First Interstate Bank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis of First Interstate Bank—spot regulatory, economic, and technological forces shaping its future and seize actionable insights to refine your investment or strategy. This concise, expertly researched report saves you hours of work and is ready for boardrooms or pitch decks. Buy the full version now for the complete, editable breakdown and immediate download.

Political factors

Post-Election Regulatory Shifts

The 2024 post-election shift put consumer protection and bank oversight higher on the federal agenda, with CFPB and OCC leadership changes likely to tighten supervisory focus; regional banks like First Interstate saw compliance costs rise—estimated industry-wide by 7–12% in 2025 per Oliver Wyman projections.

Geopolitical Stability in Western Markets

Geopolitical tensions in 2025, including energy price volatility—Brent crude averaging ~$78/bbl YTD—raise input costs for First Interstate Bank clients in the Mountain West, increasing credit risk for energy-exposed loans. Political instability affecting global supply chains has pushed fertilizer and equipment prices up ~12% since 2023, pressuring agricultural margins and loan demand. The bank monitors federal trade policies and tariffs that could cut regional ag export volumes—US agricultural exports were $188.5B in 2024—potentially impacting commercial credit quality.

State-Level Legislative Influence

Operating across 10 Western states, First Interstate must navigate divergent state political climates and legislative agendas that affect compliance and branch strategy.

Shifts in state tax codes and incentive programs—e.g., recent 2024 business tax changes in Arizona reducing credits by 12%—can alter community bank profitability and customer acquisition costs.

Movements toward state-chartered public banks in Oregon and California create a localized competitive threat; Oregon’s 2025 proposals target $2–3B in public deposits.

Federal Fiscal Policy Direction

Political decisions on federal spending and the 2025 debt ceiling standoffs drive market confidence and raised 10-year Treasury yields to about 4.3% in Jan 2025, directly affecting First Interstate’s securities valuation and funding costs.

As a holder of sizable securities portfolios, First Interstate is exposed to Washington brinkmanship that can shift fed funds expectations; implied 1-year OIS rates moved 75 bps during 2024–25 turbulence.

Annual appropriations determine SBA and other government-backed lending capacity—SBA loan volumes grew ~12% in 2024, meaning changes in appropriations materially affect originations and credit support.

- 10‑yr Treasury ~4.3% (Jan 2025)

- OIS volatility ~75 bps (2024–25)

- SBA loan volume +12% (2024)

Community Reinvestment Act Modernization

- Increased capital/staff for underserved lending

- Mid-2020s rules: stricter documentation and 5–8% community loan growth targets

- Noncompliance can delay/restrict M&A approvals; review times up ~20%

Regulatory Tightening, Energy Volatility Raise Compliance and Credit Risks for First Interstate

Federal regulatory tightening post-2024 elevates compliance costs (industry +7–12% est. 2025) and CRA enforcement demands 5–8% community loan growth; geopolitical energy volatility (Brent ~$78/bbl YTD 2025) and 10‑yr Treasury ~4.3% (Jan 2025) increase credit and market risk across First Interstate’s Mountain West footprint.

| Metric | Value |

|---|---|

| Compliance cost change (est.) | +7–12% (2025) |

| CRA community loan target | 5–8% annual |

| Brent crude | ~$78/bbl (YTD 2025) |

| 10‑yr Treasury | ~4.3% (Jan 2025) |

What is included in the product

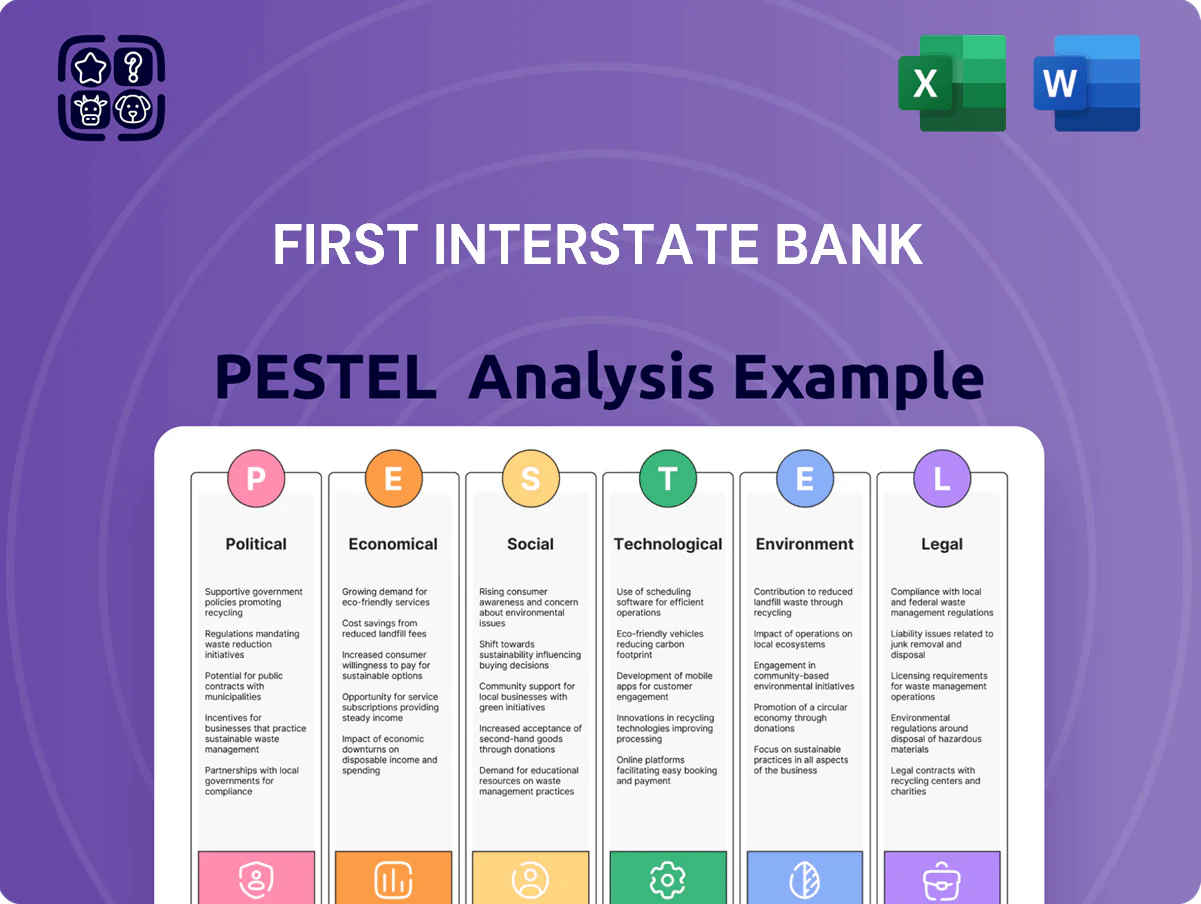

Explores how external macro-environmental factors uniquely affect First Interstate Bank across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region-specific data and trends to reveal actionable risks and opportunities.

A concise, visually segmented PESTLE summary for First Interstate Bank that highlights regulatory, economic, and technological impacts for quick reference during meetings or presentations.

Economic factors

Interest Rate Environment Stabilization

Following late-2025 stabilization after aggressive Fed hikes, regional bank net interest margins rebounded to ~3.25% in 2024 from 2.45% in 2022; First Interstate must now manage deposit costs (national average savings rate ~0.50% vs. Jumbo CDs ~3.5% in 2024) against loan yields (regional CRE loan yields ~6.2% in 2024) to protect profits.

Regional Economic Diversification

The Western US economies—notably Montana, Wyoming and Idaho—remain concentrated in agriculture, tourism and energy; for example, agriculture and mining accounted for roughly 8–12% of these states’ GDP in 2023, making First Interstate Bank’s NPLs and deposit flows sensitive to commodity cycles. Regional droughts and a 2022–23 softening in energy prices contributed to elevated ag-related delinquencies, while FY2024 saw the bank’s regional loan growth moderate versus national averages. Expansion into tech hubs and fast-growing urban centers in the Intermountain West, where metro employment grew 2.5–3.5% in 2024, helps diversify credit risk and stabilizes deposits against localized commodity price shocks.

Inflationary Pressures on Operating Costs

Persistent inflation through 2025 pushed First Interstate Bank's operating expenses up about 6-8% year-over-year, driven by a 7.5% rise in labor costs and higher branch maintenance outlays; this contributed to a reported efficiency ratio near 60% in 2024. Talent acquisition costs rose as industry median compensation increased ~6% in 2024, squeezing margins. The bank is accelerating digital investments to automate processes and curb human-capital and overhead growth.

Consumer Debt and Credit Quality

Economic shifts reducing household disposable income pressure First Interstate Bank’s consumer loan and mortgage portfolios; U.S. real disposable personal income fell 1.2% annualized in Q4 2025, tightening borrower capacity.

Rising delinquency rates—U.S. credit card delinquency rose to 4.6% in Q4 2025—signal heightened credit risk, prompting closer monitoring by risk teams.

First Interstate maintains conservative underwriting and low loan-to-value practices; its consumer delinquency ratio remained below the national average at 2.1% as of Dec 2025, supporting resilience.

- Q4 2025 U.S. real disposable income -1.2% annualized

- Q4 2025 U.S. credit card delinquency 4.6%

- First Interstate consumer delinquency 2.1% (Dec 2025)

Housing Market Dynamics

- Median home price Pacific ~$590,000 (2025 Q4)

- Mortgage transactions down ~10–15% YoY after rate hikes

- Office loans ~12% of CRE exposure

- Supply constraints sustain price resilience

Rate normalization lifts NIM to ~3.25% as deposit costs, CRE yields and consumer stress squeeze margins

Rate normalization lifted NIM to ~3.25% in 2024 while deposit costs (savings ~0.50% vs. jumbo CDs ~3.5% in 2024) and CRE yields (~6.2%) drive margin decisions; regional commodity exposure (ag/mining 8–12% GDP) raises asset volatility. Inflation pushed operating expenses +6–8% (efficiency ~60%); consumer stress (real DPI -1.2% Q4 2025) and higher delinquencies (card 4.6% vs FIB 2.1%) increase credit monitoring.

| Metric | Value |

|---|---|

| NIM (2024) | ~3.25% |

| Savings rate (2024) | ~0.50% |

| Jumbo CDs (2024) | ~3.5% |

| CRE yield (2024) | ~6.2% |

| Efficiency ratio (2024) | ~60% |

| Real DPI Q4 2025 | -1.2% |

| Card delinquency Q4 2025 | 4.6% |

| FIB consumer delinquency Dec 2025 | 2.1% |

Preview the Actual Deliverable

First Interstate Bank PESTLE Analysis

The preview shown here is the exact First Interstate Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, final document available for immediate download after payment.

The layout, content, and structure visible in the preview are identical to the file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis of First Interstate Bank—spot regulatory, economic, and technological forces shaping its future and seize actionable insights to refine your investment or strategy. This concise, expertly researched report saves you hours of work and is ready for boardrooms or pitch decks. Buy the full version now for the complete, editable breakdown and immediate download.

Political factors

Post-Election Regulatory Shifts

The 2024 post-election shift put consumer protection and bank oversight higher on the federal agenda, with CFPB and OCC leadership changes likely to tighten supervisory focus; regional banks like First Interstate saw compliance costs rise—estimated industry-wide by 7–12% in 2025 per Oliver Wyman projections.

Geopolitical Stability in Western Markets

Geopolitical tensions in 2025, including energy price volatility—Brent crude averaging ~$78/bbl YTD—raise input costs for First Interstate Bank clients in the Mountain West, increasing credit risk for energy-exposed loans. Political instability affecting global supply chains has pushed fertilizer and equipment prices up ~12% since 2023, pressuring agricultural margins and loan demand. The bank monitors federal trade policies and tariffs that could cut regional ag export volumes—US agricultural exports were $188.5B in 2024—potentially impacting commercial credit quality.

State-Level Legislative Influence

Operating across 10 Western states, First Interstate must navigate divergent state political climates and legislative agendas that affect compliance and branch strategy.

Shifts in state tax codes and incentive programs—e.g., recent 2024 business tax changes in Arizona reducing credits by 12%—can alter community bank profitability and customer acquisition costs.

Movements toward state-chartered public banks in Oregon and California create a localized competitive threat; Oregon’s 2025 proposals target $2–3B in public deposits.

Federal Fiscal Policy Direction

Political decisions on federal spending and the 2025 debt ceiling standoffs drive market confidence and raised 10-year Treasury yields to about 4.3% in Jan 2025, directly affecting First Interstate’s securities valuation and funding costs.

As a holder of sizable securities portfolios, First Interstate is exposed to Washington brinkmanship that can shift fed funds expectations; implied 1-year OIS rates moved 75 bps during 2024–25 turbulence.

Annual appropriations determine SBA and other government-backed lending capacity—SBA loan volumes grew ~12% in 2024, meaning changes in appropriations materially affect originations and credit support.

- 10‑yr Treasury ~4.3% (Jan 2025)

- OIS volatility ~75 bps (2024–25)

- SBA loan volume +12% (2024)

Community Reinvestment Act Modernization

- Increased capital/staff for underserved lending

- Mid-2020s rules: stricter documentation and 5–8% community loan growth targets

- Noncompliance can delay/restrict M&A approvals; review times up ~20%

Regulatory Tightening, Energy Volatility Raise Compliance and Credit Risks for First Interstate

Federal regulatory tightening post-2024 elevates compliance costs (industry +7–12% est. 2025) and CRA enforcement demands 5–8% community loan growth; geopolitical energy volatility (Brent ~$78/bbl YTD 2025) and 10‑yr Treasury ~4.3% (Jan 2025) increase credit and market risk across First Interstate’s Mountain West footprint.

| Metric | Value |

|---|---|

| Compliance cost change (est.) | +7–12% (2025) |

| CRA community loan target | 5–8% annual |

| Brent crude | ~$78/bbl (YTD 2025) |

| 10‑yr Treasury | ~4.3% (Jan 2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect First Interstate Bank across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region-specific data and trends to reveal actionable risks and opportunities.

A concise, visually segmented PESTLE summary for First Interstate Bank that highlights regulatory, economic, and technological impacts for quick reference during meetings or presentations.

Economic factors

Interest Rate Environment Stabilization

Following late-2025 stabilization after aggressive Fed hikes, regional bank net interest margins rebounded to ~3.25% in 2024 from 2.45% in 2022; First Interstate must now manage deposit costs (national average savings rate ~0.50% vs. Jumbo CDs ~3.5% in 2024) against loan yields (regional CRE loan yields ~6.2% in 2024) to protect profits.

Regional Economic Diversification

The Western US economies—notably Montana, Wyoming and Idaho—remain concentrated in agriculture, tourism and energy; for example, agriculture and mining accounted for roughly 8–12% of these states’ GDP in 2023, making First Interstate Bank’s NPLs and deposit flows sensitive to commodity cycles. Regional droughts and a 2022–23 softening in energy prices contributed to elevated ag-related delinquencies, while FY2024 saw the bank’s regional loan growth moderate versus national averages. Expansion into tech hubs and fast-growing urban centers in the Intermountain West, where metro employment grew 2.5–3.5% in 2024, helps diversify credit risk and stabilizes deposits against localized commodity price shocks.

Inflationary Pressures on Operating Costs

Persistent inflation through 2025 pushed First Interstate Bank's operating expenses up about 6-8% year-over-year, driven by a 7.5% rise in labor costs and higher branch maintenance outlays; this contributed to a reported efficiency ratio near 60% in 2024. Talent acquisition costs rose as industry median compensation increased ~6% in 2024, squeezing margins. The bank is accelerating digital investments to automate processes and curb human-capital and overhead growth.

Consumer Debt and Credit Quality

Economic shifts reducing household disposable income pressure First Interstate Bank’s consumer loan and mortgage portfolios; U.S. real disposable personal income fell 1.2% annualized in Q4 2025, tightening borrower capacity.

Rising delinquency rates—U.S. credit card delinquency rose to 4.6% in Q4 2025—signal heightened credit risk, prompting closer monitoring by risk teams.

First Interstate maintains conservative underwriting and low loan-to-value practices; its consumer delinquency ratio remained below the national average at 2.1% as of Dec 2025, supporting resilience.

- Q4 2025 U.S. real disposable income -1.2% annualized

- Q4 2025 U.S. credit card delinquency 4.6%

- First Interstate consumer delinquency 2.1% (Dec 2025)

Housing Market Dynamics

- Median home price Pacific ~$590,000 (2025 Q4)

- Mortgage transactions down ~10–15% YoY after rate hikes

- Office loans ~12% of CRE exposure

- Supply constraints sustain price resilience

Rate normalization lifts NIM to ~3.25% as deposit costs, CRE yields and consumer stress squeeze margins

Rate normalization lifted NIM to ~3.25% in 2024 while deposit costs (savings ~0.50% vs. jumbo CDs ~3.5% in 2024) and CRE yields (~6.2%) drive margin decisions; regional commodity exposure (ag/mining 8–12% GDP) raises asset volatility. Inflation pushed operating expenses +6–8% (efficiency ~60%); consumer stress (real DPI -1.2% Q4 2025) and higher delinquencies (card 4.6% vs FIB 2.1%) increase credit monitoring.

| Metric | Value |

|---|---|

| NIM (2024) | ~3.25% |

| Savings rate (2024) | ~0.50% |

| Jumbo CDs (2024) | ~3.5% |

| CRE yield (2024) | ~6.2% |

| Efficiency ratio (2024) | ~60% |

| Real DPI Q4 2025 | -1.2% |

| Card delinquency Q4 2025 | 4.6% |

| FIB consumer delinquency Dec 2025 | 2.1% |

Preview the Actual Deliverable

First Interstate Bank PESTLE Analysis

The preview shown here is the exact First Interstate Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, final document available for immediate download after payment.

The layout, content, and structure visible in the preview are identical to the file you’ll own upon checkout.