent supply than rural markets.

- Wage growth 4.1% YoY (Texas, 2024)

- IT security vacancy rate 5.2% (US, 2024)

- Higher staffing costs compress margins

- Talent concentrated in metros vs rural areas

Real Estate Market Stability

The bank’s heavy real estate lending ties its asset quality to property valuations and housing starts; Texas housing starts fell 6% in 2024 vs 2023, increasing sensitivity to price corrections.

High mortgage rates—30-year fixed averaged about 7.1% in late 2025—have damped residential loan demand, pressuring origination volumes.

Commercial RE occupancy in Texas slipped to ~88% in 2024, so monitoring oversupply and rent trends is vital to protect the balance sheet.

- Exposure tied to TX housing starts down 6% (2024)

- 30-year mortgage ~7.1% (late 2025)

- Commercial occupancy ~88% (2024)

TX tech-fueled loan growth offsets margin squeeze and housing risk

Economic tailwinds from TX tech/health growth (tech jobs +22% since 2015) and metro GDP gains (Fort Worth +3.8% 2024) bolster loan demand, while persistent inflation (CPI ~3.4% YoY Dec 2025), rising wages (+4.1% 2024) and higher IT costs compress margins; real estate exposure remains key risk with housing starts -6% (2024) and 30-yr mortgage ~7.1% (late 2025).

| Metric | Value |

|---|---|

| Tech jobs change | +22% since 2015 |

| Fort Worth GDP 2024 | +3.8% |

| CPI Dec 2025 | ~3.4% YoY |

| Wage growth 2024 | +4.1% YoY |

| Housing starts 2024 | -6% |

| 30-yr mortgage | ~7.1% (late 2025) |

What You See Is What You Get

First Financial Bank PESTLE Analysis

The preview shown here is the exact First Financial Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and tech disruption are shaping First Financial Bank’s strategic outlook in our concise PESTLE brief—perfect for investors and advisors who need immediate clarity. Purchase the full PESTLE Analysis to access detailed risk ratings, scenario impacts, and actionable recommendations you can use in reports and decision-making.

Political factors

Federal Reserve Monetary Policy Shifts

Entering 2026, First Financial Bank operates in a more stabilized rate environment after 2022–2024 volatility; the federal funds rate settled near 5.25%–5.50% in late 2025, supporting a modest rebound in NIMs (industry averages rose ~15–30 bps in 2025). Fed policy shifts directly alter loan demand and NIM, while political pressure to balance employment and 2% inflation targets remains a key planning risk.

Texas State Regulatory Environment

As a Texas-based institution, First Financial Bank benefits from the state's political stability and pro-business agenda, where Texas GDP grew 4.1% in 2024, supporting community banking expansion.

State-level deregulatory trends and incentives for corporate growth have aided regional loan origination—Texas commercial real estate lending rose 6.3% year-over-year in 2024.

However, Texas-specific mandates on financial disclosures and municipal lending—recently tightened for certain public funds in 2024—can increase compliance costs and shift competitive dynamics.

U.S. Trade Policies and Agriculture

Political shifts in U.S. trade deals and farm subsidies directly affect First Financial Bank's rural and commercial clients; Texas exported $338 billion in goods in 2023, so tariff changes can quickly alter revenues of agricultural and manufacturing borrowers.

Changes to subsidy programs (USDA outlays were about $45.5 billion in 2024) influence farm cash flow and loan performance, requiring the bank to reassess credit risk.

Rising geopolitical tensions that disrupted supply chains in 2022–24 pushed corn and soybean price volatility beyond 20%, so monitoring global risks is essential for portfolio resilience.

Government Spending and Infrastructure

Federal and Texas state allocations—Texas received about $22.3B from the 2021 Infrastructure Investment and Jobs Act and continues to tap ARPA/IIJA funds—create indirect opportunities for First Financial Bank to expand commercial lending and deposits tied to construction and contractor cash flows.

Political initiatives for rural broadband and energy (Texas broadband grants ~$1.6B 2022–24, expanding grid/clean energy investments) drive demand for localized banking services and project financing in underserved counties.

First Financial’s participation in public-private partnerships depends on political willingness for deficit spending and incentives; shifts in state budget priorities or federal appropriation timing can materially affect deal pipelines and credit exposure.

- Texas IIJA-related funding ~$22.3B — lending pipeline for construction/municipal projects

- Broadband grants ~$1.6B (2022–24) — localized deposit and SMB lending opportunities

- PPP participation tied to political appetite for deficit spending — impacts timing and volume of municipal financing

Taxation Policy Changes

Potential shifts in corporate tax rates after federal elections could change First Financial Bank's effective tax rate—raising it from 21% to, for example, 25% would cut after-tax net income by ~3.2% given 2024 pre-tax profit of $1.2B, forcing reallocation of capital and tighter ROE targets.

Altered tax incentives for real estate or small businesses (e.g., 10% reduced investment credits) would likely lower commercial mortgage and SBA loan originations from 2024 levels—originations fell 4.5% YoY when incentives were trimmed in prior cycles.

Management must stay agile, revising dividend payout (current yield ~2.1%) and reinvestment plans quickly to preserve capital and maintain Tier 1 CET1 ratio near 11.8% under shifting fiscal regimes.

- Higher corporate tax rates → lower net income, tighter capital allocation

- Reduced real estate/small business incentives → fewer loan applications, lower originations

- Need to adjust dividend policy and reinvestment to protect CET1 (~11.8%) and ROE

Stability, Fed Rates & Infrastructure Boost First Financial; Tax, Disclosure Risks Loom

Political stability in Texas, federal rate policy (fed funds ~5.25–5.50% late 2025) and IIJA/ARPA allocations (~$22.3B to TX) support First Financial’s commercial lending and deposits, while tighter state disclosure rules, potential federal tax rises (21%→25% would cut after-tax income ~3.2% on $1.2B pre-tax 2024) and farm subsidy shifts ($45.5B USDA 2024) raise compliance and credit risks.

| Factor | 2024–25 Data |

|---|---|

| Fed funds | 5.25–5.50% |

| TX IIJA | $22.3B |

| USDA outlays | $45.5B |

| Pre-tax profit (FFB 2024) | $1.2B |

What is included in the product

Explores how external macro-environmental factors uniquely affect First Financial Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific dynamics, and forward-looking insights to inform strategy, risk mitigation, and investor communications.

A concise, visually segmented PESTLE summary for First Financial Bank that’s easy to drop into presentations or strategy packs, helping teams quickly align on external risks, regulatory shifts, and market positioning while allowing for context-specific notes and on-the-go sharing.

Economic factors

Regional Economic Diversification

Texas has shifted from oil and gas toward tech and healthcare, with tech employment up 22% and healthcare employment up 14% statewide since 2015, stabilizing First Financial Bank’s risk profile.

Strong GDP growth in key markets—Fort Worth metro GDP +3.8% in 2024, Houston +3.2%, Abilene showing continued regional expansion—drives commercial and consumer banking demand.

Sector diversification reduces exposure to energy shocks, helping insulate the bank from localized downturns in any single industry.

Inflationary Trends and Cost of Living

Persistent inflation through 2025 eroded consumer purchasing power, with US CPI up ~3.4% year-over-year as of Dec 2025, pressuring deposit growth and fee income for First Financial Bank.

Rising labor costs and a ~6–8% increase in IT maintenance and cloud spend forced tighter expense management to protect efficiency ratios that hovered near mid-50s in 2024–25.

Inflation also affected collateral valuation for the bank's sizable real estate loan book; residential and commercial property price growth varied regionally, complicating LTV assessments and loss-given-default modeling.

Energy Market Volatility

Despite diversification, Texas remains sensitive to oil and gas swings; Brent fell ~45% in 2020 and energy prices still drove TX GDP volatility—energy & mining made up 7.5% of Texas GDP in 2023. First Financial Bank’s commercial portfolio has material exposure to energy services and secondary suppliers; a 30%+ price collapse historically raises charge-off risk, potentially lifting NPAs and reducing regional loan growth (Dallas Fed: energy-related bank losses spiked in 2015–16).

Labor Market Dynamics

Tight Texas labor markets lifted average wages 4.1% YoY in 2024, supporting deposit growth at First Financial Bank but raising personnel costs and compressing net interest margin.

Competition for skilled bankers and cybersecurity talent drives higher recruiting and retention spend; national vacancy rates for IT security roles hit 5.2% in 2024, pushing salaries above regional averages.

Scaling branch and digital operations hinges on local workforce availability across the bank’s Texas footprint; metropolitan areas show stronger talent supply than rural markets.

- Wage growth 4.1% YoY (Texas, 2024)

- IT security vacancy rate 5.2% (US, 2024)

- Higher staffing costs compress margins

- Talent concentrated in metros vs rural areas

Real Estate Market Stability

The bank’s heavy real estate lending ties its asset quality to property valuations and housing starts; Texas housing starts fell 6% in 2024 vs 2023, increasing sensitivity to price corrections.

High mortgage rates—30-year fixed averaged about 7.1% in late 2025—have damped residential loan demand, pressuring origination volumes.

Commercial RE occupancy in Texas slipped to ~88% in 2024, so monitoring oversupply and rent trends is vital to protect the balance sheet.

- Exposure tied to TX housing starts down 6% (2024)

- 30-year mortgage ~7.1% (late 2025)

- Commercial occupancy ~88% (2024)

TX tech-fueled loan growth offsets margin squeeze and housing risk

Economic tailwinds from TX tech/health growth (tech jobs +22% since 2015) and metro GDP gains (Fort Worth +3.8% 2024) bolster loan demand, while persistent inflation (CPI ~3.4% YoY Dec 2025), rising wages (+4.1% 2024) and higher IT costs compress margins; real estate exposure remains key risk with housing starts -6% (2024) and 30-yr mortgage ~7.1% (late 2025).

| Metric | Value |

|---|---|

| Tech jobs change | +22% since 2015 |

| Fort Worth GDP 2024 | +3.8% |

| CPI Dec 2025 | ~3.4% YoY |

| Wage growth 2024 | +4.1% YoY |

| Housing starts 2024 | -6% |

| 30-yr mortgage | ~7.1% (late 2025) |

What You See Is What You Get

First Financial Bank PESTLE Analysis

The preview shown here is the exact First Financial Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.