Fair Isaac Boston Consulting Group Matrix

See the Bigger Picture

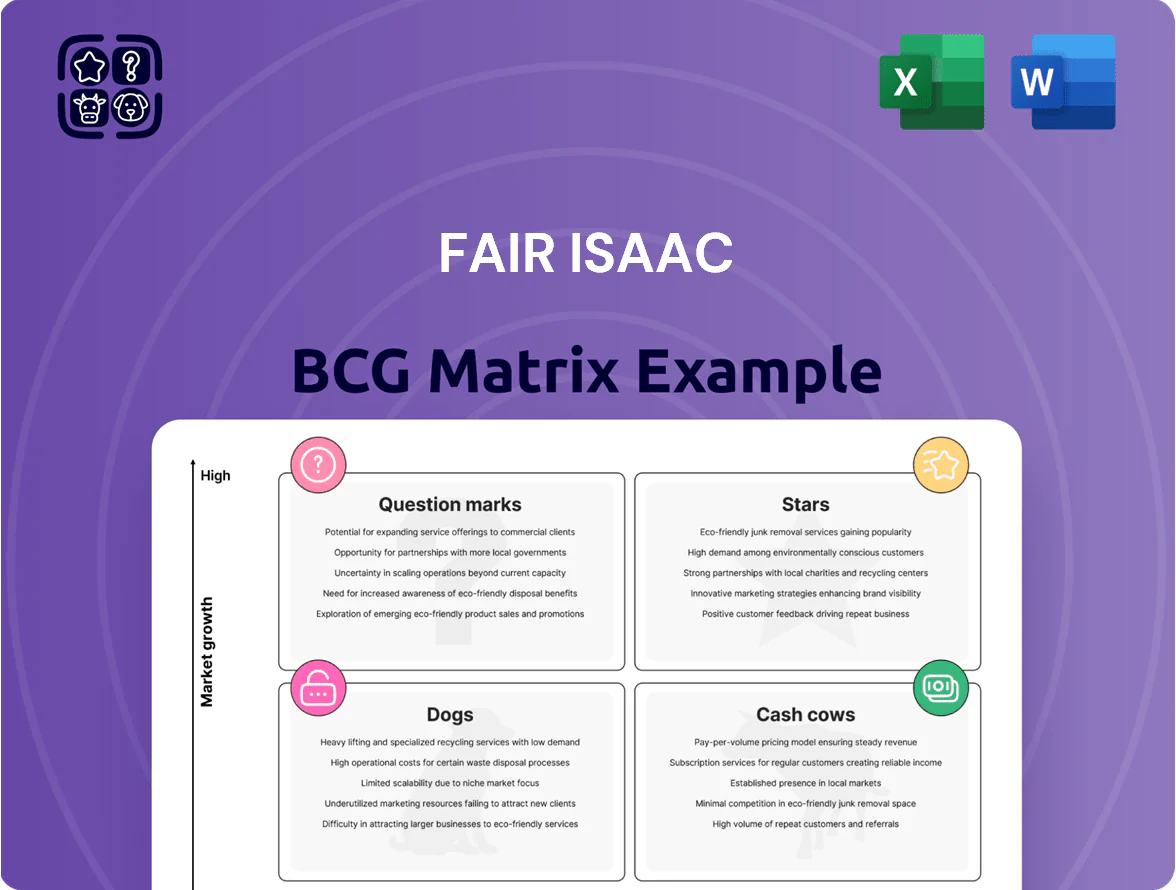

Fair Isaac’s BCG Matrix snapshot highlights how its product portfolio balances growth potential and cash generation—spotting Stars, Cash Cows, Question Marks, and Dogs at a glance while pointing to where strategic focus and capital should flow. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a comprehensive, data-driven breakdown, actionable recommendations, and downloadable Word and Excel deliverables to inform investment, product, and resource-allocation decisions.

Stars

FICO Platform Cloud Solutions

The FICO Platform Cloud Solutions is the primary growth driver as banks and lenders shift decisioning to cloud; cloud decisioning market projected at $18.6B in 2025 with FICO holding ~22% share in decisioning software per 2025 IDC estimates.

It captures high market share in digital transformation by offering a unified data and analytics environment, processing >1 trillion transaction events monthly across clients.

High R&D spend—FICO invested $220M in 2024—keeps it ahead of cloud-native rivals, while platform scalability sustains its market-leader position.

Falcon Fraud Manager

Falcon Fraud Manager is the industry standard for real-time payment fraud detection, protecting over 2.5 billion accounts and blocking an estimated $12.4 billion in fraudulent losses annually as of 2025.

With instant payments volume growing ~18% CAGR through 2028, real-time security demand is rising fast, keeping Falcon in the Stars quadrant of the BCG matrix.

FICO holds a dominant share (~35% global market for real-time payment fraud platforms), using ML models that detect fraud in milliseconds to prevent crime before it occurs.

To sustain growth and repel specialized AI cybersecurity startups, FICO needs continued marketing spend and R&D; analysts recommend 12–15% of Falcon revenue reinvested into product and go-to-market support.

Enterprise AI and Machine Learning Models

FICO has embedded advanced AI/ML across its scoring and decisioning products, driving leadership in a predictive analytics market growing ~15% CAGR to $52B by 2025; these models power automated, high‑precision risk decisions used by ~90 of the top 100 US banks.

AI offerings yield strong revenue—FICO reported software revenue of $929M in FY2024—but require heavy R&D and cloud spend; ongoing investment and compliance work for AI transparency raise operating cash needs.

Given FICO’s market share, regulatory relationships, and recurring licensing, these AI models are positioned to shift from cash-intensive stars to durable profit centers as tech and rules stabilize by 2027–2028.

Emerging Market Scoring Initiatives

FICO is rapidly expanding scoring in India, Brazil, and Southeast Asia as financial inclusion brings ~200M new consumers into formal credit from 2019–2024; these regions could add ~10–15% revenue growth by 2026 if adoption mirrors historical entry rates.

FICO uses its global brand to capture share early, but localized rivals and regulatory compliance push upfront capex ~USD 50–150M per region; success is key to keeping its global credit-risk leadership.

- Target regions: India, Brazil, SEA

- New consumers 2019–2024: ~200M

- Potential revenue uplift by 2026: 10–15%

- Estimated capex per region: USD 50–150M

- Risk: local competitors, regulation

Decision Management Suite

The Decision Management Suite provides tools to design and deploy complex analytical apps and drives business process automation; FICO reported software revenue of $619m in 2024, with analytics and decisioning a core growth driver.

It holds a strong position in the enterprise market—FICO claims >40% share in decisioning for financial services and net promoter scores above 50—fueling high customer loyalty and recurring license revenue.

To keep star status, FICO is investing in UX and integrations: 2024 R&D spend was $126m and over 60 prebuilt connectors for cloud platforms were released to support large-scale deployments.

- Comprehensive decisioning tools

- Strong enterprise share (>40% in finance)

- High customer loyalty (NPS >50)

- 2024 revenue $619m; R&D $126m

- 60+ cloud connectors for integration

FICO: Fraud Fortress—$12.4B blocked, 2.5B accounts, cloud leader fueling growth

FICO stars: cloud decisioning (18.6B market 2025; FICO ~22% share), Falcon fraud (35% real-time payments share; protects 2.5B accounts; blocks $12.4B fraud annually), and Decision Management (2024 software rev $619M; >40% finance share; NPS >50); high R&D ($220M 2024) supports growth but requires 12–15% reinvestment to hold lead.

| Metric | Value |

|---|---|

| Cloud market 2025 | $18.6B |

| FICO cloud share | ~22% |

| Falcon accounts protected | 2.5B |

| Falcon blocked losses | $12.4B/yr |

| Real-time payments share | ~35% |

| Decisioning rev 2024 | $619M |

| R&D 2024 | $220M |

| Recommended reinvest | 12–15% of Falcon rev |

What is included in the product

Comprehensive BCG Matrix review detailing Stars, Cash Cows, Question Marks, and Dogs with strategic investment guidance.

One-page Fair Isaac BCG Matrix placing each product in a quadrant for clear portfolio decisions

Cash Cows

B2B Mortgage Credit Scoring

The FICO mortgage-credit-scoring business is a mature cash cow: FICO holds roughly 80%–90% share of US mortgage score use and enjoys high operating margins (mid-40s percent in 2024).

Mortgage growth is slow and cyclical, tied to interest rates and housing activity—US mortgage originations fell ~30% in 2023 vs 2021 peak—so revenue growth tracks macro cycles, not rapid adoption.

The segment generates large free cash flow with low incremental marketing/infrastructure spend, funding FICO’s cloud and AI R&D; mortgage-related EBITDA provided an estimated $400–600M annual cash cushion in 2024.

Consumer myFICO Services

The myFICO brand delivers direct-to-consumer credit monitoring and identity-theft protection in a mature US market; FICO reported Consumer segment revenue of $380M in 2024, driven by ~2.5M subscribers and high brand recognition.

Low customer-acquisition costs and strong retention produce steady subscription revenue and ~60–70% gross margins, making it a classic cash cow despite slower market growth vs. enterprise software.

Only incremental product updates and customer support are needed to sustain this reliable liquidity source for the parent company.

Credit Card Origination Scoring

FICO credit scores dominate card origination, holding roughly 60–70% market share among US issuers as of 2025, in a mature, low-growth lending market.

The segment is deeply embedded in the workflows of top banks—JPMorgan, Bank of America, Citigroup—driving high switching costs and stable renewals.

With core scoring developed, expenses center on maintenance, data security, and model governance; 2024 upkeep and security spend estimated at ~$120–150M.

Licensing and services generate predictable recurring revenue—FICO reported roughly $1.9B in 2024 analytics/licensing revenue—providing steady cash flow for planning.

Collections and Recovery Software

FICO Collections and Recovery is a mature, low-growth product that remains essential across cycles; FICO held roughly 30–40% share of global collections software in 2024, helping lenders lift recovery rates by 5–12 percentage points per program.

High client switching costs and 80–90% contract renewal rates create stable, profitable cash flows that fund riskier growth areas and R&D.

- Market share: ~30–40% (2024)

- Recovery lift: 5–12% per implementation

- Renewal rate: 80–90%

- Growth: low single digits annually

Auto Loan Risk Assessment

FICO’s auto-loan scoring underpins ~70% of US auto originations, using FICO scores to price millions of loans yearly; this mature, consolidated market gives FICO steady pricing power and low growth pressure as originations were ~16.5 million units in 2024, keeping share resilient.

Auto lending yields consistent revenue with low capex needs—segment margins exceed company average—and in 2024 cash flows funded high-growth bets across the FICO Platform, supporting analytics and SaaS expansion.

- High share: ~70% US auto origination reliance

- Mature market: 16.5M new vehicle sales (2024)

- Stable cash: low capex, above-average margins

- Funds growth: cash redeployed to SaaS/analytics

FICO’s High‑Margin Cash Cows Fuel SaaS/AI Growth: $1.9B Analytics, $400–600M Mortgage EBITDA

FICO’s Cash Cows: dominant mortgage and card scoring plus collections and auto scoring generate high-margin, recurring cash—mortgage EBITDA ~$400–600M (2024), analytics/licensing revenue $1.9B (2024), consumer revenue $380M (2024), retention 80–90%, gross margins 60–70%, upkeep ~$120–150M (2024); these low-growth, high-cash segments fund FICO’s SaaS/AI growth.

| Metric | 2024/2025 |

|---|---|

| Analytics/licensing rev | $1.9B (2024) |

| Mortgage EBITDA | $400–600M (2024) |

| Consumer rev | $380M (2024) |

| Gross margins | 60–70% |

| Upkeep/security spend | $120–150M (2024) |

What You’re Viewing Is Included

Fair Isaac BCG Matrix

The file you're previewing is the exact Fair Isaac BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This professional document, prepared by strategy experts, contains market-backed positioning, quadrant insights, and clear action recommendations for immediate use. Upon purchase you'll get the same editable, printable file delivered straight to your inbox—no surprises, no extra edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Fair Isaac’s BCG Matrix snapshot highlights how its product portfolio balances growth potential and cash generation—spotting Stars, Cash Cows, Question Marks, and Dogs at a glance while pointing to where strategic focus and capital should flow. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a comprehensive, data-driven breakdown, actionable recommendations, and downloadable Word and Excel deliverables to inform investment, product, and resource-allocation decisions.

Stars

FICO Platform Cloud Solutions

The FICO Platform Cloud Solutions is the primary growth driver as banks and lenders shift decisioning to cloud; cloud decisioning market projected at $18.6B in 2025 with FICO holding ~22% share in decisioning software per 2025 IDC estimates.

It captures high market share in digital transformation by offering a unified data and analytics environment, processing >1 trillion transaction events monthly across clients.

High R&D spend—FICO invested $220M in 2024—keeps it ahead of cloud-native rivals, while platform scalability sustains its market-leader position.

Falcon Fraud Manager

Falcon Fraud Manager is the industry standard for real-time payment fraud detection, protecting over 2.5 billion accounts and blocking an estimated $12.4 billion in fraudulent losses annually as of 2025.

With instant payments volume growing ~18% CAGR through 2028, real-time security demand is rising fast, keeping Falcon in the Stars quadrant of the BCG matrix.

FICO holds a dominant share (~35% global market for real-time payment fraud platforms), using ML models that detect fraud in milliseconds to prevent crime before it occurs.

To sustain growth and repel specialized AI cybersecurity startups, FICO needs continued marketing spend and R&D; analysts recommend 12–15% of Falcon revenue reinvested into product and go-to-market support.

Enterprise AI and Machine Learning Models

FICO has embedded advanced AI/ML across its scoring and decisioning products, driving leadership in a predictive analytics market growing ~15% CAGR to $52B by 2025; these models power automated, high‑precision risk decisions used by ~90 of the top 100 US banks.

AI offerings yield strong revenue—FICO reported software revenue of $929M in FY2024—but require heavy R&D and cloud spend; ongoing investment and compliance work for AI transparency raise operating cash needs.

Given FICO’s market share, regulatory relationships, and recurring licensing, these AI models are positioned to shift from cash-intensive stars to durable profit centers as tech and rules stabilize by 2027–2028.

Emerging Market Scoring Initiatives

FICO is rapidly expanding scoring in India, Brazil, and Southeast Asia as financial inclusion brings ~200M new consumers into formal credit from 2019–2024; these regions could add ~10–15% revenue growth by 2026 if adoption mirrors historical entry rates.

FICO uses its global brand to capture share early, but localized rivals and regulatory compliance push upfront capex ~USD 50–150M per region; success is key to keeping its global credit-risk leadership.

- Target regions: India, Brazil, SEA

- New consumers 2019–2024: ~200M

- Potential revenue uplift by 2026: 10–15%

- Estimated capex per region: USD 50–150M

- Risk: local competitors, regulation

Decision Management Suite

The Decision Management Suite provides tools to design and deploy complex analytical apps and drives business process automation; FICO reported software revenue of $619m in 2024, with analytics and decisioning a core growth driver.

It holds a strong position in the enterprise market—FICO claims >40% share in decisioning for financial services and net promoter scores above 50—fueling high customer loyalty and recurring license revenue.

To keep star status, FICO is investing in UX and integrations: 2024 R&D spend was $126m and over 60 prebuilt connectors for cloud platforms were released to support large-scale deployments.

- Comprehensive decisioning tools

- Strong enterprise share (>40% in finance)

- High customer loyalty (NPS >50)

- 2024 revenue $619m; R&D $126m

- 60+ cloud connectors for integration

FICO: Fraud Fortress—$12.4B blocked, 2.5B accounts, cloud leader fueling growth

FICO stars: cloud decisioning (18.6B market 2025; FICO ~22% share), Falcon fraud (35% real-time payments share; protects 2.5B accounts; blocks $12.4B fraud annually), and Decision Management (2024 software rev $619M; >40% finance share; NPS >50); high R&D ($220M 2024) supports growth but requires 12–15% reinvestment to hold lead.

| Metric | Value |

|---|---|

| Cloud market 2025 | $18.6B |

| FICO cloud share | ~22% |

| Falcon accounts protected | 2.5B |

| Falcon blocked losses | $12.4B/yr |

| Real-time payments share | ~35% |

| Decisioning rev 2024 | $619M |

| R&D 2024 | $220M |

| Recommended reinvest | 12–15% of Falcon rev |

What is included in the product

Comprehensive BCG Matrix review detailing Stars, Cash Cows, Question Marks, and Dogs with strategic investment guidance.

One-page Fair Isaac BCG Matrix placing each product in a quadrant for clear portfolio decisions

Cash Cows

B2B Mortgage Credit Scoring

The FICO mortgage-credit-scoring business is a mature cash cow: FICO holds roughly 80%–90% share of US mortgage score use and enjoys high operating margins (mid-40s percent in 2024).

Mortgage growth is slow and cyclical, tied to interest rates and housing activity—US mortgage originations fell ~30% in 2023 vs 2021 peak—so revenue growth tracks macro cycles, not rapid adoption.

The segment generates large free cash flow with low incremental marketing/infrastructure spend, funding FICO’s cloud and AI R&D; mortgage-related EBITDA provided an estimated $400–600M annual cash cushion in 2024.

Consumer myFICO Services

The myFICO brand delivers direct-to-consumer credit monitoring and identity-theft protection in a mature US market; FICO reported Consumer segment revenue of $380M in 2024, driven by ~2.5M subscribers and high brand recognition.

Low customer-acquisition costs and strong retention produce steady subscription revenue and ~60–70% gross margins, making it a classic cash cow despite slower market growth vs. enterprise software.

Only incremental product updates and customer support are needed to sustain this reliable liquidity source for the parent company.

Credit Card Origination Scoring

FICO credit scores dominate card origination, holding roughly 60–70% market share among US issuers as of 2025, in a mature, low-growth lending market.

The segment is deeply embedded in the workflows of top banks—JPMorgan, Bank of America, Citigroup—driving high switching costs and stable renewals.

With core scoring developed, expenses center on maintenance, data security, and model governance; 2024 upkeep and security spend estimated at ~$120–150M.

Licensing and services generate predictable recurring revenue—FICO reported roughly $1.9B in 2024 analytics/licensing revenue—providing steady cash flow for planning.

Collections and Recovery Software

FICO Collections and Recovery is a mature, low-growth product that remains essential across cycles; FICO held roughly 30–40% share of global collections software in 2024, helping lenders lift recovery rates by 5–12 percentage points per program.

High client switching costs and 80–90% contract renewal rates create stable, profitable cash flows that fund riskier growth areas and R&D.

- Market share: ~30–40% (2024)

- Recovery lift: 5–12% per implementation

- Renewal rate: 80–90%

- Growth: low single digits annually

Auto Loan Risk Assessment

FICO’s auto-loan scoring underpins ~70% of US auto originations, using FICO scores to price millions of loans yearly; this mature, consolidated market gives FICO steady pricing power and low growth pressure as originations were ~16.5 million units in 2024, keeping share resilient.

Auto lending yields consistent revenue with low capex needs—segment margins exceed company average—and in 2024 cash flows funded high-growth bets across the FICO Platform, supporting analytics and SaaS expansion.

- High share: ~70% US auto origination reliance

- Mature market: 16.5M new vehicle sales (2024)

- Stable cash: low capex, above-average margins

- Funds growth: cash redeployed to SaaS/analytics

FICO’s High‑Margin Cash Cows Fuel SaaS/AI Growth: $1.9B Analytics, $400–600M Mortgage EBITDA

FICO’s Cash Cows: dominant mortgage and card scoring plus collections and auto scoring generate high-margin, recurring cash—mortgage EBITDA ~$400–600M (2024), analytics/licensing revenue $1.9B (2024), consumer revenue $380M (2024), retention 80–90%, gross margins 60–70%, upkeep ~$120–150M (2024); these low-growth, high-cash segments fund FICO’s SaaS/AI growth.

| Metric | 2024/2025 |

|---|---|

| Analytics/licensing rev | $1.9B (2024) |

| Mortgage EBITDA | $400–600M (2024) |

| Consumer rev | $380M (2024) |

| Gross margins | 60–70% |

| Upkeep/security spend | $120–150M (2024) |

What You’re Viewing Is Included

Fair Isaac BCG Matrix

The file you're previewing is the exact Fair Isaac BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This professional document, prepared by strategy experts, contains market-backed positioning, quadrant insights, and clear action recommendations for immediate use. Upon purchase you'll get the same editable, printable file delivered straight to your inbox—no surprises, no extra edits required.